LNG Tank Container Market

LNG Tank Container Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678314 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

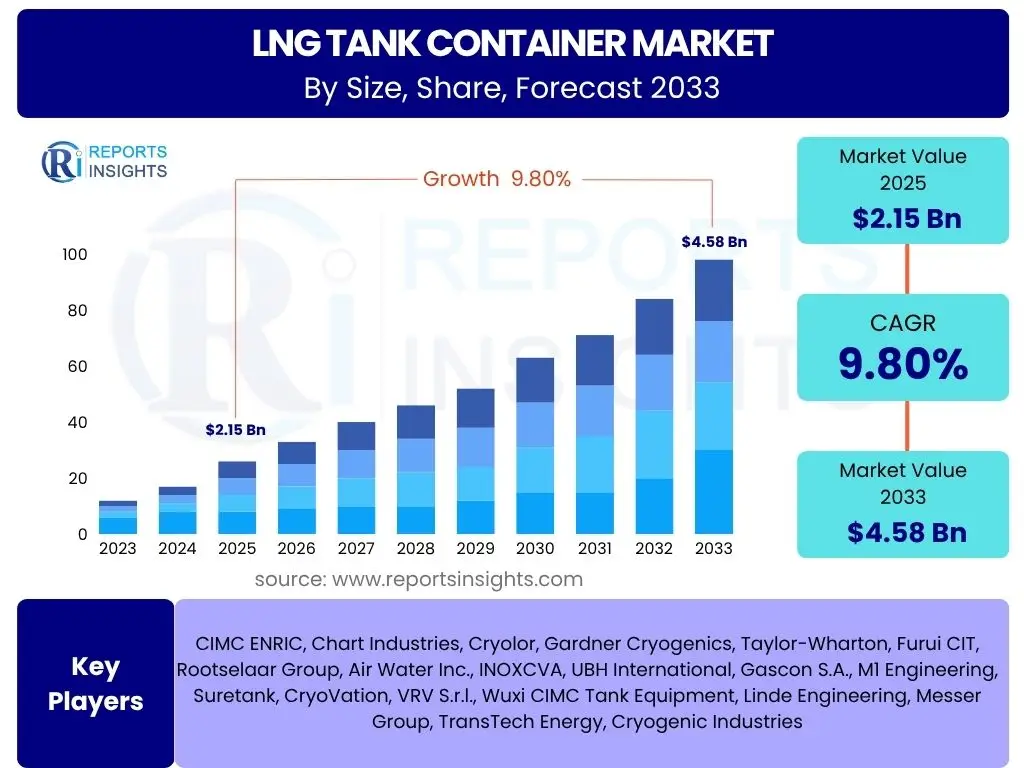

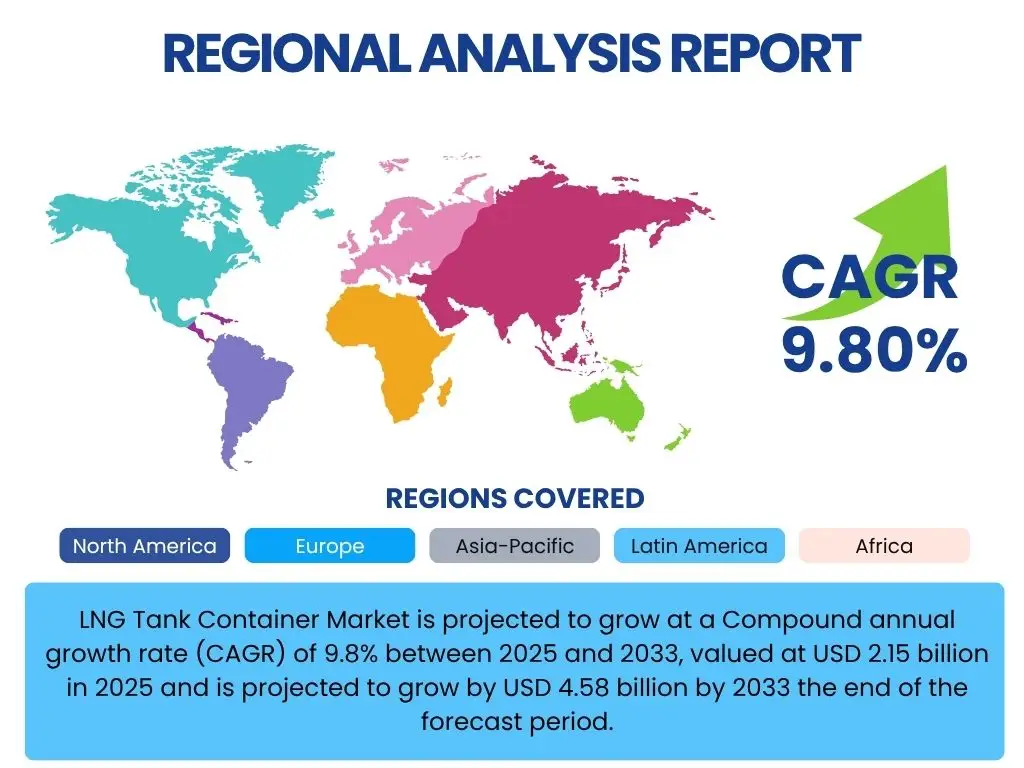

LNG Tank Container Market is projected to grow at a Compound annual growth rate (CAGR) of 6.7% between 2025 and 2033, valued at USD 350 Million in 2025 and is projected to reach USD 585 Million by 2033 the end of the forecast period.

Key LNG Tank Container Market Trends & Insights

The LNG tank container market is experiencing significant transformation driven by the global energy transition and evolving logistics demands. A prominent trend is the accelerating adoption of liquefied natural gas (LNG) as a cleaner burning fuel across various sectors, including marine transport, heavy-duty trucking, and industrial applications. This shift is primarily fueled by stringent environmental regulations aimed at reducing greenhouse gas emissions and air pollution, making LNG an increasingly attractive alternative to traditional fossil fuels. The expansion of LNG bunkering infrastructure and the development of more efficient and larger capacity tank containers are crucial enablers of this trend, facilitating broader access and reducing logistical complexities for end-users.

Another key insight is the growing emphasis on small-scale LNG solutions, particularly for supplying energy to remote regions, off-grid industries, and distributed power generation. This trend leverages the flexibility and modularity of tank containers, allowing for efficient last-mile delivery of LNG where pipeline infrastructure is impractical or unavailable. Furthermore, technological advancements in container design, such as enhanced insulation materials and lighter composite structures, are contributing to improved safety, increased payload capacity, and reduced operational costs. The market is also witnessing greater integration of digital technologies for tracking, monitoring, and optimizing LNG supply chains, further enhancing efficiency and reliability.

- Increasing adoption of LNG as a cleaner fuel in marine and road transport sectors.

- Expansion of global LNG bunkering infrastructure to support cleaner shipping.

- Growing demand for small-scale LNG solutions for remote and industrial applications.

- Technological advancements in tank container design, including enhanced insulation and lighter materials.

- Rising focus on safety standards and regulatory compliance in LNG handling and transport.

- Digitalization and IoT integration for optimized logistics and real-time monitoring of tank containers.

- Development of new trade routes and markets for LNG distribution via multimodal transport.

AI Impact Analysis on LNG Tank Container

The integration of Artificial intelligence (AI) is set to revolutionize various aspects of the LNG tank container market, primarily by enhancing operational efficiency, improving safety protocols, and optimizing logistics. AI-powered predictive analytics can forecast demand for LNG more accurately, enabling better inventory management and reducing storage costs. Furthermore, AI algorithms can analyze vast datasets from sensor-equipped containers to predict potential equipment failures, facilitating proactive maintenance and minimizing downtime. This capability is crucial for maintaining the integrity and reliability of critical infrastructure like LNG tank containers, which operate under demanding conditions.

In terms of logistics and supply chain management, AI offers transformative potential for route optimization, real-time tracking, and risk assessment. AI-driven systems can process complex variables such as weather patterns, traffic congestion, and geopolitical events to recommend the most efficient and safest transport routes for LNG tank containers. This not only reduces transit times and fuel consumption but also enhances overall supply chain resilience. Moreover, AI can be leveraged for advanced safety monitoring, detecting anomalies in pressure, temperature, or structural integrity, and alerting operators to potential hazards, thereby significantly reducing the risk of accidents and improving compliance with stringent safety regulations in the transportation of hazardous materials.

- Enhanced demand forecasting and inventory management through predictive analytics.

- Optimized logistics and route planning for LNG tank containers, reducing transit times and costs.

- Predictive maintenance for tank containers and associated equipment, minimizing downtime.

- Real-time safety monitoring and anomaly detection to prevent incidents and improve operational safety.

- Improved risk assessment and mitigation strategies for multimodal LNG transport.

- Automated compliance checks and reporting for regulatory adherence.

- Data-driven decision-making for network optimization and resource allocation.

Key Takeaways LNG Tank Container Market Size & Forecast

- The global LNG tank container market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 6.7% from 2025 to 2033.

- Market valuation is estimated at USD 350 Million in 2025, with a forecast to reach USD 585 Million by the end of 2033.

- Key growth drivers include the escalating global demand for cleaner energy sources and the expansion of small-scale LNG applications.

- Technological advancements in tank container design and materials are enhancing safety and efficiency.

- Asia Pacific is anticipated to remain a dominant region, driven by industrial growth and energy transition initiatives.

- Challenges such as volatile natural gas prices and stringent safety regulations require strategic navigation for sustained growth.

- Opportunities lie in the increasing adoption of LNG as a marine and heavy-duty vehicle fuel.

LNG Tank Container Market Drivers Impact Analysis

The growth of the LNG tank container market is fundamentally propelled by several critical drivers that collectively underscore the strategic importance of liquefied natural gas in the global energy landscape. A primary driver is the accelerating global shift towards cleaner energy sources, driven by heightened environmental awareness and stringent regulations aimed at reducing carbon emissions. LNG, as a cleaner burning fossil fuel, offers a viable pathway for industries and transportation sectors to lower their environmental footprint, thereby stimulating demand for efficient and safe storage and transport solutions like tank containers.

Another significant driver is the increasing versatility and flexibility that LNG tank containers offer in terms of multimodal transportation. These containers enable seamless movement of LNG across diverse geographies via road, rail, and sea, facilitating access to markets where traditional pipeline infrastructure is unfeasible or economically prohibitive. This modularity is particularly beneficial for the burgeoning small-scale LNG market, which serves remote industrial sites, distributed power generation, and small-scale bunkering operations. Furthermore, ongoing technological advancements in tank container design, including improved insulation, lighter composite materials, and enhanced safety features, are making these units more efficient, cost-effective, and secure, thereby boosting their appeal and utility in the energy supply chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Demand for Cleaner Energy | +2.1% | Global, especially Asia Pacific, Europe | Long-term |

| Expansion of Small-Scale LNG Applications | +1.8% | Asia Pacific, Emerging Economies | Medium-term |

| Increasing Adoption of LNG as Marine Fuel | +1.5% | Europe, North America, Key Shipping Hubs | Medium-term |

| Advancements in Tank Container Technology | +0.8% | Global | Ongoing, Short-term benefits |

| Development of LNG Infrastructure | +0.5% | Global, especially Asia, Europe | Long-term |

LNG Tank Container Market Restraints Impact Analysis

Despite its significant growth potential, the LNG tank container market faces several formidable restraints that could temper its expansion. One of the primary concerns revolves around the inherent volatility of natural gas prices. Fluctuations in global energy markets can directly impact the economic viability of LNG as a fuel or energy source, making long-term investment decisions challenging for potential users. Such price instability can deter companies from converting to LNG-fueled fleets or investing in new LNG-powered industrial processes, thereby slowing the demand for tank containers.

Another critical restraint is the high initial capital expenditure associated with investing in LNG infrastructure and the tank containers themselves. The specialized nature of LNG storage and transport necessitates robust, cryogenic containers and dedicated handling facilities, which come with a substantial upfront cost. This financial barrier can be particularly prohibitive for smaller businesses or in emerging markets where capital availability is limited. Additionally, stringent safety regulations and complex permitting processes surrounding the storage, handling, and transportation of a cryogenic and flammable substance like LNG can add layers of complexity, cost, and time delays to projects, further impacting market growth by increasing operational hurdles and compliance burdens.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Natural Gas Prices | -1.2% | Global | Short to Medium-term |

| High Capital Investment and Infrastructure Costs | -0.9% | Emerging Markets, Developing Nations | Long-term |

| Stringent Safety Regulations and Permitting | -0.7% | Global, Highly Regulated Regions | Ongoing |

| Competition from Alternative Energy Sources | -0.4% | Developed Markets | Long-term |

LNG Tank Container Market Opportunities Impact Analysis

The LNG tank container market is poised to capitalize on several promising opportunities that align with global energy trends and logistical advancements. A significant opportunity lies in the continued expansion of small-scale LNG supply chains, particularly in regions lacking extensive pipeline networks or access to large-scale regasification terminals. These smaller, more agile distribution networks leverage the flexibility of tank containers to deliver LNG to remote industrial facilities, power plants, and residential areas, opening up new market segments and ensuring energy access where it was previously unfeasible.

Furthermore, the maritime and heavy-duty transport sectors present a substantial growth avenue as industries seek to comply with increasingly strict emission regulations, such as those set by the International Maritime Organization (IMO). LNG is emerging as a preferred alternative fuel for ships and trucks due to its lower emissions of sulfur oxides, nitrogen oxides, and particulate matter compared to conventional fuels. This shift translates directly into a heightened demand for LNG bunkering solutions and land-based refueling infrastructure, significantly driving the need for LNG tank containers. The ongoing development of new international trade corridors and the increasing recognition of LNG as a versatile and reliable energy source for various off-grid and peak-shaving applications further contribute to a robust opportunity landscape for the LNG tank container market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Small-Scale LNG Distribution | +1.5% | Asia Pacific, Emerging Markets | Long-term |

| Increasing Adoption of LNG as Marine and Vehicle Fuel | +1.3% | Global, Europe, North America | Medium to Long-term |

| Expansion into New Geographies and Trade Routes | +0.9% | Africa, Latin America, Southeast Asia | Long-term |

| Technological Innovation in Container Design | +0.6% | Global | Short to Medium-term |

LNG Tank Container Market Challenges Impact Analysis

The LNG tank container market, while promising, must navigate several significant challenges that could impede its growth trajectory. One notable challenge is the persistent concern around safety and public perception. Despite advancements in design and strict regulations, the transportation of cryogenic and flammable materials like LNG carries inherent risks. Public apprehension, often exacerbated by a lack of understanding or isolated incidents, can lead to opposition to new infrastructure projects (the "Not In My Backyard" or NIMBY effect) and logistical routes, potentially slowing down market expansion and increasing project costs due to prolonged approval processes and additional safety measures.

Another critical challenge lies in the complex regulatory landscape and the need for global standardization. Different regions and countries have varying regulations concerning the design, testing, certification, and operation of LNG tank containers. This lack of universal standards can create barriers to international trade and multimodal transport, increasing operational complexities and costs for companies operating across diverse jurisdictions. Furthermore, the development of adequate refueling and storage infrastructure, especially in emerging markets, poses a significant hurdle. While demand for LNG might be present, the absence of robust supply chain infrastructure, including bunkering stations and road networks capable of handling heavy loads, can limit the practical application and adoption of LNG tank containers, creating bottlenecks in the overall market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Safety Concerns and Public Perception | -0.8% | Global, Populated Areas | Long-term |

| Regulatory Complexities and Lack of Standardization | -0.6% | International Trade, Diverse Regions | Ongoing |

| Infrastructure Bottlenecks in Emerging Markets | -0.5% | Asia Pacific, Africa, Latin America | Medium to Long-term |

| Geopolitical Instability Affecting Supply Chains | -0.3% | Global, Conflict Zones | Short-term |

LNG Tank Container Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global LNG Tank Container Market, covering crucial aspects of market dynamics, competitive landscape, and future growth trajectories. The report is meticulously prepared to offer strategic insights for stakeholders, investors, and business professionals seeking to understand the current state and future potential of this vital industry segment.

| Report Attributes | Report Details |

|---|---|

| Report Name | LNG Tank Container Market |

| Market Size in 2025 | USD 350 Million |

| Market Forecast in 2033 | USD 585 Million |

| Growth Rate | CAGR of 2025 to 2033 6.7% |

| Number of Pages | 200 |

| Key Companies Covered | CIMC, Rootselaar Group, FURUISE, Uralcryomash, UBH International, M1 Engineering, Air Water Plant & Engineering, LUXI Group, Corban Energy Group, Bewellcn Shanghai |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

:Understanding the LNG tank container market through its various segmentations provides a granular view of its structure and evolving dynamics. This comprehensive analysis allows businesses to pinpoint specific areas of growth, identify niche markets, and tailor strategies to address distinct requirements within the industry. The market is primarily segmented by the physical dimensions of the tank containers and by their diverse applications in the transportation sector, reflecting the varying needs of different end-use industries and logistical operations.

The segmentation by product type is crucial as it dictates the capacity and suitability of containers for different transport volumes and infrastructure constraints. Smaller containers offer greater flexibility for last-mile delivery and localized distribution, while larger units are more efficient for bulk transport over long distances. Similarly, the application segmentation highlights the critical role LNG tank containers play across different modes of transport, underscoring their versatility in facilitating the global movement of liquefied natural gas to meet growing energy demands in both established and emerging markets.

Market Product Type Segmentation:-- < 25 ft: These smaller tank containers are ideal for niche applications requiring lower volumes or for navigating areas with restricted access. They offer enhanced flexibility for localized distribution and are often used for small-scale industrial supply or as backup fuel sources.

- 25-40 ft: This segment represents the most common and versatile size range for LNG tank containers. These containers balance capacity with ease of intermodal transport, making them suitable for both land (road and rail) and marine transportation over medium to long distances. They are widely adopted for their efficiency in general LNG logistics.

- > 40 ft: Larger tank containers are designed for maximizing volume efficiency over longer hauls, particularly in marine transport where economies of scale are critical. These containers are used for bulk transport of LNG to major distribution hubs or large industrial consumers.

- Marine transportation: This segment involves the use of LNG tank containers for shipping liquefied natural gas across seas and oceans. It includes the supply of LNG for power generation, industrial use, and increasingly, as a bunkering fuel for LNG-powered vessels, driven by stringent maritime emission regulations and the push for cleaner shipping.

- Land transportation: This application encompasses the movement of LNG tank containers via road and rail networks. Road transport facilitates direct delivery to end-users such as industrial facilities, gas stations, or remote power plants, especially for small-scale and last-mile distribution. Rail transport is utilized for cost-effective bulk movement of LNG over long distances within continents, providing a crucial link in multimodal supply chains.

Regional Highlights

The global LNG tank container market exhibits distinct regional dynamics, driven by varying energy policies, infrastructure development, and demand for cleaner fuels. Identifying the leading regions and understanding their unique contributions is essential for strategic planning and market penetration.

-

Asia Pacific (APAC): This region is a dominant force in the LNG tank container market, primarily driven by robust economic growth, increasing industrialization, and rapidly escalating energy demands from countries like China, India, and Southeast Asian nations. The region's pivot towards cleaner energy sources to combat severe air pollution and meet decarbonization targets is fueling the adoption of LNG across power generation, industrial, and transportation sectors. Significant investments in LNG import terminals and pipeline infrastructure, coupled with the rising popularity of small-scale LNG solutions for off-grid energy access, further cement APAC's leading position.

-

Europe: Europe represents a mature yet dynamic market for LNG tank containers, heavily influenced by its energy security objectives and ambitious environmental regulations. Following geopolitical shifts, there's an intensified focus on diversifying gas supplies and reducing reliance on traditional pipeline gas, making LNG imports via tank containers an increasingly vital component of the energy mix. The continent is also at the forefront of adopting LNG as a marine and heavy-duty vehicle fuel, propelled by strict emissions standards and a well-developed network of bunkering and refueling stations, particularly in countries like Germany, France, and the Netherlands.

-

North America: The market in North America is significantly shaped by its abundant domestic natural gas production and growing export capabilities. While pipeline infrastructure is extensive, LNG tank containers are gaining traction for specialized applications such as peak shaving, industrial fueling in remote areas, and cross-border trade with Mexico and Canada. The region is also seeing an uptick in LNG as a transportation fuel, driven by economic incentives and environmental benefits, although adoption rates vary by state and province.

-

Middle East and Africa (MEA): This region is emerging as a significant player, particularly due to its vast natural gas reserves and a growing need for energy diversification and infrastructure development. Countries in the Middle East are investing in LNG export facilities, while African nations are exploring LNG imports via flexible container solutions to address energy deficits and power industrial growth. The nascent stage of small-scale LNG adoption and the potential for new trade routes represent substantial long-term growth opportunities.

-

Latin America: The LNG tank container market in Latin America is characterized by varying levels of development, with countries like Brazil, Argentina, and Chile showing increasing interest in LNG for power generation and industrial use. The flexibility of tank containers is particularly appealing in regions with challenging geographies or underdeveloped pipeline networks, allowing for decentralized energy supply and reducing reliance on more carbon-intensive fuels. Investments in regasification terminals and domestic distribution networks are key indicators of future market expansion.

Top Key Players:

The market research report covers the analysis of key stake holders of the LNG Tank Container Market. These companies represent leading manufacturers and solution providers, playing pivotal roles in innovation, production, and global distribution within the sector. Their strategic initiatives, product development, and geographic reach are crucial in shaping the competitive landscape of the market.

- CIMC

- Rootselaar Group

- FURUISE

- Uralcryomash

- UBH International

- M1 Engineering

- Air Water Plant & Engineering

- LUXI Group

- Corban Energy Group

- Bewellcn Shanghai

Frequently Asked Questions:

What is an LNG tank container?

An LNG tank container is a specialized intermodal container designed for the safe and efficient transport of liquefied natural gas (LNG). These containers are built to withstand extreme temperatures and pressures, typically featuring cryogenic insulation to maintain LNG in its liquid state at approximately -162°C (-260°F), enabling its multimodal shipment via road, rail, and sea.

What are the primary uses and applications of LNG tank containers?

LNG tank containers are primarily used for the flexible distribution of liquefied natural gas where traditional pipeline infrastructure is unavailable or uneconomical. Key applications include supplying LNG to industrial facilities, remote power plants, and residential areas, as well as providing LNG as a marine and heavy-duty vehicle fuel. They are crucial for small-scale LNG projects and cross-border trade.

What are the key benefits of using LNG tank containers for transport?

The main benefits of using LNG tank containers include their versatility for multimodal transport (road, rail, sea), enabling access to diverse markets and remote locations. They offer enhanced logistical flexibility, reduced infrastructure costs compared to pipelines, and promote the use of cleaner-burning fuel, contributing to lower emissions and improved environmental performance in the supply chain.

What safety standards govern LNG tank containers?

LNG tank containers are governed by rigorous international and national safety standards due to the cryogenic and flammable nature of LNG. Key regulations include those set by the International Maritime Organization (IMO) for marine transport, ISO standards for intermodal containers, and various national hazardous materials transport regulations (e.g., ADR for road transport in Europe, DOT in the USA). These standards cover design, construction, testing, certification, and operational procedures.

What factors are driving the growth of the LNG tank container market?

The market's growth is primarily driven by the increasing global demand for cleaner energy sources, stricter environmental regulations promoting LNG adoption, and the expansion of small-scale LNG applications for remote and industrial uses. Furthermore, advancements in tank container technology improving efficiency and safety, along with the growing use of LNG as a marine and heavy-duty vehicle fuel, are significant growth contributors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted