LNG As A Bunker Fuel Market

LNG As A Bunker Fuel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708332 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

LNG As A Bunker Fuel Market Size

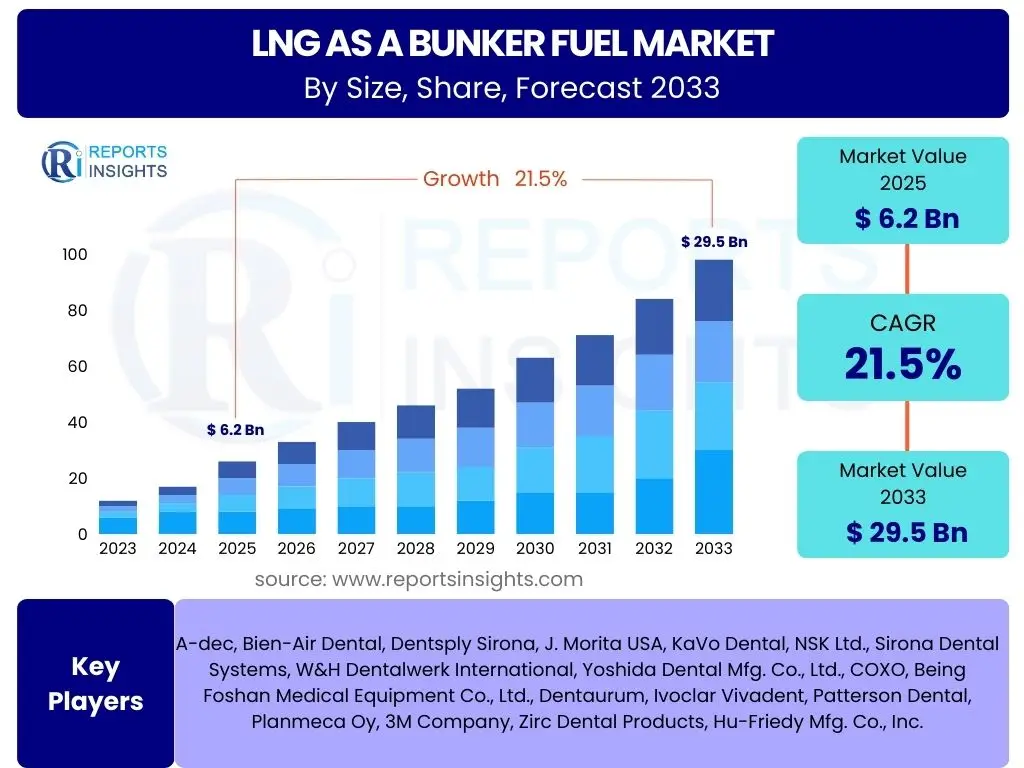

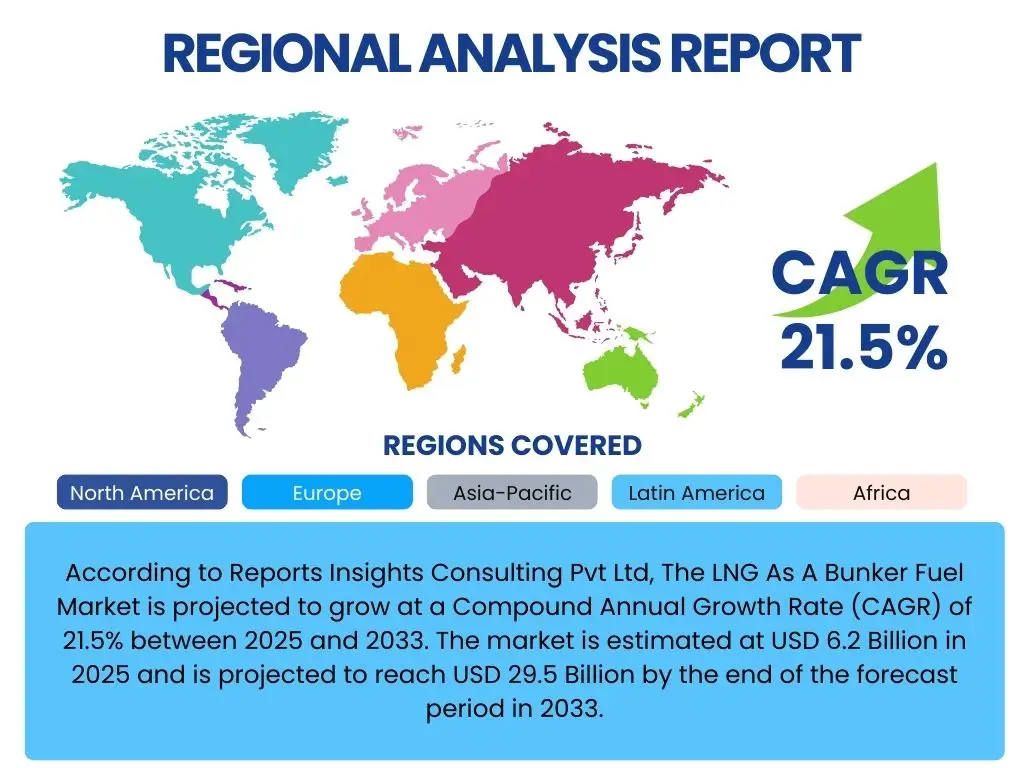

According to Reports Insights Consulting Pvt Ltd, The LNG As A Bunker Fuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 29.5 Billion by the end of the forecast period in 2033.

Key LNG As A Bunker Fuel Market Trends & Insights

The LNG as a bunker fuel market is significantly shaped by the global push towards decarbonization and stringent environmental regulations from organizations like the International Maritime Organization (IMO). Key insights reveal a growing preference for LNG due to its lower emissions profile compared to conventional marine fuels, particularly in reducing sulfur oxides (SOx) and nitrogen oxides (NOx), alongside a notable reduction in particulate matter. The industry is also witnessing rapid development in bunkering infrastructure and advancements in dual-fuel engine technology, making LNG a more viable and attractive option for various vessel types across different maritime sectors. Stakeholders frequently inquire about the pace of infrastructure development, the long-term cost competitiveness of LNG, and the potential for integrating more sustainable variants such as bio-LNG and synthetic LNG into the existing supply chain.

Furthermore, the trend towards larger vessels and increasing global trade volumes contributes to the demand for efficient and compliant fuel solutions. The maritime industry's commitment to achieving net-zero emissions by 2050 is a powerful long-term driver, positioning LNG as a crucial transition fuel. Strategic partnerships between energy companies, port authorities, and shipping lines are fostering the establishment of comprehensive bunkering networks, ensuring reliable supply and reducing logistical complexities. These collaborations are essential for overcoming initial investment hurdles and accelerating the market's expansion.

- Increasing adoption driven by IMO 2020 regulations and future emission reduction targets, including the EEXI and CII frameworks.

- Expansion of global LNG bunkering infrastructure and supply chains, particularly in major shipping hubs and emerging markets.

- Technological advancements in dual-fuel engines for enhanced efficiency, lower boil-off rates, and improved performance across various vessel sizes.

- Growing interest and pilot projects in bio-LNG and synthetic LNG (e-LNG) to further reduce the carbon footprint and ensure long-term sustainability.

- Strategic investments by port authorities and energy companies in the development of small-scale LNG terminals and mobile bunkering solutions.

- Rising awareness and corporate social responsibility initiatives among shipping companies to reduce environmental impact.

AI Impact Analysis on LNG As A Bunker Fuel

The integration of artificial intelligence within the LNG as a bunker fuel sector is primarily focused on enhancing operational efficiency, optimizing logistics, and ensuring stringent safety standards. User interest often revolves around how AI can streamline bunkering operations, predict maintenance needs for complex machinery, and improve overall supply chain management. AI is poised to provide predictive analytics for fuel consumption, optimize vessel routing for efficiency, and monitor emissions in real-time, thereby contributing to both economic benefits and environmental compliance. Expectations are high for AI to reduce human error and enhance decision-making in critical operations, particularly given the inherent complexities of handling cryogenic fuels.

The application of AI extends to optimizing the entire LNG value chain, from production and liquefaction to storage, transportation, and final bunkering. Predictive modeling can forecast demand fluctuations, allowing suppliers to manage inventory more effectively and minimize waste. In terms of safety, AI-powered surveillance and sensor networks can provide early detection of potential hazards, improving response times and mitigating risks associated with LNG handling. This technological evolution not only improves cost-efficiency but also reinforces the safety credentials of LNG as a marine fuel, addressing a key concern among potential adopters.

- Predictive maintenance for LNG engines, bunkering equipment, and storage tanks, minimizing downtime and extending asset lifespan.

- Optimization of bunkering schedules and vessel routes using real-time data to reduce fuel consumption, emissions, and operational costs.

- Real-time monitoring and analysis of emissions data to ensure regulatory compliance and provide actionable insights for environmental reporting.

- Enhanced safety protocols through AI-driven risk assessment, anomaly detection in operations, and automated alerts for potential hazards.

- Improved supply chain visibility and efficiency, from LNG production and liquefaction to last-mile delivery and bunkering operations.

- Autonomous or semi-autonomous bunkering systems, leveraging AI for precise positioning and flow control, reducing human error.

- Data analytics for market forecasting, identifying demand patterns, and optimizing pricing strategies for LNG bunker suppliers.

Key Takeaways LNG As A Bunker Fuel Market Size & Forecast

The LNG as a bunker fuel market is positioned for robust expansion, driven primarily by environmental mandates and the increasing availability of bunkering infrastructure. Key takeaways underscore the critical role of regulatory frameworks, such as the IMO's emission reduction targets, in accelerating market adoption. The market's future trajectory is heavily reliant on sustained investment in infrastructure development and the continuous innovation in propulsion technologies. The projected growth indicates a clear shift in maritime fuel preferences, reflecting a broader industry commitment to sustainability.

Stakeholders are increasingly focusing on the long-term economic viability and the pathway for integrating more sustainable variants like bio-LNG and synthetic LNG into the existing supply chain. The substantial projected market size by 2033 suggests that LNG is not merely a short-term compliance solution but a foundational component of the future maritime energy mix. Strategic collaborations, technological advancements, and supportive regulatory environments will be crucial in unlocking the full potential of this market and enabling the shipping industry to meet its decarbonization goals effectively.

- Significant market growth projected, with a CAGR of 21.5% from 2025 to 2033, underscoring strong industry confidence.

- Market valuation is expected to nearly quintuple, from USD 6.2 Billion in 2025 to USD 29.5 Billion by 2033, indicating a rapidly expanding sector.

- Continued expansion of bunkering infrastructure globally is paramount for widespread adoption and sustained market momentum.

- LNG offers a compelling and proven solution for meeting immediate and near-term emission reduction targets, particularly SOx, NOx, and particulate matter.

- Strategic collaborations between energy providers, ports, and shipping companies are crucial for fostering a robust and reliable supply chain.

- The market is evolving towards more sustainable forms of LNG, such as bio-LNG and synthetic LNG, signaling a cleaner and more diversified future for marine fuels.

- Regulatory stability and clarity regarding future emission standards will play a vital role in encouraging further investment and accelerating market transition.

LNG As A Bunker Fuel Market Drivers Analysis

The LNG as a bunker fuel market is propelled by a confluence of environmental, regulatory, and technological factors. Primarily, the stringent emission regulations imposed by the International Maritime Organization (IMO), notably the IMO 2020 sulfur cap and forthcoming greenhouse gas reduction targets, have significantly increased the demand for cleaner marine fuels. LNG offers a compliant solution by virtually eliminating SOx and particulate matter emissions, and substantially reducing NOx and CO2 emissions compared to traditional heavy fuel oil.

Beyond regulatory compliance, the increasing environmental consciousness within the shipping industry and among consumers drives demand for more sustainable shipping practices. This societal pressure encourages shipping companies to invest in LNG-fueled vessels, enhancing their corporate image and aligning with global decarbonization efforts. Furthermore, the expansion of LNG bunkering infrastructure in key maritime hubs, coupled with advancements in dual-fuel engine technology, makes LNG an increasingly practical and attractive option, diminishing previous barriers to adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Environmental Regulations (IMO 2020, EEXI, CII) | +6.5% | Global, particularly Europe and Asia Pacific | Short-to-Mid Term (2025-2030) |

| Growing Demand for Sustainable Shipping and Decarbonization | +5.0% | Global, driven by corporate ESG goals | Mid-to-Long Term (2026-2033) |

| Expansion of Global LNG Bunkering Infrastructure | +4.0% | Major shipping routes and port hubs (Singapore, Rotterdam) | Mid Term (2025-2030) |

| Technological Advancements in Dual-Fuel Engines | +3.5% | Global, driven by shipbuilding innovation | Short-to-Mid Term (2025-2029) |

| Favorable Price Competitiveness of LNG Compared to Compliant Fuels | +2.5% | Regionally variable, linked to natural gas prices | Variable (Short-to-Long Term) |

LNG As A Bunker Fuel Market Restraints Analysis

Despite significant growth potential, the LNG as a bunker fuel market faces several notable restraints that could temper its expansion. One of the primary barriers is the high upfront capital investment required for constructing new LNG-fueled vessels or converting existing ones. This substantial initial cost, encompassing specialized engines, cryogenic fuel tanks, and safety systems, can deter shipowners, particularly smaller operators, from making the transition, despite the long-term operational cost savings and environmental benefits.

Another significant restraint is the limited availability of bunkering infrastructure in certain regions and ports. While major maritime hubs are rapidly developing LNG bunkering capabilities, many smaller or less frequented ports still lack the necessary facilities, restricting the operational flexibility of LNG-fueled vessels. Furthermore, concerns regarding the price volatility of natural gas, which directly impacts LNG prices, introduce an element of financial uncertainty for fleet operators. Regulatory uncertainty beyond current mandates and the ongoing debate surrounding methane slip from LNG engines also present challenges, influencing investment decisions and public perception.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment for Newbuilds and Conversions | -3.5% | Global, impacts smaller shipping companies | Mid-to-Long Term (2025-2033) |

| Limited LNG Bunkering Infrastructure in Certain Regions | -3.0% | Developing maritime nations, secondary ports | Mid Term (2025-2030) |

| Price Volatility of Natural Gas | -2.0% | Global, linked to energy market dynamics | Variable (Short-to-Long Term) |

| Concerns Regarding Methane Slip from LNG Engines | -1.5% | Global, impacts long-term GHG reduction targets | Mid-to-Long Term (2028-2033) |

| Regulatory Uncertainty Beyond Current IMO Mandates | -1.0% | Global, impacts long-term investment planning | Long Term (2030-2033) |

LNG As A Bunker Fuel Market Opportunities Analysis

The LNG as a bunker fuel market is ripe with opportunities that can accelerate its growth and solidify its position as a leading alternative marine fuel. A significant opportunity lies in the rapid development of small-scale LNG terminals and mobile bunkering solutions, which can serve smaller ports and regions where extensive fixed infrastructure is not yet economically viable. This expansion of accessible bunkering points will significantly enhance the operational flexibility and appeal of LNG-fueled vessels, broadening the market beyond established global hubs.

Furthermore, the increasing adoption of LNG in a wider range of vessel types, beyond traditional container ships and tankers, presents substantial growth avenues. Cruise ships, ferries, Ro-Ro vessels, and even offshore supply vessels are increasingly turning to LNG for environmental compliance and operational efficiency. The integration of bio-LNG and synthetic LNG into the existing supply chain offers a compelling pathway to further decarbonize shipping, appealing to companies with ambitious net-zero targets and positioning LNG as a truly sustainable long-term solution. Government incentives and funding for green shipping initiatives also provide a strong impetus for market development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Small-Scale LNG Terminals and Mobile Bunkering | +4.5% | Emerging markets and smaller ports globally | Mid-to-Long Term (2026-2033) |

| Increasing Adoption in Diverse Vessel Types (Cruise, Ferries, Ro-Ro) | +4.0% | Global, driven by specific niche markets | Short-to-Mid Term (2025-2030) |

| Integration of Bio-LNG and Synthetic LNG into Supply Chain | +3.5% | Global, particularly regions with strong sustainability goals | Long Term (2028-2033) |

| Government Incentives and Funding for Green Shipping Initiatives | +3.0% | Europe, Asia Pacific (e.g., EU Green Deal, specific national programs) | Short-to-Mid Term (2025-2030) |

| Development of Robust Digital Platforms for Bunkering Optimization | +2.0% | Global, enhancing efficiency across the value chain | Mid Term (2027-2032) |

LNG As A Bunker Fuel Market Challenges Impact Analysis

The LNG as a bunker fuel market, while promising, must navigate several significant challenges that could impede its trajectory. One key challenge is the complexity of the global regulatory landscape, which, despite offering environmental incentives, can be fragmented and subject to change. Varying local and regional regulations for LNG handling, storage, and safety can create operational hurdles and increase compliance costs for international shipping companies, making standardized operations difficult across diverse jurisdictions.

Another substantial challenge stems from the competition posed by other emerging alternative fuels, such as methanol, ammonia, and hydrogen. While these alternatives are still in earlier stages of development for marine applications, their potential for deeper decarbonization in the long run presents a future competitive threat to LNG. Furthermore, overcoming public perception of natural gas as a "transition" fuel, rather than a definitive long-term solution, requires continuous industry efforts to highlight its immediate environmental benefits and the pathway towards renewable LNG variants. Supply chain disruptions, often influenced by geopolitical events or natural disasters, can also pose challenges to fuel availability and price stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Evolving Global Regulatory Landscape | -2.5% | Global, impacting compliance and investment decisions | Mid-to-Long Term (2025-2033) |

| Competition from Emerging Alternative Fuels (Methanol, Ammonia, Hydrogen) | -2.0% | Global, especially in long-term decarbonization strategies | Long Term (2030-2033) |

| Establishing Standardized Safety Protocols and Training | -1.8% | Global, impacts operational readiness and risk management | Short-to-Mid Term (2025-2029) |

| Public Perception and "Transition Fuel" Narrative | -1.2% | Global, influences investor confidence and policy support | Mid-to-Long Term (2027-2033) |

| Potential Supply Chain Disruptions and Infrastructure Vulnerabilities | -1.0% | Regionally specific, impacts fuel availability and pricing | Variable (Short Term) |

LNG As A Bunker Fuel Market - Updated Report Scope

This report provides a comprehensive and in-depth analysis of the global LNG as a bunker fuel market, covering historical trends, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges influencing the industry from 2019 to 2033. The scope includes detailed segmentation analysis by vessel type, bunkering method, and geographical regions, offering a granular view of market performance and potential. Furthermore, the report assesses the impact of emerging technologies like Artificial Intelligence on market operations and supply chain efficiencies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 29.5 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shell, TotalEnergies, ExxonMobil, BP, Equinor, FueLNG, CMA CGM, Crowley Maritime, Sumitomo Corporation, Kawasaki Kisen Kaisha (K Line), Mitsui O.S.K. Lines (MOL), Wärtsilä, Gasum, Korea Gas Corporation (KOGAS), Cheniere Energy, NYK Line, Petronas, Port of Rotterdam, QatarEnergy, Eni S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The segmentation analysis of the LNG as a bunker fuel market provides a granular understanding of demand patterns across various vessel types and bunkering methodologies. This detailed breakdown highlights the specific requirements and growth trajectories within different maritime sectors, offering insights into where investment and infrastructure development are most critical. Understanding these segments is vital for stakeholders to tailor their services, optimize supply chains, and strategically position themselves in this evolving market. Each segment presents unique opportunities and challenges influenced by vessel operational profiles, trade routes, and regulatory pressures.

For instance, the adoption rate of LNG varies significantly across vessel types due to differing fuel consumption patterns, voyage lengths, and economic considerations for retrofitting or newbuilds. Similarly, bunkering methods are chosen based on port infrastructure, vessel size, and operational efficiency, with Ship-to-Ship (STS) being dominant in major ports and Truck-to-Ship (TTS) catering to smaller demand or less developed facilities. This comprehensive segmentation allows for a precise evaluation of market potential and the development of targeted strategies.

- By Vessel Type

- Container Ships

- Tankers

- Bulk Carriers

- Ferries & Ro-Ro

- Cruise Ships

- Others (Offshore Vessels, Car Carriers, Tugs)

- By Bunkering Method

- Ship-to-Ship (STS)

- Truck-to-Ship (TTS)

- Port-to-Ship (PTS)

- Others (Barge-to-Ship, Container-to-Ship)

Regional Highlights

- Europe: Leading the global adoption of LNG as a bunker fuel, driven by stringent EU environmental policies, extensive inland waterway networks, and well-established bunkering hubs in ports like Rotterdam, Amsterdam, and major Nordic ports. The region benefits from robust government support and a proactive approach to sustainable shipping.

- Asia Pacific (APAC): A rapidly growing market with significant potential, characterized by increasing maritime trade and strategic bunkering locations in Singapore, China (Shanghai, Shenzhen, Ningbo), Japan, and South Korea. This growth is supported by national government initiatives for green shipping and substantial investments in port infrastructure.

- North America: An emerging market with increasing interest in coastal shipping, the Great Lakes, and inland waterways. Adoption is primarily driven by US EPA regulations (especially in Emission Control Areas) and the abundant availability of natural gas resources, supporting the development of regional bunkering facilities.

- Middle East & Africa (MEA): Gaining strategic importance due to major oil and gas producers (e.g., UAE, Qatar) exploring diversification into bunkering services for global maritime traffic, particularly through the Suez Canal. Investments in port infrastructure are increasing to support LNG bunkering capabilities.

- Latin America: A nascent but developing market with potential for growth in countries like Brazil, Mexico, and Chile, as regional trade expands and environmental awareness increases. Development is slower than other regions but is poised for acceleration with increasing investment and regulatory clarity.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LNG As A Bunker Fuel Market.

- Shell

- TotalEnergies

- ExxonMobil

- BP

- Equinor

- FueLNG (joint venture between Shell and Keppel Offshore & Marine)

- CMA CGM

- Crowley Maritime Corporation

- Sumitomo Corporation

- Kawasaki Kisen Kaisha (K Line)

- Mitsui O.S.K. Lines (MOL)

- Wärtsilä Corporation

- Gasum Ltd.

- Korea Gas Corporation (KOGAS)

- Cheniere Energy, Inc.

- NYK Line (Nippon Yusen Kaisha)

- Petronas

- Port of Rotterdam

- QatarEnergy

- Eni S.p.A.

- Fluxys SA

Frequently Asked Questions

What is driving the growth of the LNG as a bunker fuel market?

The primary drivers are stringent environmental regulations from the International Maritime Organization (IMO) and local authorities, the necessity for lower-emission marine fuels to reduce air pollution, and the expanding global infrastructure for LNG bunkering and supply.

How much is the LNG as a bunker fuel market expected to grow by 2033?

The market is projected to reach USD 29.5 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 21.5% from an estimated USD 6.2 Billion in 2025.

What are the main environmental benefits of using LNG as a marine fuel?

LNG virtually eliminates sulfur oxides (SOx) and particulate matter, significantly reduces nitrogen oxides (NOx) by up to 85%, and lowers carbon dioxide (CO2) emissions by up to 25% compared to conventional marine fuels, helping ships meet stringent emission standards.

What are the key challenges facing the LNG as a bunker fuel market?

Major challenges include high upfront capital investment for new vessels or conversions, the still-developing global bunkering infrastructure in some regions, the price volatility of natural gas, and the competitive emergence of other alternative fuels like methanol and ammonia.

Which regions are leading the adoption of LNG as a bunker fuel?

Europe, particularly ports like Rotterdam and Amsterdam, is leading in adoption due to robust environmental policies. Asia Pacific, with key hubs like Singapore, China, Japan, and South Korea, is experiencing rapid growth driven by expanding trade and significant investments in bunkering infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted