Metallic Glass Market

Metallic Glass Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705785 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

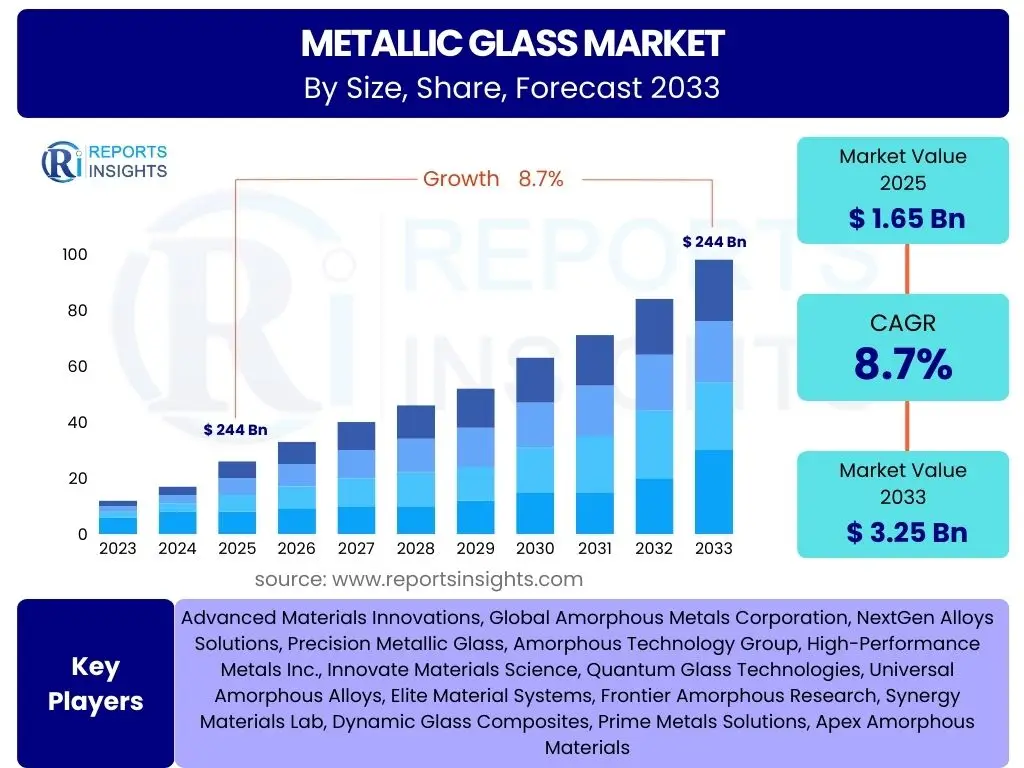

Metallic Glass Market Size

According to Reports Insights Consulting Pvt Ltd, The Metallic Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.65 Billion in 2025 and is projected to reach USD 3.25 Billion by the end of the forecast period in 2033.

Key Metallic Glass Market Trends & Insights

The Metallic Glass market is undergoing significant transformation, driven by an increasing demand for materials possessing superior mechanical, magnetic, and corrosive properties that traditional crystalline alloys cannot match. A key trend involves the continuous innovation in alloy compositions, focusing on developing new metallic glass formulations with enhanced ductility and workability, addressing the historical challenge of inherent brittleness. This research and development push is opening doors to applications previously considered unfeasible, particularly in structural components where high strength-to-weight ratios are critical.

Furthermore, the market is witnessing a strong push towards miniaturization across various industries, especially in consumer electronics and medical devices. Metallic glass, with its high elastic limit, excellent corrosion resistance, and unique processing capabilities, is ideally suited for these compact and high-performance applications. The integration of advanced manufacturing techniques, such as additive manufacturing and precision casting, is also gaining traction, enabling the production of complex metallic glass geometries with improved efficiency and reduced material waste. This evolution in manufacturing processes is poised to further accelerate the market's growth and broaden its industrial adoption.

- Increasing focus on developing ductile metallic glass alloys.

- Rising demand from miniaturized electronic components and medical devices.

- Advancements in additive manufacturing technologies for complex geometries.

- Growing adoption in high-performance sports equipment and luxury goods.

- Shift towards energy-efficient magnetic materials for power applications.

AI Impact Analysis on Metallic Glass

Artificial Intelligence (AI) is set to revolutionize the Metallic Glass market by significantly accelerating the discovery, design, and optimization of novel amorphous alloys. Users frequently inquire about how AI can shorten the lengthy R&D cycles characteristic of materials science. AI's capabilities in predictive modeling and data analytics allow researchers to virtually screen countless alloy compositions and processing parameters, identifying promising candidates with desired properties much faster than traditional experimental methods. This computational approach not only reduces time and cost but also enables the exploration of vast compositional spaces that would be impractical otherwise, leading to the development of next-generation metallic glasses with tailored characteristics.

Beyond material discovery, AI's impact extends into manufacturing and quality control, addressing common concerns regarding production scalability and consistency. AI-powered algorithms can optimize production parameters in real-time, such as cooling rates during solidification or annealing temperatures, to minimize defects and ensure consistent amorphous structures. Furthermore, machine learning models can analyze sensor data from manufacturing lines to predict potential failures or deviations in material properties, enabling proactive adjustments and enhancing overall yield. This integration of AI promises to make metallic glass production more efficient, cost-effective, and suitable for industrial scale, addressing a critical bottleneck in its broader commercial adoption.

- Accelerated material discovery and alloy design through predictive modeling.

- Optimization of manufacturing processes for improved efficiency and yield.

- Enhanced quality control and defect prediction in production.

- Simulation of material properties under various conditions.

- Enabling autonomous materials research and development.

Key Takeaways Metallic Glass Market Size & Forecast

The Metallic Glass market is poised for robust expansion, driven by its unparalleled material properties and burgeoning applications across high-tech industries. The projected Compound Annual Growth Rate (CAGR) signifies a strong underlying demand for advanced materials capable of offering superior performance over conventional metals. This growth trajectory indicates a market transition from niche applications to more widespread industrial adoption, fueled by ongoing research and development efforts to overcome existing limitations such as brittleness and manufacturing scalability. The forecast suggests that metallic glass will increasingly become a material of choice where high strength, corrosion resistance, and specific magnetic properties are paramount.

Furthermore, the significant increase in market value from 2025 to 2033 reflects the confidence in commercialization of new metallic glass alloys and the expansion into diverse end-use sectors. Key drivers include miniaturization trends in electronics, the need for lightweight components in automotive and aerospace, and advanced medical device requirements. As manufacturing processes become more refined and cost-effective, the market is expected to capture a larger share in these demanding applications. The strategic investments in R&D and the potential for breakthrough applications are central to sustaining this impressive growth, making metallic glass a critical material for future technological advancements.

- Projected strong growth (8.7% CAGR) indicating increasing adoption.

- Significant market value increase from USD 1.65 Billion to USD 3.25 Billion.

- Demand driven by superior mechanical, magnetic, and corrosive properties.

- Expansion into high-tech applications like electronics, automotive, and medical.

- Technological advancements addressing production and property limitations.

Metallic Glass Market Drivers Analysis

The unique combination of properties inherent to metallic glasses—including high strength, superior hardness, excellent corrosion resistance, and distinct magnetic behaviors—is a primary catalyst for market growth. Unlike traditional crystalline metals, the amorphous atomic structure of metallic glasses eliminates dislocations and grain boundaries, leading to enhanced mechanical properties. This makes them ideal for applications requiring durability and resilience in extreme conditions, such as those found in aerospace, automotive, and industrial machinery components. The demand for materials that can withstand high stress, wear, and corrosive environments without degradation is continuously rising, positioning metallic glass as a preferred solution.

Moreover, the ongoing trend of miniaturization across various industries, particularly in consumer electronics and medical devices, significantly drives the adoption of metallic glass. Its ability to be precisely molded into complex shapes with high surface finish, coupled with excellent spring-back properties and magnetic shielding capabilities, makes it invaluable for compact and high-performance components. From smartphone casings and connectors to surgical instruments and implants, the material's unique attributes enable innovative product designs and enhanced functionality. As industries continue to push the boundaries of device size and performance, the demand for metallic glass is expected to accelerate further.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization & High-Performance Electronics | +2.1% | Asia Pacific, North America, Europe | Short to Medium Term (2025-2029) |

| Demand for Lightweight Automotive Components | +1.8% | Europe, North America, Asia Pacific | Medium Term (2027-2033) |

| Advancements in Medical Devices | +1.5% | North America, Europe | Short to Medium Term (2025-2030) |

| Renewable Energy and Smart Grid Applications | +1.3% | Europe, Asia Pacific | Medium to Long Term (2028-2033) |

| Aerospace and Defense Applications | +1.0% | North America, Europe | Long Term (2029-2033) |

Metallic Glass Market Restraints Analysis

Despite the exceptional properties of metallic glasses, their high production costs and complex manufacturing processes pose significant restraints on market expansion. The specialized techniques required for rapid cooling rates, often involving bulk metallic glass (BMG) formation, can be energy-intensive and require precise control, leading to elevated manufacturing expenses compared to conventional metals. Furthermore, the limited availability of specialized equipment and expertise for processing these materials adds to the overall cost, making metallic glass less competitive for large-volume, price-sensitive applications. Until more economical and scalable production methods are developed, cost will remain a barrier to wider adoption, particularly in mass-market industries.

Another major restraint is the inherent brittleness of most metallic glasses, especially when compared to ductile crystalline metals. While they possess very high strength and elastic limits, their lack of macroscopic plasticity means they are prone to catastrophic failure under tensile stress or impact without significant deformation. This characteristic limits their application in structural components where high toughness and ductility are critical safety requirements. Overcoming this brittleness without compromising other desirable properties remains a significant challenge for researchers and material scientists, impacting the material's suitability for a broader range of engineering applications and slowing its market penetration into sectors demanding high damage tolerance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs & Complex Manufacturing | -2.5% | Global | Short to Medium Term (2025-2030) |

| Limited Scalability for Mass Production | -1.9% | Global | Short to Medium Term (2025-2030) |

| Inherent Brittleness and Processing Difficulties | -1.7% | Global | Short to Medium Term (2025-2030) |

| Competition from Conventional Materials | -1.2% | Global | Short to Medium Term (2025-2029) |

Metallic Glass Market Opportunities Analysis

The emergence of additive manufacturing, specifically 3D printing technologies such as selective laser melting (SLM) and electron beam melting (EBM), presents a transformative opportunity for the metallic glass market. These technologies enable the fabrication of complex metallic glass components with intricate geometries and tailored internal structures that are impossible to achieve through traditional casting or machining. This capability unlocks new design freedoms for engineers, allowing for optimized part performance, reduced material waste, and rapid prototyping. As additive manufacturing technologies mature and become more accessible, they can significantly lower the barriers to producing custom metallic glass parts for niche, high-value applications, thereby expanding market reach.

Furthermore, continuous research and development efforts aimed at discovering new metallic glass alloys and expanding their application portfolio offer substantial growth opportunities. Scientists are actively exploring new compositional systems beyond traditional zirconium-based alloys, seeking to develop metallic glasses with improved ductility, lower cost, and enhanced performance tailored for specific industry needs. The potential for metallic glass to displace conventional materials in currently underserved or emerging applications—such as specialized tools, high-efficiency transformers, or advanced biomedical implants—remains vast. Strategic partnerships between research institutions, material suppliers, and end-use industries can accelerate the commercialization of these new alloys and foster innovative applications, driving significant market expansion in the long term.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Additive Manufacturing (3D Printing) Adoption | +2.3% | Global, particularly North America, Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Development of New Alloys & Applications | +2.0% | Global | Long Term (2029-2033) |

| Cost Reduction through Advanced Manufacturing Techniques | +1.6% | Global | Medium Term (2026-2031) |

| Untapped Potential in Consumer Goods & Luxury Sector | +1.1% | Asia Pacific, North America, Europe | Short to Medium Term (2025-2029) |

Metallic Glass Market Challenges Impact Analysis

One of the enduring challenges for the metallic glass market is overcoming the perception and practical limitations of its inherent brittleness for broader structural applications. While metallic glasses boast impressive strength and elasticity, their lack of ductility under tension or impact makes them less suitable for large-scale structural components where energy absorption and damage tolerance are critical design parameters. Engineers often prefer materials that exhibit significant plastic deformation before failure, allowing for predictable behavior and safety margins. Developing metallic glass compositions or composites that retain their amorphous advantages while demonstrating improved toughness and resistance to brittle fracture is a key research area, but successful widespread implementation remains a significant hurdle requiring substantial material science breakthroughs.

Furthermore, establishing cost-effective and truly scalable production methods for metallic glass, particularly for bulk metallic glass parts, presents a significant challenge. Current fabrication processes often involve rapid cooling rates to prevent crystallization, which can limit the size and complexity of the parts that can be produced. Achieving industrial-scale output at competitive prices requires significant investment in advanced manufacturing infrastructure and continuous innovation in processing techniques. The absence of widespread manufacturing infrastructure and standardized production protocols also contributes to higher unit costs and longer lead times, impeding the material's ability to compete with established conventional metals in high-volume markets. Addressing these production challenges is crucial for metallic glass to move beyond niche applications and realize its full commercial potential.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Overcoming Brittleness for Broader Structural Applications | -2.0% | Global | Long Term (2028-2033) |

| Developing Cost-Effective & Scalable Production Methods | -1.8% | Global | Medium to Long Term (2027-2033) |

| Limited Public Awareness and Industry Adoption | -1.5% | Global | Short to Medium Term (2025-2030) |

| Intellectual Property and Commercialization Barriers | -1.0% | Global | Medium Term (2026-2031) |

Metallic Glass Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Metallic Glass Market, covering historical trends, current market dynamics, and future growth projections. The study encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It aims to offer strategic insights for stakeholders, aiding in informed decision-making and competitive positioning within the evolving metallic glass industry. The report highlights emerging trends, the impact of technological advancements, and the competitive landscape to provide a holistic view of the market's potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.65 Billion |

| Market Forecast in 2033 | USD 3.25 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Materials Innovations, Global Amorphous Metals Corporation, NextGen Alloys Solutions, Precision Metallic Glass, Amorphous Technology Group, High-Performance Metals Inc., Innovate Materials Science, Quantum Glass Technologies, Universal Amorphous Alloys, Elite Material Systems, Frontier Amorphous Research, Synergy Materials Lab, Dynamic Glass Composites, Prime Metals Solutions, Apex Amorphous Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metallic Glass market is intricately segmented to provide a detailed understanding of its diverse applications and material compositions. This segmentation allows for precise market analysis, identifying key growth areas and niche opportunities across various end-use industries and material types. The comprehensive breakdown highlights the versatility of metallic glass, demonstrating its suitability for distinct functional requirements, from high-strength components to specific magnetic applications.

- By Type:

- Zirconium-based Metallic Glass

- Iron-based Metallic Glass

- Copper-based Metallic Glass

- Magnesium-based Metallic Glass

- Others (e.g., Titanium-based, Nickel-based)

- By Application:

- Consumer Electronics

- Automotive

- Medical & Healthcare

- Aerospace & Defense

- Sports & Leisure

- Industrial Components

- Others (e.g., Energy, Luxury Goods)

- By End-Use Industry:

- Manufacturing & Machinery

- Telecommunications

- Energy & Power

- Building & Construction

- Biotechnology

- Other Industries

Regional Highlights

- North America: This region is a significant hub for research and development in advanced materials, including metallic glass. High adoption rates in aerospace, defense, and medical device industries drive market growth. The presence of key R&D institutions and a strong innovation ecosystem contribute to its leading position.

- Europe: Europe stands out due to its robust automotive sector and stringent regulations for energy efficiency and lightweighting, which naturally favor the adoption of metallic glass. Countries like Germany and France are pioneers in advanced manufacturing and material science research, fostering market expansion.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily driven by the massive consumer electronics manufacturing base, rapid industrialization, and increasing investments in R&D in countries like China, Japan, and South Korea. The demand for miniaturized and high-performance components significantly fuels the market here.

- Latin America: While currently a smaller market, Latin America shows emerging potential with increasing industrialization and investment in sectors like automotive and infrastructure, which could slowly adopt metallic glass for specific applications.

- Middle East and Africa (MEA): The MEA region is expected to witness gradual growth, driven by diversification efforts in industrial sectors, increasing infrastructure development, and nascent interest in advanced materials for energy and defense applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metallic Glass Market.

- Advanced Materials Innovations

- Global Amorphous Metals Corporation

- NextGen Alloys Solutions

- Precision Metallic Glass

- Amorphous Technology Group

- High-Performance Metals Inc.

- Innovate Materials Science

- Quantum Glass Technologies

- Universal Amorphous Alloys

- Elite Material Systems

- Frontier Amorphous Research

- Synergy Materials Lab

- Dynamic Glass Composites

- Prime Metals Solutions

- Apex Amorphous Materials

Frequently Asked Questions

What is metallic glass?

Metallic glass, also known as amorphous metal, is a class of metallic alloys with a disordered atomic structure, similar to glass, rather than the crystalline structure found in traditional metals. This unique atomic arrangement imparts exceptional properties such as high strength, elasticity, hardness, corrosion resistance, and specific magnetic characteristics.

What are the primary applications of metallic glass?

Metallic glass finds applications across diverse sectors including consumer electronics (e.g., smartphone components, connectors), automotive (e.g., lightweight structural parts, gears), medical & healthcare (e.g., surgical instruments, implants), aerospace & defense, sports & leisure equipment, and industrial components due to its superior mechanical and magnetic properties.

How does metallic glass differ from traditional metals?

Unlike traditional metals which have an ordered, crystalline atomic structure, metallic glass possesses an amorphous, disordered atomic arrangement. This lack of grain boundaries and dislocations gives metallic glass superior properties like higher elastic limit, increased hardness, excellent corrosion resistance, and unique magnetic behaviors not typically found in crystalline metals.

What are the major challenges in the metallic glass market?

Key challenges in the metallic glass market include high production costs and complex manufacturing processes, limited scalability for mass production, and the inherent brittleness of most metallic glass alloys, which restricts their use in applications requiring high ductility and toughness. Overcoming these limitations is crucial for broader market adoption.

What is the growth outlook for the metallic glass market?

The metallic glass market is projected for significant growth, with a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. This growth is driven by increasing demand from high-tech industries, continuous advancements in material science and manufacturing techniques, and the unique performance benefits metallic glass offers over conventional materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted