Marine Reinsurance Market

Marine Reinsurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705076 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

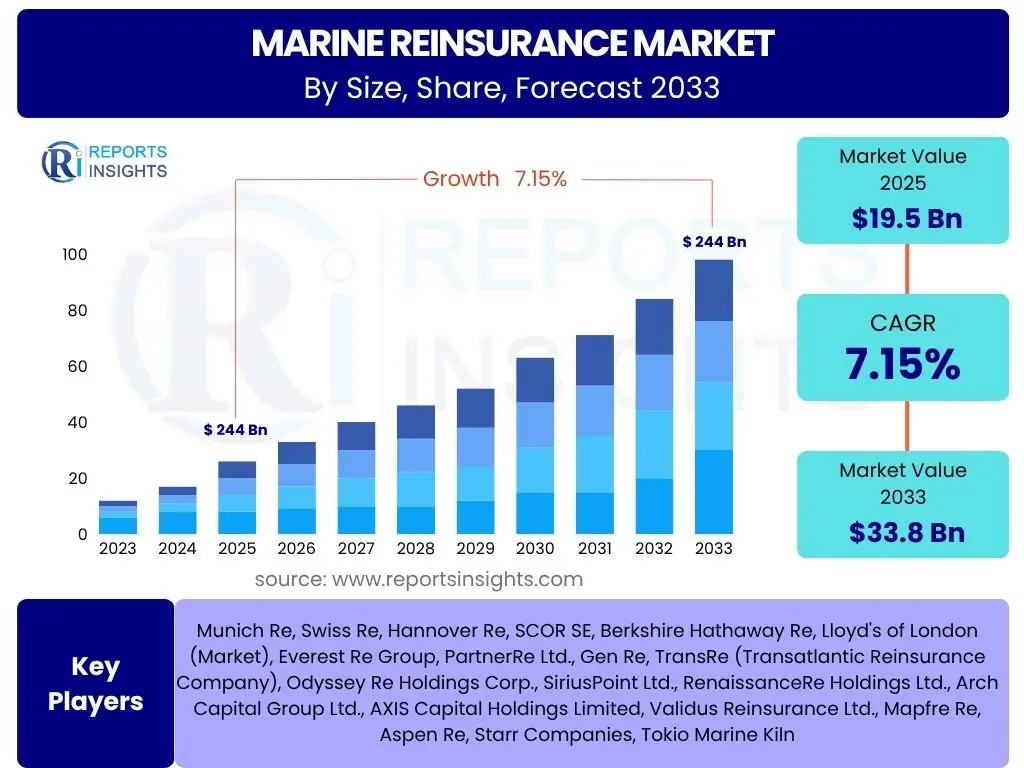

Marine Reinsurance Market Size

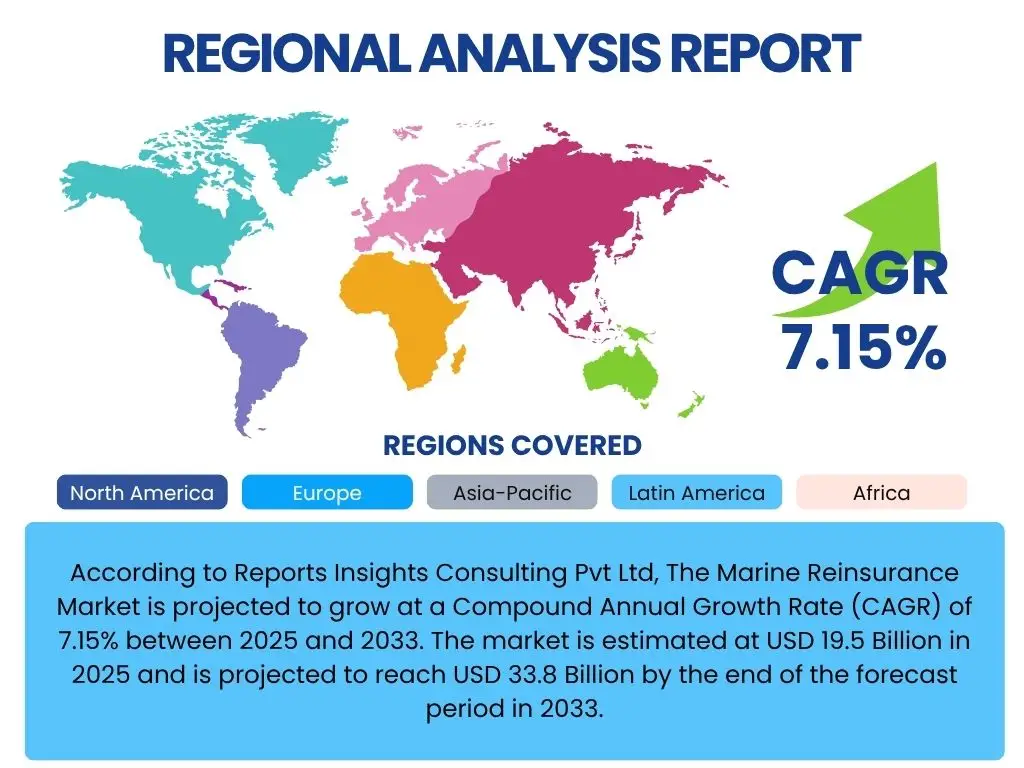

According to Reports Insights Consulting Pvt Ltd, The Marine Reinsurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.15% between 2025 and 2033. The market is estimated at USD 19.5 Billion in 2025 and is projected to reach USD 33.8 Billion by the end of the forecast period in 2033.

Key Marine Reinsurance Market Trends & Insights

User inquiries frequently center on the evolving landscape of global trade, the impact of climate change, and the role of digitalization within the marine reinsurance sector. Analysis reveals that the market is currently shaped by a complex interplay of environmental, technological, and geopolitical factors. The increasing frequency and severity of extreme weather events necessitate more sophisticated risk modeling, while advancements in shipping technology introduce both new efficiencies and novel perils. Furthermore, the global interconnectedness of supply chains means that localized disruptions can have far-reaching consequences, driving demand for comprehensive and adaptive reinsurance solutions.

A key insight is the growing emphasis on data-driven underwriting and claims management. Reinsurers are increasingly leveraging advanced analytics, satellite imagery, and IoT data to gain a more granular understanding of risks, optimize pricing, and accelerate claims processing. This shift towards more predictive and proactive risk management is a significant trend, allowing for better capital allocation and more stable market conditions. Concurrently, the push for sustainable shipping practices and the development of alternative fuels are emerging as long-term trends that will gradually reshape the risk profile of the marine industry, requiring reinsurers to innovate their product offerings.

- Escalating frequency and severity of natural catastrophes (e.g., hurricanes, typhoons).

- Integration of advanced data analytics and artificial intelligence for risk assessment.

- Increased global trade volumes and complexity, driving demand for robust coverage.

- Emergence of new risk exposures from autonomous vessels and cyber threats.

- Growing focus on environmental, social, and governance (ESG) factors in underwriting.

AI Impact Analysis on Marine Reinsurance

Common user questions regarding AI's impact on marine reinsurance highlight a blend of anticipation for efficiency gains and concerns about data privacy and algorithmic bias. The overarching expectation is that AI will revolutionize traditional processes, enabling more precise risk assessment, faster claims handling, and improved fraud detection. Users are keenly interested in how machine learning models can analyze vast datasets, including meteorological patterns, shipping routes, vessel performance, and historical claims data, to generate predictive insights that were previously unattainable. This capability promises to enhance underwriting accuracy, allowing reinsurers to price risks more effectively and reduce losses.

However, the analysis also reveals concerns about the ethical implications of AI, particularly regarding the transparency of algorithms and potential for discriminatory outcomes if not properly managed. There is a strong interest in understanding how AI will affect human roles within the industry, whether it will lead to job displacement or rather augment human expertise, creating new roles focused on data interpretation and model oversight. Despite these considerations, the consensus points towards AI becoming an indispensable tool for managing the complex and dynamic risks inherent in the marine sector, fostering greater efficiency and resilience across the market. The ability of AI to monitor real-time conditions and adapt risk models swiftly is seen as a crucial advantage in a volatile global environment.

- Enhanced predictive analytics for improved risk modeling and pricing.

- Automation of routine tasks in underwriting and claims processing.

- Advanced fraud detection capabilities through pattern recognition.

- Real-time monitoring of maritime conditions and vessel performance.

- Development of personalized and dynamic reinsurance products.

Key Takeaways Marine Reinsurance Market Size & Forecast

User queries regarding key takeaways from the marine reinsurance market size and forecast consistently focus on identifying the primary growth drivers, understanding the market's resilience to global shocks, and pinpointing areas of significant opportunity. The overarching insight is that the market is poised for steady growth, driven by an expansion in global trade and the increasing value and complexity of maritime assets. Despite periods of volatility, particularly from catastrophic events and economic downturns, the fundamental necessity of marine reinsurance for global commerce ensures its continued relevance and expansion. The forecast indicates a robust trajectory, suggesting that stakeholders must prepare for an environment characterized by both evolving risks and technological innovation.

Another crucial takeaway is the growing importance of adaptability and innovation for market participants. The landscape of marine risk is continuously changing, influenced by factors such as climate change, geopolitical tensions, and rapid technological advancements in shipping. Successful entities in this market will be those that can swiftly develop new products, leverage advanced data analytics for superior risk assessment, and foster strong client relationships. The market’s resilience is also underscored by the ability of reinsurers to absorb significant losses from major events, demonstrating their critical role in stabilizing the global marine insurance ecosystem. This underscores the robust demand for diversified and sophisticated reinsurance capacity.

- Steady market growth driven by expanding global trade and increasing asset values.

- Resilience to market shocks, underpinned by fundamental demand for risk transfer.

- Critical need for advanced analytics and technology adoption for competitive advantage.

- Emergence of new risk types (e.g., cyber, autonomous vessels) creating growth niches.

- Increasing pressure to integrate environmental, social, and governance (ESG) considerations.

Marine Reinsurance Market Drivers Analysis

The marine reinsurance market is propelled by a confluence of factors, primarily the expansion of global trade and the increasing complexity and value of maritime assets. As international commerce continues to grow, particularly with emerging economies playing a larger role, the volume of goods transported by sea escalates, inherently increasing the demand for insurance and, subsequently, reinsurance coverage. This expansion is not limited to traditional cargo but extends to highly specialized vessels, advanced offshore energy infrastructure, and increasingly valuable container ships, all requiring substantial reinsurance capacity to protect against potential losses.

Furthermore, the escalating frequency and severity of natural catastrophic events, often linked to climate change, significantly drive the demand for marine reinsurance. These events, ranging from hurricanes impacting coastal infrastructure to tsunamis affecting port operations, necessitate robust reinsurance protection to mitigate the financial impact on primary insurers. Technological advancements in shipping, such as the development of larger vessels and sophisticated navigation systems, while enhancing efficiency, also introduce new and concentrated risk exposures that require substantial risk transfer mechanisms. This constant evolution of risks and assets fuels the continuous need for specialized marine reinsurance solutions to maintain market stability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Global Trade and Maritime Activity | +1.5% | Global, particularly Asia Pacific & Emerging Markets | Long-term (2025-2033) |

| Increasing Value and Complexity of Insured Assets | +1.2% | Global, major shipping hubs | Mid-term (2027-2033) |

| Rising Frequency and Severity of Catastrophic Events | +1.0% | Global, vulnerable coastal regions | Ongoing (2025-2033) |

| Technological Advancements in Shipping (e.g., larger vessels, IoT) | +0.8% | Global, technologically advanced maritime nations | Mid-term (2026-2033) |

| Increased Focus on Regulatory Compliance and Risk Management | +0.6% | Europe, North America, key maritime jurisdictions | Short-term (2025-2027) |

Marine Reinsurance Market Restraints Analysis

The marine reinsurance market faces several significant restraints that can temper its growth trajectory. One primary restraint is the inherent cyclicality of the reinsurance market itself, which often experiences periods of soft market conditions characterized by intense competition and depressed pricing. Excess capital flowing into the reinsurance sector can lead to an oversupply of capacity, driving down premium rates and reducing profitability for reinsurers. This competitive pressure makes it challenging for reinsurers to maintain robust underwriting margins, particularly in a segment that can be prone to large, infrequent losses.

Another significant restraint is the global economic downturns and geopolitical uncertainties. Fluctuations in global trade volumes, often a direct consequence of economic slowdowns, directly impact the demand for marine insurance and, by extension, reinsurance. Geopolitical tensions, trade wars, and sanctions can disrupt established shipping routes, reduce maritime activity in certain regions, and introduce unpredictable risks, thereby creating market instability and making risk assessment more complex. Additionally, regulatory complexities across different jurisdictions, coupled with evolving international maritime laws, can create compliance burdens and restrict market access for some reinsurers, further acting as a decelerating force on market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Market Cyclicality | -0.9% | Global, mature markets (Europe, North America) | Ongoing (2025-2033) |

| Global Economic Volatility and Trade Slowdowns | -0.8% | Global, major trading nations (China, EU, US) | Short-term to Mid-term (2025-2028) |

| Accumulation of Risks and Exposure to Mega-Catastrophes | -0.7% | Global, high-risk coastal zones | Ongoing (2025-2033) |

| Regulatory Hurdles and Compliance Costs | -0.5% | Specific jurisdictions (e.g., EU, UK, US) | Long-term (2025-2033) |

| Technological Disruption and Data Security Concerns | -0.4% | Global, technologically advanced regions | Mid-term (2026-2030) |

Marine Reinsurance Market Opportunities Analysis

The marine reinsurance market presents numerous opportunities driven by evolving global dynamics and technological advancements. One significant area of opportunity lies in emerging markets, particularly in Asia Pacific, Latin America, and the Middle East and Africa. Rapid industrialization, increasing trade volumes, and infrastructure development in these regions are fueling substantial demand for marine insurance, which in turn creates a corresponding need for robust reinsurance capacity. As these economies mature and integrate further into global supply chains, the complexity and value of their maritime assets will continue to rise, offering fertile ground for reinsurers to expand their portfolios and develop tailored solutions.

Furthermore, the emergence of new and specialized risks provides considerable opportunities for innovation and growth. Risks associated with cyberattacks on maritime infrastructure, the development and operation of autonomous vessels, and the transition to alternative fuels (e.g., LNG, hydrogen) in shipping represent new frontiers for coverage. Reinsurers capable of developing sophisticated underwriting models and offering bespoke products for these nascent risk areas will gain a competitive edge. The increasing adoption of parametric insurance solutions, which pay out based on predefined triggers rather than traditional loss assessment, also offers an opportunity to streamline claims processes and attract clients seeking faster and more transparent settlements in the face of escalating weather-related events.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets and Developing Economies | +1.3% | Asia Pacific, Latin America, MEA | Long-term (2026-2033) |

| Development of New Coverage for Emerging Risks (Cyber, Autonomous Vessels) | +1.1% | Global, technologically advanced maritime hubs | Mid-term (2027-2033) |

| Leveraging Advanced Analytics and AI for Product Innovation | +0.9% | Global, tech-forward companies | Ongoing (2025-2033) |

| Growth in Offshore Renewable Energy Projects | +0.7% | Europe, North America, Asia Pacific coastal regions | Long-term (2028-2033) |

| Demand for Parametric Insurance Solutions for Catastrophic Events | +0.6% | Global, particularly high-risk zones | Mid-term (2026-2030) |

Marine Reinsurance Market Challenges Impact Analysis

The marine reinsurance market contends with several persistent challenges that require strategic navigation. One significant challenge is the inherent volatility of catastrophic losses, which can lead to substantial claims and impact underwriting profitability, especially when multiple severe events occur within a short period. The increasing frequency and intensity of natural disasters, exacerbated by climate change, mean that reinsurers face higher exposures and greater difficulty in accurately modeling future losses. This climate-related uncertainty puts pressure on capital adequacy and risk appetite, potentially leading to capacity constraints in certain high-risk zones.

Another critical challenge is the intense pricing pressure driven by overcapacity and fierce competition within the global reinsurance market. While consolidation helps some players, the broader market often struggles with soft pricing conditions that erode margins and make it difficult to achieve sustainable profitability, particularly in standard lines of business. Furthermore, geopolitical instability and trade protectionism pose substantial challenges by disrupting established trade routes, increasing war risk premiums, and introducing complexities in international sanctions compliance. These external factors are unpredictable and can swiftly alter the risk landscape, making long-term planning and portfolio management exceptionally demanding for marine reinsurers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Catastrophic Losses and Climate Change Impact | -1.0% | Global, low-lying coastal areas | Ongoing (2025-2033) |

| Persistent Soft Market Conditions and Pricing Pressure | -0.9% | Global, especially mature markets | Short-term to Mid-term (2025-2029) |

| Geopolitical Instability and Supply Chain Disruptions | -0.8% | Specific conflict zones, major shipping lanes | Ongoing (2025-2033) |

| Talent Shortage in Underwriting and Actuarial Roles | -0.6% | Global, developed insurance markets | Long-term (2025-2033) |

| Data Privacy and Cybersecurity Risks for Digital Platforms | -0.5% | Global, highly digitalized firms | Ongoing (2025-2033) |

Marine Reinsurance Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Marine Reinsurance Market, offering critical insights into market size, growth projections, key trends, drivers, restraints, opportunities, and challenges. It segments the market by reinsurance type, coverage type, end-user, and distribution channel, providing a granular view of market dynamics. Furthermore, the report includes a detailed regional analysis and profiles of leading market participants, equipping stakeholders with the knowledge necessary for strategic decision-making and competitive advantage in this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 33.8 Billion |

| Growth Rate | 7.15% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Munich Re, Swiss Re, Hannover Re, SCOR SE, Berkshire Hathaway Re, Lloyd's of London (Market), Everest Re Group, PartnerRe Ltd., Gen Re, TransRe (Transatlantic Reinsurance Company), Odyssey Re Holdings Corp., SiriusPoint Ltd., RenaissanceRe Holdings Ltd., Arch Capital Group Ltd., AXIS Capital Holdings Limited, Validus Reinsurance Ltd., Mapfre Re, Aspen Re, Starr Companies, Tokio Marine Kiln |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Marine Reinsurance Market is extensively segmented to provide a granular understanding of its diverse components, reflecting the varied nature of marine risks and the specialized requirements of different market participants. These segmentations allow for a detailed examination of market dynamics across different types of reinsurance arrangements, specific coverage needs, end-user applications, and distribution methodologies. This multi-faceted approach ensures that all critical dimensions of the market are thoroughly analyzed, from the foundational mechanisms of risk transfer to the specialized needs of specific industries within the maritime sector.

Understanding these segments is crucial for identifying growth opportunities, assessing competitive landscapes, and tailoring strategic initiatives. For instance, the distinction between facultative and treaty reinsurance highlights different risk-sharing approaches, while the various coverage types like Hull & Machinery or Offshore Energy reflect the diverse asset classes and perils involved. Similarly, analyzing end-users provides insights into the primary demand drivers, and examining distribution channels illuminates how reinsurance products reach their ultimate beneficiaries, all contributing to a comprehensive market overview and enabling targeted business strategies.

- By Reinsurance Type:

- Facultative Reinsurance: Tailored coverage for individual risks.

- Treaty Reinsurance: Covers a portfolio of risks under pre-agreed terms.

- By Coverage Type:

- Hull & Machinery: Covers physical damage to vessels.

- Cargo: Covers loss or damage to goods in transit.

- Protection & Indemnity (P&I): Covers third-party liabilities arising from vessel operation.

- Marine Liability: Broader liability coverage beyond P&I.

- Offshore Energy: Covers risks associated with oil, gas, and renewable energy installations at sea.

- Other Marine Lines: Includes war risks, kidnap & ransom, and other specialty coverages.

- By End-User:

- Ship Owners & Operators: Primary beneficiaries of hull and liability coverage.

- Logistics & Freight Forwarders: Seek cargo and liability coverage for goods movement.

- Offshore Energy Companies: Require specialized coverage for offshore assets and operations.

- Marine Service Providers: Include salvage, port services, and other support entities.

- Port Authorities: Insure against risks associated with port operations and infrastructure.

- Other Businesses: Various other entities with marine-related exposures.

- By Distribution Channel:

- Reinsurance Brokers: Facilitate placement of reinsurance contracts between cedents and reinsurers.

- Direct Reinsurers: Engage directly with primary insurers without an intermediary.

Regional Highlights

- North America: The market is characterized by a mature insurance landscape and a significant presence of large shipping companies and offshore energy operations, particularly in the Gulf of Mexico. It is heavily influenced by the frequency of hurricanes and the complexities of U.S. regulatory frameworks. Innovation in data analytics and risk modeling is a strong regional driver.

- Europe: Home to some of the world's oldest and most established maritime insurance markets, notably Lloyd's of London, Europe remains a critical hub for marine reinsurance. Strong regulatory environments, a large shipping fleet, and a leading role in offshore wind energy development contribute significantly to market demand. Scandinavia, Germany, and the UK are key contributors.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, driven by booming international trade, rapid port infrastructure development, and increasing shipbuilding activities, especially in China, Japan, South Korea, and Singapore. The rising affluence and expanding manufacturing bases are fueling unprecedented demand for marine insurance and reinsurance solutions.

- Latin America: Growth in this region is propelled by increasing commodity exports, expanding port capacities, and investments in offshore energy exploration, particularly in Brazil and Mexico. While smaller than other regions, it offers significant potential due to developing economies and increasing integration into global supply chains.

- Middle East & Africa (MEA): The MEA region's marine reinsurance market is primarily driven by its strategic location as a global shipping artery and significant oil & gas exports. Investments in port infrastructure and diversification efforts in economies like the UAE and Saudi Arabia are creating new demand. However, geopolitical risks and regional conflicts can pose considerable challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Marine Reinsurance Market.- Munich Re

- Swiss Re

- Hannover Re

- SCOR SE

- Berkshire Hathaway Re

- Lloyd's of London (Market)

- Everest Re Group

- PartnerRe Ltd.

- Gen Re

- TransRe (Transatlantic Reinsurance Company)

- Odyssey Re Holdings Corp.

- SiriusPoint Ltd.

- RenaissanceRe Holdings Ltd.

- Arch Capital Group Ltd.

- AXIS Capital Holdings Limited

- Validus Reinsurance Ltd.

- Mapfre Re

- Aspen Re

- Starr Companies

- Tokio Marine Kiln

Frequently Asked Questions

What is marine reinsurance?

Marine reinsurance is a contract through which one insurer (the ceding insurer) transfers a portion of its marine insurance risks to another insurer (the reinsurer). This process helps the primary insurer manage its exposure to large or catastrophic losses arising from maritime activities, ensuring financial stability and enabling it to underwrite more policies.

How is climate change impacting marine reinsurance?

Climate change significantly impacts marine reinsurance by increasing the frequency and severity of extreme weather events, such as hurricanes, typhoons, and floods. This leads to higher claims payouts for catastrophic losses, necessitating more sophisticated risk modeling, higher capital reserves for reinsurers, and potentially driving up reinsurance premiums.

What are the primary types of marine reinsurance?

The primary types of marine reinsurance are Facultative Reinsurance, which covers individual, specific risks, and Treaty Reinsurance, which covers a predefined portfolio of risks. Key coverage types include Hull & Machinery, Cargo, Protection & Indemnity (P&I), Marine Liability, and Offshore Energy, each addressing different aspects of marine risk.

What role does technology play in marine reinsurance?

Technology plays an increasingly crucial role in marine reinsurance by enabling enhanced data analytics, AI-driven risk assessment, real-time monitoring of vessels and weather conditions, and automation of underwriting and claims processes. This leads to more accurate pricing, faster responses, and improved fraud detection, driving efficiency and innovation across the market.

What are the growth prospects for the marine reinsurance market?

The marine reinsurance market is projected for steady growth, driven by expanding global trade volumes, increasing value and complexity of maritime assets, and the escalating need for robust coverage against catastrophic events. Emerging markets and the development of new risk solutions for cyber threats and autonomous vessels present significant future opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted