LNG Carrier Containment Market

LNG Carrier Containment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710140 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

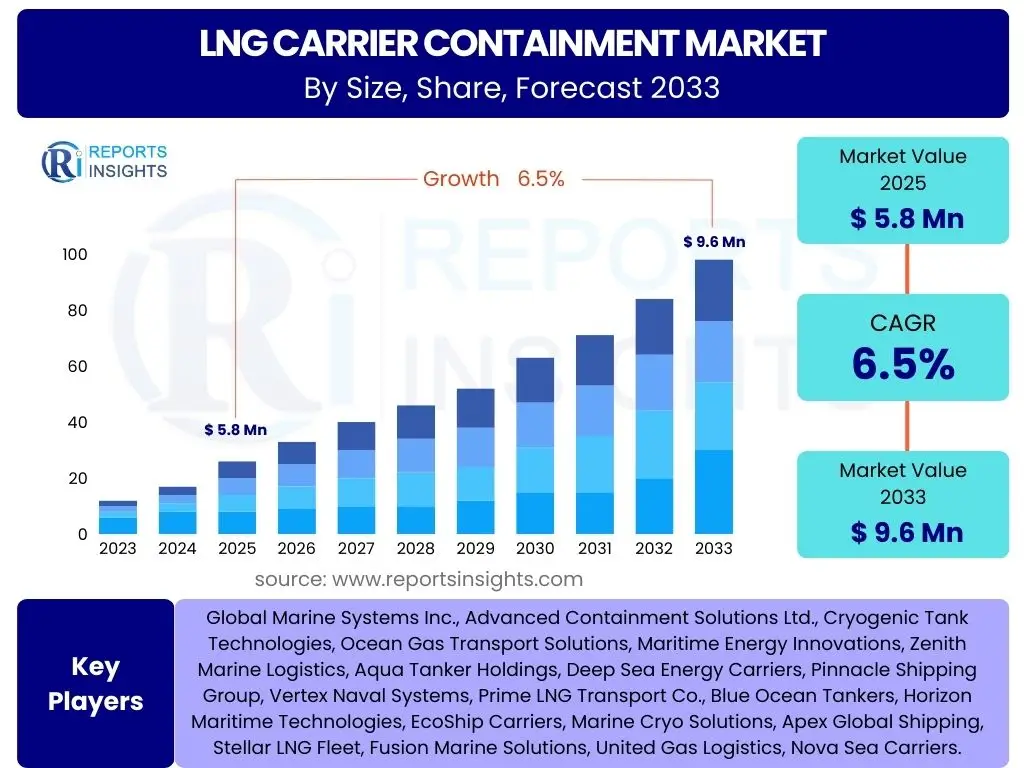

LNG Carrier Containment Market Size

According to Reports Insights Consulting Pvt Ltd, The LNG Carrier Containment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

Key LNG Carrier Containment Market Trends & Insights

The LNG Carrier Containment market is currently experiencing significant transformative shifts driven by global energy demand, environmental regulations, and technological innovation. A primary trend involves the increasing adoption of advanced membrane-type containment systems, which offer superior cargo capacity and structural efficiency compared to traditional spherical (Moss) tanks. This preference is largely due to their enhanced payload capabilities and reduced boil-off rates, making them economically attractive for long-haul voyages and large-scale projects.

Another prominent insight is the growing emphasis on decarbonization within the shipping industry, which directly influences the design and operation of LNG carriers. This includes the integration of dual-fuel propulsion systems that can utilize LNG as fuel, further improving environmental performance. Furthermore, the market is witnessing a move towards digitalization and smart ship technologies, enabling better monitoring, predictive maintenance, and operational optimization of containment systems, thereby enhancing safety and efficiency across the fleet.

- Shift towards advanced membrane containment systems for higher efficiency and capacity.

- Increasing adoption of dual-fuel LNG carriers to meet stringent emission regulations.

- Enhanced focus on boil-off gas management systems for improved operational economics.

- Integration of smart technologies for real-time monitoring and predictive maintenance.

- Expansion of small-scale LNG infrastructure and bunkering services driving demand for diverse vessel types.

- Emergence of floating storage and regasification units (FSRUs) as flexible energy solutions.

AI Impact Analysis on LNG Carrier Containment

The impact of Artificial Intelligence (AI) on the LNG Carrier Containment sector is becoming increasingly profound, particularly in optimizing operational efficiency and enhancing safety protocols. AI-powered analytics are being deployed for predictive maintenance, allowing operators to anticipate equipment failures within containment systems and address them proactively, thereby minimizing downtime and reducing maintenance costs. This capability extends to monitoring the integrity of insulation layers, detecting minor leaks, and assessing structural stresses in real-time, which are crucial for the safe transport of cryogenic liquids.

Furthermore, AI is revolutionizing route optimization for LNG carriers, leveraging complex algorithms to analyze weather patterns, ocean currents, and port congestion. This not only leads to more fuel-efficient voyages but also helps in mitigating risks associated with adverse conditions, ensuring the safe delivery of LNG. Beyond operational aspects, AI is also instrumental in the design phase of new containment systems, enabling engineers to simulate various scenarios and optimize material usage and structural configurations for enhanced performance and safety, thereby pushing the boundaries of current design capabilities.

- Predictive maintenance for containment systems, reducing unplanned downtime.

- Enhanced real-time monitoring of tank integrity, insulation, and cargo conditions.

- AI-driven route optimization for improved fuel efficiency and operational safety.

- Data analytics for better boil-off gas management and energy efficiency.

- Support for autonomous or semi-autonomous vessel operations, including cargo handling.

- Optimized design and simulation of new containment technologies.

Key Takeaways LNG Carrier Containment Market Size & Forecast

The LNG Carrier Containment market is poised for robust growth through 2033, primarily driven by the escalating global demand for natural gas as a transitional fuel and the expansion of LNG trade routes. The projected Compound Annual Growth Rate (CAGR) underscores a sustained investment in new vessel construction and the retrofitting of existing carriers to meet evolving industry standards and capacity requirements. This growth is intrinsically linked to geopolitical shifts impacting energy security and a broader global commitment to reducing carbon emissions, where LNG serves as a cleaner alternative to traditional fossil fuels.

Key takeaways indicate a significant shift towards technological sophistication, with membrane-type systems dominating newbuild orders due to their superior volumetric efficiency and lower boil-off rates. The market forecast also highlights the critical role of innovation in addressing operational challenges, such as optimizing cargo handling, enhancing safety features, and integrating advanced digital solutions for fleet management. These advancements are essential for maximizing the economic viability and environmental performance of LNG transport, ensuring the market's trajectory remains positive and responsive to industry demands.

- Market poised for substantial growth, driven by global natural gas demand.

- Strong investment in new LNG carrier construction and fleet expansion.

- Technological advancements, especially in membrane systems, are key growth enablers.

- Increasing focus on energy security and cleaner fuel adoption globally.

- Digitalization and AI integration are transforming operational efficiency and safety.

- Asia-Pacific expected to remain a dominant region for demand and investment.

LNG Carrier Containment Market Drivers Analysis

The LNG Carrier Containment market is primarily propelled by the escalating global demand for liquefied natural gas, driven by its role as a cleaner alternative to coal and oil in power generation and industrial applications. This demand fuels the expansion of liquefaction and regasification infrastructure worldwide, necessitating a larger and more sophisticated fleet of LNG carriers. Countries increasingly prioritize energy security, leading to diversified energy portfolios that include LNG, thus stimulating long-term contracts for LNG trade and, consequently, demand for new containment solutions.

Furthermore, stringent environmental regulations imposed by the International Maritime Organization (IMO) and national bodies are accelerating the transition to cleaner marine fuels, with LNG being a prime choice. This not only encourages the construction of new LNG-fueled vessels but also prompts the retrofitting of existing ships with advanced containment systems that minimize methane slip and improve overall environmental performance. The continuous innovation in containment technology, particularly in membrane systems offering higher cargo capacity and reduced boil-off rates, acts as a significant driver, enhancing the economic viability and operational efficiency of LNG transport.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global LNG Demand | +2.1% | Asia-Pacific, Europe, Emerging Markets | 2025-2033 |

| Stricter Environmental Regulations (IMO 2020, EEXI/CII) | +1.7% | Global, particularly Europe, North America | 2025-2033 |

| Energy Security Concerns & Diversification | +1.5% | Europe, Asia-Pacific, North America | 2025-2033 |

| Advancements in Containment Technology | +0.8% | Global, especially ship-building hubs | 2025-2033 |

| Expansion of LNG Bunkering Infrastructure | +0.4% | Key shipping lanes, major ports | 2025-2033 |

LNG Carrier Containment Market Restraints Analysis

Despite robust growth prospects, the LNG Carrier Containment market faces several significant restraints. One primary challenge is the substantial capital expenditure required for the construction of new LNG carriers, which feature sophisticated containment systems. The high cost of specialized materials, advanced manufacturing processes, and the long lead times associated with shipbuilding can deter investment, particularly for smaller market participants or during periods of economic uncertainty. This financial barrier limits the pace of fleet expansion and the adoption of cutting-edge technologies.

Furthermore, geopolitical instabilities and volatile energy prices can introduce unpredictability into the LNG trade landscape. Fluctuations in LNG supply and demand, often influenced by international relations or conflicts, can impact charter rates and the overall profitability of LNG shipping, making long-term investment decisions riskier. Additionally, the development of alternative low-carbon fuels, such as green hydrogen or ammonia, poses a potential long-term threat to LNG's dominance as a transition fuel, which could eventually temper the demand for new LNG carriers and their containment systems. Regulatory hurdles and complex permitting processes in certain regions can also delay or complicate new projects, further impeding market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Newbuilds | -1.2% | Global, impacts shipowners & operators | 2025-2033 |

| Geopolitical Instability & Trade Volatility | -0.9% | Global, impacts specific trade routes | 2025-2033 |

| Fluctuating LNG Prices | -0.8% | Global market, impacts investment decisions | 2025-2033 |

| Competition from Alternative Fuels (Hydrogen, Ammonia) | -0.5% | Global, long-term impact | 2030-2033 |

| Skilled Labor Shortage in Shipbuilding | -0.3% | Major shipbuilding countries (Asia-Pacific) | 2025-2033 |

LNG Carrier Containment Market Opportunities Analysis

The LNG Carrier Containment market is rich with opportunities, primarily driven by the ongoing global energy transition and the expansion of the natural gas value chain. One significant area of opportunity lies in the burgeoning small-scale LNG market. As countries and remote regions seek access to cleaner energy, the demand for smaller LNG carriers and specialized containment solutions for localized distribution and bunkering is rapidly increasing. This segment requires innovative, modular, and cost-effective containment systems that can serve diverse applications, including coastal transport and island supply, opening new avenues for technology providers.

Another compelling opportunity stems from the development of Floating Storage and Regasification Units (FSRUs) and Floating Liquefied Natural Gas (FLNG) vessels. These offshore solutions offer flexibility and rapid deployment for importing or exporting LNG, bypassing the need for extensive onshore infrastructure. The design and construction of containment systems for FSRUs and FLNGs present unique technical challenges and opportunities for specialized engineering firms. Furthermore, the imperative for decarbonization within the shipping sector creates a substantial market for retrofitting existing vessels with advanced boil-off gas management systems and potentially new containment types, ensuring compliance with evolving environmental regulations and improving operational efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Small-Scale LNG Market | +1.4% | Emerging markets, coastal regions | 2025-2033 |

| Development of FSRU and FLNG Projects | +1.3% | Global, particularly Asia-Pacific, Africa, Latin America | 2025-2033 |

| Technological Innovation in Boil-Off Gas Management | +1.0% | Global, for newbuilds and retrofits | 2025-2033 |

| Emergence of New LNG Trade Routes | +0.7% | Arctic, East Mediterranean, Africa | 2025-2033 |

| Retrofitting of Existing LNG Carriers | +0.5% | Europe, Asia-Pacific, established fleets | 2025-2033 |

LNG Carrier Containment Market Challenges Impact Analysis

The LNG Carrier Containment market faces various challenges that could impede its growth trajectory and operational efficiency. One significant challenge is the complexity and technical sophistication required for the design, construction, and maintenance of containment systems. These systems operate under extreme cryogenic conditions, demanding highly specialized materials, precise manufacturing techniques, and expert labor. Any error or deficiency in these aspects can lead to catastrophic failures, making safety and reliability paramount and driving up development and operational costs.

Another pressing challenge is the increasing cybersecurity threat landscape. As LNG carriers become more integrated with digital technologies and autonomous systems, they become vulnerable to cyberattacks that could compromise operational control, navigation systems, or critical containment monitoring systems. Protecting these vessels from sophisticated cyber threats requires continuous investment in robust security infrastructure and personnel training, adding to the operational burden. Furthermore, the volatility in global LNG prices and the long-term investment horizons for new carriers create financial risks, as economic conditions or shifts in energy policy can significantly impact the profitability of these assets over their lifespan, requiring careful market analysis and hedging strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Cryogenic Engineering & Construction | -1.1% | Global, affects shipbuilding and design | 2025-2033 |

| Cybersecurity Threats to Integrated Systems | -0.9% | Global, impacts fleet operations | 2025-2033 |

| Strict Regulatory Compliance & Safety Standards | -0.7% | Global, impacts operational costs | 2025-2033 |

| Supply Chain Disruptions for Specialized Materials | -0.6% | Global, impacts lead times | 2025-2033 |

| Attracting & Retaining Skilled Workforce | -0.4% | Major shipbuilding and maritime nations | 2025-2033 |

LNG Carrier Containment Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global LNG Carrier Containment Market, covering historical performance from 2019 to 2023 and offering detailed forecasts up to 2033. The scope encompasses a thorough examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It includes an assessment of technological advancements, competitive landscape, and the impact of emerging trends such as AI integration and environmental regulations on market dynamics. The report aims to provide strategic insights for stakeholders, enabling informed decision-making in this critical energy transport sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Marine Systems Inc., Advanced Containment Solutions Ltd., Cryogenic Tank Technologies, Ocean Gas Transport Solutions, Maritime Energy Innovations, Zenith Marine Logistics, Aqua Tanker Holdings, Deep Sea Energy Carriers, Pinnacle Shipping Group, Vertex Naval Systems, Prime LNG Transport Co., Blue Ocean Tankers, Horizon Maritime Technologies, EcoShip Carriers, Marine Cryo Solutions, Apex Global Shipping, Stellar LNG Fleet, Fusion Marine Solutions, United Gas Logistics, Nova Sea Carriers. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LNG Carrier Containment market is extensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation helps in identifying specific growth areas, technological preferences, and operational requirements across different vessel types and applications. The primary categories for segmentation include containment type, which differentiates between established and emerging technologies like membrane and Moss systems, and vessel type, which categorizes carriers based on their specific function and size, ranging from conventional LNG carriers to specialized FSRUs and FLNGs.

Further segmentation by capacity allows for an analysis of market demand across various vessel sizes, from small-scale carriers serving niche markets to large Q-Max vessels facilitating major international trade routes. The application-based segmentation, encompassing seaborne trade, bunkering, and offshore solutions, highlights the varied end-uses of LNG transport and storage. This multi-dimensional segmentation is crucial for stakeholders to tailor their strategies, product development, and investment decisions to specific market needs and technological trends, ensuring comprehensive coverage of the evolving LNG value chain.

- By Containment Type: Membrane (e.g., GTT Mark III, NO96), Moss (Spherical), Type B (Prismatic), Type C (Cylindrical).

- By Vessel Type: Conventional LNG Carriers, Floating Storage and Regasification Units (FSRUs), Floating Liquefied Natural Gas (FLNG) Vessels, Small-Scale LNG Carriers.

- By Capacity: Small-sized (up to 40,000 cbm), Medium-sized (40,001 - 170,000 cbm), Large-sized (over 170,000 cbm, including Q-Flex and Q-Max).

- By Application: Seaborne LNG Trade, LNG Bunkering, Offshore Regasification & Storage, Coastal & Regional Distribution.

Regional Highlights

- Asia-Pacific: Dominant market for LNG imports, driven by demand from China, Japan, South Korea, and India. Significant shipbuilding capabilities and increasing intra-regional trade.

- Europe: High focus on energy security and diversification of gas supplies, leading to increased LNG imports and FSRU deployments. Stringent environmental regulations drive demand for advanced carriers.

- North America: Emerging as a major LNG exporter, particularly from the United States. Expansion of liquefaction terminals fuels demand for new carriers.

- Middle East and Africa (MEA): Key region for LNG production (e.g., Qatar) and growing demand from African nations. Investment in FLNG projects and new trade routes.

- Latin America: Growing interest in LNG imports for power generation and industrial use, particularly in countries like Brazil and Argentina, driving FSRU and small-scale LNG adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LNG Carrier Containment Market.- Global Marine Systems Inc.

- Advanced Containment Solutions Ltd.

- Cryogenic Tank Technologies

- Ocean Gas Transport Solutions

- Maritime Energy Innovations

- Zenith Marine Logistics

- Aqua Tanker Holdings

- Deep Sea Energy Carriers

- Pinnacle Shipping Group

- Vertex Naval Systems

- Prime LNG Transport Co.

- Blue Ocean Tankers

- Horizon Maritime Technologies

- EcoShip Carriers

- Marine Cryo Solutions

- Apex Global Shipping

- Stellar LNG Fleet

- Fusion Marine Solutions

- United Gas Logistics

- Nova Sea Carriers

Frequently Asked Questions

What is the projected growth rate for the LNG Carrier Containment Market?

The LNG Carrier Containment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, reaching an estimated USD 9.6 Billion by 2033.

What are the primary drivers of the LNG Carrier Containment Market?

Key drivers include the increasing global demand for LNG as a cleaner fuel, stringent environmental regulations pushing for cleaner shipping, energy security concerns, and continuous advancements in containment technologies, particularly membrane systems.

How is AI impacting the LNG Carrier Containment sector?

AI is significantly impacting the sector through predictive maintenance for containment systems, enhanced real-time monitoring of tank integrity, AI-driven route optimization for efficiency and safety, and optimized design and simulation of new containment technologies.

Which containment types are most prevalent in new LNG carrier construction?

Membrane-type containment systems, such as GTT Mark III and NO96, are increasingly prevalent in new LNG carrier construction due to their superior volumetric efficiency, reduced boil-off rates, and suitability for larger capacities compared to traditional Moss-type spherical tanks.

What role do FSRUs and FLNGs play in the market?

Floating Storage and Regasification Units (FSRUs) and Floating Liquefied Natural Gas (FLNG) vessels offer flexible and rapid deployment solutions for importing and exporting LNG, reducing the need for extensive onshore infrastructure and presenting significant opportunities for specialized containment systems in offshore applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted