Maritime Satellite Communication Market

Maritime Satellite Communication Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709080 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

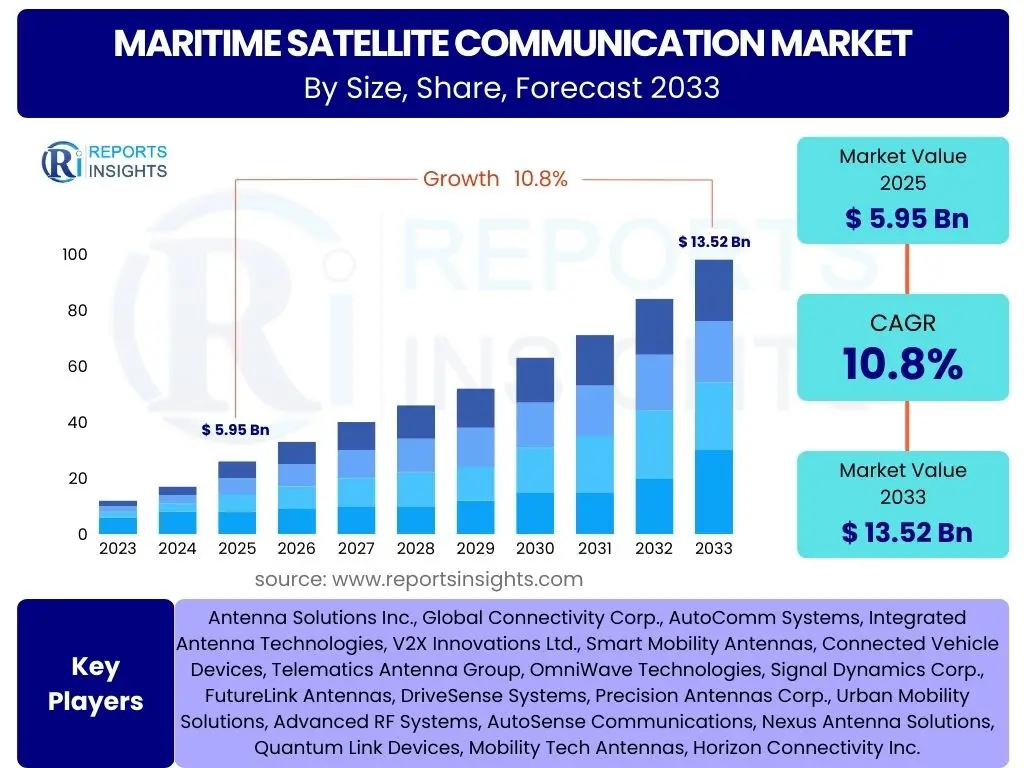

Maritime Satellite Communication Market Size

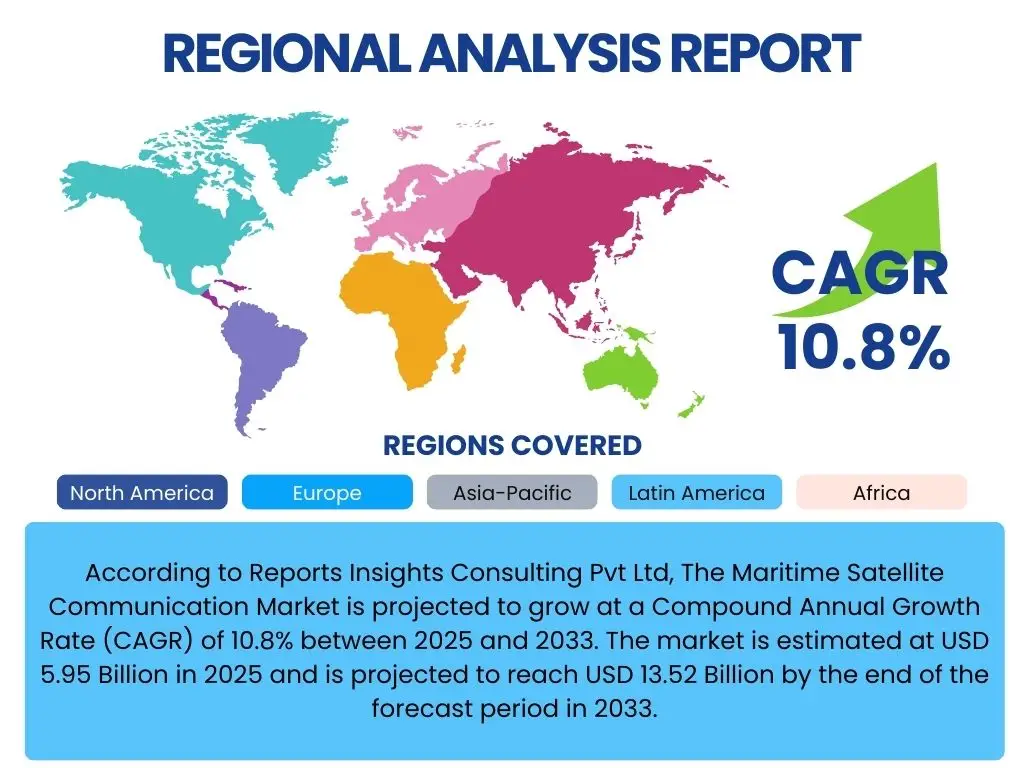

According to Reports Insights Consulting Pvt Ltd, The Maritime Satellite Communication Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 5.95 Billion in 2025 and is projected to reach USD 13.52 Billion by the end of the forecast period in 2033.

Key Maritime Satellite Communication Market Trends & Insights

User inquiries frequently highlight the rapid evolution of connectivity solutions and the increasing demand for high-bandwidth services at sea. A significant trend revolves around the expansion and deployment of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations, which are fundamentally altering the landscape by offering lower latency and higher throughput compared to traditional Geostationary Earth Orbit (GEO) systems. This shift is driving competitive pricing and enabling new applications that were previously impractical due to technical limitations.

Furthermore, the maritime industry's accelerated digitalization, driven by the adoption of IoT devices, remote monitoring, and autonomous vessel technologies, is creating an unprecedented need for robust and reliable satellite communication. Users are also interested in how these advancements contribute to operational efficiency, crew welfare, and enhanced safety protocols. The integration of advanced data analytics and cloud-based services with satellite networks is another crucial insight, facilitating optimized route planning, predictive maintenance, and real-time decision-making capabilities across various maritime operations.

- Proliferation of LEO and MEO satellite constellations for enhanced connectivity.

- Increasing demand for high-throughput and low-latency communication services.

- Integration of IoT and digitalization across the maritime sector.

- Emphasis on crew welfare and remote operational support through reliable internet.

- Growing adoption of cloud services and data analytics for operational optimization.

- Enhanced focus on cybersecurity solutions for satellite communication networks.

- Hybrid network solutions combining satellite, cellular, and terrestrial links.

AI Impact Analysis on Maritime Satellite Communication

Common user questions regarding AI's impact on maritime satellite communication frequently center on its potential to revolutionize network management, optimize data traffic, and enhance security measures. Users are keen to understand how artificial intelligence can move beyond simple automation to introduce predictive capabilities, intelligent resource allocation, and adaptive network configurations. AI algorithms are being deployed to monitor network performance in real-time, anticipate potential outages or congestion, and dynamically re-route data through available satellite links, ensuring consistent and reliable connectivity even in challenging maritime environments.

Beyond network optimization, AI is poised to play a pivotal role in enabling sophisticated applications such as autonomous vessel navigation and smart port operations, which require ultra-reliable, low-latency communication for critical data exchange. Furthermore, the integration of AI-powered analytics can help in processing vast amounts of data generated by maritime IoT devices, turning raw information into actionable insights for improved operational efficiency, fuel consumption optimization, and predictive maintenance of onboard systems. The security aspect is also a major concern, with AI being explored for advanced threat detection and anomaly identification within satellite communication channels to protect against cyber attacks.

- Optimized network traffic management and dynamic bandwidth allocation.

- Predictive maintenance for satellite communication hardware and onboard systems.

- Enhanced cybersecurity through AI-driven threat detection and anomaly analysis.

- Facilitation of autonomous vessel operations requiring ultra-reliable communication.

- Intelligent data processing and analytics for operational efficiency and fuel optimization.

- Automated fault detection and self-healing capabilities for satellite networks.

- Improved decision-making for route planning and resource deployment.

Key Takeaways Maritime Satellite Communication Market Size & Forecast

User inquiries into the market size and forecast for maritime satellite communication consistently highlight the industry's robust growth trajectory, driven by an insatiable demand for connectivity and the transformative potential of advanced satellite technologies. The forecast underscores a sustained period of expansion, primarily fueled by the increasing digitalization of shipping, the global surge in maritime trade, and the imperative for improved operational efficiency and crew welfare at sea. The shift towards LEO/MEO constellations is a critical factor enabling this growth, providing faster, more reliable, and cost-effective communication solutions that were previously unattainable.

A significant takeaway is the projected substantial increase in market valuation, indicating strong investment confidence and technological innovation within the sector. This growth is not uniform across all segments, with high-throughput services and value-added solutions expected to capture a larger share. Furthermore, the market's expansion is intrinsically linked to global economic activity, offshore energy exploration, and the ever-present need for enhanced safety and compliance in maritime operations. Stakeholders should note the convergence of satellite technology with IoT, AI, and cloud computing as a primary driver for future market opportunities and value creation.

- Significant market expansion anticipated over the forecast period (2025-2033).

- Growth primarily driven by digitalization, maritime trade, and operational efficiency demands.

- LEO and MEO constellations are key enablers for future market growth and service innovation.

- High-throughput satellite (HTS) services are gaining substantial market traction.

- Convergence with IoT, AI, and cloud platforms is crucial for value-added service development.

- Increased focus on cybersecurity and resilient communication infrastructure.

- Opportunities in new applications like autonomous shipping and remote operations.

Maritime Satellite Communication Market Drivers Analysis

The maritime satellite communication market is experiencing robust growth propelled by several foundational drivers. A primary factor is the escalating global demand for reliable and high-bandwidth connectivity across all maritime sectors, driven by the increasing digitalization of vessels, the need for enhanced operational efficiency, and the growing focus on crew welfare. The advent of new satellite technologies, particularly LEO and MEO constellations, is significantly expanding coverage and reducing latency, making advanced communication services more accessible and cost-effective. This technological leap enables the adoption of sophisticated applications onboard, from real-time data analytics to remote diagnostics and IoT integration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Bandwidth Connectivity at Sea | +2.5% | Global, particularly Asia Pacific (APAC) and Europe | 2025-2033 |

| Technological Advancements in Satellite Constellations (LEO/MEO) | +2.1% | Global, especially North America and Europe for deployment | 2025-2033 |

| Growing Digitalization and Automation in Maritime Industry | +1.8% | Global, across all shipping segments | 2025-2033 |

| Enhanced Focus on Crew Welfare and Connectivity Needs | +1.5% | Global, particularly cruise and merchant shipping | 2025-2033 |

| Expansion of Global Maritime Trade and Offshore Activities | +1.2% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

Maritime Satellite Communication Market Restraints Analysis

Despite its significant growth potential, the maritime satellite communication market faces several inherent restraints that could temper its expansion. One major hurdle is the substantial initial investment required for satellite infrastructure, including launch costs and ground segment development, which translates to higher service costs for end-users. The complex regulatory environment, encompassing international and national spectrum allocation, licensing, and data privacy laws, also poses a significant challenge, creating barriers to entry and operational complexities. Geopolitical tensions and the risk of cyberattacks targeting critical communication infrastructure represent additional concerns that can disrupt market stability and deter investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Service Costs | -1.9% | Global, affecting smaller operators | 2025-2033 |

| Regulatory Hurdles and Spectrum Allocation Challenges | -1.5% | Global, varying by region/country | 2025-2033 |

| Geopolitical Risks and Cybersecurity Threats | -1.3% | Global, particularly in sensitive regions | 2025-2033 |

| Limited Bandwidth in Remote Areas for Legacy Systems | -1.0% | Polar regions, deep ocean routes | 2025-2028 |

| Competition from Terrestrial and Hybrid Connectivity Solutions | -0.8% | Coastal areas, short-sea shipping (Europe, North America) | 2025-2033 |

Maritime Satellite Communication Market Opportunities Analysis

Significant opportunities abound within the maritime satellite communication market, particularly stemming from the accelerating pace of digital transformation across the maritime industry. The burgeoning demand for real-time data from maritime IoT devices and the increasing adoption of cloud-based services for operational management present vast avenues for satellite service providers. Furthermore, the integration of 5G technology with satellite backhaul promises to unlock ultra-low latency and high-capacity services, critical for emerging applications like autonomous shipping and smart port infrastructure. The expansion into new geographic regions, especially in developing economies with growing maritime trade, also represents a substantial growth opportunity, as these areas often lack robust terrestrial infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with 5G and IoT Technologies | +2.3% | Global, particularly technologically advanced regions | 2025-2033 |

| Emergence of Autonomous Shipping and Smart Port Initiatives | +2.0% | Europe, North America, Asia Pacific (e.g., Singapore) | 2027-2033 |

| Untapped Markets in Developing Economies and Remote Regions | +1.7% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

| Demand for Value-Added Services (e.g., Cloud, Cybersecurity, AI) | +1.4% | Global, all advanced maritime sectors | 2025-2033 |

| Renewed Focus on Environmental Monitoring and Compliance | +1.0% | Global, driven by IMO regulations | 2025-2033 |

Maritime Satellite Communication Market Challenges Impact Analysis

The maritime satellite communication market encounters several significant challenges that necessitate strategic innovation and adaptation. One prominent challenge is the imperative for interoperability between diverse satellite systems and communication protocols, which often hinders seamless integration and creates complexities for users operating hybrid networks. Maintaining consistent and high-quality service in adverse weather conditions or in regions with limited satellite coverage remains a technical hurdle, particularly for high-bandwidth applications. Furthermore, the rapidly evolving technological landscape demands continuous investment in research and development, as well as a skilled workforce capable of managing and maintaining advanced satellite communication systems, posing both financial and human resource challenges to market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability Issues Across Diverse Satellite Systems | -1.6% | Global, for multi-vendor environments | 2025-2033 |

| Maintaining Service Quality in Extreme Environmental Conditions | -1.4% | Polar routes, tropical storm regions | 2025-2033 |

| Skilled Workforce Shortage for Advanced Systems | -1.2% | Global, particularly in emerging markets | 2025-2033 |

| Rapid Technological Obsolescence and Upgrade Cycles | -1.1% | Global, affecting hardware investments | 2025-2033 |

| Data Latency for Time-Sensitive Critical Applications | -0.9% | Global, for autonomous/real-time control systems | 2025-2030 |

Maritime Satellite Communication Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Maritime Satellite Communication Market, offering critical insights into its current size, historical performance, and future growth projections. The scope includes a detailed examination of key market trends, the impact of artificial intelligence, and a thorough analysis of market drivers, restraints, opportunities, and challenges. The report segments the market by component, application, band, and platform, providing a granular view of market dynamics across various categories and geographical regions. It also profiles leading industry participants, offering a strategic understanding of the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.95 Billion |

| Market Forecast in 2033 | USD 13.52 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GlobalConnect Satcom, OceanLink Systems, AquaComms Solutions, MarineConnect Global, Voyager Satellite Services, BlueWave Telecom, SeaNet Technologies, Horizon Satellite Communications, Oceanic Digital Systems, Stellar Maritime Services, DeepBlue Communications, Transoceanic Satcom, NavSat Solutions, Zenith Marine Networks, Tide Communications Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Maritime Satellite Communication Market is comprehensively segmented to provide a detailed understanding of its diverse operational landscape and technological adoption patterns. This segmentation enables a granular analysis of market performance across various components, applications, satellite bands, and communication platforms. The component segment differentiates between the physical hardware required for connectivity and the array of services that facilitate communication, including essential connectivity, advanced value-added services, and comprehensive managed solutions. Such differentiation highlights the distinct revenue streams and technological focuses within the market, crucial for strategic planning.

Application-based segmentation is critical for understanding the varied demands of different maritime sectors, ranging from the high-volume data needs of merchant shipping to the critical communication requirements of government and military operations, as well as the unique connectivity demands of passenger and leisure vessels. Furthermore, segmenting by satellite band (C, Ku, Ka, L, X-band) and platform type (VSAT, MSS) reflects the different technical capabilities, coverage areas, and cost structures associated with each communication technology. This layered analysis reveals how various segments respond to technological advancements, regulatory changes, and evolving operational requirements, thereby shaping market growth and competitive dynamics.

- By Component: Hardware (Antennas, Transceivers, Modems, Other Hardware), Services (Connectivity Services, Value-Added Services, Managed Services)

- By Application: Merchant Shipping (Bulk Carriers, Tankers, Container Ships, General Cargo), Fishing Vessels, Offshore Oil & Gas (Rig Communication, Crew Welfare, Exploration), Passenger Ships (Cruise Ships, Ferries), Government & Military (Naval Vessels, Coast Guard, Research Vessels), Leisure Vessels, Other Applications

- By Band: C-Band, Ku-Band, Ka-Band, L-Band, X-Band, Others

- By Platform: VSAT (Very Small Aperture Terminal), MSS (Mobile Satellite Services)

Regional Highlights

- North America: Characterized by early adoption of advanced satellite technologies, significant R&D investments, and a strong presence of key market players. The region benefits from robust offshore oil and gas activities and a technologically advanced maritime industry.

- Europe: A mature market with high demand for crew welfare and operational efficiency solutions, driven by stringent environmental regulations and a large merchant fleet. The region is a hub for satellite technology innovation and deployment of hybrid networks.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to expanding maritime trade, increasing shipbuilding activities, and rising demand for digital solutions from emerging economies. Countries like China, India, and Southeast Asian nations are key growth drivers.

- Latin America: Growing market primarily fueled by offshore oil and gas exploration, increasing cruise tourism, and governmental investments in maritime security. Development of port infrastructure and trade routes further supports market expansion.

- Middle East & Africa (MEA): Emerging market with significant potential due to strategic trade routes, expanding oil and gas industry, and increasing investment in port development and maritime logistics. Demand for reliable communication for remote operations is high.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Maritime Satellite Communication Market.- GlobalConnect Satcom

- OceanLink Systems

- AquaComms Solutions

- MarineConnect Global

- Voyager Satellite Services

- BlueWave Telecom

- SeaNet Technologies

- Horizon Satellite Communications

- Oceanic Digital Systems

- Stellar Maritime Services

- DeepBlue Communications

- Transoceanic Satcom

- NavSat Solutions

- Zenith Marine Networks

- Tide Communications Group

Frequently Asked Questions

What is Maritime Satellite Communication?

Maritime Satellite Communication refers to the use of satellite technology to provide voice, data, and video connectivity to vessels at sea, enabling essential operations, navigation, crew welfare, and digital applications regardless of geographical location.

How fast is the Maritime Satellite Communication market growing?

The Maritime Satellite Communication market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033, indicating a robust expansion driven by digital transformation and increasing connectivity demands.

What are the primary drivers of this market?

Key drivers include the increasing demand for high-bandwidth connectivity, technological advancements like LEO/MEO satellite constellations, growing digitalization in the maritime industry, and an enhanced focus on crew welfare and operational efficiency.

What role does AI play in Maritime Satellite Communication?

AI significantly impacts the market by optimizing network management, enabling predictive maintenance, enhancing cybersecurity, facilitating autonomous vessel operations, and processing vast amounts of data for improved operational efficiency and decision-making.

Which regions are key for Maritime Satellite Communication market growth?

North America and Europe are technologically mature markets, while Asia Pacific (APAC) is anticipated to be the fastest-growing region due to expanding maritime trade and increasing digitalization. Latin America and MEA also present significant emerging opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted