Luxury Vehicle Market

Luxury Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701478 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

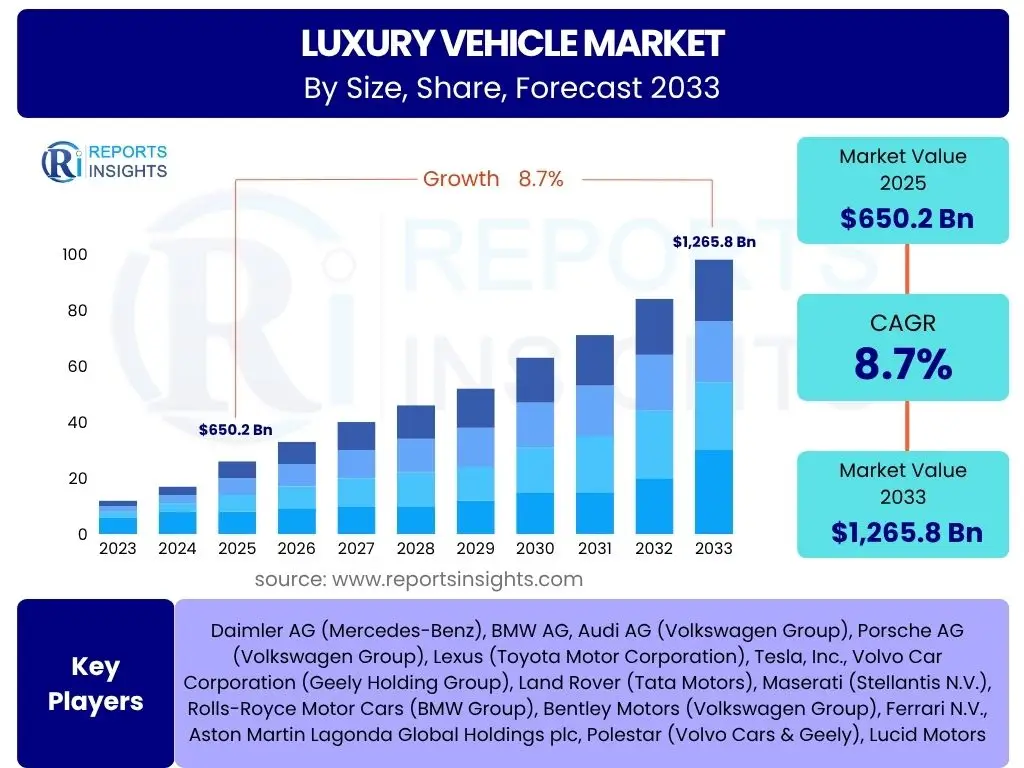

Luxury Vehicle Market Size

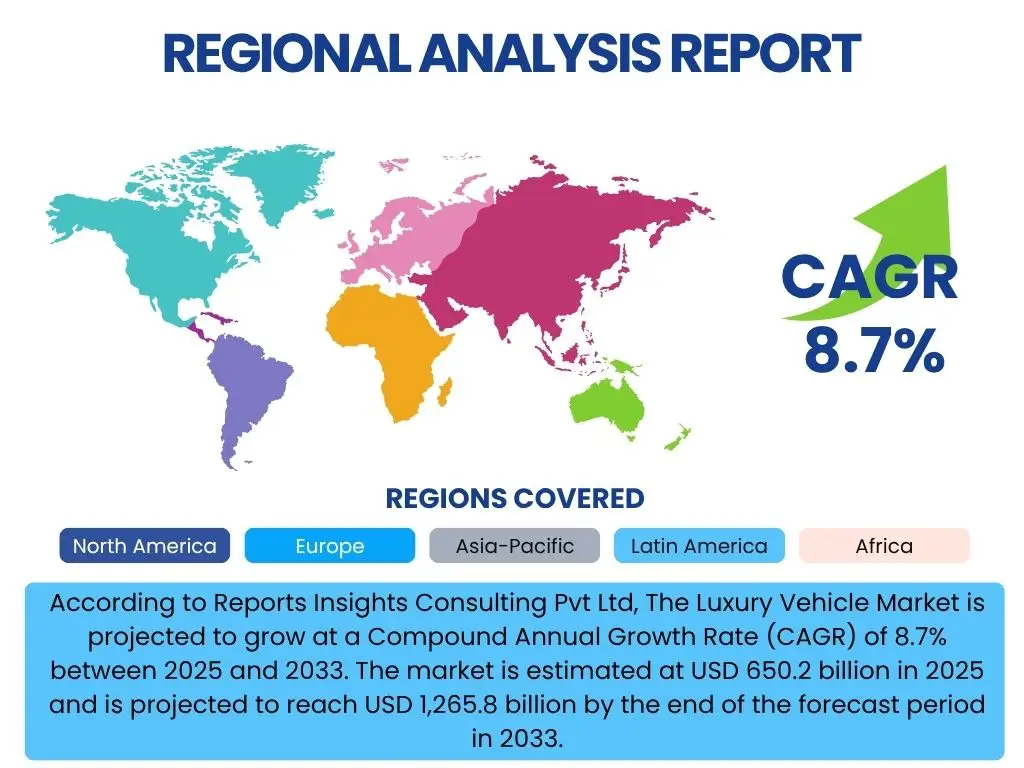

According to Reports Insights Consulting Pvt Ltd, The Luxury Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 650.2 billion in 2025 and is projected to reach USD 1,265.8 billion by the end of the forecast period in 2033.

Key Luxury Vehicle Market Trends & Insights

The luxury vehicle market is undergoing a significant transformation, driven by evolving consumer preferences and technological advancements. Consumers are increasingly valuing experiential ownership, personalization, and sustainability, moving beyond traditional indicators of luxury. This shift is leading manufacturers to focus on bespoke services, unique material choices, and advanced digital integration, creating a more immersive and exclusive brand experience. The convergence of eco-consciousness and high performance is particularly evident, with electric and hybrid luxury vehicles gaining substantial traction, reflecting a growing desire for sustainable yet uncompromising automotive excellence.

Furthermore, the market is witnessing a surge in demand for advanced connectivity features and autonomous driving capabilities, which are becoming standard expectations rather than mere differentiators. Urbanization and the rise of ultra-high-net-worth individuals in emerging economies are also fueling regional growth, particularly in Asia Pacific. Luxury brands are responding by expanding their global footprints and tailoring offerings to specific regional tastes and regulatory landscapes, ensuring continued relevance and market penetration. The emphasis is on delivering not just a vehicle, but a comprehensive luxury lifestyle proposition.

- Electrification of luxury fleets and growing adoption of Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs).

- Enhanced focus on hyper-personalization and bespoke vehicle customization options.

- Integration of advanced connectivity, infotainment, and artificial intelligence (AI) within vehicle systems.

- Rise of subscription-based models and flexible ownership programs offering premium access.

- Increased demand for Sustainable and ethically sourced materials in vehicle interiors and exteriors.

- Development of advanced driver-assistance systems (ADAS) and progression towards autonomous driving capabilities.

- Expansion of digital sales channels and virtual showrooms offering immersive buying experiences.

- Growing influence of Gen Z and Millennial high-net-worth individuals on design and technology preferences.

AI Impact Analysis on Luxury Vehicle

Artificial Intelligence is profoundly reshaping the luxury vehicle sector, primarily by enhancing the in-cabin experience, improving safety through advanced driver-assistance systems (ADAS), and optimizing vehicle performance. Consumers are particularly interested in how AI can offer highly personalized interactions, from adaptive climate control and seat adjustments based on individual preferences to predictive maintenance alerts that ensure optimal vehicle health. AI-driven infotainment systems are becoming more intuitive, offering voice commands, gesture control, and seamless integration with smart home devices, transforming the vehicle into an extension of a connected lifestyle. This focus on intelligent, proactive systems is a key area of consumer expectation and market development.

Beyond the user experience, AI is critical for the progression towards higher levels of autonomous driving. Users are keen to understand the reliability and safety implications of AI-powered self-driving features, as well as the regulatory frameworks surrounding them. In manufacturing, AI is streamlining production processes, optimizing supply chains, and enabling more precise quality control, leading to higher-quality vehicles and reduced production costs. The integration of AI also extends to post-sales services, where predictive analytics can anticipate service needs, offering a proactive and seamless ownership journey. The pervasive application of AI is setting new benchmarks for luxury, emphasizing convenience, safety, and an unparalleled level of bespoke service.

- Enhanced in-car infotainment and personalized user experiences through AI-driven interfaces.

- Advanced Driver-Assistance Systems (ADAS) and progress towards fully autonomous driving capabilities.

- Predictive maintenance and diagnostics, optimizing vehicle performance and reducing downtime.

- AI-powered design and manufacturing processes for improved efficiency and customization.

- Optimized route planning and traffic management through real-time AI analytics.

- Biometric authentication and health monitoring integration for enhanced security and comfort.

- Voice recognition and natural language processing for intuitive vehicle control.

Key Takeaways Luxury Vehicle Market Size & Forecast

The luxury vehicle market is on a robust growth trajectory, driven by increasing affluence globally and a strong desire for premium, technologically advanced, and personalized mobility solutions. The shift towards sustainable luxury, particularly electric vehicles, is a dominant theme, signaling a fundamental transformation in consumer values and manufacturing priorities. Forecasts indicate significant expansion, underscoring the resilience and adaptability of the sector despite economic fluctuations. The market is not merely about transportation but about providing an exclusive lifestyle experience, with technology and customization at its core. This holistic approach ensures sustained demand from discerning buyers worldwide.

Key insights reveal that while established markets like North America and Europe remain crucial, the Asia Pacific region, especially China, will be a primary engine of growth due to its expanding base of high-net-worth individuals. Manufacturers are strategically investing in R&D to integrate cutting-edge AI, connectivity, and autonomous features, recognizing that innovation is paramount for competitive differentiation. The increasing emphasis on bespoke services and digital retail channels also points to a future where convenience and exclusivity redefine the purchasing and ownership journey. Understanding these dynamics is essential for stakeholders looking to capitalize on the evolving luxury automotive landscape.

- Significant market growth projected, reaching over USD 1.2 trillion by 2033.

- Electrification (EVs and Hybrids) is the primary growth catalyst, reshaping product portfolios.

- Technology integration, particularly AI and advanced connectivity, is crucial for market differentiation.

- Personalization and bespoke offerings are paramount for retaining and attracting luxury consumers.

- Asia Pacific, notably China, is a key growth region due to rising disposable incomes and changing consumer preferences.

- Shift towards flexible ownership models and digital sales channels reflects evolving consumer expectations.

Luxury Vehicle Market Drivers Analysis

The global increase in disposable income, particularly among high-net-worth individuals and the emerging affluent class, is a primary driver for the luxury vehicle market. As economic prosperity rises across various regions, consumers have greater purchasing power to invest in premium products that offer superior comfort, performance, and status. This wealth accumulation fuels demand for exclusive automotive experiences, pushing manufacturers to continuously innovate and provide high-end offerings tailored to sophisticated tastes. The aspirational value associated with luxury vehicles further reinforces this demand, particularly in developing economies where owning a luxury car is a significant symbol of success and achievement.

Technological advancements also play a crucial role in driving market expansion. The integration of cutting-edge features such as advanced driver-assistance systems (ADAS), artificial intelligence (AI) for personalized experiences, sophisticated infotainment systems, and robust connectivity options enhances the appeal and value proposition of luxury vehicles. Consumers are willing to pay a premium for vehicles that offer state-of-the-art safety, convenience, and entertainment. Furthermore, the rapid evolution of electric vehicle (EV) technology has opened new avenues for growth, as luxury brands leverage electric powertrains to deliver unprecedented performance, quietness, and sustainability, attracting environmentally conscious affluent buyers who seek both luxury and ecological responsibility.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Disposable Income & Affluence | +2.5% | Global, particularly APAC (China, India), North America, Europe | Long-term (2025-2033) |

| Technological Advancements & Innovation | +2.0% | Global | Medium to Long-term (2025-2033) |

| Growing Demand for EVs & Sustainable Mobility | +1.8% | Europe, North America, China | Medium to Long-term (2025-2033) |

| Preference for Personalized & Exclusive Experiences | +1.5% | Global | Long-term (2025-2033) |

| Expansion of Luxury Infrastructure (Charging, Dealerships) | +1.0% | Emerging Markets, Europe, North America | Medium-term (2025-2029) |

Luxury Vehicle Market Restraints Analysis

The luxury vehicle market faces significant restraints, primarily stemming from the high initial purchase cost and the expensive maintenance associated with these vehicles. This premium pricing, while intrinsic to the luxury segment, can deter potential buyers, especially in the face of economic uncertainties or increasing cost of living pressures. Furthermore, the specialized components and advanced technologies in luxury cars often translate into higher servicing and repair costs, which can become a long-term financial burden for owners. This total cost of ownership remains a significant consideration for affluent consumers, potentially leading them to explore alternative premium mobility solutions or hold onto their vehicles for longer durations.

Another considerable restraint is the evolving regulatory landscape, particularly concerning stringent emission standards and safety regulations. Governments globally are implementing stricter norms to curb pollution and enhance road safety, which necessitates substantial research and development investments from luxury vehicle manufacturers. Adhering to these diverse and often complex regulations across different regions adds to production costs and can impact vehicle design, potentially slowing down new model introductions. Moreover, the nascent but growing EV charging infrastructure, especially in emerging markets, poses a practical limitation for the widespread adoption of luxury electric vehicles, despite their increasing popularity. This lack of comprehensive infrastructure can create range anxiety and inconvenience, restraining the transition from traditional internal combustion engine (ICE) luxury vehicles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Purchase and Maintenance Costs | -1.2% | Global | Long-term (2025-2033) |

| Stringent Emission & Safety Regulations | -1.0% | Europe, North America, China | Medium to Long-term (2025-2033) |

| Inadequate EV Charging Infrastructure | -0.8% | Emerging Markets, Rural Areas | Short to Medium-term (2025-2029) |

| Economic Volatility & Geopolitical Instability | -0.7% | Global | Short to Medium-term (2025-2028) |

| Intense Competition from Emerging Brands | -0.5% | Global | Long-term (2025-2033) |

Luxury Vehicle Market Opportunities Analysis

The expansion of the ultra-high-net-worth individual (UHNWI) population, particularly in emerging economies, presents a significant growth opportunity for the luxury vehicle market. As wealth continues to concentrate and grow in regions like Asia Pacific and the Middle East, there is an expanding consumer base with the financial capacity and desire for exclusive, high-performance vehicles. This demographic is often seeking status symbols, bespoke experiences, and the latest technological innovations, providing fertile ground for luxury brands to introduce new models, expand their dealership networks, and offer highly personalized services tailored to regional preferences. The sheer volume of this growing affluent segment ensures a sustained increase in demand for premium automotive products.

The rapid advancements in autonomous driving and connected car technologies also create substantial opportunities. While still evolving, the eventual widespread adoption of higher levels of autonomous driving (Level 3, 4, and 5) will redefine the in-car experience, transforming vehicles into mobile luxury lounges or offices. This presents opportunities for luxury brands to innovate with interior design, connectivity services, and unique in-cabin entertainment options that cater to occupants no longer required to focus on driving. Furthermore, the shift towards sustainable luxury and the increasing consumer demand for eco-friendly products offer brands a chance to differentiate themselves through electric and hydrogen-powered luxury vehicles, appealing to environmentally conscious affluent buyers and establishing leadership in the green luxury segment. The development of new business models, such as subscription services and fractional ownership, also caters to modern preferences for flexibility and access over outright ownership, expanding the market reach.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Ultra-High-Net-Worth Individuals (UHNWIs) | +2.3% | APAC, Middle East, North America | Long-term (2025-2033) |

| Advancements in Autonomous Driving & Connected Car Tech | +2.0% | Global | Medium to Long-term (2027-2033) |

| Increasing Demand for Sustainable & Green Luxury Vehicles | +1.7% | Europe, North America, China | Medium to Long-term (2025-2033) |

| New Business Models (Subscription, Fractional Ownership) | +1.3% | North America, Europe | Short to Medium-term (2025-2029) |

| Expansion into Untapped Emerging Markets | +1.0% | Southeast Asia, Latin America, Africa | Medium to Long-term (2026-2033) |

Luxury Vehicle Market Challenges Impact Analysis

The luxury vehicle market faces significant challenges from volatile raw material prices and ongoing supply chain disruptions. The automotive industry relies heavily on a stable supply of materials like semiconductors, rare earth metals, and specialized components. Geopolitical tensions, trade disputes, and unforeseen events such as pandemics can severely disrupt these supply chains, leading to production delays, increased manufacturing costs, and ultimately, higher vehicle prices. This unpredictability makes long-term production planning difficult and can impact the availability of new luxury models, frustrating discerning customers who expect immediate access to cutting-edge vehicles. Maintaining exclusivity and ensuring timely delivery become difficult when supply chains are unreliable.

Another major challenge is the intense competition and the rapid pace of technological change within the industry. Established luxury brands must continuously innovate to stay ahead, while new entrants, particularly those focused on electric vehicles and advanced software, are rapidly gaining market share. This competitive pressure mandates significant investment in research and development, forcing brands to constantly update their offerings with the latest features in electrification, connectivity, and autonomous driving. The need to balance traditional brand heritage with modern technological expectations, coupled with the pressure to meet evolving consumer demands for digital experiences and personalized services, creates a complex environment for luxury vehicle manufacturers to navigate effectively. Furthermore, the fluctuating global economic conditions and currency exchange rates add an extra layer of complexity to market planning and pricing strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices & Supply Chain Disruptions | -1.5% | Global | Short to Medium-term (2025-2028) |

| Intense Competition & Rapid Technological Evolution | -1.3% | Global | Long-term (2025-2033) |

| Economic Slowdowns & Consumer Spending Fluctuations | -1.0% | Global | Short-term (2025-2026) |

| Cybersecurity Risks & Data Privacy Concerns | -0.8% | Global | Long-term (2025-2033) |

| Skilled Labor Shortages in Advanced Manufacturing | -0.7% | North America, Europe, Japan | Medium to Long-term (2025-2033) |

Luxury Vehicle Market - Updated Report Scope

This report provides a detailed and comprehensive analysis of the global luxury vehicle market, covering current market dynamics, key trends, growth drivers, restraints, opportunities, and challenges. It offers a strategic outlook on market size and forecast from 2025 to 2033, segmenting the market by vehicle type, powertrain, application, sales channel, and key regional geographies. The scope includes an in-depth assessment of the competitive landscape, highlighting the strategies of prominent market players and their impact on market evolution, as well as an analysis of AI's transformative role in the sector. The report aims to equip stakeholders with actionable insights for informed decision-making and strategic planning in this rapidly evolving segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650.2 billion |

| Market Forecast in 2033 | USD 1,265.8 billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Daimler AG (Mercedes-Benz), BMW AG, Audi AG (Volkswagen Group), Porsche AG (Volkswagen Group), Lexus (Toyota Motor Corporation), Tesla, Inc., Volvo Car Corporation (Geely Holding Group), Land Rover (Tata Motors), Maserati (Stellantis N.V.), Rolls-Royce Motor Cars (BMW Group), Bentley Motors (Volkswagen Group), Ferrari N.V., Aston Martin Lagonda Global Holdings plc, Polestar (Volvo Cars & Geely), Lucid Motors |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The luxury vehicle market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of consumer preferences, technological adoption, and regional specificities, thereby informing strategic decisions for market players. By breaking down the market into various vehicle types, powertrain technologies, applications, and sales channels, the report offers a holistic view of the market structure and its underlying dynamics. This detailed classification aids in identifying niche opportunities and understanding the competitive landscape across different product offerings and distribution models.

Understanding these segments is critical for manufacturers to tailor their product development and marketing strategies. For instance, the robust growth in the SUV segment reflects shifting consumer preferences towards versatile and spacious luxury vehicles, while the rapid expansion of BEVs signifies the industry's commitment to electrification. The distinct characteristics of each segment, from the high-performance focus of sports cars to the evolving role of luxury vehicles in commercial applications, dictate varying levels of innovation, investment, and market potential. This comprehensive segmentation analysis is essential for stakeholders to navigate the complexities of the luxury automotive market and capitalize on its most promising areas.

- By Vehicle Type:

- Sedan: Traditional luxury segment emphasizing comfort, performance, and sophisticated design.

- SUV: Dominant and fastest-growing segment, offering versatility, space, and elevated driving position.

- Sports Car: Niche segment focused on high performance, speed, and driving dynamics.

- Coupe: Two-door luxury vehicles characterized by sleek designs and sporty aesthetics.

- Convertible: Vehicles with retractable roofs, appealing to leisure and lifestyle-oriented consumers.

- Other: Includes bespoke models, limousines, and specialized luxury vehicles.

- By Powertrain:

- Internal Combustion Engine (ICE): Traditional gasoline and diesel-powered luxury vehicles, still a significant market share but declining.

- Battery Electric Vehicle (BEV): Fully electric luxury cars, rapidly gaining traction due to sustainability and performance advantages.

- Plug-in Hybrid Electric Vehicle (PHEV): Combines an ICE with an electric motor and battery, offering both electric range and fuel flexibility.

- Hybrid Electric Vehicle (HEV): Utilizes an electric motor to assist the ICE, primarily for improved fuel efficiency.

- By Application:

- Personal Use: Vehicles purchased by individuals for private transportation, the largest application segment.

- Commercial Use: Includes luxury vehicles used for ride-hailing services, corporate fleets, and high-end car rentals.

- By Sales Channel:

- Dealerships: Traditional brick-and-mortar showrooms offering sales and after-sales services.

- Online Sales: Growing channel leveraging digital platforms for vehicle configuration, purchase, and delivery.

- Direct to Consumer: Manufacturer-to-consumer sales model, often seen with new EV luxury brands, bypassing traditional dealerships.

Regional Highlights

- North America: This region represents a mature and significant market for luxury vehicles, characterized by high disposable incomes, strong consumer demand for SUVs, and early adoption of advanced technologies. The United States is a key market, driving innovation in electric luxury vehicles and sophisticated in-car technology. Consumers here value performance, brand prestige, and personalization. Canada also contributes to regional growth with a growing affluent population. The market is influenced by robust economic conditions and a strong preference for large, feature-rich luxury vehicles, including a rapidly expanding electric luxury segment.

- Europe: Europe is a hub for established luxury automotive brands, known for its emphasis on engineering excellence, design sophistication, and a growing focus on sustainability. Countries like Germany, the UK, and France are major contributors to the market. Strict emission regulations and consumer demand for eco-friendly options are accelerating the transition towards electric and hybrid luxury vehicles. The region also exhibits a strong preference for premium sedans and smaller, more agile luxury vehicles suitable for urban environments, alongside a burgeoning market for luxury SUVs. Innovation in autonomous driving and advanced connectivity is also a key regional trend.

- Asia Pacific (APAC): APAC is the fastest-growing region in the luxury vehicle market, primarily driven by rising affluence in countries like China, India, Japan, and South Korea. China, in particular, is the largest single-country market for luxury vehicles, fueled by a rapidly expanding middle class and ultra-high-net-worth individuals. Consumers in this region often seek status symbols, advanced technology, and personalized features. The demand for luxury SUVs and electric vehicles is exceptionally high. Urbanization and changing consumer lifestyles contribute significantly to the market's robust expansion, with manufacturers tailoring products specifically for Asian tastes and road conditions.

- Latin America: While smaller in comparison to other regions, Latin America is an emerging market for luxury vehicles, experiencing gradual growth driven by increasing economic stability and a growing number of affluent individuals. Countries such as Brazil and Mexico are key markets, characterized by a preference for luxury SUVs and sedans. The market faces challenges related to economic volatility and infrastructure development but presents long-term potential as economies continue to mature and disposable incomes rise. Imports of luxury vehicles largely dominate the market, with increasing interest in premium brands.

- Middle East and Africa (MEA): The Middle East is a significant market for luxury vehicles, particularly driven by oil-rich economies and a high concentration of ultra-high-net-worth individuals who demand opulent and high-performance vehicles. Countries like Saudi Arabia, UAE, and Qatar are major consumers of high-end SUVs and performance cars. The African market, though nascent, shows promise in countries like South Africa. Consumers in this region prioritize luxury, power, and brand exclusivity. While the market can be influenced by oil price fluctuations, the long-term outlook remains positive due to continued wealth creation and a desire for premium products.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Luxury Vehicle Market.- Daimler AG (Mercedes-Benz)

- BMW AG

- Audi AG (Volkswagen Group)

- Porsche AG (Volkswagen Group)

- Lexus (Toyota Motor Corporation)

- Tesla, Inc.

- Volvo Car Corporation (Geely Holding Group)

- Land Rover (Tata Motors)

- Maserati (Stellantis N.V.)

- Rolls-Royce Motor Cars (BMW Group)

- Bentley Motors (Volkswagen Group)

- Ferrari N.V.

- Aston Martin Lagonda Global Holdings plc

- Polestar (Volvo Cars & Geely)

- Lucid Motors

- Rivian Automotive, Inc.

- Hyundai Motor Group (Genesis)

- GMC (General Motors)

- Acura (Honda Motor Co., Ltd.)

- Lincoln (Ford Motor Company)

Frequently Asked Questions

What is the projected growth rate of the Luxury Vehicle Market?

The Luxury Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, demonstrating robust expansion.

What key trends are shaping the Luxury Vehicle Market?

Key trends include the rapid electrification of vehicle fleets, increasing demand for personalization and bespoke services, advanced integration of AI and connectivity, and the emergence of flexible ownership models like subscriptions.

How is AI impacting the Luxury Vehicle sector?

AI is significantly enhancing in-car experiences through personalized interfaces, advancing autonomous driving capabilities, enabling predictive maintenance, and optimizing manufacturing processes for greater efficiency and customization.

Which region is expected to lead market growth for luxury vehicles?

The Asia Pacific region, particularly China, is anticipated to be the primary engine of market growth due to its rapidly expanding affluent population and increasing demand for luxury automotive products.

What are the main challenges facing the Luxury Vehicle Market?

Key challenges include volatile raw material prices, ongoing supply chain disruptions, intense competition from both established and new entrants, and the need to constantly innovate amidst rapid technological evolution.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted