Long Carbon Fiber Thermoplastic Market

Long Carbon Fiber Thermoplastic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702068 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Long Carbon Fiber Thermoplastic Market Size

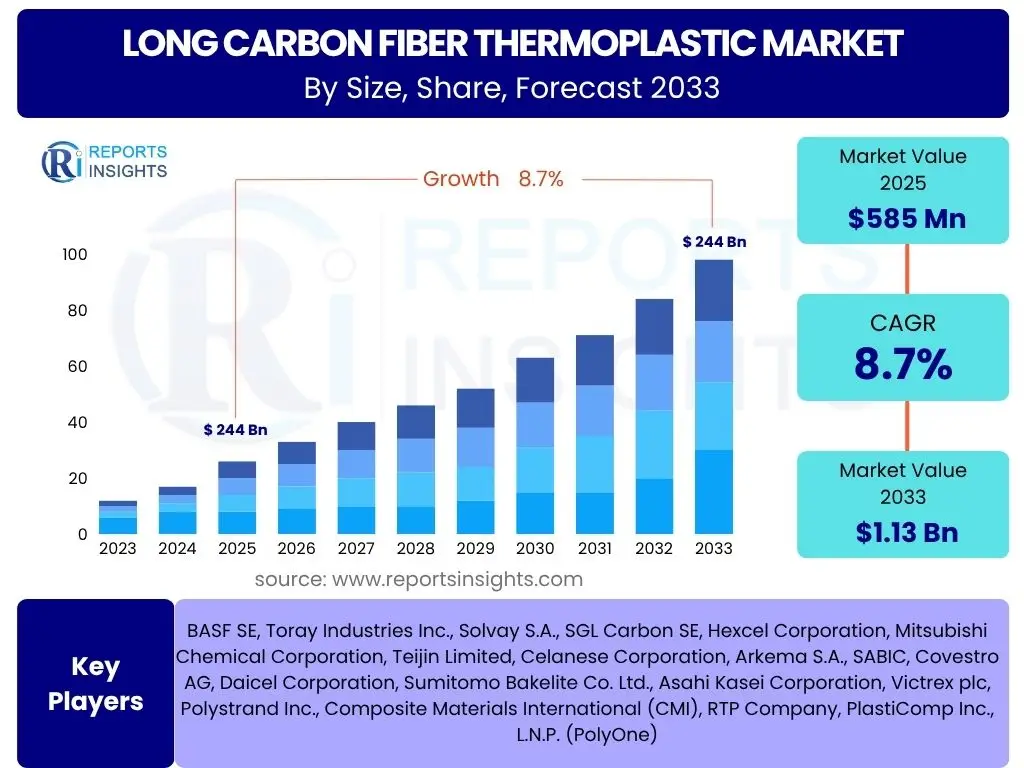

According to Reports Insights Consulting Pvt Ltd, The Long Carbon Fiber Thermoplastic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 585 Million in 2025 and is projected to reach USD 1.13 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the increasing demand for lightweight, high-performance materials across various industries, including automotive, aerospace, and consumer goods, where enhanced strength-to-weight ratios are critical for energy efficiency and product longevity.

The market's expansion is further bolstered by continuous advancements in material science and manufacturing technologies, which make long carbon fiber thermoplastics more accessible and cost-effective for a broader range of applications. These materials offer superior mechanical properties compared to traditional plastics, including improved stiffness, strength, and impact resistance, making them ideal for demanding applications that require robust and durable components. The global shift towards sustainable and recyclable materials also contributes to market growth, as thermoplastics generally offer better recyclability profiles than thermosets.

Key Long Carbon Fiber Thermoplastic Market Trends & Insights

Common inquiries regarding the Long Carbon Fiber Thermoplastic market frequently center on emerging trends that are shaping its trajectory and adoption. Users are keenly interested in understanding how technological advancements, sustainability initiatives, and evolving industry demands are influencing the development and application of these advanced composite materials. A significant portion of these questions pertains to the transition from traditional materials to lighter, stronger alternatives and the role of innovation in driving this shift, particularly in high-performance sectors.

The insights derived from analyzing these user questions reveal a strong emphasis on the push for lightweighting across industries, largely driven by stringent regulatory standards and the consumer demand for more fuel-efficient and high-performing products. Furthermore, there is considerable interest in the integration of these materials into new manufacturing paradigms, such as additive manufacturing, which promises greater design flexibility and reduced production waste. The market is also witnessing a growing focus on the development of bio-based or recycled LCF thermoplastics, aligning with broader environmental sustainability goals.

Another prevalent theme in user questions revolves around the economic viability and scalability of long carbon fiber thermoplastic production. While the performance benefits are widely acknowledged, concerns about material costs and complex processing methods often surface. This indicates a trend towards research and development aimed at reducing production expenses and simplifying manufacturing processes to accelerate wider market adoption, including the exploration of automated production lines and more efficient compounding techniques.

- Increased adoption in electric vehicles (EVs) for battery enclosures and structural components, driven by lightweighting mandates.

- Growth of additive manufacturing (3D printing) using LCF thermoplastics for prototyping and functional parts.

- Development of sustainable and recyclable LCF thermoplastic solutions to meet circular economy principles.

- Expansion into new applications such as consumer electronics, medical devices, and sporting goods.

- Focus on automation and process optimization in manufacturing to reduce production costs and cycle times.

AI Impact Analysis on Long Carbon Fiber Thermoplastic

User queries regarding the impact of Artificial Intelligence (AI) on the Long Carbon Fiber Thermoplastic market often explore how AI technologies can optimize various stages of the material lifecycle, from design and development to manufacturing and end-of-life management. Users are particularly interested in AI's potential to accelerate material discovery, predict performance characteristics, and enhance the efficiency and quality of production processes. Questions frequently touch upon the practical applications of machine learning algorithms in composite material engineering and intelligent manufacturing systems.

The analysis suggests that AI is poised to revolutionize the LCF thermoplastic sector by enabling more precise material formulation and predictive analytics for quality control. For instance, AI algorithms can analyze vast datasets of material properties and performance under various conditions, allowing engineers to design novel compositions with tailored characteristics more rapidly than traditional experimental methods. This capability reduces research and development cycles and minimizes the need for extensive physical prototyping, thereby accelerating market entry for new products.

Furthermore, AI-driven solutions are expected to significantly enhance manufacturing efficiency through intelligent process control and predictive maintenance. By monitoring real-time production data, AI can identify anomalies, optimize process parameters, and predict equipment failures before they occur, leading to reduced downtime and improved product consistency. The integration of AI in supply chain management also offers the potential for optimized logistics, inventory management, and demand forecasting, creating a more resilient and responsive LCF thermoplastic ecosystem.

- AI-driven material design and discovery for optimizing LCF thermoplastic properties and performance.

- Predictive analytics for quality control and defect detection in LCF composite manufacturing processes.

- Optimization of manufacturing parameters (e.g., temperature, pressure) using machine learning for enhanced efficiency.

- AI-powered predictive maintenance for manufacturing equipment, reducing downtime and operational costs.

- Supply chain optimization and demand forecasting through AI algorithms, improving material flow and inventory management.

Key Takeaways Long Carbon Fiber Thermoplastic Market Size & Forecast

Common user questions regarding key takeaways from the Long Carbon Fiber Thermoplastic market size and forecast frequently revolve around the most critical insights for strategic decision-making. Users are keen to understand the primary growth drivers, the largest opportunities for investment, and the significant challenges that might impede market expansion. These inquiries highlight a need for concise, actionable intelligence that summarizes the market's current state and its projected trajectory over the forecast period, enabling stakeholders to identify lucrative segments and potential risks effectively.

The analysis of these questions reveals that the robust growth projected for the LCF thermoplastic market is largely underpinned by the sustained demand for lightweighting in high-performance applications, particularly within the automotive and aerospace sectors. The forecast indicates a continued shift away from traditional materials due to the superior mechanical properties, improved fuel efficiency, and enhanced design flexibility offered by LCF thermoplastics. This trend is further amplified by increasing environmental consciousness and regulatory pressures favoring materials that contribute to reduced emissions and greater recyclability.

A crucial takeaway is the emergence of new application areas, such as consumer electronics and medical devices, which are expected to contribute significantly to market diversification and expansion beyond traditional industrial uses. While challenges related to cost and complex processing remain, ongoing research and development in manufacturing techniques and material formulations are progressively mitigating these barriers, positioning LCF thermoplastics for broader adoption and sustained growth throughout the forecast period.

- Significant market growth projected, driven primarily by lightweighting trends in automotive and aerospace.

- Strong potential for diversification into new sectors like consumer goods and medical due to evolving material needs.

- Technological advancements in manufacturing processes are crucial for overcoming cost and complexity barriers.

- Sustainability initiatives are increasingly influencing material selection, favoring recyclable LCF thermoplastics.

- Investment in R&D for novel formulations and processing techniques is key to unlocking further market opportunities.

Long Carbon Fiber Thermoplastic Market Drivers Analysis

The global Long Carbon Fiber Thermoplastic market is experiencing significant tailwinds from several key drivers, primarily centered around the increasing demand for high-performance, lightweight materials across diverse industries. The automotive sector, in particular, is a major catalyst, driven by stringent fuel efficiency standards and the accelerating adoption of electric vehicles, where weight reduction directly impacts battery range and overall performance. The continuous pursuit of enhanced structural integrity without compromising weight is fueling the demand for LCF thermoplastics, which offer superior strength-to-weight ratios compared to traditional materials.

Beyond automotive, the aerospace and defense industries are also significant contributors to market growth. The inherent need for lightweight materials to improve fuel efficiency, increase payload capacity, and reduce operational costs in aircraft and spacecraft applications makes LCF thermoplastics an attractive choice. Furthermore, advancements in composite manufacturing technologies, such as automated fiber placement and additive manufacturing, are making it more feasible and cost-effective to produce complex LCF thermoplastic components, thereby expanding their applicability and accelerating market penetration.

The growing emphasis on sustainability and recyclability is another critical driver. As industries face increasing pressure to adopt more environmentally friendly practices, the recyclability of thermoplastics positions LCF thermoplastics as a more sustainable alternative to thermoset composites. This factor, combined with their excellent mechanical properties, ensures their continued integration into products requiring both high performance and a reduced environmental footprint, opening new avenues for growth in various sectors, including renewable energy and industrial applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Materials in Automotive and Aerospace | +2.1% | Global, especially North America, Europe, Asia Pacific (China, Japan) | Short-term to Long-term (2025-2033) |

| Stringent Fuel Efficiency Regulations and Emission Standards | +1.8% | Europe, North America, Asia Pacific | Medium-term to Long-term (2025-2033) |

| Growing Adoption of Electric Vehicles (EVs) | +1.5% | Asia Pacific (China), Europe, North America | Short-term to Long-term (2025-2033) |

| Advancements in Composite Manufacturing Technologies (e.g., Additive Manufacturing) | +1.2% | Global | Medium-term to Long-term (2026-2033) |

| Emphasis on Sustainability and Recyclability of Materials | +0.9% | Europe, North America, Asia Pacific | Medium-term to Long-term (2027-2033) |

Long Carbon Fiber Thermoplastic Market Restraints Analysis

Despite the promising growth trajectory, the Long Carbon Fiber Thermoplastic market faces several significant restraints that could potentially temper its expansion. One of the primary inhibitors is the relatively high cost of long carbon fibers and the associated manufacturing processes compared to conventional materials like metals or short-fiber composites. This cost premium can be a barrier to adoption, especially in price-sensitive applications or regions, limiting the widespread integration of LCF thermoplastics to niche, high-performance segments where the benefits outweigh the expense.

Another crucial restraint is the complexity involved in processing long carbon fiber thermoplastics. These materials often require specialized equipment and expertise for processes such as injection molding, compression molding, and extrusion, particularly when dealing with intricate designs or high-volume production. The challenges include maintaining fiber integrity and dispersion, ensuring proper impregnation, and achieving consistent mechanical properties, which can deter manufacturers lacking the necessary technological infrastructure or skilled workforce.

Furthermore, the nascent stage of the LCF thermoplastic recycling infrastructure presents a significant challenge. While thermoplastics are inherently recyclable, the presence of long carbon fibers makes the recycling process more complex and costly than for unreinforced plastics. This limitation poses an environmental and economic challenge, as end-of-life solutions are still developing, potentially hindering the market's long-term sustainability goals and increasing the overall lifecycle cost of LCF thermoplastic components.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Material and Processing Costs | -1.5% | Global, particularly developing economies | Short-term to Medium-term (2025-2030) |

| Complexity of Manufacturing Processes and Specialized Equipment Needs | -1.0% | Global, especially smaller manufacturers | Short-term to Medium-term (2025-2029) |

| Limited Recyclability Infrastructure for LCF Composites | -0.8% | Global, particularly less developed regions | Medium-term to Long-term (2027-2033) |

| Competition from Alternative High-Performance Materials | -0.7% | Global | Short-term to Long-term (2025-2033) |

| Supply Chain Volatility for Carbon Fiber Raw Materials | -0.5% | Global | Short-term (2025-2027) |

Long Carbon Fiber Thermoplastic Market Opportunities Analysis

The Long Carbon Fiber Thermoplastic market is presented with numerous opportunities that could significantly accelerate its growth trajectory and expand its applications beyond traditional sectors. One of the most promising avenues lies in the increasing adoption within emerging industries such as consumer electronics, medical devices, and sporting goods. In these sectors, the demand for aesthetically pleasing, durable, and lightweight components, often with complex geometries, is rising, creating a natural fit for LCF thermoplastics that offer superior performance over conventional materials.

Furthermore, the ongoing advancements in additive manufacturing (3D printing) technologies represent a substantial opportunity. The ability to print complex LCF thermoplastic parts with high precision and customization offers unparalleled design freedom, reduces material waste, and shortens product development cycles. This synergy between LCF thermoplastics and 3D printing is opening doors for rapid prototyping and the production of functional end-use parts, particularly in niche and high-value applications where customization is paramount.

The growing global focus on developing sustainable materials also offers a significant opportunity for LCF thermoplastics. As research and development efforts lead to the creation of bio-based resins or processes for incorporating recycled carbon fibers into thermoplastic matrices, the environmental footprint of these materials will decrease. This aligns with circular economy principles and increasingly stringent environmental regulations, making LCF thermoplastics an attractive choice for companies seeking to enhance their sustainability profiles and appeal to environmentally conscious consumers and industries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas (Consumer Electronics, Medical, Sports) | +1.8% | Global, particularly Asia Pacific and North America | Medium-term to Long-term (2026-2033) |

| Advancements in Additive Manufacturing (3D Printing) Capabilities | +1.5% | Global | Medium-term to Long-term (2027-2033) |

| Development of Sustainable and Bio-based LCF Thermoplastic Solutions | +1.2% | Europe, North America | Medium-term to Long-term (2028-2033) |

| Strategic Partnerships and Collaborations Across the Value Chain | +0.9% | Global | Short-term to Long-term (2025-2033) |

| Emerging Markets Adoption and Infrastructure Development | +0.7% | Asia Pacific (India, Southeast Asia), Latin America | Medium-term to Long-term (2027-2033) |

Long Carbon Fiber Thermoplastic Market Challenges Impact Analysis

The Long Carbon Fiber Thermoplastic market, while poised for growth, must navigate several critical challenges that could impede its widespread adoption and technological advancement. One significant hurdle is the persistent cost competitiveness against traditional materials and even other composite forms, such as short-fiber reinforced plastics. The high raw material cost of long carbon fibers, coupled with the capital expenditure required for specialized processing equipment, can make LCF thermoplastics less attractive for applications where cost is a primary decision factor, thereby limiting market penetration to premium segments.

Another notable challenge lies in the technical complexities associated with processing LCF thermoplastics, particularly in achieving consistent fiber dispersion and alignment within the matrix. This directly impacts the mechanical properties of the final product and requires meticulous process control, often demanding advanced manufacturing knowledge and highly skilled labor. Ensuring optimal fiber length retention during processing, especially in high-volume production, remains a technical bottleneck that necessitates continuous innovation in compounding and molding techniques.

Furthermore, the nascent stage of the recycling infrastructure for carbon fiber composites, specifically long carbon fiber forms, presents a substantial environmental and economic challenge. While thermoplastics offer inherent recyclability, the presence of embedded carbon fibers complicates the separation and reprocessing, leading to higher recycling costs and lower material quality compared to virgin materials. Developing efficient and economically viable recycling methods is crucial for the long-term sustainability and broader acceptance of LCF thermoplastics in a circular economy. Additionally, navigating the evolving regulatory landscape concerning material sustainability and disposal adds another layer of complexity for manufacturers and end-users.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cost Competitiveness Against Traditional Materials | -1.3% | Global | Short-term to Medium-term (2025-2030) |

| Technical Hurdles in Processing (Fiber Dispersion, Length Retention) | -1.0% | Global | Short-term to Medium-term (2025-2029) |

| Lack of Mature Recycling Infrastructure for LCF Composites | -0.9% | Global | Medium-term to Long-term (2027-2033) |

| Limited Awareness and Standardization Across Industries | -0.6% | Global, particularly emerging markets | Short-term to Medium-term (2025-2030) |

| Scalability of Production for High-Volume Applications | -0.5% | Global | Medium-term (2026-2031) |

Long Carbon Fiber Thermoplastic Market - Updated Report Scope

This market insights report provides a comprehensive analysis of the Long Carbon Fiber Thermoplastic market, encompassing historical data, current market dynamics, and future projections. It delves into the key drivers, restraints, opportunities, and challenges influencing market growth across various regions and end-use industries. The scope includes detailed segmentation analysis by resin type, end-use industry, and manufacturing process, offering a granular view of market trends and competitive landscapes. The report also highlights the impact of emerging technologies and sustainability initiatives on market development.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 585 Million |

| Market Forecast in 2033 | USD 1.13 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Toray Industries Inc., Solvay S.A., SGL Carbon SE, Hexcel Corporation, Mitsubishi Chemical Corporation, Teijin Limited, Celanese Corporation, Arkema S.A., SABIC, Covestro AG, Daicel Corporation, Sumitomo Bakelite Co. Ltd., Asahi Kasei Corporation, Victrex plc, Polystrand Inc., Composite Materials International (CMI), RTP Company, PlastiComp Inc., L.N.P. (PolyOne) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Long Carbon Fiber Thermoplastic market is meticulously segmented to provide a detailed understanding of its diverse applications and material compositions. This segmentation allows for a granular analysis of market dynamics, identifying key growth areas and niche opportunities within various resin types, end-use industries, and manufacturing processes. Understanding these distinct segments is crucial for stakeholders to tailor strategies, optimize product development, and target specific market needs more effectively.

The segmentation by resin type highlights the prevalence and performance characteristics of different polymer matrices, such as polyamide (PA), polypropylene (PP), and polyether ether ketone (PEEK), each offering unique advantages for specific applications. The end-use industry segmentation further clarifies the dominant sectors leveraging LCF thermoplastics, including automotive, aerospace, and industrial applications, while also revealing emerging opportunities in consumer goods and medical devices. This multi-faceted approach to segmentation illustrates the broad utility and adaptability of long carbon fiber thermoplastic composites across the global economy.

- By Resin Type:

- Polyamide (PA)

- Polypropylene (PP)

- Polyether Ether Ketone (PEEK)

- Polycarbonate (PC)

- Polyphthalamide (PPA)

- Other Resins (e.g., PPS, PEI, PSU)

- By End-use Industry:

- Automotive

- Aerospace & Defense

- Industrial

- Consumer Goods

- Medical

- Sports & Leisure

- Electrical & Electronics

- Others (e.g., Marine, Oil & Gas)

- By Manufacturing Process:

- Injection Molding

- Extrusion

- Compression Molding

- Other Processes (e.g., Pultrusion, Automated Fiber Placement)

Regional Highlights

The global Long Carbon Fiber Thermoplastic market exhibits significant regional variations in terms of adoption, production capabilities, and growth drivers. Asia Pacific stands out as a dominant and rapidly growing region, primarily driven by robust manufacturing activities in countries like China, Japan, and South Korea, coupled with increasing demand from their burgeoning automotive and industrial sectors. North America and Europe also represent mature markets with substantial demand from their well-established aerospace, defense, and high-performance automotive industries, further supported by significant research and development investments in advanced materials.

- North America: A mature market with strong demand from the aerospace & defense and automotive sectors. The United States and Canada are key contributors, driven by stringent regulatory frameworks for fuel efficiency and a high adoption rate of advanced materials in high-performance applications. Significant investments in R&D and technological innovation characterize this region.

- Europe: A leading region in LCF thermoplastic adoption, particularly in Germany, France, and the UK, propelled by a strong automotive industry (especially premium and electric vehicles) and a robust aerospace sector. European initiatives towards sustainability and circular economy principles also drive the demand for recyclable thermoplastic composites.

- Asia Pacific (APAC): The fastest-growing market, primarily led by China, Japan, South Korea, and India. This growth is attributed to rapid industrialization, expanding manufacturing bases, increasing automotive production, and rising investments in infrastructure and renewable energy. APAC is also a hub for consumer electronics manufacturing, driving demand for lightweight components.

- Latin America: An emerging market for LCF thermoplastics, with Brazil and Mexico showing increasing adoption in their automotive and industrial sectors. Growth is stimulated by foreign investments and the growing awareness of the benefits of lightweight composite materials, though market penetration is slower compared to developed regions.

- Middle East and Africa (MEA): A nascent but potentially significant market, particularly in the UAE and Saudi Arabia, driven by diversification efforts from oil-dependent economies into manufacturing, aerospace, and defense. Investment in new industrial capabilities and infrastructure projects is expected to fuel future demand for advanced materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Long Carbon Fiber Thermoplastic Market.- BASF SE

- Toray Industries Inc.

- Solvay S.A.

- SGL Carbon SE

- Hexcel Corporation

- Mitsubishi Chemical Corporation

- Teijin Limited

- Celanese Corporation

- Arkema S.A.

- SABIC

- Covestro AG

- Daicel Corporation

- Sumitomo Bakelite Co. Ltd.

- Asahi Kasei Corporation

- Victrex plc

- Polystrand Inc.

- Composite Materials International (CMI)

- RTP Company

- PlastiComp Inc.

- L.N.P. (PolyOne)

Frequently Asked Questions

Analyze common user questions about the Long Carbon Fiber Thermoplastic market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Long Carbon Fiber Thermoplastics (LCFT)?

Long Carbon Fiber Thermoplastics (LCFTs) are composite materials reinforced with continuous or long discontinuous carbon fibers embedded in a thermoplastic polymer matrix. These materials offer superior mechanical properties, including high strength-to-weight ratio, stiffness, and impact resistance, making them ideal for high-performance applications where weight reduction and durability are crucial.

Why is the Long Carbon Fiber Thermoplastic market experiencing significant growth?

The market's growth is primarily driven by the increasing demand for lightweight materials in industries such as automotive (especially EVs), aerospace, and industrial applications to improve fuel efficiency and performance. Advancements in manufacturing technologies, coupled with a growing focus on sustainable and recyclable materials, also contribute to its expansion.

What are the primary applications of Long Carbon Fiber Thermoplastics?

LCFTs are predominantly used in the automotive sector for structural components, battery enclosures, and interior parts. They are also widely applied in aerospace for aircraft interiors and secondary structures, in industrial machinery for robust components, and increasingly in consumer goods, medical devices, and sporting equipment due to their high performance and design flexibility.

What are the main challenges in adopting Long Carbon Fiber Thermoplastics?

Key challenges include the relatively high cost of raw materials and specialized processing equipment, the technical complexity of manufacturing to ensure optimal fiber dispersion and property retention, and the developing infrastructure for recycling LCF composites. Overcoming these hurdles requires ongoing R&D and strategic investment.

How do Long Carbon Fiber Thermoplastics contribute to sustainability?

LCFTs contribute to sustainability through lightweighting, which leads to reduced energy consumption and lower emissions in vehicles and aircraft. Additionally, unlike thermoset composites, thermoplastics are inherently recyclable, offering a pathway for material recovery and reuse, thus aligning with circular economy principles and reducing environmental impact at the end of product life.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted