Marine Diesel Market

Marine Diesel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678086 | Last Updated : July 17, 2025 |

Format : ![]()

![]()

![]()

![]()

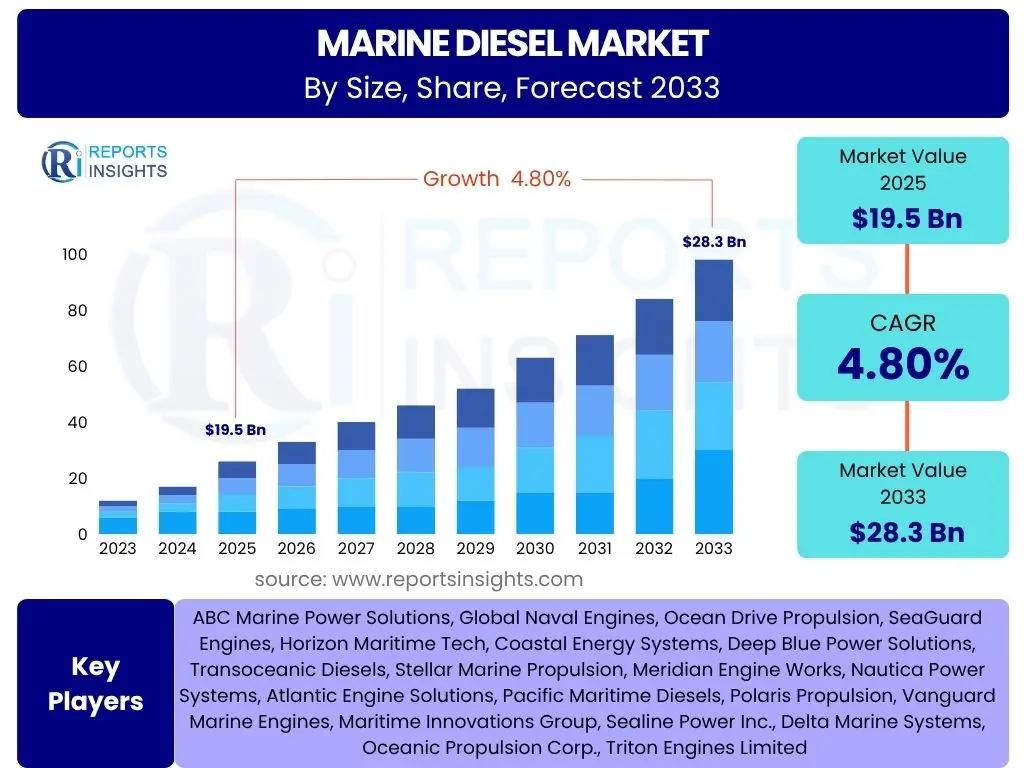

Marine Diesel Market is projected to grow at a Compound annual growth rate (CAGR) of 3.5% between 2025 and 2033, valued at USD 17.5 Billion in 2025 and is projected to grow to USD 23.0 Billion by 2033, the end of the forecast period.

Key Marine Diesel Market Trends & Insights

The Marine Diesel Market is currently undergoing a significant transformation driven by a complex interplay of environmental regulations, technological advancements, and evolving global trade dynamics. While traditional reliance on marine diesel remains strong for many vessel types, the industry is actively exploring cleaner burning fuels and more efficient engine technologies to comply with increasingly stringent emissions standards. This dual approach of optimizing conventional systems and investing in alternative solutions defines the market's current trajectory, balancing immediate operational needs with long-term sustainability goals. The drive towards decarbonization is a foundational trend, influencing everything from vessel design to fuel infrastructure development.

Furthermore, the digitalization of the maritime industry is playing a crucial role in shaping the demand and efficiency of marine diesel. Advanced analytics, real-time monitoring, and predictive maintenance are optimizing fuel consumption and extending engine lifespans, indirectly impacting market demand patterns. Geopolitical shifts and global economic growth also exert considerable influence, as disruptions in trade routes or downturns in global commerce can directly affect shipping volumes and, consequently, marine diesel consumption. Stakeholders are navigating this intricate landscape by seeking operational efficiencies and exploring strategic partnerships to remain competitive and compliant.

- Increasing adoption of low-sulfur marine fuels (VLSFO and ULSFO) in compliance with IMO 2020 regulations.

- Growing demand for Tier III and Tier IV compliant marine diesel engines offering reduced NOx emissions.

- Rise in hybrid propulsion systems integrating diesel engines with electric or battery power for enhanced efficiency.

- Focus on fuel efficiency technologies and optimized engine management systems to reduce operational costs and emissions.

- Expanding global seaborne trade and maritime tourism contributing to sustained demand for marine transportation.

- Technological advancements in engine design, including common rail fuel injection and exhaust gas recirculation (EGR).

- Development of advanced fuel additives aimed at improving combustion efficiency and reducing emissions.

AI Impact Analysis on Marine Diesel

The integration of Artificial Intelligence (AI) across the maritime sector is profoundly influencing the Marine Diesel Market, primarily by optimizing operational efficiencies and extending the lifespan of existing assets. AI-powered analytics can process vast amounts of sensor data from marine engines, providing unprecedented insights into performance, wear, and potential failures. This capability shifts maintenance from a reactive to a predictive model, significantly reducing unscheduled downtime and ensuring engines operate at peak efficiency, thereby optimizing fuel consumption and indirectly influencing demand for marine diesel by making its usage more efficient and cost-effective.

Moreover, AI contributes to route optimization and intelligent cargo management, directly leading to lower fuel consumption per voyage. By leveraging AI algorithms, vessels can identify the most fuel-efficient routes based on real-time weather conditions, ocean currents, and port congestion, minimizing transit times and fuel burn. While AI does not directly replace marine diesel, its application enhances the economic and environmental viability of diesel-powered vessels, ensuring that marine diesel remains a competitive and essential fuel source even as the industry moves towards decarbonization. This efficiency gain allows for a more strategic and sustainable use of marine diesel resources.

- AI-driven predictive maintenance optimizes engine performance and reduces fuel consumption by ensuring optimal operating conditions.

- Machine learning algorithms enhance route optimization, leading to significant fuel savings and reduced marine diesel demand per voyage.

- Real-time data analytics provided by AI systems enable better fuel management and inventory control for marine operators.

- AI supports the development of autonomous vessels, potentially leading to more consistent and fuel-efficient operational profiles.

- AI integration aids in monitoring and optimizing emission control systems, helping diesel engines meet environmental regulations more effectively.

- Intelligent vessel management systems leverage AI to improve overall fleet efficiency, impacting the collective consumption of marine diesel.

Key Takeaways Marine Diesel Market Size & Forecast

- The Marine Diesel Market is projected for steady growth, reflecting continued reliance on this fuel type across various maritime sectors despite decarbonization pressures.

- Market valuation is set to increase from USD 17.5 Billion in 2025 to USD 23.0 Billion by 2033, indicating resilient demand.

- A Compound Annual Growth Rate (CAGR) of 3.5% signifies a stable expansion, driven by global trade volumes and the large existing fleet of diesel-powered vessels.

- Significant market share will continue to be held by traditional segments like cargo and cruise ships, which predominantly rely on marine diesel.

- The forecast period emphasizes the ongoing transition within the industry, with investments in cleaner diesel technologies complementing exploration of alternative fuels.

- Regional growth patterns are expected to vary, with Asia Pacific maintaining its dominance due to high shipbuilding activity and trade volumes.

- Technological advancements aimed at improving fuel efficiency and reducing emissions from diesel engines will be critical to sustaining market growth.

Marine Diesel Market Drivers Impact Analysis

The Marine Diesel Market is significantly driven by several fundamental factors that underscore its continued relevance in global maritime operations. The sustained expansion of global trade and the resultant increase in seaborne cargo volumes necessitate a robust and reliable power source for an ever-growing fleet of vessels. Marine diesel, with its proven reliability, energy density, and established infrastructure, remains the preferred choice for a vast majority of the global shipping industry. The economic imperative to transport goods efficiently across continents continues to be a primary catalyst for demand.

Additionally, the slow pace of adoption and the significant investment required for widespread alternative fuel infrastructure mean that marine diesel will remain indispensable for a considerable period. While cleaner fuels are gaining traction, the vast existing fleet of vessels is designed for diesel, and conversion or replacement presents substantial logistical and financial challenges. The continuous advancements in diesel engine technology, which aim to improve fuel efficiency and reduce emissions, also contribute to its longevity, offering solutions that bridge the gap towards future zero-emission targets. Furthermore, the expansion of niche maritime sectors such as offshore support, fishing, and defense continues to create specialized demand for marine diesel, where its operational characteristics are particularly well-suited.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Seaborne Trade Growth | +1.2% | Asia Pacific, Europe, North America | Short- to Mid-term |

| Increasing Demand for Cargo and Passenger Shipping | +0.9% | Global, particularly emerging economies | Short- to Mid-term |

| Technological Advancements in Diesel Engines | +0.7% | Europe, Asia Pacific (Engine Manufacturing Hubs) | Mid- to Long-term |

| Limited Viability of Alternative Fuel Infrastructure | +0.5% | Global, especially developing regions | Mid- to Long-term |

| Cost-Effectiveness and Reliability of Diesel Propulsion | +0.4% | Global | Short- to Mid-term |

| Growth in Offshore Activities and Specialized Vessels | +0.3% | North Sea, Gulf of Mexico, Asia Pacific, West Africa | Mid-term |

| Military and Defense Naval Vessel Demand | +0.2% | North America, Europe, Asia Pacific | Long-term |

Marine Diesel Market Restraints Impact Analysis

The Marine Diesel Market faces significant headwinds, primarily stemming from the global push for environmental sustainability and stringent regulatory frameworks. The International Maritime Organization (IMO) has implemented increasingly stricter regulations on sulfur oxide (SOx), nitrogen oxide (NOx), and greenhouse gas (GHG) emissions, compelling the shipping industry to reduce its carbon footprint. Compliance with these regulations often necessitates costly technological upgrades to existing diesel engines or a shift towards alternative, cleaner fuels, thereby exerting downward pressure on marine diesel demand. The financial burden of meeting these standards can be substantial for vessel operators, influencing their fuel choices and investment strategies.

Furthermore, the escalating development and adoption of alternative marine fuels, such as Liquefied Natural Gas (LNG), methanol, hydrogen, and various forms of electrification, pose a direct competitive threat to marine diesel. As infrastructure for these alternatives expands and their economic viability improves, a gradual but discernible shift away from traditional diesel is anticipated, especially in new builds and specific vessel segments. Volatility in crude oil prices also acts as a restraint, making long-term planning challenging for operators and sometimes driving a search for more stable, predictable energy sources. Public and investor pressure for greener shipping practices further incentivizes the move away from fossil fuels, creating a complex operating environment for the marine diesel market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations (IMO 2020, EEXI, CII) | -1.5% | Global | Short- to Long-term |

| Increasing Adoption of Alternative Fuels (LNG, Methanol, Hydrogen) | -1.2% | Europe, Asia Pacific, North America (Ports & New Builds) | Mid- to Long-term |

| High Capital Costs for Emission Abatement Technologies (Scrubbers, SCR) | -0.8% | Global | Short- to Mid-term |

| Volatile Crude Oil Prices | -0.6% | Global | Short-term (Fluctuating) |

| Public and Investor Pressure for Decarbonization | -0.4% | Europe, North America | Mid- to Long-term |

| Aging Vessel Fleet Requiring Significant Modernization or Replacement | -0.3% | Global | Long-term |

Marine Diesel Market Opportunities Impact Analysis

Despite the challenges, the Marine Diesel Market presents several notable opportunities driven by ongoing industry developments and strategic innovations. One significant area of opportunity lies in the continuous development of advanced diesel engine technologies that are more fuel-efficient and capable of meeting stricter emission standards. Innovations such as common rail fuel injection systems, advanced turbocharging, and exhaust gas after-treatment solutions like selective catalytic reduction (SCR) and exhaust gas recirculation (EGR) enhance the appeal of diesel, allowing it to remain compliant and competitive even in a decarbonizing environment. These technological leaps ensure that diesel engines can offer improved environmental performance without compromising on power and reliability.

Furthermore, the growing demand for hybrid propulsion systems offers a compelling avenue for marine diesel. In such systems, diesel engines work in conjunction with electric motors or batteries, providing flexibility, reducing fuel consumption in certain operating modes, and enabling vessels to operate in emission-controlled areas. This hybrid approach allows for the retention of diesel's benefits while integrating cleaner power sources. The vast existing global fleet of diesel-powered vessels also represents a significant opportunity for the retrofitting market, providing avenues for engine upgrades, optimization, and the adoption of cleaner marine diesel fuels (e.g., biodiesel blends), extending the operational life and compliance of these assets. Additionally, the increasing focus on the circular economy and sustainable practices can drive demand for advanced biofuels compatible with diesel engines, creating new market niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced & Fuel-Efficient Diesel Engines | +1.0% | Europe, Asia Pacific (Engine Manufacturers) | Mid- to Long-term |

| Increasing Demand for Hybrid Propulsion Systems | +0.8% | Global, particularly coastal shipping | Mid- to Long-term |

| Growth in Retrofitting and Engine Upgrade Market for Existing Vessels | +0.7% | Global (Fleet Owners) | Short- to Mid-term |

| Adoption of Bio-Diesel Blends and Synthetic Marine Fuels | +0.6% | Europe, North America, Countries with strong sustainability goals | Mid- to Long-term |

| Niche Applications Requiring High Power Density & Reliability | +0.5% | Defense, Offshore, Fishing (Specialized Vessels) | Long-term |

| Development of Carbon Capture Technologies for Marine Vessels | +0.4% | Europe, Asia Pacific (Research & Development) | Long-term |

Marine Diesel Market Challenges Impact Analysis

The Marine Diesel Market faces a formidable array of challenges, largely centered around the imperative for environmental compliance and the rapid evolution of alternative energy solutions. The most pressing challenge is navigating the increasingly complex and stringent global regulations aimed at decarbonizing shipping. Meeting targets such as the IMO's 2050 GHG emission reduction goals demands fundamental shifts in propulsion technology and fuel choices, which often bypass conventional diesel. The significant capital expenditure required to upgrade existing vessels with emission reduction technologies, or to invest in new, compliant vessels, presents a considerable financial hurdle for shipping companies, potentially accelerating the transition away from diesel.

Another critical challenge lies in the rapid advancement and growing economic competitiveness of alternative fuels and propulsion systems. While marine diesel offers established reliability, the long-term strategic direction of the maritime industry is clearly moving towards fuels like LNG, methanol, ammonia, and hydrogen, as well as full electrification for shorter routes. This trend poses a direct threat to marine diesel's market dominance, as new builds increasingly opt for dual-fuel capabilities or entirely non-diesel solutions. Furthermore, the volatility of global crude oil prices, which directly impacts the cost of marine diesel, introduces significant operational uncertainty for shipping lines, making it difficult to forecast fuel expenses and eroding profitability. The broader negative perception of fossil fuels and mounting pressure from environmental advocacy groups and financial institutions also compel companies to seek cleaner alternatives, placing marine diesel at a strategic disadvantage.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Evolving Decarbonization Targets (IMO 2050) | -1.8% | Global | Long-term & Strategic |

| Competition from Developing Alternative Fuels & Propulsion | -1.5% | Europe, Asia Pacific (New Building & Infrastructure) | Mid- to Long-term |

| High Investment Required for Fleet Modernization & Conversion | -1.0% | Global | Short- to Mid-term |

| Supply Chain Disruptions Affecting Fuel Availability & Pricing | -0.7% | Global | Short-term (Periodic) |

| Technological Lock-in for Existing Diesel Fleets | -0.5% | Global | Mid- to Long-term |

| Public Perception and Green Finance Pressures | -0.4% | Europe, North America, Investor Hubs | Mid-term |

Marine Diesel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Marine Diesel Market, offering a robust understanding of its current landscape and future growth trajectory. It meticulously segments the market by type, application, end-use industry, and geography, presenting a detailed overview of key trends, drivers, restraints, opportunities, and challenges. The report delivers critical insights into market size, forecast values, and competitive dynamics, empowering stakeholders with the data necessary for strategic decision-making and sustainable growth in the global maritime sector.

| Report Attributes | Report Details |

|---|---|

| Report Name | Marine Diesel Market |

| Market Size in 2025 | USD 17.5 Billion |

| Market Forecast in 2033 | USD 23.0 Billion |

| Growth Rate | CAGR of 2025 to 2033 3.5% |

| Number of Pages | 250 |

| Key Companies Covered | Wartsila, Caterpillar, Mitsubishi, Yanmar, MAN, MES, Hyundai, Doosan, CSSC, Deutz, Niigata Power Systems, Kawasaki Heavy Industries, Rolls-Royce, Volvo Penta, CSIC, Daihatsu, Mhi-mme, WeiCai, STX Engine, RongAn Power |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

Market Product Type Segmentation:-- Low-speed Marine Diesel: Typically used in large cargo vessels and tankers, optimized for fuel efficiency and continuous operation at lower RPMs.

- Medium-speed Marine Diesel: Versatile engines suitable for a wide range of vessels including cruise ships, ferries, and some cargo ships, balancing power and efficiency.

- High-speed Marine Diesel: Primarily used in smaller vessels such as fast ferries, offshore support vessels, yachts, and naval ships, valued for their compact size and high power output.

- Cargo Ship: Dominant application, encompassing container ships, bulk carriers, oil tankers, and general cargo vessels that form the backbone of global trade.

- Cruise Ship: Includes passenger cruise liners and ferries, requiring reliable and efficient power for propulsion and onboard electricity generation.

- Other: This segment comprises specialized vessels such as fishing boats, tugboats, offshore supply vessels, naval ships, research vessels, and governmental patrol boats, each with unique operational demands for marine diesel.

Regional Highlights

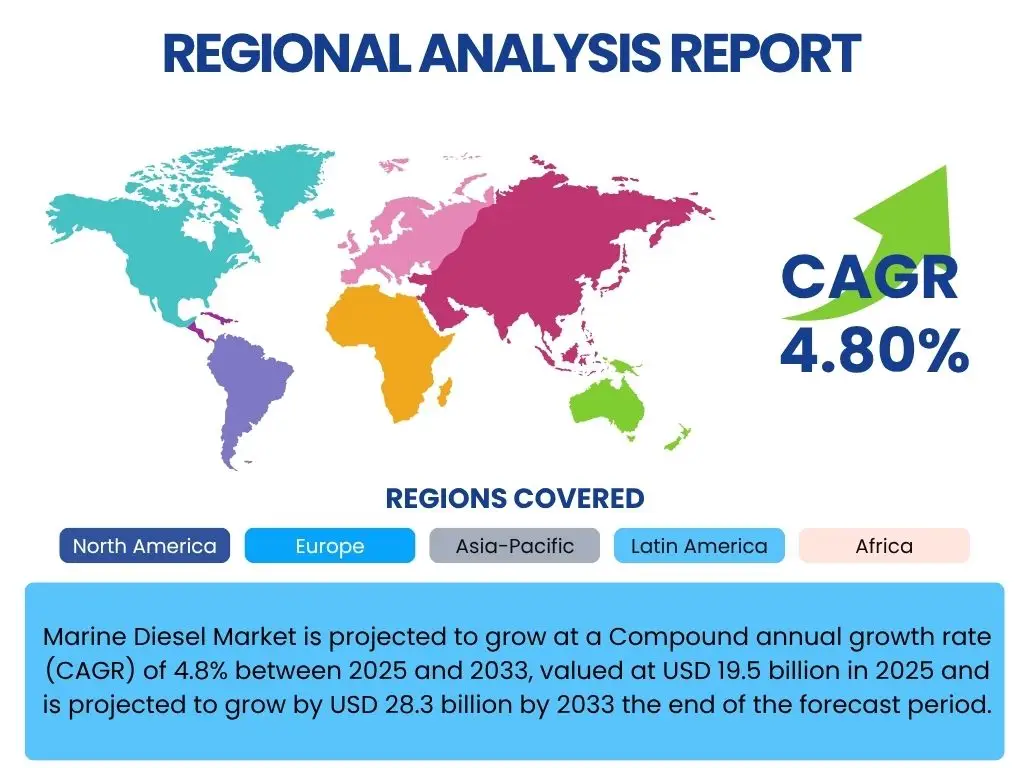

The Marine Diesel Market exhibits diverse regional dynamics, heavily influenced by global trade routes, shipbuilding activity, regulatory environments, and the presence of major maritime industries. Each region contributes uniquely to the market's overall landscape, reflecting varying levels of industrialization, strategic geopolitical importance, and environmental policy implementation. Understanding these regional specificities is crucial for stakeholders aiming to identify key growth pockets and potential challenges, as demand patterns and investment in alternative solutions often differ significantly across geographies.

Asia Pacific remains the undisputed leader in both marine diesel consumption and engine manufacturing, driven by robust shipbuilding industries and the region's central role in global trade and manufacturing. Europe, while also a significant consumer, is at the forefront of implementing stringent environmental regulations and pioneering alternative fuel technologies, influencing the future trajectory of marine propulsion. North America maintains a steady demand, particularly for its domestic maritime trade and offshore activities, while Latin America, and the Middle East and Africa are emerging markets with growing maritime infrastructure and increasing trade volumes.

- Asia Pacific (APAC): The largest and fastest-growing region, driven by extensive shipbuilding activities in countries like China, South Korea, and Japan. High volumes of international trade, booming manufacturing sectors, and increasing domestic maritime transport fuel a consistent demand for marine diesel. Its vast coastal areas and numerous busy ports make it a critical hub for diesel consumption, particularly for cargo ships.

- Europe: A mature market with strong regulatory influence, particularly from the European Union. While demand for marine diesel remains significant, especially for established trade routes and diverse fleet types, the region is a leader in adopting and developing cleaner marine fuels and hybrid propulsion solutions. Countries like Germany, Norway, and the Netherlands are key players in marine engine technology and green shipping initiatives.

- North America: Exhibits stable demand primarily due to its domestic shipping, offshore oil and gas industry, and increasing cruise tourism. The region adheres to strict emission regulations in specific Emission Control Areas (ECAs), promoting the use of cleaner marine diesel or alternative abatement technologies. The Great Lakes and significant coastal trade routes contribute to consistent consumption.

- Latin America: An emerging market with growing maritime trade, particularly in agricultural commodities and mineral exports. Investments in port infrastructure and an expanding fleet, though smaller than other regions, are contributing to an increased demand for marine diesel. Brazil, Mexico, and Argentina are key countries driving this growth.

- Middle East and Africa (MEA): This region is characterized by its strategic location along major global shipping lanes, significant oil and gas exports, and increasing intra-regional trade. Demand for marine diesel is robust due to bunkering activities and the growth of local maritime industries, including offshore support and fishing fleets. The development of port capacities across the Arabian Gulf and Africa further supports market expansion.

Top Key Players:

The market research report covers the analysis of key stake holders of the Marine Diesel Market. Some of the leading players profiled in the report include -:- Wartsila

- Caterpillar

- Mitsubishi

- Yanmar

- MAN

- MES

- Hyundai

- Doosan

- CSSC

- Deutz

- Niigata Power Systems

- Kawasaki Heavy Industries

- Rolls-Royce

- Volvo Penta

- CSIC

- Daihatsu

- Mhi-mme

- WeiCai

- STX Engine

- RongAn Power

Frequently Asked Questions:

What is the current market size of the Marine Diesel Market?

The Marine Diesel Market was valued at USD 17.5 Billion in 2025. This valuation reflects its substantial role in powering global shipping, encompassing various vessel types from large cargo carriers to passenger ships and specialized vessels. The market size is influenced by global trade volumes, fuel prices, and the ongoing transition within the maritime industry towards more sustainable practices, which includes the adoption of cleaner diesel variants and engine technologies. This foundational market size underpins future growth projections and strategic planning for stakeholders.

What is the projected growth rate for the Marine Diesel Market from 2025 to 2033?

The Marine Diesel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.5% between 2025 and 2033. This consistent growth rate indicates a sustained demand for marine diesel, despite increasing regulatory pressures and the emergence of alternative fuels. The growth is primarily driven by the expansion of global seaborne trade, the continued reliance on diesel propulsion for existing fleets, and ongoing technological advancements in diesel engine efficiency. This moderate but steady growth signifies the market's resilience and adaptability within the evolving maritime landscape.

What are the key factors driving the Marine Diesel Market?

Key drivers of the Marine Diesel Market include the robust growth in global seaborne trade and cargo volumes, which necessitate reliable and energy-dense propulsion systems for efficient transportation. The proven cost-effectiveness and operational reliability of diesel engines, combined with the limited widespread infrastructure for alternative marine fuels, continue to bolster its demand. Furthermore, continuous advancements in diesel engine technology, aimed at improving fuel efficiency and reducing emissions, help maintain it

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted