Medical Cyclotron Market

Medical Cyclotron Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709730 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Medical Cyclotron Market Size

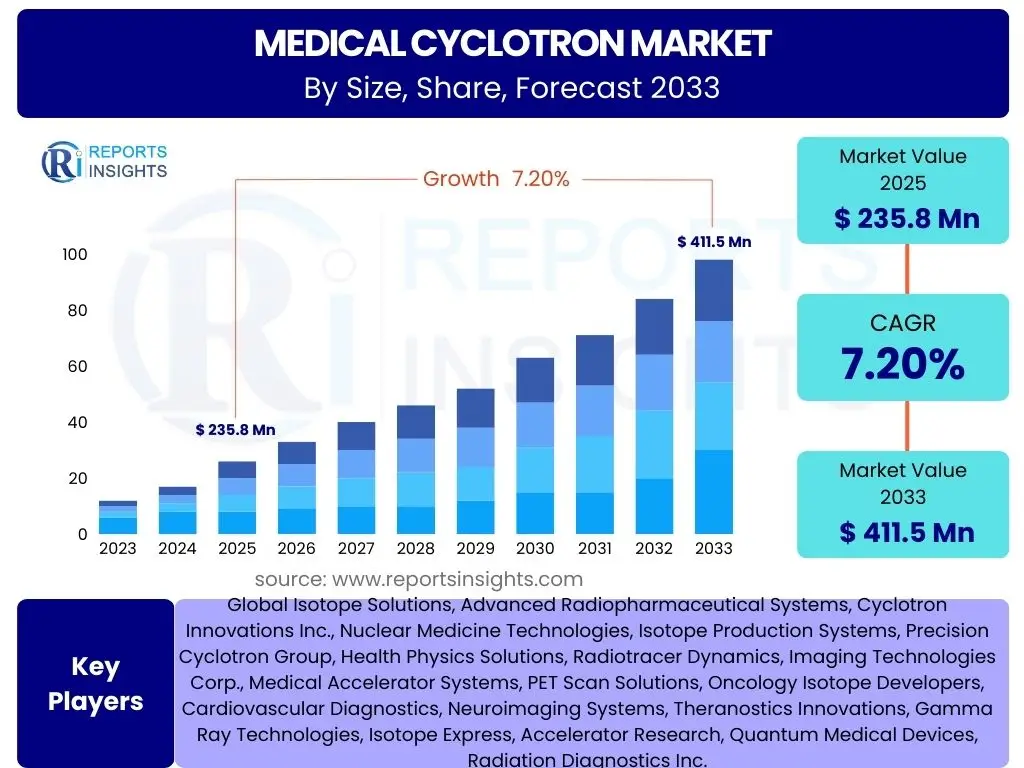

According to Reports Insights Consulting Pvt Ltd, The Medical Cyclotron Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 235.8 million in 2025 and is projected to reach USD 411.5 million by the end of the forecast period in 2033.

Key Medical Cyclotron Market Trends & Insights

Analysis of common user questions regarding Medical Cyclotron market trends and insights reveals significant interest in technological advancements, the expanding scope of nuclear medicine applications, and geographical market shifts. Users are keen to understand how innovations in cyclotron design, such as smaller footprint and higher energy efficiency, are shaping the industry. There is also considerable focus on the increasing demand for various medical isotopes, particularly those used in advanced diagnostic imaging and emerging theranostic approaches.

Furthermore, inquiries frequently address the evolution of healthcare infrastructure, particularly in developing economies, and the growing adoption of Positron Emission Tomography (PET) and Single-Photon Emission Computed Tomography (SPECT) technologies. The market is experiencing a shift towards integrated solutions that combine cyclotron facilities with radiopharmaceutical production, streamlining the supply chain for critical medical diagnostics and therapies. This integration is crucial for enhancing operational efficiency and ensuring timely access to life-saving radioisotopes.

- Increasing demand for medical isotopes, especially F-18 FDG and Ga-68, driven by rising cancer incidence.

- Technological advancements leading to compact, higher-energy, and more automated cyclotron systems.

- Growing adoption of PET-CT and SPECT imaging modalities in oncology, cardiology, and neurology.

- Shift towards theranostics, combining diagnostics and therapy using radioactive isotopes, driving isotope demand.

- Expansion of nuclear medicine facilities and research centers globally, particularly in emerging economies.

- Integration of cyclotron facilities with radiopharmaceutical production to optimize supply chains.

AI Impact Analysis on Medical Cyclotron

Common user questions related to the impact of Artificial Intelligence (AI) on the Medical Cyclotron domain predominantly center on its potential to enhance operational efficiency, improve diagnostic accuracy, and accelerate radiopharmaceutical research. Users frequently inquire about how AI can optimize cyclotron parameters for increased isotope yield, predict maintenance needs to minimize downtime, and streamline the complex processes involved in radiopharmaceutical synthesis. The expectation is that AI will introduce unprecedented levels of precision and automation into cyclotron operations, making the production of critical medical isotopes more reliable and cost-effective.

Moreover, there is considerable interest in AI's role in advancing the application of radiopharmaceuticals. This includes questions about AI-powered image analysis for more accurate interpretation of PET/SPECT scans, potentially leading to earlier disease detection and more personalized treatment plans. Users are also exploring AI's capacity to accelerate the discovery and development of novel radiotracers, significantly shortening the time from conceptualization to clinical application. The integration of AI is seen as a transformative force, promising to enhance the utility and accessibility of nuclear medicine procedures by optimizing every stage from isotope production to patient diagnosis and therapy.

- AI-driven optimization of cyclotron operation parameters for enhanced isotope production efficiency and yield.

- Predictive maintenance algorithms for cyclotrons, reducing downtime and extending equipment lifespan.

- Automation of radiopharmaceutical synthesis and quality control processes using AI, ensuring consistency and safety.

- AI-assisted image reconstruction and analysis in PET/SPECT scans, leading to improved diagnostic accuracy and precision.

- Acceleration of novel radiotracer discovery and development through AI-powered drug design and simulation.

- Enhanced personalized medicine approaches by integrating AI insights from imaging data with treatment planning.

Key Takeaways Medical Cyclotron Market Size & Forecast

Analysis of common user questions about the Medical Cyclotron market size and forecast highlights a strong emphasis on the sustainability of growth, regional disparities in market development, and the long-term investment viability within the sector. Users are keen to understand the underlying drivers contributing to the projected CAGR and what specific factors will sustain market expansion through 2033. There's a particular focus on how increasing global health expenditures, especially in oncology, directly translate into demand for cyclotron-produced medical isotopes, solidifying the market's trajectory.

Furthermore, inquiries often revolve around the anticipated market values in both the near and long term, reflecting stakeholder interest in strategic planning and investment opportunities. The consistent growth forecast underscores the indispensable role of nuclear medicine in modern diagnostics and therapeutics, particularly with the rise of chronic diseases and the aging global population. Understanding these key takeaways is crucial for market participants looking to leverage growth opportunities and mitigate potential challenges in this technologically advanced and capital-intensive industry.

- The Medical Cyclotron Market is poised for substantial growth, driven primarily by the escalating demand for diagnostic and therapeutic radiopharmaceuticals.

- Significant market expansion is anticipated in emerging economies due to improving healthcare infrastructure and increased access to advanced medical imaging.

- Technological innovation, particularly in developing compact and cost-effective cyclotrons, will be a critical factor in market penetration and adoption.

- The shift towards theranostics and personalized medicine is expected to create new avenues for market growth and isotope demand.

- Strategic investments in research and development for novel isotopes and advanced production techniques will define market leadership.

Medical Cyclotron Market Drivers Analysis

The Medical Cyclotron Market is significantly propelled by the increasing global incidence of chronic diseases, particularly cancer, which necessitates advanced diagnostic and therapeutic solutions. The escalating demand for Positron Emission Tomography (PET) and Single-Photon Emission Computed Tomography (SPECT) scans, crucial for early disease detection and treatment monitoring, directly fuels the need for cyclotron-produced medical isotopes such as F-18 and Ga-68. This demand is further amplified by an aging global population, which is more susceptible to age-related conditions requiring nuclear medicine interventions.

Moreover, continuous advancements in radiopharmaceutical research and development are introducing new isotopes and applications, expanding the clinical utility of nuclear medicine. This innovation cycle not only broadens the scope of treatable conditions but also enhances the precision and efficacy of existing therapies. Favorable regulatory frameworks and increasing government funding for healthcare infrastructure, especially in developing countries, also play a pivotal role in accelerating the adoption and installation of medical cyclotrons, thereby sustaining market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising incidence of chronic diseases, particularly cancer | +2.1% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Increasing demand for PET-CT and SPECT imaging | +1.8% | Global, high growth in emerging economies | 2025-2033 (Mid to Long-term) |

| Technological advancements in radiopharmaceutical production | +1.5% | North America, Europe, Japan | 2025-2030 (Short to Mid-term) |

| Growing adoption of theranostics | +1.3% | North America, Europe, select APAC countries | 2027-2033 (Mid to Long-term) |

Medical Cyclotron Market Restraints Analysis

Despite robust growth drivers, the Medical Cyclotron Market faces significant restraints, primarily due to the exceptionally high capital investment required for purchasing and installing these sophisticated systems. The substantial initial outlay for the cyclotron itself, coupled with the costs associated with facility construction, shielding, and specialized infrastructure, creates a formidable barrier to entry for many healthcare providers and research institutions. This high upfront cost can deter smaller organizations and limit market penetration, especially in regions with constrained healthcare budgets.

Furthermore, the stringent regulatory requirements and complex licensing procedures for operating cyclotrons and producing radioactive isotopes pose a considerable challenge. Compliance with these regulations necessitates extensive documentation, specialized expertise, and ongoing monitoring, adding to the operational burden and costs. The shortage of skilled professionals, including nuclear medicine physicians, radiochemists, and cyclotron operators, further exacerbates these restraints, as specialized training and expertise are critical for the safe and efficient operation of these advanced systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital investment for purchase and installation | -1.9% | Global, especially emerging economies | 2025-2033 (Long-term) |

| Stringent regulatory framework and licensing | -1.5% | Global, particularly North America, Europe | 2025-2033 (Ongoing) |

| Shortage of skilled personnel (radiochemists, operators) | -1.2% | Global, significant in rapidly growing markets | 2025-2033 (Long-term) |

| Challenges in radioactive waste management | -0.8% | Global | 2025-2033 (Ongoing) |

Medical Cyclotron Market Opportunities Analysis

Significant opportunities in the Medical Cyclotron Market stem from the continuous advancements in isotope production technology and the development of novel radiopharmaceuticals. Innovations leading to more efficient, compact, and automated cyclotron systems can broaden accessibility and reduce operational complexities, making these essential tools available to a wider range of healthcare facilities. The increasing investment in research and development for new diagnostic and therapeutic agents, particularly those for personalized medicine and theranostics, creates a sustained demand for a diverse array of medical isotopes.

Moreover, the expansion of healthcare infrastructure in emerging economies across Asia Pacific, Latin America, and the Middle East offers substantial untapped market potential. As these regions improve their medical capabilities and increase healthcare spending, the adoption of advanced nuclear medicine technologies, including cyclotrons, is expected to surge. Strategic partnerships between cyclotron manufacturers, radiopharmaceutical producers, and healthcare providers to establish integrated production and distribution networks can further capitalize on these growth opportunities, enhancing market reach and efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in compact and cost-effective cyclotron technology | +1.7% | Global, particularly in new market entries | 2025-2030 (Short to Mid-term) |

| Development of novel radiopharmaceuticals for new applications | +1.4% | North America, Europe, Japan | 2026-2033 (Mid to Long-term) |

| Expansion of healthcare infrastructure in emerging economies | +1.2% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 (Long-term) |

| Increasing adoption of theranostic agents | +1.0% | North America, Europe, select high-growth markets | 2027-2033 (Mid to Long-term) |

Medical Cyclotron Market Challenges Impact Analysis

The Medical Cyclotron Market is confronted with several significant challenges that could impede its growth trajectory. One primary challenge is the intense competition among market players, driven by the specialized nature of the technology and the high stakes involved in radiopharmaceutical production. This competitive landscape often leads to price pressures and demands for continuous innovation, requiring substantial R&D investments that small and medium-sized enterprises might find difficult to sustain. Furthermore, the limited half-life of many medical isotopes necessitates proximity to end-users, creating complex logistical and distribution challenges, especially in geographically dispersed healthcare networks.

Another critical challenge lies in ensuring the continuous supply chain of raw materials and precursor chemicals required for isotope production, which can be vulnerable to geopolitical instabilities or supply disruptions. The need for highly specialized and expensive facilities, including extensive radiation shielding and specialized air handling systems, further restricts widespread adoption, especially in regions with limited capital resources or infrastructure. Overcoming these challenges will require strategic foresight, collaborative efforts, and innovative solutions to maintain market vitality and ensure equitable access to nuclear medicine technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial setup and operational costs | -1.5% | Global, particularly developing nations | 2025-2033 (Long-term) |

| Limited half-life of medical isotopes and logistics | -1.1% | Global, impacting remote areas | 2025-2033 (Ongoing) |

| Supply chain complexities for raw materials | -0.9% | Global | 2025-2030 (Short to Mid-term) |

| Strict environmental and safety regulations | -0.7% | Global, impacting operational expenditure | 2025-2033 (Ongoing) |

Medical Cyclotron Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Medical Cyclotron Market, encompassing historical data from 2019 to 2023, current market estimates for 2025, and projections through 2033. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report also details market segmentation by various parameters such as cyclotron type, application, and end-user, alongside a thorough regional analysis to highlight geographical trends and growth prospects. Strategic profiles of leading market players are included to provide insights into the competitive environment and key business strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 235.8 Million |

| Market Forecast in 2033 | USD 411.5 Million |

| Growth Rate | 7.2% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Isotope Solutions, Advanced Radiopharmaceutical Systems, Cyclotron Innovations Inc., Nuclear Medicine Technologies, Isotope Production Systems, Precision Cyclotron Group, Health Physics Solutions, Radiotracer Dynamics, Imaging Technologies Corp., Medical Accelerator Systems, PET Scan Solutions, Oncology Isotope Developers, Cardiovascular Diagnostics, Neuroimaging Systems, Theranostics Innovations, Gamma Ray Technologies, Isotope Express, Accelerator Research, Quantum Medical Devices, Radiation Diagnostics Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Medical Cyclotron Market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation allows for precise analysis of key growth areas, technological preferences, and end-user adoption patterns. By dissecting the market based on cyclotron type, application, end-user, and isotope type, stakeholders can identify specific niches and tailor their strategies to leverage distinct opportunities within each segment.

For instance, the segmentation by cyclotron type distinguishes between low-energy and high-energy systems, reflecting different production capabilities and target isotopes. Application-based segmentation highlights the dominant role of oncology, while also recognizing the growing importance of cardiology and neurology in nuclear medicine. End-user segmentation provides insight into the primary consumers of cyclotron-produced isotopes, ranging from large hospitals to specialized research facilities, influencing distribution and service models across the industry. This granular analysis is crucial for understanding market maturity and emerging trends.

- By Type:

- Low Energy Cyclotrons (<15 MeV)

- High Energy Cyclotrons (>15 MeV)

- By Application:

- Oncology (PET Imaging, Radiotherapy Planning)

- Cardiology (Perfusion Imaging, Viability Studies)

- Neurology (Neuroreceptor Imaging, Dementia Diagnosis)

- Others (Infection Imaging, Research & Development)

- By End-User:

- Hospitals

- Diagnostic Centers

- Research Institutions

- Pharmaceutical & Biotechnology Companies

- By Isotope Type:

- Fluorine-18 (F-18)

- Gallium-68 (Ga-68)

- Carbon-11 (C-11)

- Nitrogen-13 (N-13)

- Oxygen-15 (O-15)

- Other Isotopes (e.g., Iodine-123, Technetium-99m precursors)

Regional Highlights

- North America: Dominates the market due to robust healthcare infrastructure, high adoption of advanced diagnostic imaging techniques, significant R&D investments in nuclear medicine, and a high incidence of chronic diseases. The United States and Canada are key contributors.

- Europe: A mature market characterized by strong regulatory support, increasing healthcare expenditure, and a growing aging population. Germany, France, and the UK are prominent countries driving market growth.

- Asia Pacific (APAC): Expected to witness the highest growth rate due to improving healthcare access, increasing awareness of nuclear medicine, rising cancer prevalence, and significant government initiatives to upgrade medical facilities. China, Japan, and India are emerging as major markets.

- Latin America: Demonstrates steady growth with increasing investments in healthcare infrastructure and rising demand for advanced diagnostic services, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): Emerging market with nascent but growing nuclear medicine capabilities, driven by increasing healthcare spending, development of specialized medical centers, and efforts to diversify healthcare services in countries like Saudi Arabia and UAE.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Medical Cyclotron Market.- Global Isotope Solutions

- Advanced Radiopharmaceutical Systems

- Cyclotron Innovations Inc.

- Nuclear Medicine Technologies

- Isotope Production Systems

- Precision Cyclotron Group

- Health Physics Solutions

- Radiotracer Dynamics

- Imaging Technologies Corp.

- Medical Accelerator Systems

- PET Scan Solutions

- Oncology Isotope Developers

- Cardiovascular Diagnostics

- Neuroimaging Systems

- Theranostics Innovations

- Gamma Ray Technologies

- Isotope Express

- Accelerator Research

- Quantum Medical Devices

- Radiation Diagnostics Inc.

Frequently Asked Questions

Analyze common user questions about the Medical Cyclotron market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Medical Cyclotron Market?

The Medical Cyclotron Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033, reaching an estimated USD 411.5 million by 2033.

What are the primary applications of medical cyclotrons?

Medical cyclotrons are primarily used for producing radioisotopes essential for diagnostic imaging, particularly PET-CT and SPECT scans, across oncology, cardiology, and neurology applications, as well as for emerging theranostic treatments.

How does AI impact the medical cyclotron industry?

AI significantly impacts the industry by optimizing cyclotron operations for higher isotope yield, enabling predictive maintenance, automating radiopharmaceutical synthesis, enhancing diagnostic image analysis, and accelerating novel radiotracer discovery.

What are the key challenges faced by the Medical Cyclotron Market?

Key challenges include the high capital investment for equipment and facilities, stringent regulatory requirements, the limited half-life of many medical isotopes leading to logistical complexities, and a shortage of skilled personnel.

Which regions are expected to drive market growth for medical cyclotrons?

North America currently dominates, while Asia Pacific is anticipated to exhibit the highest growth rate due to improving healthcare infrastructure, increasing disease prevalence, and rising healthcare expenditure in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted