Metrology Service Market

Metrology Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710425 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

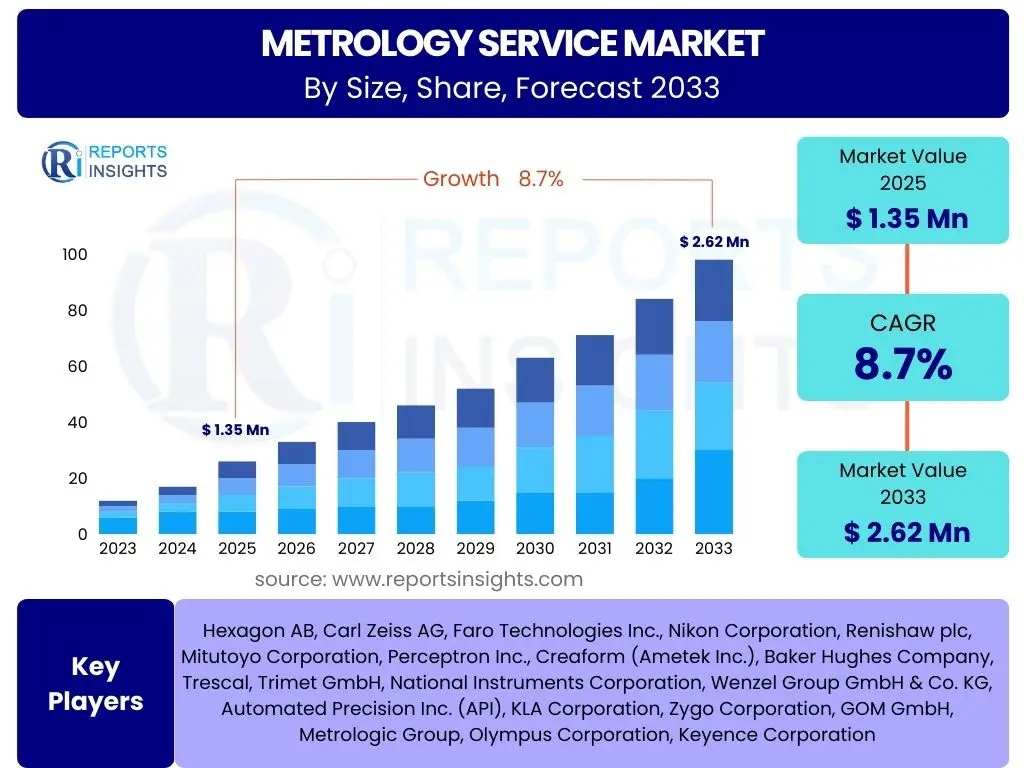

Metrology Service Market Size

According to Reports Insights Consulting Pvt Ltd, The Metrology Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.35 billion in 2025 and is projected to reach USD 2.62 billion by the end of the forecast period in 2033.

Key Metrology Service Market Trends & Insights

The metrology service market is currently undergoing a significant transformation, driven by the increasing demand for precision and accuracy across various industries. Common user inquiries often revolve around the emerging technologies and operational shifts influencing the sector. Key insights indicate a pronounced move towards automation, digitalization, and the integration of advanced data analytics, fundamentally reshaping how quality control and measurement processes are executed. This shift is not merely about adopting new tools but about establishing more efficient, reliable, and intelligent measurement ecosystems.

Industry 4.0 initiatives are a primary catalyst, fostering the adoption of smart metrology solutions that enable real-time monitoring and feedback loops in manufacturing. Users frequently ask about the practical implications of these trends on manufacturing efficiency and product quality. The market is witnessing a surge in demand for multi-sensor systems, non-contact measurement techniques, and portable metrology devices, which offer greater flexibility and applicability in diverse industrial settings. Furthermore, the emphasis on sustainability and resource optimization is prompting the development of metrology services that support leaner production processes and reduced waste, aligning with global environmental objectives.

- Integration of Industry 4.0 and smart manufacturing principles.

- Rising adoption of automated and intelligent metrology systems.

- Increased demand for multi-sensor and non-contact measurement technologies.

- Proliferation of data analytics and cloud-based metrology solutions.

- Growing emphasis on portable and in-line metrology for real-time quality control.

AI Impact Analysis on Metrology Service

User questions regarding the impact of Artificial Intelligence (AI) on metrology services frequently center on how AI can enhance precision, speed, and automation, while also addressing concerns about data integrity and the complexity of implementation. AI is fundamentally transforming metrology by enabling more sophisticated data analysis, predictive maintenance for metrology equipment, and advanced pattern recognition in inspection processes. This allows for the identification of subtle defects or deviations that might be overlooked by traditional methods, significantly improving quality assurance and reducing the likelihood of costly errors in production.

The application of AI in metrology extends to optimizing measurement strategies, automating repetitive inspection tasks, and facilitating faster decision-making through intelligent algorithms. This translates into enhanced operational efficiency and a reduction in human intervention, freeing up skilled personnel for more complex analytical tasks. While the benefits in terms of accuracy and speed are clear, users also express interest in the learning curve associated with AI tools, the ethical implications of autonomous decision-making in critical quality checks, and the robust cybersecurity measures required to protect sensitive manufacturing data. The integration of machine learning into metrology software enables systems to learn from historical data, adapt to new measurement challenges, and continually improve their performance over time, promising a future of increasingly intelligent and self-optimizing metrology solutions.

- Enhanced data processing and analysis for complex measurement data.

- Automation of inspection routines and quality control processes.

- Predictive maintenance for metrology equipment, improving uptime.

- Improved defect detection and classification through advanced pattern recognition.

- Optimization of measurement strategies and reduction of human error.

Key Takeaways Metrology Service Market Size & Forecast

Common user questions about the Metrology Service market size and forecast often aim to understand the underlying drivers of growth and the strategic implications for businesses operating within or relying on this sector. A key takeaway is the consistent and robust growth projected for the market, indicating an escalating global demand for high-precision measurement and quality assurance services. This growth is directly linked to the expansion of high-value manufacturing industries, the increasing complexity of products, and the stringent regulatory environments that necessitate rigorous quality control throughout the production lifecycle. The market's upward trajectory signifies a critical investment area for industries striving for operational excellence and competitive advantage.

Furthermore, the forecast underscores the importance of technological innovation in sustaining market expansion. Companies that invest in advanced metrology solutions, including those incorporating AI, automation, and digital integration, are poised to capture a larger share of this growing market. Another significant insight is the shift towards a service-oriented model, where businesses increasingly opt for specialized metrology services rather than significant capital investment in equipment. This trend offers flexibility and access to cutting-edge technology without the burden of ownership, making expertise a paramount offering. The sustained growth forecasts validate the metrology service market as a cornerstone for global manufacturing quality and innovation.

- Robust and consistent market growth expected through 2033, driven by precision demand.

- Technological advancements, particularly AI and automation, are crucial for market leadership.

- Shift towards outsourcing metrology services to leverage specialized expertise and technology.

- High-value manufacturing sectors are key growth engines for metrology service adoption.

- Market expansion is a direct reflection of increasing product complexity and stringent quality standards.

Metrology Service Market Drivers Analysis

The metrology service market's expansion is significantly propelled by several key drivers that reflect the evolving demands of modern manufacturing and industrial practices. A primary driver is the escalating need for high-precision and quality control across diverse industries, including automotive, aerospace, medical devices, and electronics. As products become more complex and manufacturing tolerances tighter, the reliance on advanced metrology services for verification and validation intensifies. This is further exacerbated by the global push for zero-defect manufacturing and adherence to international quality standards, compelling companies to invest in or outsource sophisticated measurement and inspection capabilities.

Another crucial driver is the rapid adoption of Industry 4.0 and smart manufacturing initiatives. These paradigms emphasize automation, data exchange, and real-time monitoring, creating a fertile ground for integrated metrology solutions. The demand for in-line and near-line metrology, predictive maintenance services, and digital metrology solutions that can integrate seamlessly into networked production environments is on the rise. Moreover, the growth of advanced manufacturing techniques such as additive manufacturing (3D printing) requires specialized metrology services to ensure the dimensional accuracy and structural integrity of complex geometries, presenting new opportunities for market players.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Precision Manufacturing | +2.1% | Global (esp. APAC, Europe, North America) | Long-term |

| Growing Adoption of Industry 4.0 & Automation | +1.8% | Global (esp. Developed Economies) | Medium to Long-term |

| Stringent Quality Standards and Regulatory Compliance | +1.5% | Global | Long-term |

| Expansion of Automotive, Aerospace, and Medical Industries | +1.3% | North America, Europe, APAC | Medium-term |

| Advancements in Additive Manufacturing | +1.1% | Global | Medium to Long-term |

Metrology Service Market Restraints Analysis

Despite the robust growth trajectory, the metrology service market faces several significant restraints that could potentially impede its full potential. One of the primary limitations is the high initial capital investment required for advanced metrology equipment and software. For small and medium-sized enterprises (SMEs), the cost of acquiring and maintaining state-of-the-art metrology systems can be prohibitive, often leading them to delay or forgo investments in cutting-edge solutions. This cost factor can also limit the rate of adoption of new technologies, particularly in developing regions where budget constraints are more prevalent.

Another key restraint is the scarcity of skilled professionals proficient in operating and interpreting complex metrology systems. Modern metrology involves sophisticated software, intricate calibration processes, and an understanding of advanced analytical techniques, requiring a highly specialized workforce. The shortage of such expertise can lead to inefficient utilization of advanced equipment, inaccurate measurements, and a general slowdown in the adoption of high-tech metrology services. Furthermore, economic uncertainties and geopolitical instability can lead to reduced industrial spending, impacting the demand for outsourced metrology services as companies prioritize essential operations over new investments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Cost of Ownership | -1.6% | Developing Economies, SMEs Globally | Short to Medium-term |

| Shortage of Skilled Metrology Professionals | -1.3% | Global | Medium-term |

| Complexity of Integrating Advanced Metrology Solutions | -1.0% | Global | Short-term |

| Economic Downturns and Industrial Slowdowns | -0.8% | Regional (e.g., Europe, North America) | Short-term |

| Lack of Standardization Across Measurement Platforms | -0.7% | Global | Long-term |

Metrology Service Market Opportunities Analysis

The metrology service market presents numerous promising opportunities for growth and innovation, driven by evolving industrial landscapes and technological advancements. One significant opportunity lies in the burgeoning adoption of metrology in emerging applications such as electric vehicle (EV) manufacturing, consumer electronics, and renewable energy sectors. These industries demand extremely tight tolerances and rigorous quality checks for new materials and complex components, creating a fertile ground for specialized metrology services that can cater to their unique requirements. The rapid pace of innovation in these fields necessitates adaptable and highly accurate measurement solutions, which metrology service providers are uniquely positioned to offer.

Furthermore, the increasing trend towards outsourcing non-core activities, particularly in quality control and inspection, offers a substantial opportunity for metrology service providers. Many companies prefer to leverage the expertise and advanced equipment of third-party service providers rather than investing heavily in their own metrology departments. This allows them to focus on their primary manufacturing competencies while ensuring access to cutting-edge metrology technology. The development and integration of cloud-based metrology solutions and data analytics platforms also represent a significant growth avenue, enabling remote monitoring, predictive analysis, and more efficient management of measurement data across distributed operations, thereby enhancing service delivery and value for customers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Application Areas (EVs, Consumer Electronics) | +1.9% | Global (esp. APAC, North America, Europe) | Medium to Long-term |

| Increased Outsourcing of Quality Control and Inspection | +1.7% | Global | Medium-term |

| Development of Cloud-based and Remote Metrology Solutions | +1.5% | Global | Medium-term |

| Strategic Partnerships and Collaborations | +1.2% | Global | Short to Medium-term |

| Growth in Advanced Materials and Nanotechnology | +1.0% | North America, Europe | Long-term |

Metrology Service Market Challenges Impact Analysis

The metrology service market, while dynamic and growing, faces several pertinent challenges that necessitate innovative solutions and strategic adaptations. One significant challenge is the rapid pace of technological obsolescence, where advanced metrology equipment and software can quickly become outdated due to continuous innovation in measurement science and manufacturing processes. This demands constant investment in research and development, as well as regular upgrades and training, to remain competitive and offer state-of-the-art services. Service providers must manage the delicate balance between adopting new technologies and ensuring a return on investment within a reasonable timeframe, particularly as customer expectations for accuracy and speed continue to rise.

Another critical challenge involves ensuring data security and interoperability across diverse metrology systems and client platforms. As metrology increasingly integrates with digital ecosystems and leverages cloud technologies, protecting sensitive intellectual property and proprietary manufacturing data becomes paramount. The lack of universal standards for data exchange can also hinder seamless integration and analysis, leading to inefficiencies and potential errors. Furthermore, managing the complexity of diverse client requirements, ranging from small batch, highly customized inspections to large-volume, automated quality control, presents operational and logistical hurdles for service providers. These challenges require robust, adaptable, and secure solutions to maintain market leadership and client trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.4% | Global | Short to Medium-term |

| Data Security and Interoperability Concerns | -1.2% | Global | Medium-term |

| Maintaining Accuracy Across Diverse Environments | -1.0% | Global | Long-term |

| Intellectual Property Protection for Proprietary Data | -0.9% | Global | Long-term |

| Intense Competition and Pricing Pressures | -0.8% | Global | Short to Medium-term |

Metrology Service Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Metrology Service Market, covering historical data, current market dynamics, and future projections. It delves into critical market attributes, identifies key trends, drivers, restraints, and opportunities, and offers a detailed segmentation analysis by various factors. The scope includes a thorough examination of the competitive landscape, profiling key industry players and assessing their strategic initiatives to provide stakeholders with actionable insights for informed decision-making and strategic planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.62 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hexagon AB, Carl Zeiss AG, Faro Technologies Inc., Nikon Corporation, Renishaw plc, Mitutoyo Corporation, Perceptron Inc., Creaform (Ametek Inc.), Baker Hughes Company, Trescal, Trimet GmbH, National Instruments Corporation, Wenzel Group GmbH & Co. KG, Automated Precision Inc. (API), KLA Corporation, Zygo Corporation, GOM GmbH, Metrologic Group, Olympus Corporation, Keyence Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metrology Service Market is meticulously segmented to provide a granular understanding of its diverse components and their contributions to the overall market landscape. This detailed segmentation allows for targeted analysis of growth drivers, challenges, and opportunities within specific market niches, enabling stakeholders to identify key areas for investment and strategic development. The market is primarily segmented by offering, type of metrology, application, and end-user industry, reflecting the varied needs and technological advancements across different sectors. This structure helps in dissecting the market to understand where demand is concentrated and how different technologies are being adopted.

- By Offering:

- Hardware: Comprises the physical metrology equipment.

- Software: Includes measurement software, data analysis tools, and control systems.

- Services: Encompasses calibration, inspection, consulting, and training services.

- By Type:

- Coordinate Measuring Machines (CMMs): Touch-probe and non-contact CMMs for precise 3D measurements.

- Optical Metrology: Laser scanners, photogrammetry, and structured light systems.

- 3D Scanning: Solutions for complex geometry capture and digitization.

- Vision Measuring Machines: Image-based measurement systems for automated inspection.

- Form Metrology: Devices for measuring surface roughness, roundness, and contours.

- Automated Optical Inspection (AOI): For high-speed inspection in electronics manufacturing.

- Others: Include advanced non-destructive testing (NDT) metrology and specialized systems.

- By Application:

- Quality Control & Inspection: The largest segment, ensuring product compliance and defect detection.

- Reverse Engineering: For recreating designs from existing physical parts.

- Assembly & Alignment: Ensuring precise fitting of components.

- Tooling & Fixture Inspection: Verifying the accuracy of manufacturing tools.

- Part Sorting: Automated sorting based on dimensional criteria.

- Prototyping & Design: For validation of initial designs.

- Others: Diverse niche applications across industries.

- By End-User Industry:

- Automotive: For components, body-in-white, and engine parts.

- Aerospace & Defense: High-precision parts for aircraft, rockets, and military equipment.

- General Manufacturing: Diverse products requiring quality assurance.

- Electronics & Semiconductors: Micro-components and PCB inspection.

- Medical & Life Sciences: Implants, prosthetics, and pharmaceutical devices.

- Heavy Machinery: Large-scale components for industrial equipment.

- Energy & Power: Turbines, solar panels, and wind components.

- Construction: Structural analysis and infrastructure projects.

- Others: Including research & development, education, and specialized manufacturing.

Regional Highlights

The global Metrology Service Market exhibits distinct regional dynamics, influenced by industrialization levels, technological adoption rates, and regulatory environments. Each major geographical segment contributes uniquely to the market's overall growth and innovation landscape, showcasing varying degrees of maturity and potential.

- North America: This region is a leading adopter of advanced metrology services, driven by robust aerospace & defense, automotive, and medical device manufacturing sectors. Significant investments in research and development, coupled with a strong emphasis on automation and Industry 4.0, position North America as a hub for metrology innovation. The presence of key market players and a high demand for precision engineering further fuels market growth.

- Europe: Characterized by a mature manufacturing base, particularly in Germany's automotive and machinery industries, Europe demonstrates a high demand for sophisticated metrology solutions. The region is at the forefront of Industry 4.0 implementation and boasts stringent quality standards, driving the need for advanced inspection and quality control services. Emphasis on sustainable manufacturing and digitalization also contributes to strong market expansion.

- Asia Pacific (APAC): APAC represents the fastest-growing market for metrology services, primarily due to rapid industrialization, expanding manufacturing capabilities, and increasing foreign direct investment in countries like China, India, Japan, and South Korea. The region's vast automotive, electronics, and general manufacturing sectors are continuously upgrading their quality control processes, leading to significant adoption of both traditional and advanced metrology services. The drive for export-oriented growth and competitive pricing also necessitates high-quality production.

- Latin America: This region is an emerging market for metrology services, with growth primarily driven by the expansion of the automotive and general manufacturing industries in countries like Brazil and Mexico. While adoption of advanced technologies is increasing, the market is still developing, offering considerable opportunities for international service providers.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, supported by infrastructure development, diversification of economies away from oil, and investments in manufacturing and energy sectors. The demand for metrology services is primarily concentrated in sectors such as oil & gas, construction, and nascent automotive industries, with potential for significant expansion as industrialization progresses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metrology Service Market.- Hexagon AB

- Carl Zeiss AG

- Faro Technologies Inc.

- Nikon Corporation

- Renishaw plc

- Mitutoyo Corporation

- Perceptron Inc.

- Creaform (Ametek Inc.)

- Baker Hughes Company

- Trescal

- Trimet GmbH

- National Instruments Corporation

- Wenzel Group GmbH & Co. KG

- Automated Precision Inc. (API)

- KLA Corporation

- Zygo Corporation

- GOM GmbH

- Metrologic Group

- Olympus Corporation

- Keyence Corporation

Frequently Asked Questions

What is the projected growth rate for the Metrology Service Market?

The Metrology Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, driven by increasing demand for precision and quality control across industries.

How is Industry 4.0 influencing the Metrology Service Market?

Industry 4.0 is a major driver, promoting the integration of automated, digital, and data-driven metrology solutions for real-time monitoring, enhanced efficiency, and predictive maintenance in smart manufacturing environments.

What role does AI play in modern Metrology Services?

AI enhances metrology by enabling advanced data analysis, automating inspection processes, improving defect detection through pattern recognition, and optimizing measurement strategies, leading to greater accuracy and reduced human error.

What are the main challenges faced by the Metrology Service Market?

Key challenges include rapid technological obsolescence, high initial investment costs for advanced equipment, a shortage of skilled professionals, and concerns related to data security and interoperability across diverse systems.

Which industries are the primary consumers of Metrology Services?

The primary end-user industries include automotive, aerospace & defense, general manufacturing, electronics & semiconductors, and medical & life sciences, all requiring stringent quality control and high-precision measurement.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted