Medical Device Adhesive Market

Medical Device Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700380 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Medical Device Adhesive Market Size

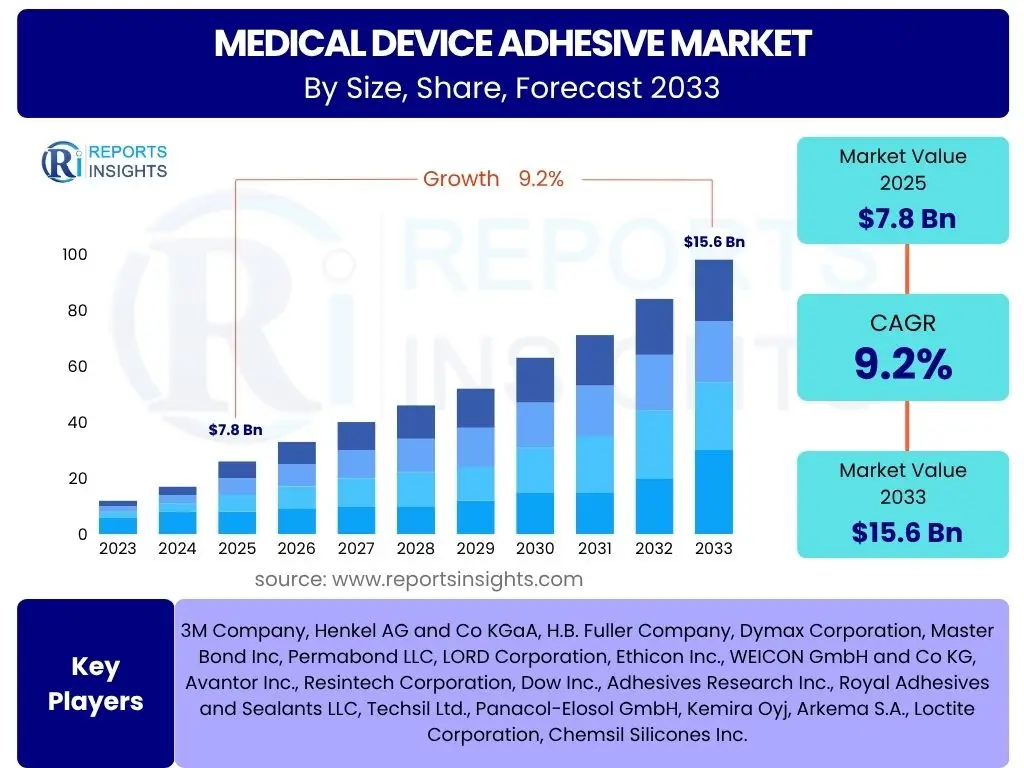

Medical Device Adhesive Market is projected to grow at a Compound annual growth rate (CAGR) of 9.2% between 2025 and 2033, valued at USD 7.8 billion in 2025 and is projected to grow to USD 15.6 billion By 2033 the end of the forecast period.

The medical device adhesive market is poised for substantial expansion, driven by continuous innovation in medical technology and an increasing global demand for advanced healthcare solutions. This significant growth trajectory reflects the critical role adhesives play in ensuring the safety, efficacy, and functionality of a wide array of medical devices, from implantable devices to surgical instruments and wearable sensors. The projected market size and CAGR underscore a robust future for this specialized sector, indicating strong investment opportunities and a fertile ground for technological advancements.

The forecasted figures represent a compound annual growth rate that significantly outpaces many traditional manufacturing sectors, highlighting the dynamic nature and inherent resilience of the medical industry. This growth is not merely quantitative but also qualitative, focusing on high-performance, biocompatible, and application-specific adhesive solutions. The substantial increase in market valuation from 2025 to 2033 signifies an escalating reliance on sophisticated adhesive technologies to meet stringent regulatory requirements and evolving clinical needs across various medical applications.

Key Medical Device Adhesive Market Trends & Insights

The medical device adhesive market is undergoing significant transformations, driven by technological advancements, evolving regulatory landscapes, and increasing demands for enhanced patient safety and device performance. These trends collectively shape the trajectory of the industry, influencing product development, application areas, and market competitiveness. Understanding these dynamics is crucial for stakeholders aiming to innovate and expand within this specialized sector.

- Growing adoption of minimally invasive surgical procedures demanding specialized adhesives for smaller, more complex devices.

- Increasing preference for biocompatible and bioresorbable adhesives to reduce patient complications and improve long-term outcomes.

- Integration of smart adhesive technologies with sensor capabilities for monitoring and diagnostic medical devices.

- Shift towards solvent-free and UV-curable adhesives due to environmental regulations and faster manufacturing processes.

- Rising demand for customizable adhesive solutions tailored to specific device designs and material compatibility requirements.

- Expansion of home healthcare and wearable medical devices boosting the need for flexible, durable, and skin-friendly adhesives.

- Emergence of 3D printing in medical device manufacturing, requiring novel adhesive formulations for additive processes.

- Focus on improving supply chain resilience and local manufacturing capabilities for critical adhesive components.

- Accelerated research and development into advanced material science to enhance adhesive strength, flexibility, and longevity.

- Implementation of stringent quality control and testing standards for medical-grade adhesives, impacting formulation and production.

AI Impact Analysis on Medical Device Adhesive

Artificial intelligence (AI) is beginning to exert a transformative influence across various sectors of healthcare, and the medical device adhesive market is no exception. While direct AI application in adhesive formulation is nascent, its indirect impacts through R&D acceleration, quality control, and supply chain optimization are becoming increasingly pronounced. AI's capacity to analyze vast datasets, predict material behaviors, and optimize manufacturing processes offers unprecedented opportunities for innovation and efficiency within this specialized market.

The integration of AI into the medical device adhesive lifecycle is primarily observed in areas such as predictive analytics for material degradation, automated quality inspection, and intelligent supply chain management. This technological convergence promises to enhance the reliability and performance of adhesives, reduce development cycles, and ensure higher compliance with stringent regulatory standards. As AI capabilities evolve, its role in designing novel adhesive chemistries and optimizing application methods is expected to grow, fundamentally reshaping how medical device adhesives are developed, manufactured, and utilized.

- Accelerated material discovery and formulation through AI-driven predictive modeling and simulation, reducing R&D timelines.

- Enhanced quality control and defect detection in adhesive application using AI-powered vision systems and anomaly detection.

- Optimized manufacturing processes for adhesives, including curing times and dosage, via machine learning algorithms.

- Improved supply chain efficiency and risk management for adhesive raw materials through predictive analytics.

- Personalized adhesive solutions for unique medical device geometries or patient-specific applications using AI-driven design tools.

- Smart adhesive systems with integrated AI for real-time performance monitoring and predictive maintenance in devices.

- Data-driven insights for understanding adhesive failure mechanisms and improving product longevity.

- Automation of regulatory compliance checks and documentation for new adhesive formulations.

Key Takeaways Medical Device Adhesive Market Size & Forecast

- The medical device adhesive market is projected for robust growth, with a CAGR of 9.2% from 2025 to 2033.

- Market valuation is expected to nearly double, from USD 7.8 billion in 2025 to USD 15.6 billion by 2033.

- Growth is primarily fueled by advancements in medical technology, rising demand for minimally invasive procedures, and increased adoption of wearable devices.

- Biocompatibility, regulatory compliance, and performance reliability are paramount factors influencing market expansion.

- Innovation in adhesive formulations, including bioresorbable and smart materials, represents key market trends.

- AI's indirect impact through R&D optimization, quality control, and supply chain efficiency is increasingly significant.

- Opportunities exist in customizable solutions, sustainable practices, and emerging economies.

- Challenges include stringent regulatory pathways, raw material volatility, and the need for highly specialized application techniques.

Medical Device Adhesive Market Drivers Analysis

The medical device adhesive market is significantly propelled by a confluence of factors that underscore its indispensable role in modern healthcare. These drivers collectively create a robust demand landscape, fostering innovation and expansion within the sector. A primary driver is the accelerating pace of innovation in medical device manufacturing itself, which constantly seeks more reliable, durable, and sophisticated bonding solutions. As devices become smaller, more complex, and more functional, the need for advanced adhesives that can withstand harsh biological environments and maintain integrity over long periods becomes critical. This pushes adhesive manufacturers to develop novel formulations that meet exacting performance standards.

Furthermore, the global demographic shift towards an aging population is leading to an increased incidence of chronic diseases and age-related conditions, thereby stimulating demand for a broader range of medical devices, particularly those for long-term care, diagnosis, and monitoring. This demographic trend directly translates into a heightened need for medical-grade adhesives that are not only effective but also biocompatible and safe for prolonged contact with human tissue. The growing preference for minimally invasive surgical procedures is another significant catalyst. These procedures often require smaller, more intricate instruments where traditional fastening methods are impractical, making specialized adhesives the preferred bonding solution due to their precision and ability to create strong, hermetic seals in confined spaces.

The escalating focus on patient safety and stringent regulatory frameworks globally also acts as a driver, albeit with challenges. Compliance with regulations such as the European Union's Medical Device Regulation (MDR) and the U.S. FDA's guidelines necessitates the use of high-quality, extensively tested adhesives. This drives manufacturers to invest heavily in research and development to produce adhesives that not only perform optimally but also meet rigorous biocompatibility and sterilization requirements, thereby ensuring product reliability and minimizing risks to patients. The expansion of healthcare infrastructure in emerging economies and the rising adoption of advanced medical technologies in these regions further contribute to the growing demand for medical device adhesives.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Minimally Invasive Procedures | +2.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Advancements in Medical Device Technology & Complexity | +2.0% | Globally, with innovation hubs in USA, Germany, Japan | Mid to Long-term (2027-2033) |

| Rising Global Geriatric Population and Chronic Disease Prevalence | +1.8% | Europe, Japan, North America, China, India | Long-term (2028-2033) |

| Stringent Regulatory Landscape for Medical Devices | +1.5% | Europe (MDR), North America (FDA), Japan (PMDA) | Ongoing, Continuous Impact |

| Growing Adoption of Wearable and Portable Medical Devices | +1.2% | North America, Asia Pacific, Europe | Short to Mid-term (2025-2029) |

| Increased Focus on Biocompatible and Specialty Adhesives | +1.0% | Global Market, driven by R&D | Mid-term (2026-2031) |

Medical Device Adhesive Market Restraints Analysis

While the medical device adhesive market demonstrates robust growth potential, it is simultaneously influenced by several significant restraints that can impede its expansion. One of the primary limiting factors is the exceptionally stringent regulatory approval process. Medical adhesives, especially those used in implantable devices or for direct tissue contact, must undergo rigorous testing for biocompatibility, toxicity, and long-term stability. The high cost and extended timelines associated with gaining these approvals can significantly deter new market entrants and slow down the introduction of innovative products, thereby limiting market dynamism and innovation. The complexity of these regulations varies by region, adding further layers of challenge for global market players.

Another considerable restraint is the high cost of raw materials and the volatility in their supply. Many specialized medical adhesives utilize unique polymers, initiators, and additives that are often derived from petroleum-based sources or are subject to limited availability. Fluctuations in commodity prices, geopolitical events, and disruptions in the global supply chain can lead to increased manufacturing costs, which are then passed on to device manufacturers, potentially impacting the overall affordability of medical devices. This dependency on specific raw materials also poses risks in terms of supply security and the ability to scale production rapidly in response to demand surges.

Furthermore, the need for highly specialized application techniques and equipment for certain advanced adhesives can act as a restraint. Some medical adhesives require precise dispensing, specific curing conditions (e.g., UV light, heat), or controlled environmental parameters for optimal performance. This complexity can increase manufacturing costs for device producers and necessitate significant investment in specialized machinery and operator training. The performance limitations of existing adhesives, such as issues with long-term durability, sterilization resistance, or bonding to diverse substrates, also present a constraint, requiring continuous research and development to overcome these hurdles and meet evolving clinical demands.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Approval Processes and Compliance Costs | -2.0% | Global, especially Europe (MDR), North America (FDA) | Ongoing, Continuous Impact |

| High Cost and Volatility of Raw Materials | -1.5% | Global Supply Chain Impact | Short to Mid-term (2025-2028) |

| Complexity of Application and Need for Specialized Equipment | -1.0% | Manufacturing Hubs Globally | Mid-term (2026-2030) |

| Performance Limitations of Current Adhesive Technologies | -0.8% | R&D Focused Regions | Long-term (2029-2033) |

Medical Device Adhesive Market Opportunities Analysis

Despite the challenges, the medical device adhesive market presents a multitude of compelling opportunities for growth and innovation. One significant area of opportunity lies in the burgeoning field of customizable and application-specific adhesive solutions. As medical devices become increasingly specialized, particularly for patient-specific implants or complex surgical instruments, there is a rising demand for adhesives that can be precisely formulated to bond disparate materials, withstand unique sterilization processes, or offer particular mechanical properties. This customization trend opens doors for adhesive manufacturers to collaborate closely with device developers, fostering deeper partnerships and creating high-value, niche market segments.

The continuous advancements in biomaterials and nanotechnology also present substantial opportunities. Research into bioresorbable adhesives, which naturally degrade and are absorbed by the body after serving their purpose, is a particularly promising avenue, eliminating the need for removal surgeries and reducing foreign body reactions. Similarly, the integration of smart functionalities into adhesives, such as those that can release drugs, change properties in response to physiological stimuli, or incorporate sensing capabilities, could revolutionize device performance and patient monitoring. These innovations pave the way for a new generation of therapeutic and diagnostic medical devices.

Furthermore, the expansion of healthcare markets in emerging economies and the increasing adoption of advanced medical devices in these regions represent a significant growth opportunity. Countries in Asia Pacific, Latin America, and parts of the Middle East and Africa are investing heavily in healthcare infrastructure and access to modern medical technologies. This expanding patient base and rising healthcare expenditure create a fertile ground for market penetration for medical device adhesives. Additionally, the increasing focus on sustainability and environmentally friendly manufacturing practices offers an opportunity for developing bio-based or solvent-free adhesive formulations, catering to a growing demand for greener products across the healthcare industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Biocompatible and Bioresorbable Adhesives | +2.8% | Global, driven by R&D in developed markets | Mid to Long-term (2027-2033) |

| Expansion into Emerging Markets and Healthcare Infrastructure | +2.2% | Asia Pacific, Latin America, Middle East, Africa | Mid-term (2026-2031) |

| Integration of Smart Adhesives and Advanced Functionalities | +1.7% | North America, Europe, Asia Pacific (Technology Hubs) | Long-term (2028-2033) |

| Increasing Demand for Customizable and Application-Specific Solutions | +1.5% | Global, driven by specialized medical device manufacturing | Short to Mid-term (2025-2029) |

| Focus on Sustainable and Environmentally Friendly Formulations | +1.0% | Europe, North America (Eco-conscious markets) | Mid-term (2026-2031) |

Medical Device Adhesive Market Challenges Impact Analysis

The medical device adhesive market, while experiencing significant growth, is not without its distinct set of challenges that can impact its development and adoption. A foremost challenge involves navigating the complex and constantly evolving regulatory landscape. Adhesives used in medical devices, particularly those with direct patient contact or long-term implants, face stringent approvals from bodies like the FDA in the U.S. and the EMA in Europe. Compliance requires extensive and costly testing for biocompatibility, toxicity, stability, and sterility. The long lead times and high failure rates associated with these approvals can delay product launches, increase development costs, and create significant barriers to market entry for new innovators, thereby stifling rapid advancements.

Another critical challenge is the inherent variability and complexity of bonding different substrates. Medical devices are often composed of diverse materials, including various plastics, metals, ceramics, and even biological tissues, each with unique surface properties. Developing a single adhesive that can reliably bond all these materials under varying environmental conditions (e.g., temperature, moisture, sterilization methods) while maintaining biocompatibility is a formidable engineering challenge. This often necessitates specialized adhesive formulations for each specific application, which can increase manufacturing complexity and inventory management for both adhesive suppliers and device manufacturers. Achieving consistent, high-performance bonds across a wide range of materials remains a significant hurdle.

Furthermore, the market faces challenges related to supply chain resilience and raw material sourcing. Many high-performance medical-grade adhesives rely on specialized chemicals and polymers, the supply of which can be vulnerable to geopolitical instability, trade disputes, or natural disasters. Disruptions in the supply chain can lead to raw material shortages, price volatility, and production delays, directly impacting the manufacturing timelines and costs of medical devices. The need for specialized storage and handling conditions for certain adhesive chemistries also adds to the logistical complexities. Overcoming these challenges requires strategic partnerships, diversification of suppliers, and investment in robust inventory management systems to ensure continuity of supply and maintain competitive pricing in a demanding market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Evolving Regulatory Compliance | -2.2% | Global, particularly developed markets (EU, US) | Ongoing, Long-term |

| Difficulties in Bonding Diverse and Complex Substrates | -1.8% | Global Manufacturing & R&D | Mid to Long-term (2027-2033) |

| Supply Chain Volatility and Raw Material Sourcing | -1.5% | Global Supply Chain Impact | Short to Mid-term (2025-2028) |

| High R&D Investment for Specialized Formulations | -1.0% | Developed Markets (Innovation Hubs) | Ongoing, Long-term |

| Performance Demands under Harsh Sterilization Methods | -0.7% | Global Medical Device Production | Mid-term (2026-2030) |

Medical Device Adhesive Market - Updated Report Scope

This comprehensive market research report offers a detailed analysis of the Medical Device Adhesive Market, providing critical insights into its current state, historical performance, and future projections. The report covers a wide array of market dynamics, including key trends, growth drivers, restraints, opportunities, and challenges impacting the industry. It meticulously segments the market by various parameters, offers extensive regional analysis, and profiles major market players, equipping stakeholders with actionable intelligence for strategic decision-making. The scope encompasses the period from 2019 to 2033, with 2024 as the base year, offering a clear outlook for market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 billion |

| Market Forecast in 2033 | USD 15.6 billion |

| Growth Rate | 9.2% (CAGR from 2025 to 2033) |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Henkel AG and Co KGaA, H.B. Fuller Company, Dymax Corporation, Master Bond Inc, Permabond LLC, LORD Corporation, Ethicon Inc., WEICON GmbH and Co KG, Avantor Inc., Resintech Corporation, Dow Inc., Adhesives Research Inc., Royal Adhesives and Sealants LLC, Techsil Ltd., Panacol-Elosol GmbH, Kemira Oyj, Arkema S.A., Loctite Corporation, Chemsil Silicones Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Medical Device Adhesive Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation allows for targeted analysis of market opportunities, enabling stakeholders to identify high-growth areas and tailor strategies to specific industry needs. The categorization by resin type, application, end-user, and curing type offers a comprehensive view of how different adhesive chemistries and their uses contribute to the overall market landscape. Each segment represents a unique set of demands, technological requirements, and regulatory considerations, highlighting the multifaceted nature of the medical device adhesive industry.

Understanding these segments is crucial for manufacturers, suppliers, and investors alike, as it helps in pinpointing where innovation is most critical, where market penetration is most feasible, and which end-user categories are driving specific demands. For instance, the performance requirements for an adhesive used in an implantable medical device differ significantly from those for a disposable diagnostic device. Similarly, the curing mechanism chosen for an adhesive greatly influences the manufacturing process and speed of device assembly. This detailed segmentation analysis serves as a fundamental framework for strategic planning and competitive positioning within the complex ecosystem of medical device manufacturing.

- By Resin Type: This segment categorizes adhesives based on their chemical composition, influencing their properties and suitability for various medical applications.

- Cyanoacrylates: Known for rapid bonding and high strength, often used for external applications or temporary fixation.

- Silicones: Valued for biocompatibility, flexibility, and heat resistance, suitable for implantable and wearable devices.

- Polyurethanes: Offer excellent flexibility and strong adhesion, used in catheters and other flexible medical components.

- Epoxies: Provide high bond strength and chemical resistance, ideal for structural bonding in rigid devices.

- Acrylics: Known for versatility, fast curing, and good adhesion to a variety of substrates.

- Others: Includes specialized formulations like hydrogels, hot melts, and solvent-based adhesives for niche applications.

- By Application: This segment highlights the diverse uses of medical adhesives across the healthcare spectrum, reflecting varied performance requirements.

- Medical Device Assembly: Encompasses adhesives used in the manufacturing and assembly of medical instruments and components.

- Catheters

- Syringes

- Endoscopes

- Respiratory Devices

- Diagnostic Devices

- Prosthetics and Orthotics

- Drug Delivery Systems

- Wearable Devices: Adhesives for devices worn on the body for monitoring or therapeutic purposes, requiring skin-friendly and durable properties.

- Dental Adhesives: Specifically formulated for dental restorative procedures and orthodontic applications.

- Medical Tapes and Labels: Adhesives used for securing dressings, identifying medical equipment, or packaging.

- Surgical Sealants: Used in surgical procedures to prevent leaks from tissues or blood vessels.

- Medical Device Assembly: Encompasses adhesives used in the manufacturing and assembly of medical instruments and components.

- By End User: This segment focuses on the primary consumers of medical device adhesives, reflecting the diverse operational environments and purchasing patterns.

- Hospitals and Clinics: Major consumers for a wide range of devices, surgical procedures, and patient care.

- Ambulatory Surgical Centers: Growing segment driving demand for adhesives used in outpatient procedures.

- Diagnostic Laboratories: Utilize adhesives in diagnostic kits and laboratory equipment.

- Medical Device Manufacturers: The largest end-user group, incorporating adhesives into their product lines.

- Research Institutes: Employ adhesives for R&D in new medical technologies and device prototypes.

- By Curing Type: This segment differentiates adhesives based on their activation mechanism, impacting manufacturing processes and application speed.

- Light Curing: Adhesives that cure rapidly when exposed to UV or visible light, suitable for high-speed assembly.

- Heat Curing: Adhesives that require elevated temperatures for activation, offering strong, durable bonds.

- Moisture Curing: Adhesives that react with ambient moisture for polymerization, suitable for certain environmental conditions.

- Pressure Sensitive: Adhesives that form a bond upon application of light pressure, commonly used in medical tapes.

- Other Curing Types: Includes anaerobic, solvent evaporation, and two-part chemical reaction curing methods.

Regional Highlights

The global medical device adhesive market exhibits distinct regional dynamics, influenced by varying healthcare expenditures, regulatory frameworks, technological adoption rates, and demographic trends. Each major geographical region contributes uniquely to the market's growth and presents specific opportunities and challenges for adhesive manufacturers and medical device companies. Analyzing these regional highlights is essential for understanding global market distribution and for formulating effective localization strategies.

- North America: This region holds a significant share of the medical device adhesive market, driven by its well-established healthcare infrastructure, high healthcare spending, and a robust medical device industry. The United States, in particular, leads in medical device innovation and adoption of advanced technologies, fostering strong demand for high-performance, specialized adhesives. Stringent regulatory standards set by the FDA also drive the demand for premium, highly compliant adhesive solutions. The rising prevalence of chronic diseases and an aging population further contribute to sustained market growth in this region.

- Europe: Europe represents another substantial market for medical device adhesives, characterized by its mature healthcare systems, strong research and development capabilities, and emphasis on patient safety. Countries like Germany, France, and the UK are major contributors to medical device manufacturing and R&D. The implementation of the Medical Device Regulation (MDR) has intensified the focus on biocompatibility and rigorous testing for adhesives, influencing product development and market entry. Growth is also spurred by increasing surgical procedures and the demand for innovative, minimally invasive devices.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for medical device adhesives during the forecast period. This growth is primarily attributed to improving healthcare infrastructure, rising disposable incomes, increasing awareness about advanced medical treatments, and a large patient pool in populous countries like China and India. Government initiatives to promote local medical device manufacturing, coupled with growing medical tourism, are also key drivers. The region offers significant opportunities for market players due to its rapid economic development and expanding healthcare access.

- Latin America: This region is experiencing steady growth in the medical device adhesive market, fueled by increasing healthcare investments, expanding access to medical services, and a rising prevalence of non-communicable diseases. Countries such as Brazil and Mexico are leading the way in adopting modern medical technologies. While regulatory frameworks are developing, the demand for affordable and effective medical solutions continues to drive the adoption of adhesives in various device applications.

- Middle East and Africa (MEA): The MEA region is witnessing emerging opportunities for medical device adhesives, primarily due to increasing healthcare expenditure, government initiatives to upgrade healthcare facilities, and a growing focus on medical tourism in certain countries like UAE and Saudi Arabia. While smaller in market share compared to developed regions, the ongoing investment in healthcare infrastructure and rising awareness of advanced medical treatments are expected to drive gradual but consistent growth in the demand for medical device adhesives across the region.

Top Key Players:

The market research report covers the analysis of key stake holders of the Medical Device Adhesive Market. Some of the leading players profiled in the report include -:- 3M Company

- Henkel AG and Co KGaA

- H.B. Fuller Company

- Dymax Corporation

- Master Bond Inc

- Permabond LLC

- LORD Corporation

- Ethicon Inc.

- WEICON GmbH and Co KG

- Avantor Inc.

- Resintech Corporation

- Dow Inc.

- Adhesives Research Inc.

- Royal Adhesives and Sealants LLC

- Techsil Ltd.

- Panacol-Elosol GmbH

- Kemira Oyj

- Arkema S.A.

- Loctite Corporation

- Chemsil Silicones Inc.

Frequently Asked Questions:

What is the current market size of the Medical Device Adhesive Market?

The Medical Device Adhesive Market was valued at USD 7.8 billion in 2025 and is projected to reach USD 15.6 billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of 9.2% during the forecast period from 2025 to 2033. This growth is driven by increasing demand for advanced medical devices and expanding healthcare infrastructure globally.What are the key drivers for the growth of the Medical Device Adhesive Market?

Key drivers include the rising demand for minimally invasive surgical procedures, continuous advancements in medical device technology leading to more complex designs, the global aging population and increasing prevalence of chronic diseases, and stringent regulatory requirements that necessitate high-quality, reliable adhesive solutions. The growing adoption of wearable and portable medical devices also significantly contributes to market expansion.How does AI impact the Medical Device Adhesive Market?

AI primarily impacts the Medical Device Adhesive Market by accelerating material discovery through predictive modeling, enhancing quality control and defect detection during manufacturing, and optimizing supply chain efficiency for raw materials. While direct AI integration into adhesive chemistry is emerging, its indirect influence through process optimization and data-driven insights is crucial for innovation, reducing development cycles, and ensuring product reliability.What are the main types of adhesives used in medical devices?

The main types of adhesives used in medical devices are categorized by their resin type and curing mechanism. Common resin types include cyanoacrylates, silicones, polyurethanes, epoxies, and acrylics, each offering specific properties suitable for various applications. Curing types encompass light curing (UV/visible light), heat curing, moisture curing, and pressure-sensitive adhesives, enabling diverse manufacturing processes and performance characteristics.Which regions are leading the Medical Device Adhesive Market, and why?

North America and Europe currently lead the Medical Device Adhesive Market due to their advanced healthcare infrastructures, high R&D investments, stringent regulatory environments, and significant adoption of sophisticated medical technologies. However, the Asia Pacific region is projected to be the fastest-growing market, driven by rapidly improving healthcare access, increasing healthcare expenditure, and a large patient base in developing economies like China and India.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted