Foundry Binder Market

Foundry Binder Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701628 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

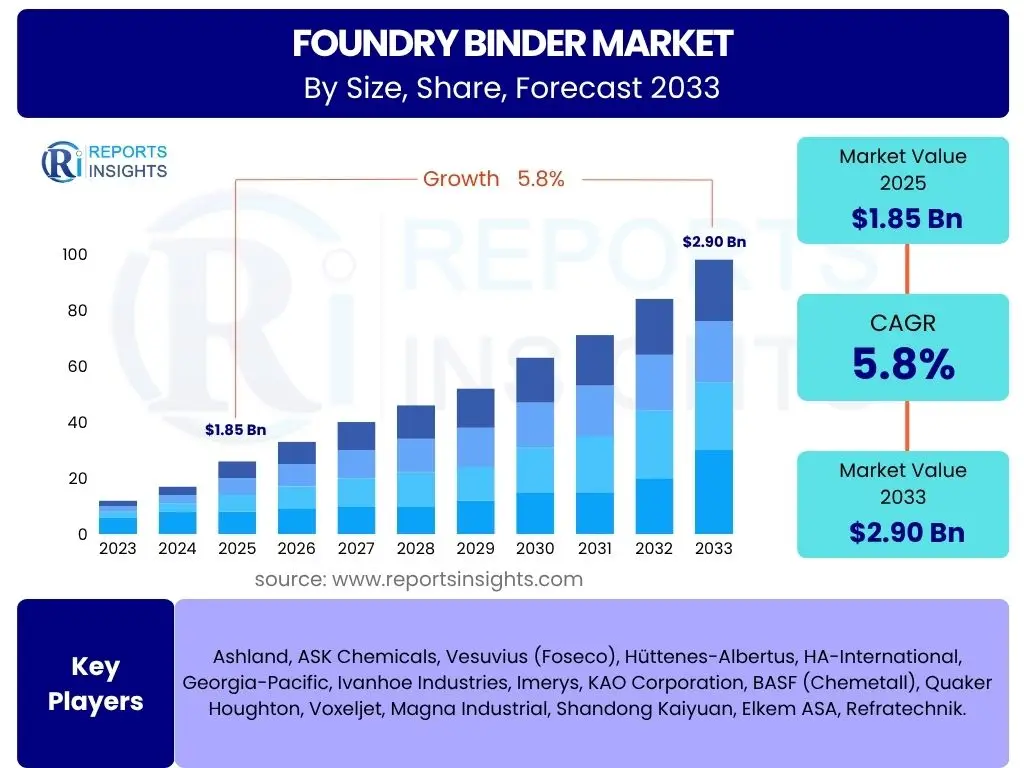

Foundry Binder Market Size

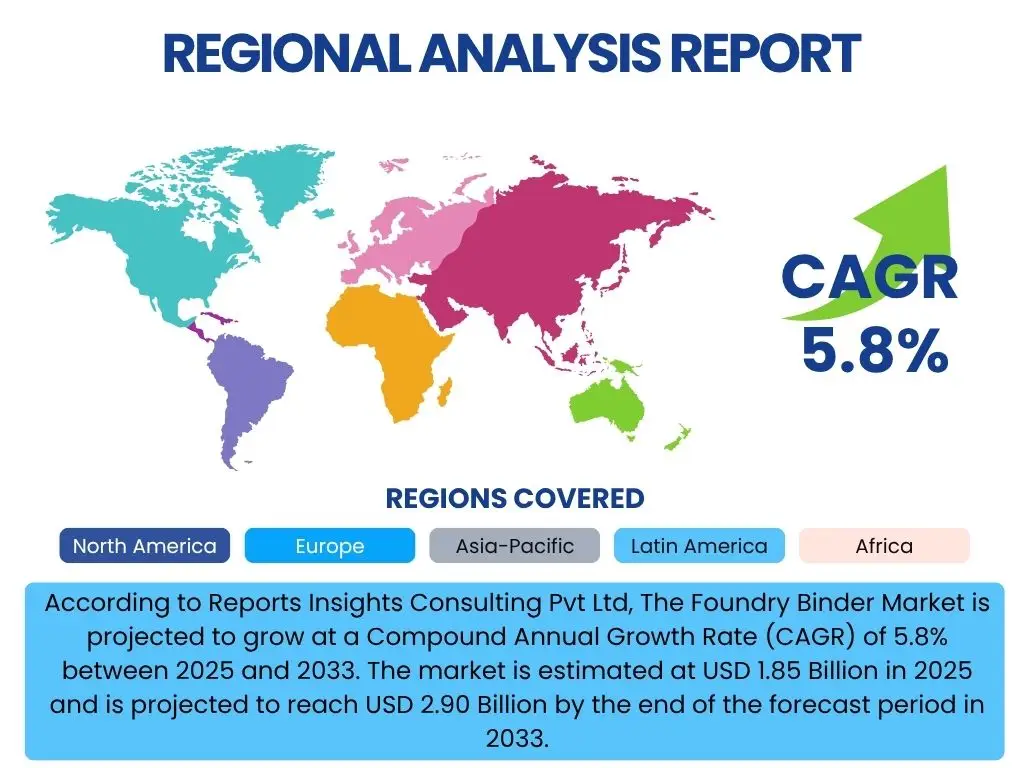

According to Reports Insights Consulting Pvt Ltd, The Foundry Binder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 2.90 Billion by the end of the forecast period in 2033.

Key Foundry Binder Market Trends & Insights

The Foundry Binder Market is currently undergoing significant transformation, driven by evolving industrial demands and stringent environmental regulations. Users frequently inquire about the trajectory of sustainability within the market, the impact of advanced materials on binder formulation, and the overarching shift towards more efficient manufacturing processes. Key insights reveal a robust push towards eco-friendly solutions, an increasing integration of automation in casting, and a growing emphasis on high-performance binders that can withstand extreme conditions while reducing overall production costs. These trends collectively shape the market's growth trajectory and innovation landscape.

Furthermore, the market is witnessing a convergence of digital technologies with traditional foundry practices. Foundries are exploring smart manufacturing principles, incorporating data analytics to optimize binder usage and improve casting quality. This drive for operational excellence, coupled with the rising demand for lightweight and complex castings across various industries, underscores the dynamic nature of the foundry binder sector. The focus remains on achieving a balance between performance, cost-effectiveness, and environmental responsibility.

- Shift towards eco-friendly and bio-based binder systems to meet sustainability goals and regulations.

- Increased adoption of automation and digitalization in foundry operations to optimize binder application and casting processes.

- Growing demand for high-performance binders capable of producing intricate and lightweight castings for advanced applications.

- Development of innovative binder chemistries offering improved strength, reduced emissions, and faster curing times.

- Emphasis on circular economy principles, including binder reclamation and reuse technologies to minimize waste.

AI Impact Analysis on Foundry Binder

Common user questions regarding AI's impact on the Foundry Binder market often revolve around its potential for process optimization, quality enhancement, and predictive capabilities. There is a strong interest in how AI can contribute to more efficient material usage, reduce waste, and improve the overall consistency of foundry operations. Users seek to understand if AI can predict optimal binder formulations for specific applications or anticipate equipment failures, thereby minimizing downtime and operational costs.

The consensus suggests that AI is poised to revolutionize foundry operations by enabling data-driven decision-making. Through machine learning algorithms, AI can analyze vast datasets from casting processes, including temperature, humidity, and binder consumption, to identify patterns and anomalies. This allows for real-time adjustments, predictive maintenance of machinery, and optimization of binder quantities, leading to significant improvements in efficiency, quality, and sustainability. While the adoption rate may vary, the industry recognizes AI as a critical tool for future competitive advantage.

- Process Optimization: AI algorithms can analyze real-time data from casting operations to optimize binder mixing, application, and curing parameters, leading to reduced waste and improved efficiency.

- Quality Control: Machine learning models can detect defects in castings early by analyzing sensory data, ensuring consistent quality and reducing scrap rates, often linked to binder performance.

- Predictive Maintenance: AI can forecast equipment failures in binder dispensing and mixing systems, enabling proactive maintenance and minimizing costly downtime.

- Material Characterization: AI-driven analysis can accelerate the development of new binder formulations by predicting material properties and performance characteristics based on chemical structures.

- Supply Chain Management: AI can optimize inventory levels of binders and raw materials, predict demand fluctuations, and improve logistics, ensuring timely availability and cost efficiency.

Key Takeaways Foundry Binder Market Size & Forecast

Key takeaways from the Foundry Binder Market size and forecast indicate a consistent and positive growth trajectory driven by several interdependent factors. Users are keen to understand the primary drivers of this growth, the most promising application areas, and the geographical regions expected to exhibit the strongest expansion. The market's resilience is largely attributed to the sustained demand from the automotive and industrial machinery sectors, alongside emerging opportunities in aerospace and defense, which require high-precision castings.

The forecast highlights a significant emphasis on technological advancements aimed at enhancing binder performance and reducing environmental footprints. This includes the development of binders that offer superior strength-to-weight ratios, emit fewer volatile organic compounds (VOCs), and are amenable to recycling. The growth is also supported by increasing industrialization in developing economies, which necessitates the expansion of manufacturing capabilities, including robust foundry operations. Ultimately, the market is poised for innovation-led expansion, balancing industrial efficiency with environmental stewardship.

- The market exhibits steady growth, primarily fueled by demand from the automotive, heavy machinery, and construction sectors.

- Significant growth opportunities are emerging from the development of eco-friendly and sustainable binder solutions.

- Asia Pacific is projected to be the fastest-growing region, driven by rapid industrialization and expansion of manufacturing bases.

- Technological advancements in binder chemistry and application methods are crucial for market expansion.

- Increased focus on reducing VOC emissions and improving worker safety is influencing product development and adoption.

Foundry Binder Market Drivers Analysis

The Foundry Binder Market's expansion is fundamentally propelled by the robust growth in various end-use industries, particularly the automotive, heavy machinery, and construction sectors. As global population and industrialization continue to expand, so does the demand for cast metal components integral to these industries. The automotive sector, for instance, requires high-precision castings for engine blocks, cylinder heads, and transmission components, driving the need for advanced foundry binders that ensure dimensional accuracy and structural integrity. Similarly, the construction and industrial machinery industries demand durable and reliable cast parts for equipment, further stimulating market growth.

Moreover, the increasing focus on lightweight materials and fuel efficiency, especially in the automotive and aerospace industries, necessitates the use of complex and intricate cast designs. Advanced foundry binders are crucial for achieving these complex geometries with minimal defects. Concurrently, stringent environmental regulations globally are pushing manufacturers towards eco-friendly and low-emission binder systems. This regulatory pressure acts as a significant driver for innovation, encouraging the development and adoption of sustainable binder technologies that align with environmental compliance while maintaining high performance standards.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Automotive and Heavy Machinery Industries | +1.5% | Global, particularly Asia Pacific (China, India), North America, Europe | 2025-2033 |

| Increasing Demand for Lightweight and Complex Castings | +1.2% | North America, Europe, Asia Pacific (Japan, South Korea) | 2025-2033 |

| Stringent Environmental Regulations and Sustainability Initiatives | +1.0% | Europe, North America, Asia Pacific (China, India) | 2025-2033 |

| Technological Advancements in Foundry Processes | +0.8% | Global, especially developed economies | 2025-2033 |

| Infrastructure Development and Industrialization in Emerging Economies | +0.7% | Asia Pacific (Southeast Asia), Latin America, MEA | 2025-2033 |

Foundry Binder Market Restraints Analysis

Despite robust growth drivers, the Foundry Binder Market faces several notable restraints that can impede its full potential. One of the primary concerns is the volatility in raw material prices. The production of many foundry binders relies on petrochemical derivatives and other chemical compounds, whose costs are susceptible to fluctuations in global oil prices and supply chain disruptions. This unpredictability in raw material costs directly impacts the production expenses for binder manufacturers, potentially leading to increased end-product prices and affecting profit margins for foundries.

Another significant restraint is the high energy consumption associated with certain foundry processes, particularly those involving high-temperature curing or drying of molds. Foundries are energy-intensive operations, and rising energy costs, coupled with a global push towards energy efficiency and decarbonization, place considerable pressure on the industry. This can increase operational expenditure, making it challenging for foundries to adopt more expensive, albeit advanced, binder systems without significant capital investment. Additionally, the stringent environmental regulations, while a driver for sustainable binders, can also act as a restraint due to the high compliance costs and the complexity of implementing new, eco-friendly processes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.9% | Global, all regions impacted by commodity markets | 2025-2033 |

| High Energy Consumption in Foundry Processes | -0.7% | Europe, North America, parts of Asia Pacific (high energy costs) | 2025-2033 |

| Stringent Environmental Regulations and Compliance Costs | -0.6% | Europe, North America, East Asia | 2025-2033 |

| Competition from Alternative Manufacturing Technologies | -0.5% | Developed Economies (e.g., additive manufacturing) | 2025-2033 |

| Disposal Challenges of Spent Foundry Sand | -0.4% | Global, particularly densely populated industrial areas | 2025-2033 |

Foundry Binder Market Opportunities Analysis

The Foundry Binder Market presents compelling opportunities for growth and innovation, particularly in the development and widespread adoption of sustainable and environmentally friendly binder solutions. With increasing global awareness and regulatory pressures concerning industrial emissions and waste, there is a significant demand for bio-based binders, inorganic binders, and binder systems with low VOC (Volatile Organic Compound) emissions. Companies investing in research and development for such green alternatives are poised to capture a larger market share as industries shift towards more sustainable manufacturing practices. This trend aligns with corporate sustainability goals and offers a competitive edge in environmentally conscious markets.

Furthermore, the expansion of industrial manufacturing capabilities in emerging economies, particularly across Asia Pacific, Latin America, and parts of Africa, offers substantial untapped market potential. These regions are experiencing rapid urbanization, infrastructure development, and industrial growth, leading to an increased demand for cast components across various sectors. As these economies industrialize, the need for advanced foundry technologies, including high-performance binders, will escalate. Additionally, the continuous advancements in foundry automation and the integration of smart manufacturing technologies create opportunities for specialized binders that complement these high-tech processes, enhancing efficiency and product quality.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Eco-friendly and Bio-based Binders | +1.3% | Global, particularly Europe, North America, Asia Pacific | 2025-2033 |

| Expansion in Emerging Economies and Industrialization | +1.1% | Asia Pacific (China, India, Southeast Asia), Latin America | 2025-2033 |

| Increasing Demand for Specialty and High-Performance Castings | +0.9% | Global, especially automotive, aerospace, medical sectors | 2025-2033 |

| Integration of Automation and Digital Technologies in Foundries | +0.8% | Developed Economies, advanced foundries globally | 2025-2033 |

| Recycling and Reclamation of Foundry Sand | +0.7% | Global, particularly regions with strict waste management | 2025-2033 |

Foundry Binder Market Challenges Impact Analysis

The Foundry Binder Market faces significant challenges, notably related to the efficient and environmentally responsible disposal of spent foundry sand. Spent sand, often contaminated with binder residues and other impurities, poses an environmental concern and a logistical challenge for foundries. While efforts are ongoing to promote reuse and recycling, a substantial portion still ends up in landfills, leading to environmental impact and increased operational costs for disposal. This challenge necessitates continuous innovation in binder chemistry to facilitate easier sand reclamation or the development of binders that leave benign residues.

Another critical challenge is the intense competition from alternative manufacturing processes, such as forging, machining, and increasingly, additive manufacturing (3D printing). While casting remains a cost-effective method for mass production of complex shapes, these alternative technologies offer specific advantages in terms of design flexibility, lead times, or material waste for certain applications. Foundries and binder manufacturers must continuously innovate to highlight the unique benefits of casting and ensure that binders support these advantages. Additionally, the foundry industry faces a persistent shortage of skilled labor, which impacts the adoption of new technologies and the efficient operation of complex casting processes, including the proper handling and application of advanced binders.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Disposal and Environmental Impact of Spent Foundry Sand | -0.8% | Global, particularly densely populated industrial zones | 2025-2033 |

| Competition from Alternative Manufacturing Technologies | -0.7% | Developed economies, high-precision manufacturing sectors | 2025-2033 |

| Shortage of Skilled Labor in the Foundry Industry | -0.6% | North America, Europe, parts of Asia Pacific | 2025-2033 |

| High Capital Investment for New Technologies and Compliance | -0.5% | Global, smaller foundries particularly affected | 2025-2033 |

| Fluctuations in Energy Costs and Supply Chain Disruptions | -0.4% | Global, particularly Europe and energy-dependent regions | 2025-2033 |

Foundry Binder Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Foundry Binder Market, covering its current size, historical performance from 2019 to 2023, and a detailed forecast extending to 2033. The scope includes a thorough examination of market drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. Key market trends, segmentation by binder type, process, and end-use industry, along with a granular regional analysis, are meticulously presented to provide a holistic view of the market landscape. The report also profiles leading companies, highlighting their competitive strategies and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.90 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ashland, ASK Chemicals, Vesuvius (Foseco), Hüttenes-Albertus, HA-International, Georgia-Pacific, Ivanhoe Industries, Imerys, KAO Corporation, BASF (Chemetall), Quaker Houghton, Voxeljet, Magna Industrial, Shandong Kaiyuan, Elkem ASA, Refratechnik. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Foundry Binder Market is comprehensively segmented by type, process, and end-use industry to provide a granular understanding of its diverse landscape and market dynamics. This segmentation allows for precise analysis of market performance across different product categories and application methods, revealing specific growth pockets and evolving preferences. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions, aligning with the specific needs of various foundry operations and industries.

By dissecting the market along these lines, the report offers detailed insights into the dominance of certain binder types, the prevalence of particular casting processes, and the varying demands from key industrial consumers. For instance, the demand for organic binders often correlates with specific performance requirements, while inorganic binders gain traction due to their environmental advantages. Similarly, the choice of casting process dictates the type of binder required, influencing market share distribution. The end-use industry segmentation provides a clear picture of demand drivers, showcasing how growth in sectors like automotive or heavy machinery directly impacts the consumption of specific foundry binders.

- By Type:

- Organic Binders: Dominate due to versatility and performance, including Phenolic Resins, Furan Resins, Urethane Binders, Acrylic Binders, and Epoxy Binders.

- Inorganic Binders: Gaining traction for environmental benefits, such as Silicate Binders, Phosphate Binders, Ceramic Binders, and Geopolymer Binders.

- By Process:

- No-Bake Process: Widely used for its flexibility and high precision.

- Cold Box Process: Valued for speed and production efficiency.

- Hot Box Process: Preferred for high-volume production of smaller castings.

- Green Sand Process: Traditional and most common for its cost-effectiveness.

- Shell Molding Process: Utilized for intricate designs and high surface finish.

- By End-Use Industry:

- Automotive: Largest consumer due to demand for engine components, chassis, and body parts.

- Heavy Machinery: Significant segment including construction, agriculture, and mining equipment.

- Aerospace & Defense: Growing demand for lightweight, high-strength components.

- Industrial Equipment: Diverse applications across manufacturing and processing.

- Energy & Power: Castings for turbines, valves, and other power generation components.

Regional Highlights

The Foundry Binder Market exhibits distinct regional dynamics, influenced by varying industrial landscapes, regulatory frameworks, and economic development levels. Asia Pacific stands out as the largest and fastest-growing market, primarily driven by rapid industrialization and significant investments in manufacturing sectors, particularly in China and India. These countries are global hubs for automotive production, heavy machinery manufacturing, and infrastructure development, leading to immense demand for cast components and, consequently, foundry binders. Furthermore, the region is witnessing increasing adoption of advanced foundry technologies to meet stringent quality requirements and environmental standards.

North America and Europe represent mature markets with a strong focus on technological advancements, high-performance binders, and sustainable solutions. In these regions, the emphasis is on developing eco-friendly binder systems, improving casting efficiency through automation, and serving specialized industries like aerospace and advanced automotive. While growth rates may be more moderate compared to Asia Pacific, these regions lead in innovation and premium product adoption. Latin America and the Middle East & Africa (MEA) are emerging markets, showing steady growth propelled by developing industrial bases and infrastructure projects, although their market shares are currently smaller compared to the leading regions. Each region contributes uniquely to the global market, reflecting localized industry trends and regulatory environments.

- Asia Pacific: Dominates the market due to robust growth in China, India, and Southeast Asian countries. Characterized by expansive automotive, construction, and manufacturing industries, coupled with increasing adoption of modern foundry practices and environmental regulations.

- North America: A mature market with a strong emphasis on high-performance binders for automotive, aerospace, and general industrial applications. Driven by technological innovation, automation, and a growing focus on environmentally compliant solutions.

- Europe: A significant market focusing on sustainability, advanced binder chemistries, and stringent environmental regulations. Germany, France, and the UK are key contributors, driven by precision engineering, automotive, and machinery sectors.

- Latin America: An emerging market showing consistent growth, particularly in Brazil and Mexico, fueled by automotive manufacturing and industrial development. Increasing foreign investments contribute to market expansion.

- Middle East & Africa (MEA): A smaller but growing market, influenced by infrastructure development, energy sector investments, and industrial diversification initiatives. Saudi Arabia, UAE, and South Africa are notable contributors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Foundry Binder Market.- Ashland Global Holdings Inc.

- ASK Chemicals GmbH

- Vesuvius Plc (Foseco)

- Hüttenes-Albertus Chemische Werke GmbH

- HA-International LLC

- Georgia-Pacific Chemicals LLC

- Ivanhoe Industries, Inc.

- Imerys S.A.

- Kao Corporation

- BASF SE (Chemetall)

- Quaker Houghton

- Voxeljet AG

- Magna Industrial Co. Limited

- Shandong Kaiyuan Chemical Co., Ltd.

- Elkem ASA

- Refratechnik Group

- Sumitomo Bakelite Co., Ltd.

- Mitsubishi Chemical Corporation

- Lanxess AG

- DSM-Firmenich AG

Frequently Asked Questions

Analyze common user questions about the Foundry Binder market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are foundry binders and why are they important in metal casting?

Foundry binders are chemical agents used to bind sand grains together to form molds and cores for metal casting. They are crucial as they provide the necessary strength, stability, and permeability to the sand mold, ensuring precise dimensions and a smooth surface finish for the cast metal parts, which is essential for quality and efficiency in manufacturing processes.

What are the primary types of foundry binders used today?

The primary types of foundry binders include organic and inorganic binders. Organic binders, such as phenolic, furan, and urethane resins, offer high strength and flexibility. Inorganic binders, like silicates and phosphates, are gaining popularity due to their environmental benefits, producing fewer emissions and making sand reclamation easier, aligning with sustainability trends.

Which industries are the major consumers of foundry binders?

The automotive industry is the largest consumer of foundry binders, requiring numerous cast components for engines, transmissions, and structural parts. Other major consumers include the heavy machinery industry (construction, agriculture, mining equipment), aerospace and defense, railway, and industrial equipment sectors, all relying on durable and precisely manufactured metal castings.

What are the key trends shaping the future of the foundry binder market?

Key trends include a strong shift towards eco-friendly and bio-based binder systems, driven by environmental regulations and corporate sustainability goals. Additionally, increasing automation and digitalization in foundries, the demand for high-performance binders for lightweight and complex castings, and advancements in binder recycling technologies are significant future drivers.

How do environmental regulations impact the foundry binder market?

Environmental regulations significantly impact the market by driving the demand for binders with lower emissions, particularly reduced volatile organic compounds (VOCs). This pushes manufacturers to develop and adopt more sustainable, low-odor, and inorganic binder solutions, influencing product innovation, market preferences, and compliance costs for foundries globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted