Magnetron Sputtering System Market

Magnetron Sputtering System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709382 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

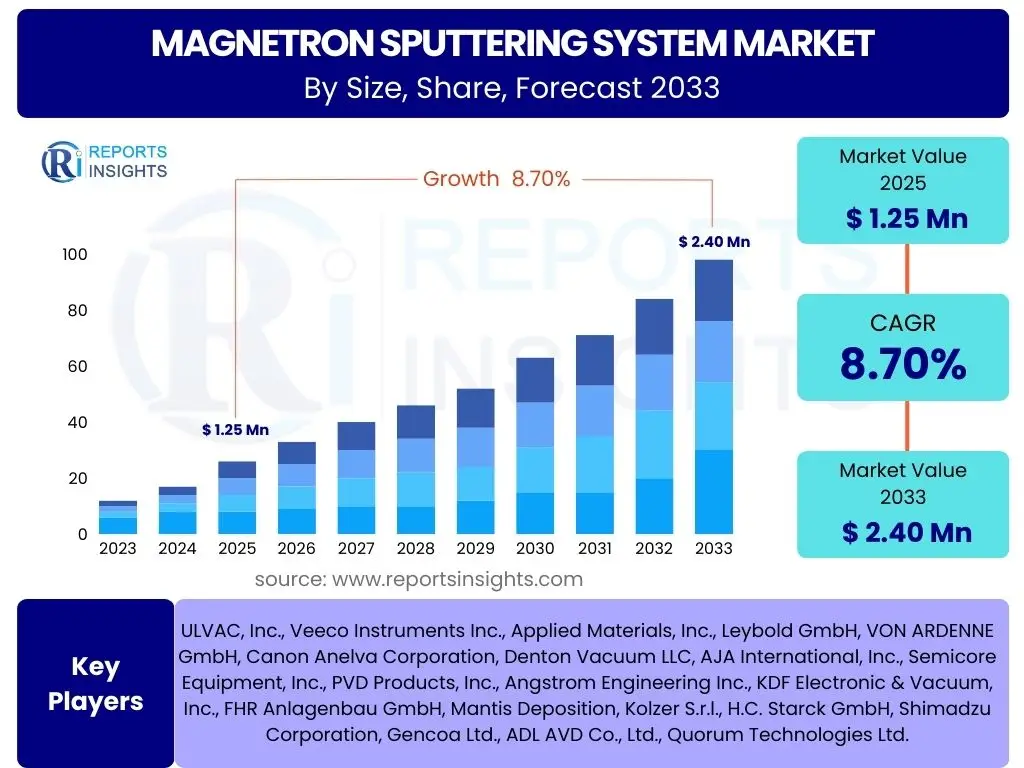

Magnetron Sputtering System Market Size

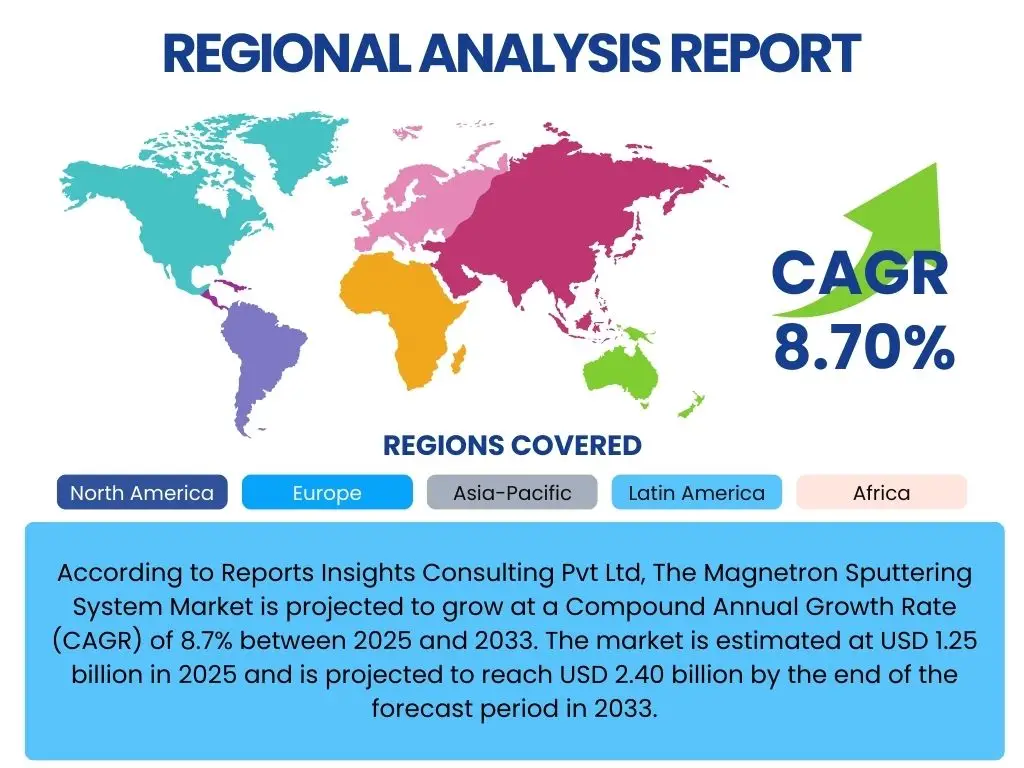

According to Reports Insights Consulting Pvt Ltd, The Magnetron Sputtering System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.40 billion by the end of the forecast period in 2033.

Key Magnetron Sputtering System Market Trends & Insights

The Magnetron Sputtering System market is witnessing several transformative trends driven by advancements in materials science, increasing demand for high-performance coatings, and the miniaturization of electronic components. Users frequently inquire about the latest technological shifts, application expansions, and the sustainability aspects influencing market growth. Key insights reveal a robust push towards multi-target systems, enhanced process control for complex alloy deposition, and the integration of smart manufacturing principles to optimize throughput and coating quality.

Another significant trend gaining momentum is the growing adoption of High Power Impulse Magnetron Sputtering (HiPIMS) for superior film properties, particularly in hard and wear-resistant coatings. Furthermore, the market is observing a rising preference for environmentally friendly coating solutions, moving away from traditional electroplating methods, which positions sputtering as a critical technology for future industrial applications. These trends collectively indicate a market evolving towards higher precision, broader material versatility, and sustainable operational models.

- Increasing adoption of HiPIMS for advanced material deposition.

- Growing demand for multi-layer and complex alloy coatings in various industries.

- Miniaturization of electronic components driving demand for precise thin-film deposition.

- Integration of automation and real-time process monitoring for enhanced efficiency.

- Shift towards eco-friendly and sustainable coating technologies.

- Expansion into emerging applications such as flexible electronics and quantum computing.

AI Impact Analysis on Magnetron Sputtering System

Common user questions related to the impact of Artificial Intelligence (AI) on Magnetron Sputtering Systems revolve around process optimization, predictive maintenance, and the role of AI in material discovery and development. Users are keen to understand how AI can improve coating quality, reduce operational costs, and accelerate research and development cycles. The consensus points towards AI becoming an indispensable tool for enhancing the efficiency and capabilities of sputtering processes, moving beyond traditional empirical methods.

AI's influence extends to real-time parameter adjustment, identifying optimal sputtering conditions, and predicting potential equipment failures before they occur. This integration promises a significant leap in productivity, material utilization, and consistency of deposited films, thereby fostering innovation in various high-tech sectors. While implementation presents challenges such as data infrastructure and algorithm development, the long-term benefits in terms of precision, speed, and cost-effectiveness are poised to revolutionize the industry.

- Enhanced process optimization through real-time data analysis and predictive control.

- Predictive maintenance for sputtering equipment, reducing downtime and operational costs.

- Accelerated material discovery and development via AI-driven simulations and data correlation.

- Improved coating uniformity and quality consistency through intelligent parameter adjustments.

- Automation of sputtering recipes and workflows, leading to increased throughput and efficiency.

- Reduced human error and dependence on empirical trial-and-error methods.

Key Takeaways Magnetron Sputtering System Market Size & Forecast

User inquiries concerning key takeaways from the Magnetron Sputtering System market size and forecast frequently center on understanding the primary growth drivers, the most promising application areas, and the underlying technological shifts. Insights reveal that the market is on a robust growth trajectory, primarily fueled by the semiconductor, automotive, and medical industries' increasing demand for advanced thin-film coatings. The forecast underscores a sustained period of expansion, supported by ongoing innovation in sputtering technology and material science.

A crucial takeaway is the pivotal role of technological advancements, particularly in HiPIMS and multi-target systems, which are enabling the deposition of more complex and higher-performance films. Furthermore, the market's resilience is evident in its adaptability to diverse industrial requirements, from aesthetic coatings to highly functional protective layers. This robust outlook is underpinned by strong R&D investments and an expanding array of applications, making magnetron sputtering a cornerstone technology in advanced manufacturing.

- Significant market growth driven by the semiconductor and electronics industries.

- Increasing adoption in automotive, medical, and aerospace sectors for protective and functional coatings.

- Technological advancements, especially in HiPIMS and advanced control systems, are crucial for market expansion.

- Asia Pacific remains a dominant region due to high manufacturing capacities and technological investments.

- Opportunities abound in emerging applications such as flexible electronics and renewable energy.

Magnetron Sputtering System Market Drivers Analysis

The Magnetron Sputtering System market is propelled by a confluence of factors, primarily the surging demand for advanced materials and high-performance coatings across diverse industrial sectors. The relentless pace of innovation in electronics, particularly in semiconductor manufacturing and display technologies, necessitates precise and uniform thin-film deposition, for which magnetron sputtering is ideally suited. Furthermore, the automotive and aerospace industries are increasingly relying on sputtering for wear-resistant, corrosion-protective, and aesthetic coatings that enhance product lifespan and performance.

The shift towards sustainable manufacturing processes also acts as a significant driver. As industries seek alternatives to traditional wet chemical processes, magnetron sputtering offers a dry, environmentally friendlier deposition method. Additionally, the medical device sector's stringent requirements for biocompatible and antimicrobial coatings on implants and instruments contribute substantially to market demand. These combined factors create a strong impetus for the continued expansion and technological evolution of magnetron sputtering systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Semiconductor & Electronics Industry | +1.5% | Asia Pacific (China, South Korea, Taiwan), North America, Europe | Short to Long-term |

| Increasing Demand for Thin-Film Coatings in Automotive & Aerospace | +1.2% | Europe (Germany), North America (USA), Asia Pacific (Japan, China) | Medium to Long-term |

| Advancements in Material Science & Nanotechnology | +1.0% | Global (USA, Germany, Japan) | Long-term |

| Rising Adoption in Medical Devices & Implants | +0.8% | North America, Europe | Medium-term |

| Shift Towards Eco-friendly Coating Technologies | +0.7% | Europe, North America, Asia Pacific | Medium to Long-term |

Magnetron Sputtering System Market Restraints Analysis

Despite its significant growth prospects, the Magnetron Sputtering System market faces several notable restraints that could temper its expansion. One primary challenge is the substantial capital investment required for purchasing and installing these advanced systems. This high upfront cost can be a barrier for smaller enterprises or those in developing regions, limiting wider adoption. Additionally, the operational complexity and the need for highly skilled personnel to operate and maintain these sophisticated systems contribute to overall operational expenses, posing a restraint for industries with limited technical expertise.

Furthermore, the availability and cost fluctuations of target materials, which are crucial components in the sputtering process, can impact market stability and profitability. Supply chain disruptions and geopolitical tensions affecting raw material sourcing can lead to increased manufacturing costs. Competition from alternative thin-film deposition techniques, such as evaporation and chemical vapor deposition (CVD), also presents a restraint, especially where specific application requirements might favor these other methods based on cost, material compatibility, or process simplicity. These factors necessitate continuous innovation and cost-optimization strategies within the magnetron sputtering industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment & Operational Costs | -0.8% | Global, particularly SMEs | Short to Medium-term |

| Availability & Cost Volatility of Target Materials | -0.6% | Asia Pacific, Europe, North America | Short to Medium-term |

| Competition from Alternative Deposition Technologies | -0.5% | Global | Medium-term |

| Need for Highly Skilled Operators & Maintenance Staff | -0.4% | Developing Regions, SMEs | Short to Medium-term |

Magnetron Sputtering System Market Opportunities Analysis

The Magnetron Sputtering System market is ripe with opportunities driven by the emergence of new technologies and the expansion into previously untapped application areas. The advent of flexible electronics, wearable devices, and advanced packaging solutions creates significant demand for ultra-thin, highly conductive, and transparent coatings, which magnetron sputtering can efficiently produce. Furthermore, the burgeoning field of renewable energy, particularly solar cells and solid-state batteries, offers substantial growth avenues for sputtering systems to deposit critical functional layers with precision and scalability.

Innovation in material science continues to open new frontiers, with opportunities in developing advanced alloys, composites, and functional coatings for extreme environments. The increasing focus on smart surfaces, IoT devices, and quantum computing also necessitates novel thin-film properties achievable through advanced sputtering techniques. Customization and specialized niche market penetration, coupled with ongoing research into next-generation sputtering sources like HiPIMS for even superior film characteristics, present compelling opportunities for market participants to expand their product portfolios and capture new revenue streams globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Flexible Electronics & Wearables | +1.2% | Asia Pacific (South Korea, China, Japan), North America, Europe | Medium to Long-term |

| Growth in Renewable Energy (Solar Cells, Energy Storage) | +1.0% | Asia Pacific (China, India), Europe, North America | Medium to Long-term |

| Development of Advanced Alloys & Nanomaterials | +0.9% | Global (R&D Hubs in USA, Germany, Japan) | Long-term |

| Expansion into Smart Surfaces & IoT Devices | +0.8% | North America, Europe, Asia Pacific | Medium-term |

Magnetron Sputtering System Market Challenges Impact Analysis

The Magnetron Sputtering System market faces several challenges that require strategic navigation to sustain growth. A significant technical challenge is achieving uniform coating deposition over large substrates, which is critical for applications like large-area displays and architectural glass. Maintaining precise control over film thickness and composition, especially for multi-layer or complex alloy depositions, presents ongoing engineering hurdles. Furthermore, the issue of target material utilization efficiency, where a considerable portion of the target material might not be effectively deposited, impacts operational costs and material waste, demanding continuous improvements in system design.

Beyond technical aspects, the intense competition within the advanced manufacturing sector and from other thin-film technologies compels continuous innovation, which can be resource-intensive for manufacturers. The rapid obsolescence of technology also poses a challenge, as companies must frequently upgrade their systems to remain competitive. Additionally, intellectual property disputes and the complexity of patent landscapes in highly specialized materials and processes can hinder market entry and collaboration. Addressing these challenges requires sustained R&D, strategic partnerships, and a focus on cost-effective, high-performance solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Coating Uniformity Over Large Substrates | -0.7% | Global (especially Display & Architectural Glass Manufacturers) | Medium to Long-term |

| High Target Material Consumption & Waste | -0.6% | Global | Short to Medium-term |

| Complexity in Depositing Advanced & Multi-layer Films | -0.5% | Global (R&D intensive industries) | Medium-term |

| Intense Competition & Rapid Technological Obsolescence | -0.4% | Global | Short to Medium-term |

Magnetron Sputtering System Market - Updated Report Scope

This report offers an in-depth analysis of the global Magnetron Sputtering System market, providing a detailed understanding of its current landscape, historical performance, and future growth prospects. It covers comprehensive market sizing, segmentation analysis, regional insights, and a competitive assessment of key market players. The scope includes an examination of critical market drivers, restraints, opportunities, and challenges, along with a forward-looking perspective on technological advancements and their impact, particularly from Artificial Intelligence, to offer actionable intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 billion |

| Market Forecast in 2033 | USD 2.40 billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ULVAC, Inc., Veeco Instruments Inc., Applied Materials, Inc., Leybold GmbH, VON ARDENNE GmbH, Canon Anelva Corporation, Denton Vacuum LLC, AJA International, Inc., Semicore Equipment, Inc., PVD Products, Inc., Angstrom Engineering Inc., KDF Electronic & Vacuum, Inc., FHR Anlagenbau GmbH, Mantis Deposition, Kolzer S.r.l., H.C. Starck GmbH, Shimadzu Corporation, Gencoa Ltd., ADL AVD Co., Ltd., Quorum Technologies Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Magnetron Sputtering System market is extensively segmented to provide a granular view of its various facets, enabling a detailed understanding of market dynamics across different technologies, applications, and end-use sectors. This segmentation highlights the diverse requirements and technological preferences driving specific market niches, ranging from basic DC sputtering for general coatings to advanced HiPIMS for high-performance applications. Understanding these segments is crucial for identifying growth opportunities and tailoring product development strategies.

The end-use industry segmentation further clarifies the primary demand drivers, with semiconductor and electronics representing a significant portion due to the need for intricate thin films. Other substantial contributors include the automotive sector for protective coatings and the medical industry for biocompatible surfaces. This comprehensive segmentation provides a roadmap for market participants to strategize effectively within the complex ecosystem of magnetron sputtering technology.

- By Type:

- DC Magnetron Sputtering

- RF Magnetron Sputtering

- Pulsed DC Magnetron Sputtering

- HiPIMS (High Power Impulse Magnetron Sputtering)

- By Application:

- Thin-film Deposition

- Etching

- Surface Modification

- By End-use Industry:

- Semiconductor & Electronics

- Automotive

- Medical

- Aerospace & Defense

- Energy (Solar, Batteries)

- Optics & Displays

- Tools & Components

- Others (Research & Development, Decorative Coatings)

Regional Highlights

The global Magnetron Sputtering System market exhibits distinct regional dynamics, influenced by varying levels of industrialization, technological adoption, and investment in key sectors. Asia Pacific stands out as the dominant region, primarily driven by the robust growth of its semiconductor, electronics manufacturing, and display industries, particularly in countries like China, South Korea, Taiwan, and Japan. These nations are major hubs for both production and innovation in thin-film technologies, leading to high demand for sputtering systems.

North America and Europe represent mature markets characterized by significant R&D activities, strong aerospace and defense sectors, and increasing adoption in advanced medical device manufacturing. These regions are also at the forefront of developing next-generation sputtering technologies and sustainable coating solutions. Latin America, the Middle East, and Africa are emerging markets, showing gradual growth fueled by industrialization efforts and increasing foreign investments in manufacturing and infrastructure, particularly in automotive and basic industrial coatings.

- Asia Pacific: Dominant market share due to strong semiconductor, electronics, and display manufacturing sectors in China, South Korea, Taiwan, and Japan. Rapid industrialization and investment in advanced manufacturing.

- North America: Significant market for high-precision applications in aerospace, medical devices, and advanced R&D. Focus on technological innovation and high-value coatings.

- Europe: Strong presence in automotive, industrial coatings, and specialized electronics. Emphasis on sustainable manufacturing and advanced material research, particularly in Germany and the UK.

- Latin America: Emerging market with growing adoption in automotive and industrial sectors, driven by expanding manufacturing bases and foreign direct investment.

- Middle East & Africa (MEA): Gradual market development, primarily in oil & gas equipment, construction materials, and nascent electronics manufacturing. Potential for growth with diversification initiatives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Magnetron Sputtering System Market.- ULVAC, Inc.

- Veeco Instruments Inc.

- Applied Materials, Inc.

- Leybold GmbH

- VON ARDENNE GmbH

- Canon Anelva Corporation

- Denton Vacuum LLC

- AJA International, Inc.

- Semicore Equipment, Inc.

- PVD Products, Inc.

- Angstrom Engineering Inc.

- KDF Electronic & Vacuum, Inc.

- FHR Anlagenbau GmbH

- Mantis Deposition

- Kolzer S.r.l.

- H.C. Starck GmbH

- Shimadzu Corporation

- Gencoa Ltd.

- ADL AVD Co., Ltd.

- Quorum Technologies Ltd.

Frequently Asked Questions

What is a Magnetron Sputtering System?

A Magnetron Sputtering System is a vacuum coating technology that uses a plasma to eject material from a target, which then deposits as a thin film onto a substrate. It employs magnetic fields to confine and guide electrons, increasing the ionization efficiency and deposition rate compared to conventional sputtering.

How does magnetron sputtering differ from other PVD techniques?

Magnetron sputtering offers superior film adhesion, density, and uniformity compared to thermal evaporation, and lower deposition temperatures than chemical vapor deposition (CVD). Its key distinction lies in using magnetic fields to enhance plasma density, leading to higher deposition rates and more controlled film growth.

What are the primary applications of magnetron sputtering systems?

Magnetron sputtering systems are widely used in the semiconductor industry for integrated circuits, in optics for anti-reflective coatings, in display manufacturing for transparent conductive oxides, in automotive for decorative and protective layers, and in medical devices for biocompatible coatings on implants.

What are the key advantages of using magnetron sputtering technology?

Key advantages include the ability to deposit a wide range of materials (metals, alloys, nitrides, oxides), excellent film adhesion, high density, and uniform thickness. It allows for precise control over film properties, is scalable for large substrates, and offers relatively lower substrate temperatures compared to other techniques.

What is the future outlook for the Magnetron Sputtering System market?

The market is projected for robust growth, driven by increasing demand from the semiconductor, automotive, and medical industries. Innovations in HiPIMS technology, AI integration for process optimization, and expansion into emerging applications like flexible electronics and renewable energy storage will further fuel its expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted