Medical Rubber Stopper Market

Medical Rubber Stopper Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706655 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

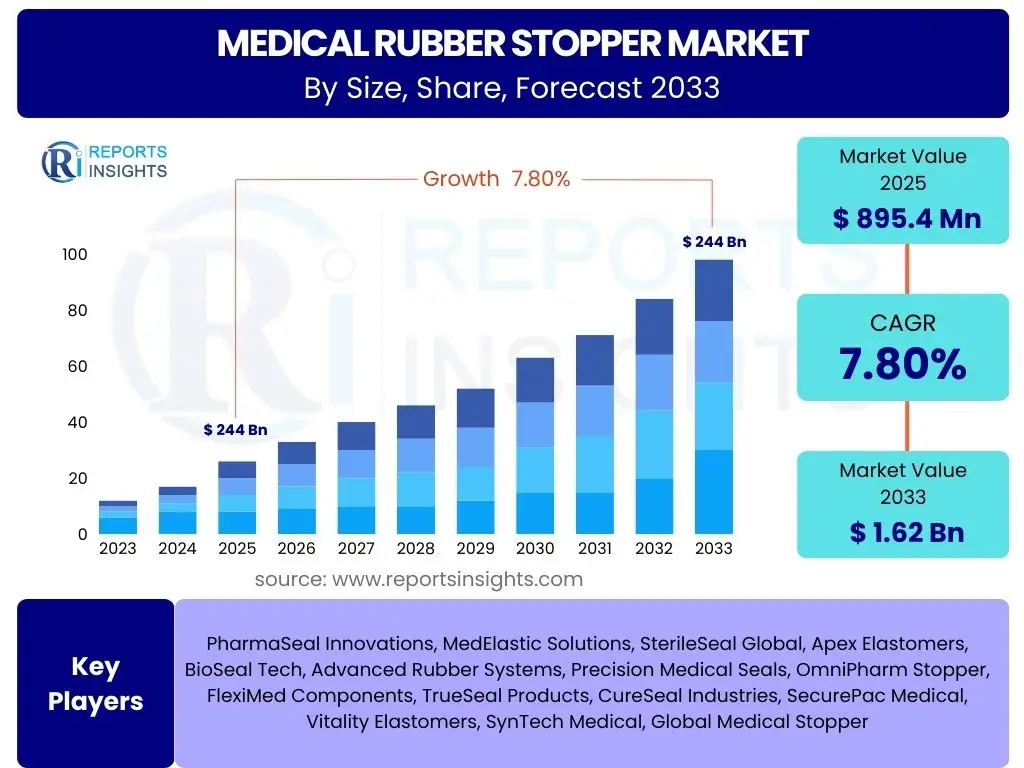

Medical Rubber Stopper Market Size

According to Reports Insights Consulting Pvt Ltd, The Medical Rubber Stopper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 895.4 Million in 2025 and is projected to reach USD 1.62 Billion by the end of the forecast period in 2033.

Key Medical Rubber Stopper Market Trends & Insights

The medical rubber stopper market is experiencing dynamic shifts driven by advancements in drug delivery systems and evolving regulatory landscapes. Key trends indicate a strong move towards enhanced material purity, compatibility with advanced biologic drugs, and innovative designs that support high-volume sterile manufacturing. Users frequently inquire about the latest innovations in stopper materials, how new drug formulations influence stopper design, and the impact of increasing demand for pre-filled syringes on market trends.

A significant trend involves the development of low-extractable and low-particulate stoppers, crucial for maintaining the integrity and efficacy of sensitive pharmaceutical compounds, especially biologics and biosimilars. This is coupled with a growing emphasis on stoppers that offer superior barrier properties against moisture and gas permeation, safeguarding drug stability over extended shelf lives. Furthermore, the market is seeing increased adoption of ready-to-use (RTU) stoppers, which streamline aseptic filling processes and reduce the risk of contamination in pharmaceutical manufacturing.

- Shift towards advanced elastomer formulations (e.g., bromobutyl, chlorobutyl) for enhanced chemical inertness and barrier properties.

- Growing demand for stoppers compatible with pre-filled syringes, cartridges, and auto-injectors due to convenience and reduced medication errors.

- Emphasis on high-purity, low-extractable, and low-particulate stoppers to ensure drug stability and patient safety.

- Increased adoption of ready-to-use (RTU) and washed-and-sterilized stoppers for streamlined aseptic processing.

- Integration of smart packaging solutions and anti-counterfeiting features in stopper designs.

- Focus on sustainable manufacturing practices and recyclable materials for environmental responsibility.

AI Impact Analysis on Medical Rubber Stopper

The integration of Artificial Intelligence (AI) and machine learning (ML) is beginning to profoundly influence the medical rubber stopper manufacturing sector, primarily through optimization of production processes, quality control, and supply chain management. Common user questions revolve around how AI can enhance the precision of manufacturing, improve defect detection, and streamline inventory and logistics for these critical components. The industry is exploring AI's potential to ensure consistent product quality and reduce waste, thereby impacting both operational efficiency and cost-effectiveness.

AI's role in quality assurance is particularly noteworthy. By leveraging computer vision and machine learning algorithms, manufacturers can automate and significantly improve the accuracy of defect detection, identifying minute imperfections that might be missed by human inspection. Predictive maintenance, another AI application, allows for the anticipation of equipment failures, minimizing downtime and optimizing production schedules. While AI does not directly influence the material science of stoppers, its application in manufacturing processes contributes to the overall reliability and quality of the final product, addressing critical safety and regulatory concerns in the pharmaceutical sector.

- Enhanced quality control through AI-powered vision systems for automated defect detection and inspection, ensuring high-purity standards.

- Optimization of manufacturing processes via machine learning algorithms for improved efficiency, reduced material waste, and minimized production cycles.

- Predictive maintenance of machinery and equipment, reducing unplanned downtime and enhancing operational reliability in stopper production facilities.

- Supply chain optimization using AI for demand forecasting, inventory management, and logistics, ensuring timely availability of stoppers.

- Data analytics and AI for material characterization and formulation optimization, indirectly aiding in the development of new stopper compounds.

Key Takeaways Medical Rubber Stopper Market Size & Forecast

The Medical Rubber Stopper market is poised for significant growth, driven by an expanding pharmaceutical industry, particularly the injectable drug segment, and increasing global healthcare expenditure. Key insights indicate that regulatory stringency and the demand for high-quality, sterile packaging solutions will continue to be primary market shapers. Users often seek clear summaries on the critical factors influencing market expansion, the most promising segments for investment, and the overall trajectory of the market through the forecast period.

The market's robust Compound Annual Growth Rate (CAGR) of 7.8% signifies a healthy and expanding sector, moving towards higher value-added products. This growth is heavily influenced by the rise of biologics and biosimilars, which necessitate highly inert and precise sealing solutions to maintain their efficacy. Furthermore, the global shift towards patient self-administration of injectable drugs, facilitated by pre-filled syringes and auto-injectors, will be a major catalyst for stopper demand, solidifying its essential role in modern healthcare delivery systems.

- The market is projected for steady growth, driven by advancements in drug delivery and stringent regulatory mandates.

- Injectable drug formulations, including biologics and biosimilars, are key growth catalysts, demanding specialized stopper materials.

- North America and Europe currently dominate, but Asia Pacific is emerging as a high-growth region due to expanding pharmaceutical manufacturing and healthcare infrastructure.

- Technological innovation in material science and manufacturing processes will be crucial for competitive advantage.

- Focus on sterility, low-extractables, and ready-to-use solutions will define future product development.

Medical Rubber Stopper Market Drivers Analysis

The medical rubber stopper market is significantly propelled by the continuous expansion of the global pharmaceutical and biotechnology sectors, especially the increasing pipeline of injectable drugs. The rising prevalence of chronic diseases worldwide necessitates more sophisticated and frequent drug administration, directly boosting the demand for secure and sterile packaging components like rubber stoppers. Furthermore, advancements in drug delivery systems, such as the growing adoption of pre-filled syringes and auto-injectors, streamline drug administration and enhance patient compliance, creating substantial demand for compatible stopper solutions.

Stringent regulatory requirements from bodies like the FDA and EMA for drug safety, purity, and stability mandate the use of high-quality, inert rubber stoppers, which effectively seals and protects sensitive pharmaceutical formulations. These regulations drive manufacturers to invest in research and development for advanced materials and production processes, ensuring compliance and enhancing product integrity. The global increase in healthcare expenditure, coupled with an aging population, further fuels the demand for pharmaceutical products, consequently expanding the market for medical rubber stoppers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for injectable drugs & biologics | +2.1% | Global (North America, Europe, Asia Pacific) | 2025-2033 |

| Increasing prevalence of chronic diseases | +1.8% | Global | 2025-2033 |

| Advancements in drug delivery systems (e.g., pre-filled syringes) | +1.6% | Global | 2025-2033 |

| Stringent regulatory requirements for drug safety and sterility | +1.2% | North America, Europe | 2025-2033 |

| Rising global healthcare expenditure | +1.1% | Asia Pacific, Latin America | 2025-2033 |

Medical Rubber Stopper Market Restraints Analysis

Despite robust growth drivers, the medical rubber stopper market faces certain restraints that could impact its expansion. One significant challenge is the volatility and fluctuating prices of raw materials, primarily synthetic rubber and various additives, which can lead to increased production costs and pressure on profit margins for manufacturers. Geopolitical instability and supply chain disruptions further exacerbate this issue, making consistent pricing and supply difficult to maintain.

Another notable restraint is the stringent regulatory approval process for medical components, including rubber stoppers. Manufacturers must adhere to rigorous quality and biocompatibility standards, such as those set by the FDA (e.g., 21 CFR Part 177.2600) and ISO guidelines. The extensive testing, validation, and documentation required for product approval can be time-consuming and costly, potentially delaying market entry for innovative products and increasing overall operational expenses. Additionally, the potential for drug-stopper interaction, leading to leaching or adsorption, necessitates extensive compatibility testing, adding complexity and cost to drug development, which can indirectly restrain market growth for certain stopper types.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices | -1.5% | Global | Short-to-Mid Term |

| Stringent regulatory approval processes and compliance costs | -1.2% | North America, Europe | Long Term |

| Risk of drug-stopper interaction and extractables/leachables concerns | -0.8% | Global | Ongoing |

| High capital investment required for advanced manufacturing | -0.7% | Global | Long Term |

Medical Rubber Stopper Market Opportunities Analysis

The medical rubber stopper market presents several promising opportunities for growth and innovation. The increasing global focus on sterile and ready-to-use packaging solutions, driven by pharmaceutical companies seeking to enhance efficiency and reduce contamination risks, creates a significant avenue for specialized stopper products. This demand is further amplified by the expansion of contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) which require a consistent supply of high-quality, pre-validated stoppers for their diverse client portfolios.

Furthermore, the rising adoption of novel drug delivery systems, such as pre-filled syringes, auto-injectors, and wearable drug delivery devices, necessitates the development of highly customized and compatible rubber stoppers. This presents an opportunity for manufacturers to innovate in design, material science, and manufacturing precision to meet the evolving requirements of these advanced systems. The untapped potential in emerging economies, characterized by improving healthcare infrastructure and growing pharmaceutical markets, also offers significant expansion opportunities for manufacturers willing to establish local presence or strategic partnerships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of advanced, low-extractable rubber formulations | +1.9% | Global | Mid-to-Long Term |

| Increasing adoption of ready-to-use (RTU) and sterilized stoppers | +1.7% | Global (Developed Markets) | 2025-2030 |

| Expansion into emerging markets (e.g., Asia Pacific, Latin America) | +1.5% | Asia Pacific, Latin America, MEA | Long Term |

| Rising demand for customized stopper solutions for novel drug delivery | +1.3% | Global | Ongoing |

Medical Rubber Stopper Market Challenges Impact Analysis

The medical rubber stopper market faces inherent challenges that demand continuous innovation and adaptation from manufacturers. Maintaining the utmost sterility and integrity of stoppers throughout the manufacturing, packaging, and delivery process is paramount, given their direct contact with pharmaceutical products. Any lapse in sterility can lead to drug contamination, posing significant patient safety risks and incurring severe regulatory penalties for pharmaceutical companies, placing immense pressure on stopper suppliers.

Moreover, ensuring compatibility with a vast array of diverse and often sensitive drug formulations is a persistent challenge. Different drugs have varying chemical properties, and the interaction between the drug product and the stopper material must be meticulously evaluated to prevent leaching of stopper components into the drug or adsorption of drug components by the stopper. This necessitates extensive research and development, costly testing protocols, and a broad portfolio of specialized stopper materials. The global supply chain for raw materials and finished goods can also present challenges, including logistical complexities, geopolitical risks, and the potential for disruptions that affect production timelines and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining sterility and product integrity throughout the supply chain | -1.0% | Global | Ongoing |

| Ensuring compatibility with diverse and sensitive drug formulations | -0.9% | Global | Ongoing |

| High capital expenditure for advanced manufacturing and cleanroom facilities | -0.8% | Global | Long Term |

| Managing complex global supply chain logistics and disruptions | -0.7% | Global | Short-to-Mid Term |

Medical Rubber Stopper Market - Updated Report Scope

This report provides an in-depth analysis of the global Medical Rubber Stopper market, covering market sizing, growth forecasts, competitive landscape, and key market dynamics. It offers comprehensive insights into market drivers, restraints, opportunities, and challenges, along with detailed segmentation analysis by type, material, application, and end-user. Regional market trends and country-specific insights are also examined to provide a holistic view of the market's current state and future prospects, aiding stakeholders in strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 895.4 Million |

| Market Forecast in 2033 | USD 1.62 Billion |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | PharmaSeal Innovations, MedElastic Solutions, SterileSeal Global, Apex Elastomers, BioSeal Tech, Advanced Rubber Systems, Precision Medical Seals, OmniPharm Stopper, FlexiMed Components, TrueSeal Products, CureSeal Industries, SecurePac Medical, Vitality Elastomers, SynTech Medical, Global Medical Stopper |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Medical Rubber Stopper market is comprehensively segmented to provide granular insights into its diverse components and drivers. These segmentations are critical for understanding specific market dynamics, identifying high-growth areas, and tailoring strategies for various product types, materials, applications, and end-users. Each segment offers unique opportunities and challenges influenced by technological advancements, regulatory mandates, and evolving healthcare needs.

The categorization by product type differentiates stoppers based on their primary function, such as lyophilization stoppers designed for freeze-dried products or injection stoppers optimized for parenteral drug administration. Material segmentation highlights the shift towards advanced elastomers like bromobutyl and chlorobutyl due to their superior chemical inertness and barrier properties, crucial for sensitive drug formulations. Application and end-user segments reflect the diverse use cases across the pharmaceutical value chain, from vial and syringe sealing in drug manufacturing to diagnostic kits in laboratories, providing a clear picture of demand patterns and strategic focus areas.

- By Product Type: Lyophilization Stoppers, Injection Stoppers, Vial Stoppers, Bottle Stoppers, Serum Stoppers, Diagnostic Stoppers

- By Material: Bromobutyl Rubber, Chlorobutyl Rubber, Natural Rubber, Silicone Rubber, Other Elastomers

- By Application: Vials, Syringes, Bottles, Cartridges, Diagnostic Kits, Bags, Other Applications

- By End-User: Pharmaceutical & Biopharmaceutical Companies, Contract Manufacturing Organizations (CMOs), Research & Academic Institutes, Diagnostic Laboratories, Hospitals & Clinics

Regional Highlights

- North America: This region dominates the medical rubber stopper market, primarily driven by a robust pharmaceutical and biotechnology industry, high R&D investments, and stringent regulatory frameworks. The increasing adoption of advanced drug delivery systems, particularly in the United States and Canada, coupled with a high prevalence of chronic diseases, fuels the demand for high-quality stoppers.

- Europe: Europe represents a significant market share, characterized by a well-established pharmaceutical manufacturing base, strong healthcare infrastructure, and favorable government initiatives promoting drug innovation. Countries like Germany, France, and the UK are key contributors, focusing on advanced sterile packaging solutions and biologics production.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate during the forecast period. This growth is attributed to the rapid expansion of the pharmaceutical sector in countries like China, India, and Japan, increasing healthcare expenditure, and a growing patient population. Rising foreign direct investments in healthcare and the establishment of new manufacturing facilities further propel market expansion.

- Latin America: This region is experiencing steady growth, driven by improving healthcare access, increasing pharmaceutical production, and growing awareness regarding sterile drug packaging. Countries like Brazil and Mexico are emerging as key markets, supported by economic development and healthcare reforms.

- Middle East and Africa (MEA): The MEA market is gradually expanding, primarily due to increasing investments in healthcare infrastructure, a rising prevalence of chronic diseases, and efforts to reduce reliance on imported pharmaceuticals. Government initiatives to develop local manufacturing capabilities in countries like Saudi Arabia and UAE contribute to market growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Medical Rubber Stopper Market.- PharmaSeal Innovations

- MedElastic Solutions

- SterileSeal Global

- Apex Elastomers

- BioSeal Tech

- Advanced Rubber Systems

- Precision Medical Seals

- OmniPharm Stopper

- FlexiMed Components

- TrueSeal Products

- CureSeal Industries

- SecurePac Medical

- Vitality Elastomers

- SynTech Medical

- Global Medical Stopper

- Integrity Seal Solutions

- Elite Medical Rubber

- PharmaSure Seals

- NextGen Elastomers

- MediPack Technologies

Frequently Asked Questions

Analyze common user questions about the Medical Rubber Stopper market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current estimated size of the Medical Rubber Stopper Market?

The Medical Rubber Stopper Market is estimated at USD 895.4 Million in 2025.

What is the projected growth rate for the Medical Rubber Stopper Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033.

Which factors are primarily driving the Medical Rubber Stopper Market growth?

Key drivers include the rising demand for injectable drugs, advancements in drug delivery systems, increasing prevalence of chronic diseases, and stringent regulatory requirements for drug safety and sterility.

What are the key trends shaping the Medical Rubber Stopper Market?

Major trends include a shift towards advanced elastomer formulations, growing demand for stoppers compatible with pre-filled syringes, emphasis on high-purity and low-extractable stoppers, and the adoption of ready-to-use (RTU) solutions.

Which region is expected to lead market growth in the coming years?

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate due to its expanding pharmaceutical sector, increasing healthcare expenditure, and growing patient population.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted