Microelectromechanical System Production Equipment Market

Microelectromechanical System Production Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706513 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Microelectromechanical System Production Equipment Market Size

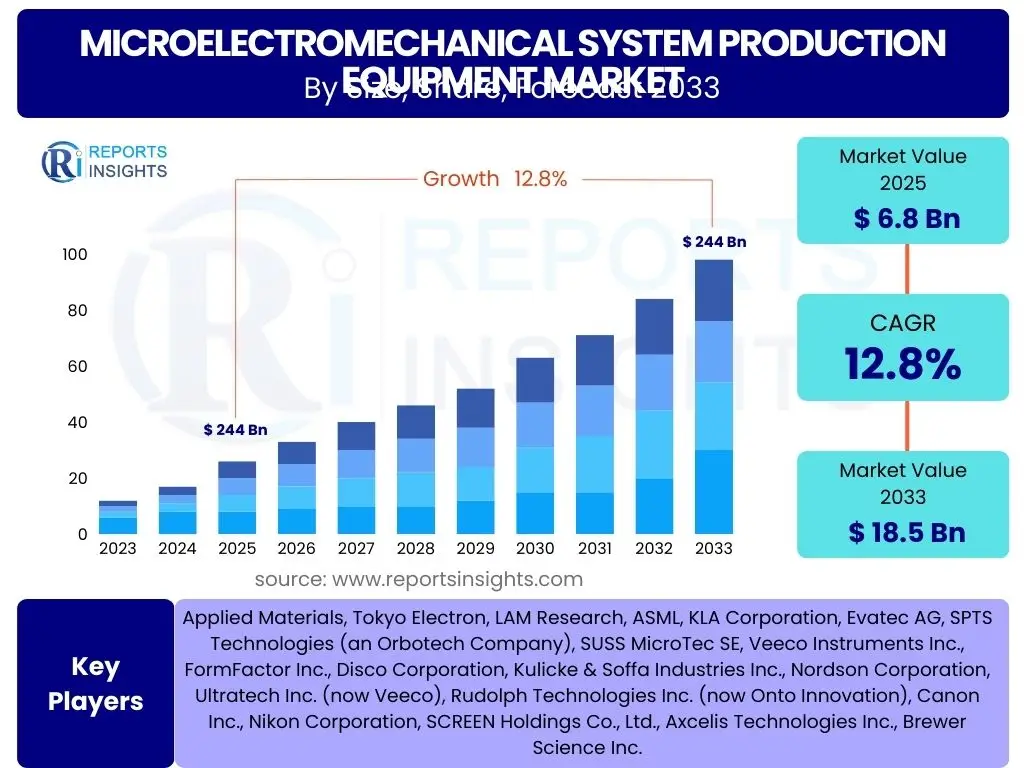

According to Reports Insights Consulting Pvt Ltd, The Microelectromechanical System Production Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 18.5 Billion by the end of the forecast period in 2033.

Key Microelectromechanical System Production Equipment Market Trends & Insights

The Microelectromechanical System (MEMS) production equipment market is witnessing significant transformation driven by the increasing integration of MEMS devices across diverse industries. There is a strong emphasis on achieving higher levels of precision, miniaturization, and functionality in MEMS components, which directly translates into a demand for more sophisticated and efficient production tools. This includes advancements in lithography, etching, deposition, and packaging technologies that can handle complex 3D structures and heterogeneous integration.

Furthermore, the market is profoundly influenced by the overarching trends of smart manufacturing and Industry 4.0, leading to greater automation and data-driven processes in MEMS fabs. The proliferation of IoT devices, the rapid expansion of 5G infrastructure, and the continuous innovation in the automotive and healthcare sectors are creating sustained demand for advanced MEMS sensors and actuators. This necessitates production equipment capable of higher throughput, improved yield, and adaptable manufacturing processes to meet varied application requirements and scale.

- Growing demand for miniaturized and high-performance MEMS devices across consumer electronics and automotive sectors.

- Increased investment in advanced packaging technologies for MEMS to enable multi-functional integration.

- Emergence of 5G technology driving demand for RF MEMS and timing devices.

- Adoption of artificial intelligence and machine learning for predictive maintenance and process optimization in manufacturing.

- Expansion of MEMS applications in healthcare, including point-of-care diagnostics and wearable medical devices.

- Focus on sustainable and energy-efficient MEMS production processes.

AI Impact Analysis on Microelectromechanical System Production Equipment

Artificial Intelligence (AI) is poised to significantly revolutionize the Microelectromechanical System (MEMS) production equipment market by enhancing various stages of the manufacturing process. Users are keenly interested in how AI can improve efficiency, reduce costs, and accelerate innovation. AI algorithms are increasingly being applied to optimize equipment performance, enabling predictive maintenance, fault detection, and real-time process control. This leads to higher uptime, reduced unscheduled downtimes, and more consistent product quality, which are critical in the high-precision MEMS fabrication environment.

Beyond operational efficiencies, AI is also transforming the design and development phases of MEMS devices and their corresponding production equipment. Machine learning models can analyze vast datasets from past manufacturing runs to identify optimal process parameters, leading to improved yield and faster ramp-up times for new product introductions. Furthermore, AI-driven automation systems are enhancing the precision and repeatability of complex fabrication steps, such as deposition, etching, and lithography, allowing for the creation of more intricate and reliable MEMS structures. The integration of AI facilitates adaptive manufacturing, where equipment can adjust to subtle variations in materials or environmental conditions, ensuring consistent output.

- Enhanced process control and optimization through real-time data analysis.

- Predictive maintenance for production equipment, minimizing downtime and increasing operational efficiency.

- Automated defect detection and classification, improving yield rates and quality control.

- Accelerated design and simulation of MEMS devices and manufacturing processes.

- Adaptive manufacturing systems capable of dynamic adjustments based on AI insights.

- Optimized resource allocation and energy consumption within fabrication facilities.

Key Takeaways Microelectromechanical System Production Equipment Market Size & Forecast

The Microelectromechanical System (MEMS) production equipment market is positioned for substantial growth, driven by the expanding adoption of MEMS across diverse and critical applications. Stakeholders are particularly interested in understanding the long-term potential and strategic implications of this market's upward trajectory. The forecast indicates a robust Compound Annual Growth Rate (CAGR) through 2033, signaling continuous technological advancements and increasing investment in manufacturing capabilities to meet the escalating demand for high-performance and miniaturized devices. This growth is underpinned by the pervasive trend of smart technology integration, from consumer gadgets to industrial automation and advanced medical devices.

A key takeaway from the market forecast is the pivotal role of innovation in sustaining this growth, especially in areas such as advanced materials processing, novel lithography techniques, and integrated packaging solutions. Furthermore, the market's expansion highlights opportunities for equipment manufacturers to diversify their offerings and cater to niche applications requiring specialized MEMS capabilities. The competitive landscape will likely intensify, prompting companies to focus on R&D, strategic partnerships, and regional expansion to capture market share and leverage emerging opportunities in Asia Pacific and other rapidly developing economies. The market's resilience is also attributed to its foundational role in enabling critical technologies that span multiple high-growth sectors.

- Robust market expansion fueled by pervasive demand for MEMS across various industries.

- Significant investment required in advanced manufacturing technologies to support next-generation MEMS.

- Growing importance of miniaturization, integration, and performance in MEMS device fabrication.

- Asia Pacific anticipated to remain a dominant region, driven by extensive manufacturing infrastructure and consumer electronics demand.

- Emphasis on automation, AI integration, and smart factory initiatives to enhance production efficiency and yield.

- Opportunities for specialization in equipment for emerging MEMS applications such as bio-MEMS and quantum sensing.

Microelectromechanical System Production Equipment Market Drivers Analysis

The Microelectromechanical System (MEMS) production equipment market is primarily propelled by the exponential growth in demand for MEMS devices across a multitude of applications. The proliferation of smart devices, connected cars, and advanced healthcare solutions directly translates into a higher requirement for sophisticated sensors and actuators, necessitating continuous investment in advanced manufacturing capabilities. This surging demand fosters innovation in equipment design, pushing for higher precision, greater throughput, and improved cost-efficiency in MEMS fabrication processes. The ongoing miniaturization trend across industries also acts as a significant driver, as it mandates highly specialized and precise equipment capable of manufacturing intricate structures at the micro and nano scales.

Additionally, the rapid advancements in fields such as 5G technology, artificial intelligence, and augmented/virtual reality are creating new avenues for MEMS applications, further boosting the market for production equipment. For instance, the deployment of 5G networks relies heavily on RF MEMS, while AI integration in edge computing requires high-performance MEMS sensors. Furthermore, governmental initiatives and private sector investments in semiconductor manufacturing capabilities, particularly in regions like Asia Pacific, contribute significantly to market expansion. These investments aim to establish robust domestic supply chains and enhance technological leadership, directly increasing the procurement of MEMS production equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of IoT Devices & Connected Technologies | +2.5% | Global, especially North America & APAC | 2025-2033 |

| Increasing Adoption in Automotive Electronics (ADAS, Infotainment) | +2.0% | Europe, North America, Japan, China | 2025-2033 |

| Growth in Healthcare & Medical Devices (Wearables, Diagnostics) | +1.8% | North America, Europe, APAC | 2026-2033 |

| Advancements in 5G Technology and Infrastructure Deployment | +1.5% | Global, particularly China, South Korea, USA | 2025-2030 |

| Miniaturization and Integration Trends Across Industries | +1.2% | Global | 2025-2033 |

Microelectromechanical System Production Equipment Market Restraints Analysis

Despite the robust growth prospects, the Microelectromechanical System (MEMS) production equipment market faces several significant restraints that could impede its trajectory. One primary concern is the substantial capital expenditure required for establishing and upgrading MEMS fabrication facilities. The high cost of advanced equipment, coupled with the need for specialized cleanroom environments and highly skilled personnel, creates a considerable barrier to entry for new players and can slow down capacity expansion for existing ones. This financial burden can particularly affect smaller enterprises or regions with limited investment capabilities.

Another major restraint involves the inherent technological complexity and the rapid obsolescence of manufacturing techniques in the MEMS sector. Developing and refining production processes for new MEMS designs often requires extensive research and development, leading to long lead times and high associated costs. Furthermore, the specialized nature of MEMS fabrication means that equipment is often highly customized, limiting its versatility and resale value. Geopolitical tensions and trade disputes also pose a significant risk, potentially disrupting global supply chains for critical components and raw materials, thereby impacting the production and delivery of MEMS equipment. The need for precise and intricate manufacturing also necessitates stringent quality control and high yield rates, which can be challenging to achieve and maintain, adding to operational complexities and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Operational Costs | -1.5% | Global | 2025-2033 |

| Technological Complexity and Rapid Obsolescence | -1.2% | Global | 2025-2030 |

| Supply Chain Vulnerabilities and Geopolitical Risks | -1.0% | Global | 2025-2028 |

| Skilled Labor Shortage and Talent Gap | -0.8% | North America, Europe, parts of APAC | 2025-2033 |

| Stringent Quality Requirements and Yield Challenges | -0.7% | Global | Ongoing |

Microelectromechanical System Production Equipment Market Opportunities Analysis

The Microelectromechanical System (MEMS) production equipment market is rich with opportunities stemming from emerging applications and technological convergence. The continuous drive towards smaller, more efficient, and interconnected devices presents significant avenues for growth. Innovations in areas such as advanced packaging, heterogeneous integration, and flexible electronics are creating new demands for specialized equipment capable of handling diverse materials and complex multi-chip assemblies. Furthermore, the advent of quantum technologies and the increasing sophistication of bio-MEMS and lab-on-a-chip devices are opening up entirely new, high-value market segments for precision manufacturing equipment. These advanced applications often require novel processing techniques, pushing the boundaries of current MEMS fabrication capabilities and prompting investment in next-generation tools.

Geographically, emerging economies, particularly in Asia Pacific, offer substantial growth opportunities. Countries like Vietnam, India, and Malaysia are increasingly becoming attractive locations for semiconductor and MEMS manufacturing due to favorable government policies, growing local demand, and lower operational costs. This shift presents equipment manufacturers with opportunities to expand their market presence and establish new distribution and service networks. Additionally, the increasing focus on sustainability and energy efficiency in manufacturing processes provides an opportunity for equipment suppliers to develop and market greener technologies that reduce energy consumption and material waste during MEMS production, appealing to environmentally conscious companies and regulations. Strategic partnerships and collaborations between equipment manufacturers, MEMS foundries, and research institutions can also accelerate innovation and market penetration for advanced solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Applications (e.g., Quantum Computing, AR/VR, Bio-MEMS) | +2.2% | Global, particularly North America, Europe, Japan | 2027-2033 |

| Growth in Advanced Packaging and Heterogeneous Integration | +1.8% | Global, especially APAC | 2025-2033 |

| Increased Investment in Emerging Manufacturing Regions (Southeast Asia) | +1.5% | Southeast Asia, India | 2026-2033 |

| Development of More Sustainable and Energy-Efficient Equipment | +1.0% | Global | 2025-2033 |

| Strategic Collaborations and Partnerships for R&D and Market Expansion | +0.9% | Global | Ongoing |

Microelectromechanical System Production Equipment Market Challenges Impact Analysis

The Microelectromechanical System (MEMS) production equipment market faces several notable challenges that require strategic navigation by industry players. One significant hurdle is the intense competition among equipment manufacturers. The market is dominated by a few large players, but niche specialists also exist, leading to continuous pressure on pricing, innovation cycles, and market share. This competitive environment necessitates substantial investment in research and development to maintain a technological edge, which can be particularly challenging for smaller firms or those with limited R&D budgets. Additionally, the highly specialized nature of MEMS production often requires bespoke solutions, making standardization difficult and increasing the complexity of equipment development and support.

Another critical challenge involves the cyclical nature of the broader semiconductor industry, which can lead to unpredictable demand for MEMS production equipment. Economic downturns or oversupply cycles can result in significant fluctuations in capital expenditure by MEMS manufacturers, impacting equipment sales and revenue streams. Furthermore, intellectual property (IP) protection and infringement issues are prevalent in this technologically advanced sector. Protecting proprietary designs and manufacturing processes, while also navigating existing patents, adds legal complexities and potential litigation risks. Finally, the rapid pace of technological advancements, while a driver, also poses a challenge in terms of keeping equipment up-to-date and compatible with evolving MEMS designs and materials, requiring continuous adaptation and investment from equipment suppliers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressures | -1.3% | Global | Ongoing |

| Cyclical Nature of the Semiconductor Industry | -1.0% | Global | Short to Medium Term |

| Complex IP Landscape and Potential Infringement Issues | -0.8% | Global | Ongoing |

| Rapid Technological Advancements Requiring Continuous R&D | -0.7% | Global | Ongoing |

| Adherence to Evolving Regulatory Standards and Environmental Compliance | -0.5% | Europe, North America, Japan | Medium to Long Term |

Microelectromechanical System Production Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Microelectromechanical System (MEMS) Production Equipment Market, covering historical data, current market dynamics, and future projections. It thoroughly examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report offers detailed insights into technological trends, competitive landscape, and strategic recommendations for stakeholders aiming to navigate and capitalize on the market's evolving environment. It serves as a vital resource for strategic decision-making, market entry strategies, and investment planning within the global MEMS production equipment industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 18.5 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, Tokyo Electron, LAM Research, ASML, KLA Corporation, Evatec AG, SPTS Technologies (an Orbotech Company), SUSS MicroTec SE, Veeco Instruments Inc., FormFactor Inc., Disco Corporation, Kulicke & Soffa Industries Inc., Nordson Corporation, Ultratech Inc. (now Veeco), Rudolph Technologies Inc. (now Onto Innovation), Canon Inc., Nikon Corporation, SCREEN Holdings Co., Ltd., Axcelis Technologies Inc., Brewer Science Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Microelectromechanical System (MEMS) production equipment market is comprehensively segmented to provide granular insights into its various facets, enabling a detailed understanding of market dynamics across different technologies, applications, and manufacturing scales. This segmentation highlights the diverse requirements within the MEMS industry, from the foundational equipment used in wafer fabrication to specialized tools for packaging and testing. Each segment plays a crucial role in the overall ecosystem, catering to specific manufacturing needs and technological advancements.

The segmentation by type reflects the broad categories of equipment utilized in MEMS manufacturing, such as deposition, etching, and lithography tools, which are fundamental to creating the intricate structures of MEMS devices. The application-based segmentation showcases the primary industries driving demand for MEMS, including high-growth sectors like consumer electronics, automotive, and healthcare, illustrating where the most significant investments in production capabilities are being made. Furthermore, segmentation by wafer size and manufacturing process provides critical insights into the evolving standards and techniques employed in MEMS fabrication, indicating shifts towards larger wafer sizes for economies of scale and advanced processes for complex device architectures. This detailed breakdown facilitates targeted market analysis and strategic planning for equipment manufacturers and MEMS producers alike.

- By Type: This segment includes various categories of equipment crucial for MEMS fabrication, such as Deposition Equipment (covering PVD, CVD, ALD, Sputtering), Etching Equipment (Dry Etching, Wet Etching), Lithography Equipment (Photolithography, Nanoimprint Lithography), Metrology and Inspection Equipment (Optical Metrology, Electrical Metrology, Particle Inspection), Wafer Bonding Equipment, Dicing Equipment, Packaging Equipment, and Other Production Equipment vital for the complete manufacturing flow.

- By Application: This segmentation focuses on the end-use industries driving the demand for MEMS devices, including Consumer Electronics (Smartphones, Wearables, Gaming Consoles, IoT Devices), Automotive (ADAS, TPMS, Engine Control, Infotainment), Healthcare (Diagnostic Devices, Medical Implants, Drug Delivery Systems), Industrial (Industrial Automation, Robotics, Process Control), Aerospace & Defense (Navigation Systems, Sensing, Communication), Telecommunications (5G Infrastructure, Optical Communication), and other niche applications.

- By Wafer Size: This segment analyzes equipment tailored for different wafer diameters, including 4-inch and Below, 6-inch, 8-inch, and 12-inch and Above, reflecting the industry's shift towards larger wafers for increased production efficiency and lower per-die costs.

- By Process: This category differentiates equipment based on the core manufacturing processes employed, such as Bulk Micromachining, Surface Micromachining, LIGA (Lithographie, Galvanoformung, Abformung), and DRIE (Deep Reactive Ion Etching), highlighting the diverse technological approaches in MEMS fabrication.

Regional Highlights

- Asia Pacific (APAC): APAC is anticipated to remain the dominant region in the Microelectromechanical System Production Equipment Market, primarily driven by the presence of a robust electronics manufacturing ecosystem in countries like China, Taiwan, South Korea, and Japan. These countries are major hubs for semiconductor fabrication, consumer electronics production, and automotive manufacturing, leading to significant investments in MEMS foundries and advanced production capabilities. The region also benefits from increasing government support for indigenous semiconductor industries and a large consumer base for smart devices, fueling continuous demand for MEMS equipment. India and Southeast Asian countries are also emerging as key growth markets due to rising manufacturing activities and technological adoption.

- North America: North America holds a significant share in the market, characterized by strong research and development activities, particularly in advanced MEMS technologies for aerospace, defense, medical, and high-performance computing applications. The presence of leading technology companies and a focus on innovation, coupled with substantial investments in next-generation manufacturing, drives demand for high-end and specialized MEMS production equipment. The region is at the forefront of AI integration in manufacturing and the development of cutting-edge sensor technologies.

- Europe: Europe represents a strong market for MEMS production equipment, with countries like Germany, France, and the Netherlands leading in industrial automation, automotive electronics, and specialized medical devices. The region's emphasis on precision engineering, Industry 4.0 initiatives, and a robust automotive sector contributes to sustained demand. Investments in smart factories and the drive towards energy-efficient manufacturing processes also foster growth in this region.

- Latin America, Middle East, and Africa (LAMEA): These regions are expected to witness gradual growth, driven by increasing industrialization, infrastructure development, and growing adoption of smart technologies. While currently smaller in market share compared to established regions, opportunities arise from expanding consumer electronics markets, nascent automotive industries, and increasing investments in healthcare and telecommunications infrastructure. The growth in these regions is often influenced by global economic trends and the establishment of local manufacturing capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Microelectromechanical System Production Equipment Market.- Applied Materials

- Tokyo Electron

- LAM Research

- ASML

- KLA Corporation

- Evatec AG

- SPTS Technologies (an Orbotech Company)

- SUSS MicroTec SE

- Veeco Instruments Inc.

- FormFactor Inc.

- Disco Corporation

- Kulicke & Soffa Industries Inc.

- Nordson Corporation

- Ultratech Inc. (now Veeco)

- Rudolph Technologies Inc. (now Onto Innovation)

- Canon Inc.

- Nikon Corporation

- SCREEN Holdings Co., Ltd.

- Axcelis Technologies Inc.

- Brewer Science Inc.

Frequently Asked Questions

What is Microelectromechanical System (MEMS) production equipment?

MEMS production equipment refers to the specialized machinery and tools used in the fabrication of microelectromechanical systems. This includes equipment for deposition, etching, lithography, metrology, inspection, wafer bonding, dicing, and packaging, all crucial for manufacturing miniature mechanical and electrical devices.

What are the primary applications of MEMS devices?

MEMS devices are widely applied across various sectors, including consumer electronics (smartphones, wearables), automotive (ADAS, sensors for engine control), healthcare (diagnostic devices, medical implants), industrial automation (sensors, actuators), and telecommunications (RF MEMS for 5G).

Which region dominates the Microelectromechanical System Production Equipment Market?

Asia Pacific (APAC) currently dominates the MEMS production equipment market. This is attributed to the presence of major semiconductor manufacturing hubs, extensive consumer electronics production, and significant investments in advanced fabrication capabilities across countries like China, Taiwan, South Korea, and Japan.

How is AI transforming MEMS manufacturing processes?

AI is transforming MEMS manufacturing by enabling enhanced process control, predictive maintenance for equipment, automated defect detection, and accelerated design cycles. It optimizes production efficiency, improves yield rates, and allows for more complex and precise device fabrication.

What are the key challenges facing the MEMS production equipment market?

Key challenges include high capital investment requirements, intense market competition, the rapid pace of technological obsolescence, the complex intellectual property landscape, and the inherent cyclical nature of the broader semiconductor industry, which can affect demand stability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted