Metal Packaging Coating Market

Metal Packaging Coating Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702596 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

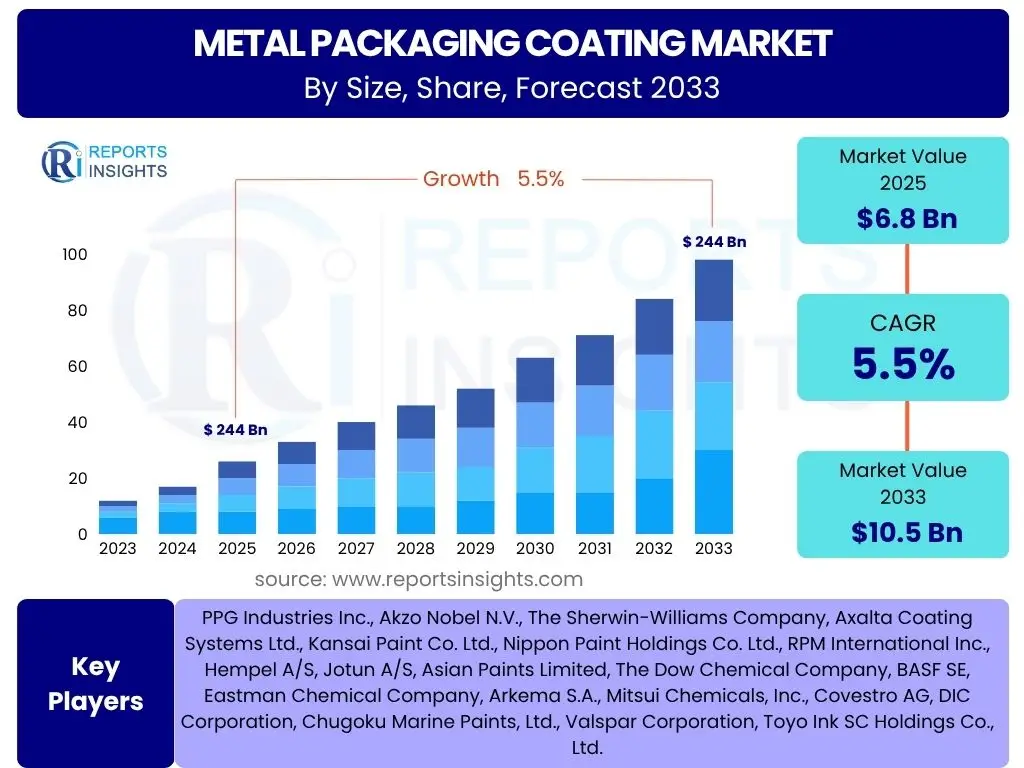

Metal Packaging Coating Market Size

According to Reports Insights Consulting Pvt Ltd, The Metal Packaging Coating Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2033.

Key Metal Packaging Coating Market Trends & Insights

The Metal Packaging Coating market is currently witnessing a significant transformation driven by a confluence of evolving consumer preferences, stringent regulatory frameworks, and technological advancements. A primary trend involves the increasing demand for sustainable and eco-friendly coating solutions, as brand owners and consumers alike prioritize recyclable and low-VOC (Volatile Organic Compound) options. This shift is propelling research and development into water-based, UV-cured, and plant-based coatings. Furthermore, the market is observing a push towards high-performance coatings that offer enhanced barrier properties against corrosion, abrasion, and product interaction, ensuring extended shelf life and product integrity. The rise of digitalization and smart packaging initiatives also influences coating formulations, with growing interest in coatings that support traceability and interactive consumer experiences.

Another prominent trend is the customization and specialization of coatings for specific applications. For instance, coatings for beverage cans are being optimized for taste neutrality and durability, while those for food cans are focusing on preventing chemical migration and maintaining food safety standards. The expansion of e-commerce has also increased the need for robust and protective coatings that can withstand the rigors of transit. Geographical market dynamics indicate a strong growth trajectory in emerging economies, particularly in Asia Pacific, driven by urbanization, rising disposable incomes, and the expansion of the packaged food and beverage sector. Developed markets, conversely, are focusing on premiumization and advanced functional coatings.

- Increasing demand for sustainable and environmentally friendly coating solutions (e.g., water-based, UV-cured, bio-based coatings).

- Focus on enhanced barrier properties for extended shelf life and product integrity.

- Development of specialized coatings for specific applications (e.g., taste-neutral beverage can coatings, BPA-non-intent food can coatings).

- Adoption of smart coating technologies for improved traceability and consumer engagement.

- Growing emphasis on regulatory compliance and food safety standards.

- Innovation in anti-corrosion and anti-abrasion coatings for industrial packaging.

- Shift towards lightweight and high-strength metal substrates necessitating compatible coating advancements.

- Customization of coating solutions based on regional climate and consumer preferences.

AI Impact Analysis on Metal Packaging Coating

Artificial intelligence (AI) is poised to significantly transform the Metal Packaging Coating market by optimizing various stages of the coating process, from research and development to quality control and supply chain management. Users anticipate AI will revolutionize material science by accelerating the discovery and formulation of novel coating materials with desired properties, such as enhanced durability, corrosion resistance, and sustainability profiles. AI-powered algorithms can analyze vast datasets of chemical compositions and performance characteristics, predicting optimal formulations and reducing the time and cost associated with traditional trial-and-error methods. This can lead to faster market introduction of innovative and compliant coating solutions.

Furthermore, AI is expected to enhance manufacturing efficiency and quality assurance within coating application processes. Predictive maintenance, enabled by AI, can monitor coating equipment in real-time, anticipate potential failures, and schedule maintenance proactively, thereby minimizing downtime and maximizing operational uptime. AI-driven vision systems and sensors can provide continuous, precise quality control, detecting defects or inconsistencies in coating thickness and adhesion with unparalleled accuracy, far surpassing human capabilities. This leads to reduced waste, improved product consistency, and higher overall production yields. Users are also keen on AI's potential to optimize supply chain logistics, predict demand fluctuations, and manage inventory more efficiently, contributing to cost savings and improved responsiveness across the entire value chain.

- Accelerated R&D and material discovery for novel coating formulations through AI-driven data analysis.

- Enhanced quality control and defect detection using AI-powered vision systems in coating lines.

- Optimized manufacturing processes and reduced downtime via AI-driven predictive maintenance.

- Improved supply chain efficiency and demand forecasting through AI algorithms.

- Personalization and customization of coating solutions based on specific application requirements and performance data.

- Reduced material waste and energy consumption through AI-optimized application parameters.

- Simulation and modeling of coating performance under various conditions, enabling faster product development.

- Development of smart coatings with embedded AI for real-time monitoring of package integrity.

Key Takeaways Metal Packaging Coating Market Size & Forecast

The Metal Packaging Coating Market is on a robust growth trajectory, driven by the expanding global demand for packaged goods, particularly in the food and beverage sectors. A key takeaway from the market forecast is the strong impetus towards sustainable and high-performance coatings, reflecting both regulatory pressures and evolving consumer preferences for eco-friendly products. The market's resilience is underscored by continuous innovation aimed at enhancing product safety, extending shelf life, and ensuring compliance with stringent global standards, particularly concerning Bisphenol A (BPA) and other potentially harmful chemicals. Emerging economies, notably in Asia Pacific, are anticipated to be pivotal growth engines, fueled by rapid urbanization, increasing disposable incomes, and the consequent surge in consumption of packaged commodities.

Moreover, the forecast highlights a significant shift towards specialized and customized coating solutions tailored to diverse applications, ranging from highly sensitive food products to robust industrial containers. Manufacturers are increasingly investing in research and development to create coatings that offer superior barrier properties, improved adhesion, and aesthetic appeal, while also being cost-effective. The integration of advanced technologies, including AI and automation, is expected to further streamline production processes, enhance quality, and foster greater efficiency across the value chain. This dynamic landscape necessitates a strategic focus on innovation, regulatory foresight, and market diversification to capitalize on the sustained growth projected for the metal packaging coating industry.

- Sustainable and high-performance coatings are critical for future market growth.

- Food and beverage packaging remains a dominant application segment, driving innovation in safe and compliant coatings.

- Asia Pacific is projected as the fastest-growing region due to increasing consumption and industrialization.

- Stringent regulations, particularly concerning BPA-non-intent coatings, heavily influence product development.

- Technological advancements, including AI integration, are enhancing manufacturing efficiency and coating properties.

- Customization and specialization of coatings for diverse end-use applications are a key trend.

- The market is characterized by a balance between cost-effectiveness and superior functional properties.

- Investment in R&D for advanced barrier and anti-corrosion solutions is essential for market players.

Metal Packaging Coating Market Drivers Analysis

The Metal Packaging Coating market is primarily propelled by the burgeoning demand for packaged goods across diverse industries, particularly food and beverages. The global population growth, coupled with increasing urbanization and disposable incomes in developing economies, has led to a significant surge in the consumption of canned foods, beverages, and aerosols. Consumers' preference for convenience, extended shelf life, and product safety further fuels the need for high-quality metal packaging coatings that offer protection against corrosion, spoilage, and chemical migration. Furthermore, the growing emphasis on sustainability in packaging is driving demand for recyclable metal containers, which in turn necessitates advanced coating solutions that are environmentally compliant and do not impede the recycling process.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for Packaged Food & Beverages | +1.8% | Global, particularly Asia Pacific & Latin America | 2025-2033 |

| Increasing Focus on Sustainable Packaging Solutions | +1.5% | North America, Europe, Developed Asia Pacific | 2025-2033 |

| Growing Awareness of Food Safety and Product Integrity | +1.2% | Global, with stringent focus in Developed Markets | 2025-2033 |

| Technological Advancements in Coating Formulations | +1.0% | Global, R&D intensive regions (e.g., EU, US, Japan) | 2025-2033 |

| Expansion of E-commerce and Industrial Packaging | +0.8% | Global, particularly high-growth e-commerce markets | 2025-2033 |

Metal Packaging Coating Market Restraints Analysis

Despite robust growth drivers, the Metal Packaging Coating market faces several significant restraints. One primary challenge is the stringent environmental regulations concerning the use of certain chemicals, such as Bisphenol A (BPA) in food contact coatings, leading to costly research and development efforts for BPA-non-intent alternatives. This regulatory landscape also affects the permissible levels of Volatile Organic Compounds (VOCs) and other hazardous air pollutants, necessitating substantial investments in compliant coating technologies. Another restraint is the volatility in raw material prices, particularly for petrochemical-derived resins and pigments, which directly impacts production costs and profitability margins for coating manufacturers. Economic downturns or geopolitical instabilities can further exacerbate these price fluctuations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental & Food Safety Regulations | -1.5% | Europe, North America, Japan | 2025-2033 |

| Volatility in Raw Material Prices | -1.0% | Global | 2025-2033 |

| Competition from Alternative Packaging Materials | -0.8% | Global, particularly Plastics & Glass | 2025-2033 |

| High Research & Development Costs for New Formulations | -0.7% | Global | 2025-2033 |

| Supply Chain Disruptions & Geopolitical Instability | -0.6% | Global | Short-to-Medium Term (2025-2028) |

Metal Packaging Coating Market Opportunities Analysis

Significant opportunities abound in the Metal Packaging Coating market, particularly driven by the growing demand for sustainable and high-performance solutions. The increasing consumer and regulatory preference for eco-friendly packaging is creating a substantial market for water-based, UV-cured, and bio-based coatings that offer reduced environmental impact without compromising protective qualities. Innovations in smart coatings, which can incorporate features like temperature indicators, anti-counterfeit measures, or even IoT connectivity, represent a nascent but high-potential area for market differentiation and value addition. Furthermore, the expansion of metal packaging applications into new end-use industries, beyond traditional food and beverages, such as pharmaceuticals, personal care, and specialized industrial chemicals, presents avenues for diversified growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-friendly & Sustainable Coatings | +1.8% | Global, driven by conscious consumers | 2025-2033 |

| Innovation in Smart & Functional Coatings | +1.5% | Developed Markets (e.g., North America, Europe) | 2027-2033 |

| Expansion into Emerging Markets & New Applications | +1.3% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Advancements in Coating Application Technologies | +1.0% | Global, particularly manufacturing hubs | 2025-2033 |

| Strategic Partnerships & Collaborations for R&D | +0.9% | Global | 2025-2033 |

Metal Packaging Coating Market Challenges Impact Analysis

The Metal Packaging Coating market faces several critical challenges that can impede its growth and profitability. One significant hurdle is the increasing complexity of regulatory compliance, particularly regarding food contact materials and environmental emissions. Adhering to diverse and evolving global standards requires continuous investment in product reformulation and testing, which can be resource-intensive and slow down market entry for new products. Another challenge is the intense competition from alternative packaging materials like plastics, glass, and flexible packaging, which often offer cost advantages or specific functional benefits that can divert demand from metal. Maintaining a competitive edge requires continuous innovation and demonstration of superior performance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex & Evolving Regulatory Landscape | -1.3% | Global, especially EU & North America | 2025-2033 |

| High Initial Investment & Operating Costs | -1.0% | Global | 2025-2033 |

| Disposal & Recycling Challenges for Mixed Materials | -0.8% | Global, particularly regions with less developed recycling infrastructure | 2025-2033 |

| Skilled Labor Shortages for Application & Formulation | -0.7% | Developed Markets | 2025-2033 |

| Intellectual Property Protection & Counterfeiting | -0.5% | Global, particularly emerging economies | 2025-2033 |

Metal Packaging Coating Market - Updated Report Scope

This report provides an in-depth analysis of the global Metal Packaging Coating Market, offering comprehensive insights into market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It delivers a detailed market forecast, competitive landscape analysis, and strategic recommendations for stakeholders navigating the evolving industry dynamics. The scope encompasses detailed segmentation by material type, coating type, application, and end-use industry, alongside a robust regional breakdown to provide a holistic understanding of market performance and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | PPG Industries Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Kansai Paint Co. Ltd., Nippon Paint Holdings Co. Ltd., RPM International Inc., Hempel A/S, Jotun A/S, Asian Paints Limited, The Dow Chemical Company, BASF SE, Eastman Chemical Company, Arkema S.A., Mitsui Chemicals, Inc., Covestro AG, DIC Corporation, Chugoku Marine Paints, Ltd., Valspar Corporation, Toyo Ink SC Holdings Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metal Packaging Coating market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation facilitates targeted strategies and investment decisions by identifying high-growth areas and specific industry needs. The market is primarily bifurcated by material type, reflecting the different metal substrates requiring specialized coatings, and by coating type, which defines the chemical composition and functional properties of the protective layers. Further segmentation by application and end-use industry highlights the varied demands from sectors ranging from consumer goods to heavy industrial usage, each requiring unique coating characteristics for optimal performance and safety. This multi-faceted segmentation ensures a comprehensive market overview, catering to the specific interests of stakeholders across the value chain.

- By Material Type:

- Steel: Widely used for food cans, general line cans, and industrial containers, offering durability and cost-effectiveness.

- Aluminum: Predominantly used for beverage cans and aerosol cans due to its lightweight, recyclability, and corrosion resistance.

- Tinplate: Employed for specialty food cans and caps, valued for its barrier properties and ease of fabrication.

- By Coating Type:

- Epoxy: Known for excellent adhesion, chemical resistance, and barrier properties, commonly used for internal can linings.

- Acrylic: Offers good clarity, UV resistance, and exterior durability, suitable for external can coatings.

- Polyester: Provides flexibility, good adhesion, and resistance to impact, often used for exterior and internal coatings.

- Vinyl: Used for its flexibility and resistance to specific chemicals, often found in industrial packaging.

- Phenolic: Offers high chemical and heat resistance, suitable for aggressive contents.

- Polyurethane: Provides excellent abrasion resistance, flexibility, and durability for high-performance applications.

- Others: Includes alkyds, silicone, and specialized blends addressing niche requirements.

- By Application:

- Food Cans: Coatings for fruits, vegetables, meats, and prepared meals, focusing on food safety and non-migration.

- Beverage Cans: Coatings for carbonated drinks, juices, and alcoholic beverages, prioritizing taste integrity and corrosion resistance.

- Aerosol Cans: Coatings for personal care products, household cleaners, and industrial sprays, requiring high pressure and chemical resistance.

- Caps & Closures: Coatings for bottle caps, jar lids, and vacuum closures, ensuring airtight seals and product integrity.

- Industrial Packaging: Coatings for drums, pails, and large containers used in chemicals, paints, and oils.

- Others: Includes coatings for specialty packaging, decorative items, and promotional tins.

- By End-Use Industry:

- Food & Beverage: The largest segment, driven by global consumption of packaged food and drinks.

- Personal Care: Includes aerosols for deodorants, hairsprays, and other cosmetic products.

- Healthcare: Packaging for pharmaceutical products, ensuring sterility and stability.

- Automotive: Coatings for parts, components, and specialty fluids packaging.

- Chemical: Packaging for industrial chemicals, paints, solvents, and adhesives.

- Others: Encompasses general line packaging, decorative packaging, and specialty industrial applications.

Regional Highlights

The global Metal Packaging Coating market exhibits distinct regional dynamics, influenced by varying levels of industrialization, regulatory environments, consumer preferences, and economic development. Each major region contributes uniquely to the market's growth and innovation landscape, presenting diverse opportunities and challenges for market players.

North America: This region is characterized by a mature market with a strong emphasis on regulatory compliance, particularly regarding BPA-non-intent coatings and VOC emissions. The robust food and beverage industry, coupled with high consumer awareness regarding product safety and sustainability, drives demand for advanced, high-performance, and eco-friendly coating solutions. Innovation in smart packaging and specialized industrial coatings is also a significant trend here. The U.S. remains the dominant market, with substantial investments in research and development to meet evolving consumer demands and stringent environmental standards. Canada also contributes steadily, driven by similar market forces.

Europe: Europe represents a highly regulated and sustainability-conscious market. Strict directives from the European Union on food contact materials, recycling, and environmental protection compel manufacturers to continuously innovate towards safer and more sustainable coating alternatives. Countries like Germany, France, and the UK are at the forefront of adopting water-based, UV-cured, and plant-based coatings. The region's strong food and beverage sector, coupled with a developed chemical and industrial packaging industry, ensures consistent demand. Emphasis on circular economy principles further accelerates the shift towards easily recyclable and de-inkable coatings.

Asia Pacific (APAC): APAC is anticipated to be the fastest-growing region in the Metal Packaging Coating market. This growth is primarily fueled by rapid urbanization, a burgeoning middle-class population, increasing disposable incomes, and the consequent surge in demand for packaged food and beverages across countries like China, India, and Southeast Asian nations. The expansion of manufacturing capabilities and the less stringent regulatory landscape compared to Western markets initially offered cost advantages, though environmental consciousness is gradually increasing. Japan and South Korea lead in technological adoption and advanced coating research, while China and India drive volume growth. The sheer scale of consumption and production in this region makes it a pivotal market for future expansion.

Latin America: This region presents a dynamic and evolving market for metal packaging coatings. Brazil and Mexico are key contributors, driven by significant growth in their respective food and beverage industries and a rising preference for convenience foods. Economic development and increasing urbanization are expanding the consumer base for packaged goods. While regulatory frameworks are developing, there's a growing awareness of global sustainability trends, leading to increasing demand for safer and more environmentally conscious coating solutions. The market here often seeks cost-effective solutions while gradually transitioning towards higher-performance coatings.

Middle East & Africa (MEA): The MEA region is experiencing steady growth, propelled by increasing infrastructure development, a growing population, and rising per capita income. The demand for packaged food and beverages, particularly in the GCC countries and South Africa, is on the rise. Investment in domestic manufacturing capabilities is also expanding, creating opportunities for metal packaging coating suppliers. While environmental regulations are still developing in many parts of the region, there is a growing recognition of global best practices, influencing the adoption of more advanced and compliant coating technologies. Strategic investments in food processing and industrial sectors are expected to drive further demand in the forecast period.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metal Packaging Coating Market.- PPG Industries Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- RPM International Inc.

- Hempel A/S

- Jotun A/S

- Asian Paints Limited

- The Dow Chemical Company

- BASF SE

- Eastman Chemical Company

- Arkema S.A.

- Mitsui Chemicals, Inc.

- Covestro AG

- DIC Corporation

- Chugoku Marine Paints, Ltd.

- Valspar Corporation

- Toyo Ink SC Holdings Co., Ltd.

Frequently Asked Questions

What is the projected growth rate of the Metal Packaging Coating Market?

The Metal Packaging Coating Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033.

Which factors are primarily driving the Metal Packaging Coating Market growth?

The market is primarily driven by the increasing global demand for packaged food and beverages, growing consumer awareness of food safety, and the rising emphasis on sustainable packaging solutions. Technological advancements in coating formulations also contribute significantly.

What are the main types of coatings used in metal packaging?

The main types of coatings include epoxy, acrylic, polyester, vinyl, phenolic, and polyurethane, each offering specific protective and functional properties tailored to various metal substrates and end-use applications.

Which region is expected to lead the Metal Packaging Coating Market growth?

The Asia Pacific region is expected to lead the market growth due to rapid urbanization, increasing disposable incomes, and the expanding packaged food and beverage industry in countries like China and India.

How do environmental regulations impact the Metal Packaging Coating Market?

Environmental regulations, particularly those concerning BPA-non-intent coatings and VOC emissions, significantly influence the market by driving research and development towards safer, more sustainable, and compliant coating formulations, often leading to increased production costs and strategic shifts for manufacturers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted