Lithography Machine Market

Lithography Machine Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707423 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

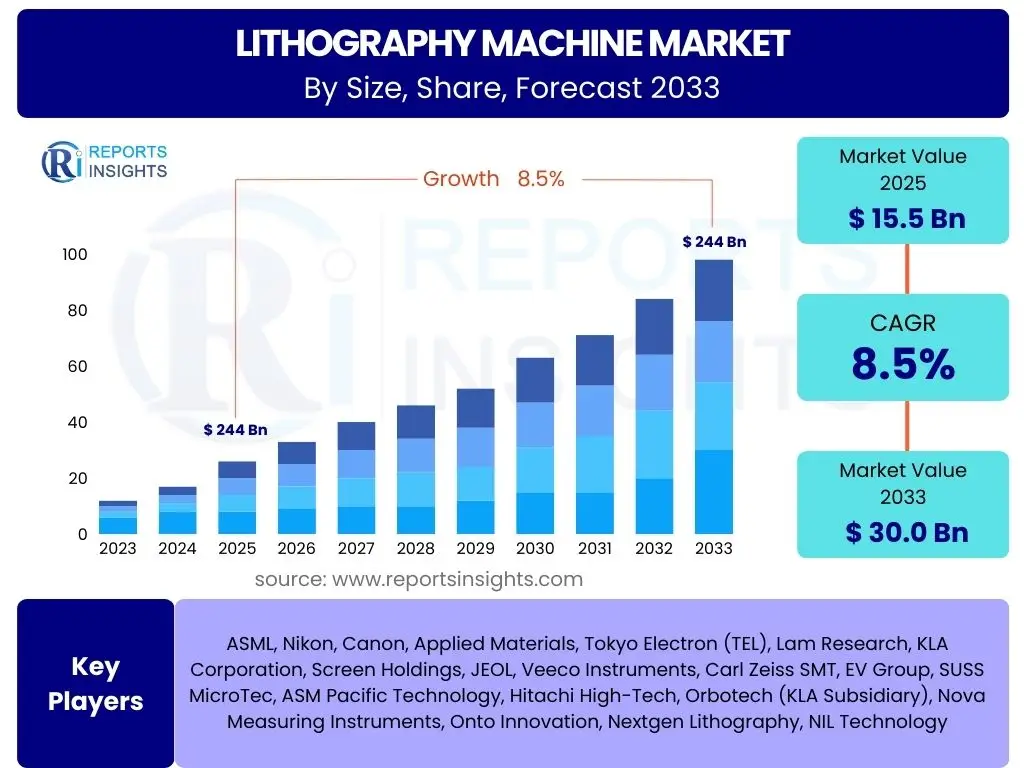

Lithography Machine Market Size

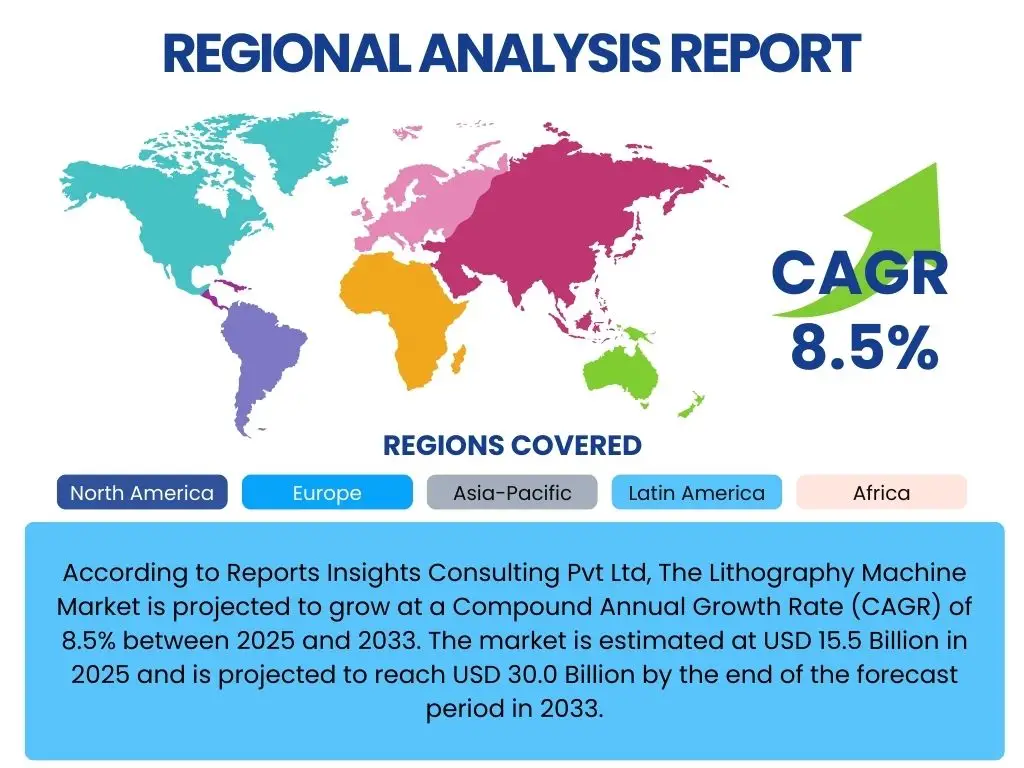

According to Reports Insights Consulting Pvt Ltd, The Lithography Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 15.5 Billion in 2025 and is projected to reach USD 30.0 Billion by the end of the forecast period in 2033.

Key Lithography Machine Market Trends & Insights

The Lithography Machine market is experiencing profound shifts driven by the relentless pursuit of miniaturization and increased computational power within the semiconductor industry. Common user inquiries often revolve around the adoption of next-generation technologies like Extreme Ultraviolet (EUV) lithography, the integration of artificial intelligence for process optimization, and the industry's response to global supply chain challenges. These trends highlight a market focused on overcoming complex technical hurdles to meet the surging demand for advanced chips across diverse applications, from high-performance computing to IoT devices. The market is also witnessing a strong emphasis on sustainability and energy efficiency in manufacturing processes, given the substantial energy requirements of lithography equipment.

Another significant trend is the diversification of lithography applications beyond traditional silicon wafers, including advanced packaging, micro-LEDs, and MEMS. This expansion is pushing the boundaries of existing lithography techniques while also spurring investment in novel approaches such as High-NA EUV, which promises even finer resolution. Furthermore, the strategic importance of semiconductor manufacturing has led to increased government investments and subsidies in various regions, aiming to bolster domestic production capabilities and reduce reliance on single-source suppliers. These initiatives are fostering a competitive yet collaborative environment for technological innovation and market expansion.

- Accelerated adoption of Extreme Ultraviolet (EUV) lithography for sub-7nm node manufacturing.

- Increased integration of AI and machine learning for predictive maintenance, process control, and defect detection.

- Growing demand for advanced packaging technologies requiring high-resolution lithography solutions.

- Focus on energy efficiency and sustainable manufacturing practices in lithography processes.

- Emergence of High-NA EUV technology to enable further scaling beyond current capabilities.

- Diversification of lithography applications into photonics, quantum computing, and bio-sensors.

- Regionalization of semiconductor manufacturing driving investment in new lithography fabs.

AI Impact Analysis on Lithography Machine

Common user questions related to the impact of AI on Lithography Machine technology frequently explore how artificial intelligence can enhance productivity, improve yield, and reduce operational costs. Users are keen to understand if AI can automate complex decision-making processes, optimize exposure parameters, or identify subtle anomalies that human operators might miss. There is a clear expectation that AI will play a transformative role in pushing the limits of resolution and throughput, while also addressing the inherent complexities and variability in semiconductor manufacturing.

AI's influence extends across the entire lithography workflow, from initial design verification and mask inspection to real-time process monitoring and predictive maintenance of the sophisticated equipment. By leveraging vast datasets generated during manufacturing, AI algorithms can identify patterns, anticipate equipment failures, and suggest optimal adjustments to improve process stability and yield. This enables semiconductor manufacturers to operate their lithography tools more efficiently, minimize downtime, and accelerate the development cycle of new chips. The integration of AI also facilitates the continuous learning and adaptation of lithography systems, leading to more robust and precise manufacturing outcomes.

- Enhancement of process control and optimization through AI-driven algorithms.

- Improved defect detection and classification using machine learning for faster analysis.

- Predictive maintenance capabilities for lithography equipment, reducing downtime and increasing tool availability.

- Automated design rule checking and mask synthesis optimization, accelerating design cycles.

- Real-time monitoring and feedback loops for exposure parameters, leading to higher yield and consistency.

- Development of self-correcting lithography systems that adapt to process variations.

- Advanced data analysis for root cause analysis of yield excursions.

Key Takeaways Lithography Machine Market Size & Forecast

User inquiries regarding the key takeaways from the Lithography Machine market size and forecast consistently highlight the critical role of these advanced machines in enabling the ongoing digital transformation. The primary insight is the sustained and robust growth trajectory, fundamentally driven by the escalating global demand for semiconductors. This demand is not merely for more chips but for increasingly sophisticated and powerful chips, which directly translates into a heightened need for cutting-edge lithography solutions capable of producing ever-smaller features. Therefore, the market’s expansion is deeply intertwined with advancements in computational intensity, data processing, and connectivity.

Another crucial takeaway is the disproportionate impact of technological leadership, particularly in Extreme Ultraviolet (EUV) lithography, on market dynamics and competitive landscapes. Companies that master and deploy these highly complex and expensive technologies are positioned at the forefront of innovation, dictating the pace of miniaturization. Furthermore, the forecast underscores the significant investment required for continued R&D and manufacturing capacity expansion, emphasizing that the market's future growth hinges on overcoming technological barriers and managing substantial capital expenditures. Geopolitical factors and supply chain resilience are also emerging as critical considerations shaping investment decisions and market distribution.

- The market exhibits strong growth, propelled by relentless global demand for advanced semiconductors.

- EUV lithography remains a pivotal technology, defining the cutting edge of chip manufacturing capabilities.

- Significant capital expenditure and R&D investment are essential for maintaining technological leadership.

- Miniaturization and increased transistor density are core drivers across all semiconductor applications.

- Geopolitical shifts and supply chain resilience are increasingly influencing regional manufacturing strategies.

- The forecast reflects a sustained need for high-precision, high-throughput lithography systems.

Lithography Machine Market Drivers Analysis

The Lithography Machine market is significantly driven by several intertwined factors, primarily stemming from the exponential growth and continuous innovation within the global semiconductor industry. The insatiable demand for smaller, faster, and more energy-efficient electronic devices, ranging from smartphones and IoT gadgets to high-performance computing and automotive electronics, directly fuels the need for advanced lithography. This pervasive demand necessitates constant advancements in chip design and manufacturing processes, with lithography being the foundational technology for patterning integrated circuits. Furthermore, the rapid expansion of emerging technologies like Artificial Intelligence, 5G, and autonomous vehicles creates new avenues for semiconductor consumption, putting immense pressure on lithography equipment manufacturers to deliver higher precision and throughput.

Government initiatives and strategic investments in semiconductor manufacturing capabilities across various regions also serve as a crucial driver. Nations are increasingly recognizing the strategic importance of a robust domestic semiconductor supply chain for economic security and technological sovereignty. This often translates into substantial subsidies, tax incentives, and funding for research and development, encouraging the establishment of new fabs and the adoption of cutting-edge lithography tools. The competitive landscape among chip manufacturers further intensifies the drive for advanced lithography, as companies strive to gain a technological edge by producing more complex and performant chips at lower costs per transistor.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth of Semiconductor Industry | +2.0% | Global (Asia Pacific, North America, Europe) | 2025-2033 (Long-term) |

| Rising Demand for Advanced Electronic Devices (5G, IoT, AI) | +1.8% | Global | 2025-2030 (Mid-term) |

| Technological Advancements and Miniaturization Trends | +1.5% | Global (esp. Developed Semiconductor Hubs) | 2025-2033 (Ongoing) |

| Government Initiatives and Investments in Local Fabs | +1.2% | USA, EU, China, Japan, South Korea | 2025-2033 (Mid to Long-term) |

| Growth in High-Performance Computing and Data Centers | +1.0% | Global | 2025-2033 (Long-term) |

Lithography Machine Market Restraints Analysis

Despite the robust growth drivers, the Lithography Machine market faces significant restraints that can temper its expansion. One of the primary limiting factors is the exorbitantly high cost associated with research and development, as well as the manufacturing of cutting-edge lithography equipment, particularly EUV systems. These machines are among the most complex and expensive tools ever built, requiring massive capital investment for development and production, which translates into high acquisition costs for chip manufacturers. This elevated entry barrier can restrict the proliferation of advanced lithography technologies to a limited number of top-tier foundries and IDMs, slowing widespread adoption and innovation across the broader semiconductor ecosystem.

Another substantial restraint is the inherent technological complexity and the need for highly specialized expertise to operate and maintain these sophisticated machines. The challenges of pushing the boundaries of physics to achieve ever-finer resolutions involve intricate optical systems, precise environmental controls, and advanced material science, making the manufacturing process extremely delicate and prone to defects. Furthermore, geopolitical tensions and supply chain vulnerabilities, particularly concerning critical components and rare materials, pose significant risks. Disruptions due to trade disputes, export controls, or natural disasters can severely impact the production and delivery of lithography machines, creating uncertainty in the market and potentially delaying capacity expansions for chip fabrication.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Equipment Acquisition | -1.5% | Global | 2025-2033 (Ongoing) |

| Immense R&D Costs and Technological Complexity | -1.0% | Global | 2025-2033 (Ongoing) |

| Skilled Labor Shortage and Talent Gap | -0.8% | Global | 2025-2030 (Mid-term) |

| Geopolitical Tensions and Supply Chain Vulnerabilities | -0.7% | Global (Specific Impact on Key Regions) | 2025-2028 (Short-term) |

| Environmental Regulations and Energy Consumption Concerns | -0.5% | Europe, North America, East Asia | 2028-2033 (Long-term) |

Lithography Machine Market Opportunities Analysis

The Lithography Machine market is ripe with opportunities driven by the continuous evolution of semiconductor technology and the broadening scope of its applications. A significant opportunity lies in the advancement and commercialization of next-generation lithography technologies beyond traditional EUV, such as High-NA EUV, Directed Self-Assembly (DSA), and nanoimprint lithography. These emerging techniques promise to enable further miniaturization and unlock new possibilities for chip design, catering to the demand for even denser and more complex integrated circuits. Investing in and perfecting these future technologies will provide a substantial competitive advantage and open up entirely new market segments for equipment manufacturers.

Furthermore, the diversification of end-use applications for semiconductors presents ample growth opportunities. Beyond traditional consumer electronics and computing, sectors like automotive electronics (for autonomous driving and electric vehicles), healthcare (for medical devices and diagnostics), and industrial automation are rapidly increasing their demand for specialized and robust chips. This creates a need for lithography solutions tailored to different material requirements, feature sizes, and production volumes, moving beyond the singular focus on logic and memory chips. Expansion into these niche but growing markets can provide stable revenue streams and reduce reliance on a few dominant chip manufacturers. Additionally, the growing focus on advanced packaging solutions, which integrate multiple chips into a single package, offers a nascent but promising market for high-precision lithography tools capable of finer interconnections and heterogeneous integration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Lithography (High-NA EUV, DSA) | +2.5% | Global (Leading R&D Hubs) | 2028-2033 (Long-term) |

| Expansion into New End-Use Applications (Automotive, Healthcare, IoT) | +1.8% | Global | 2025-2033 (Mid to Long-term) |

| Increased Adoption of Advanced Packaging Technologies | +1.5% | Asia Pacific, North America | 2025-2030 (Mid-term) |

| Growing Investment in Fab Expansions and New Fabs Globally | +1.2% | USA, Europe, Asia Pacific | 2025-2030 (Mid-term) |

| Demand for Lithography in Non-Silicon Substrates (Compound Semiconductors) | +0.9% | Global | 2028-2033 (Long-term) |

Lithography Machine Market Challenges Impact Analysis

The Lithography Machine market grapples with several formidable challenges that could impede its growth and innovation. Foremost among these is the escalating difficulty and cost associated with achieving ever-smaller feature sizes, often referred to as "Moore's Law scaling challenges." Pushing beyond current technological limits, especially for sub-3nm nodes, requires monumental R&D efforts, new materials, and entirely novel optical or patterning techniques, which significantly inflate development costs and timelines. The complexity of these advanced processes also increases the risk of manufacturing defects, directly impacting yield and overall production efficiency, posing a constant battle for manufacturers.

Another critical challenge is the intense competitive landscape and the need for continuous, rapid innovation. The lithography market is dominated by a few highly specialized players, creating a high barrier to entry for newcomers. Existing players must constantly out-innovate each other, which demands significant investment in R&D without guaranteed returns, especially given the long development cycles for new machine generations. Furthermore, the industry faces persistent intellectual property (IP) protection and security concerns, as proprietary designs and manufacturing processes are highly valuable and susceptible to espionage. Ensuring the security of these critical technologies across a globally dispersed supply chain adds another layer of complexity and risk for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ever-Shrinking Node Sizes and Physics Limitations | -1.8% | Global | 2025-2033 (Ongoing) |

| High Cost of Ownership and Maintenance of EUV Systems | -1.5% | Global | 2025-2033 (Ongoing) |

| Intensifying Competition and R&D Race | -1.0% | Global | 2025-2030 (Mid-term) |

| Supply Chain Disruptions and Component Scarcity | -0.8% | Global | 2025-2028 (Short-term) |

| Intellectual Property Protection and Cybersecurity Threats | -0.7% | Global | 2025-2033 (Ongoing) |

Lithography Machine Market - Updated Report Scope

This comprehensive market research report on the Lithography Machine market provides an in-depth analysis of industry trends, market dynamics, and competitive landscape, offering critical insights for stakeholders. It covers historical data, current market conditions, and future projections, aiming to equip businesses with the intelligence needed to make informed strategic decisions. The report delves into various market segments, regional performance, and profiles of key industry players, providing a holistic view of the market's current state and its potential trajectory over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 30.0 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML, Nikon, Canon, Applied Materials, Tokyo Electron (TEL), Lam Research, KLA Corporation, Screen Holdings, JEOL, Veeco Instruments, Carl Zeiss SMT, EV Group, SUSS MicroTec, ASM Pacific Technology, Hitachi High-Tech, Orbotech (KLA Subsidiary), Nova Measuring Instruments, Onto Innovation, Nextgen Lithography, NIL Technology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lithography Machine market is comprehensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation allows for precise analysis of market trends, growth drivers, and challenges across different technological approaches, application areas, and end-use industries. By breaking down the market into these distinct categories, stakeholders can identify specific opportunities, tailor strategies for particular niches, and gain insights into the performance of various lithography techniques in different manufacturing environments. This detailed analysis is crucial for forecasting future demand and allocating resources effectively in a rapidly evolving technological landscape.

Each segment offers unique insights into the market's structure and future potential. For instance, the "By Type" segmentation highlights the transition from older DUV technologies to cutting-edge EUV, indicating investment patterns and technological shifts. The "By Application" segment showcases how lithography is integral to different types of chip manufacturing, from high-volume memory to complex logic circuits and specialized devices. Similarly, the "By End-Use Industry" segment reveals the broadening adoption of advanced semiconductors across diverse sectors, underscoring the pervasive influence of lithography in modern technology.

- By Type: This segment categorizes lithography machines based on their light source and technology, reflecting varying capabilities and applications.

- EUV Lithography: The most advanced technology, enabling sub-7nm node manufacturing.

- DUV Lithography: Includes ArFi (Argon Fluoride Immersion), ArF Dry (Argon Fluoride Dry), and KrF (Krypton Fluoride) systems, widely used for mature and emerging nodes.

- i-line Lithography: Older technology still relevant for less critical layers and specific applications.

- Nanoimprint Lithography: Emerging technology for high-resolution patterning, particularly for non-traditional applications.

- E-beam Lithography: Used primarily for mask making and specialized, low-volume applications due to high cost and low throughput.

- Others: Includes other experimental or niche lithography techniques.

- By Application: This segmentation focuses on the specific types of semiconductor components manufactured using lithography.

- Memory Manufacturing: Includes DRAM (Dynamic Random-Access Memory) and NAND (Non-Volatile Flash Memory), high-volume production requiring advanced lithography.

- Logic Manufacturing: Encompasses CPUs (Central Processing Units), GPUs (Graphics Processing Units), ASICs (Application-Specific Integrated Circuits), and other complex logic chips, driving demand for leading-edge lithography.

- MEMS Manufacturing: Micro-Electro-Mechanical Systems, requiring specialized patterning for miniature sensors and actuators.

- Power Devices: Semiconductor devices designed for power management, often using less aggressive lithography nodes.

- Optoelectronics: Devices that interact with light, such as LEDs, lasers, and optical sensors.

- Advanced Packaging: Lithography for creating fine interconnections in heterogeneous integration and 3D stacking.

- By End-Use Industry: This segment analyzes the market based on the industries that utilize the final semiconductor products.

- Consumer Electronics: Smartphones, tablets, laptops, gaming consoles, and wearable devices.

- Automotive: Infotainment systems, ADAS (Advanced Driver-Assistance Systems), electric vehicle power electronics.

- Industrial: Automation, robotics, industrial IoT, power management.

- Healthcare: Medical imaging, diagnostic devices, implantable electronics.

- Telecommunications: 5G infrastructure, networking equipment, data transmission.

- Data Centers: Servers, storage, high-performance computing components.

- Others: Aerospace and defense, research institutions, scientific instruments.

Regional Highlights

- Asia Pacific (APAC): The APAC region stands as the undisputed powerhouse of the Lithography Machine market, driven by the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, and China. Countries like Taiwan and South Korea host the world's largest contract foundries and memory manufacturers, which are at the forefront of adopting and investing in advanced lithography technologies, including EUV. China is rapidly expanding its domestic semiconductor production capabilities, fueled by substantial government investments aimed at achieving self-sufficiency in chip manufacturing, thus creating immense demand for lithography equipment. Japan also remains a key player with its strong base in semiconductor equipment manufacturing and materials. This region is expected to continue dominating the market due to its robust manufacturing ecosystem and ongoing capacity expansions.

- North America: North America represents a critical market, particularly for research and development, advanced chip design, and the fabrication of specialized high-performance semiconductors. The region is home to leading chip designers and a growing number of new fabs, especially in the US, driven by strategic initiatives like the CHIPS Act, which aims to reshore and expand semiconductor manufacturing. This surge in domestic production capacity directly translates into increased demand for cutting-edge lithography machines. The emphasis on innovation in AI, quantum computing, and advanced computing also necessitates continuous investment in state-of-the-art lithography tools.

- Europe: Europe holds a significant position in the Lithography Machine market due to the presence of key equipment manufacturers and research institutions that are global leaders in lithography technology. The Netherlands, in particular, is home to the world's dominant EUV lithography system manufacturer. Additionally, several European countries are investing in new foundries and R&D initiatives, often focusing on specialized applications such as automotive semiconductors and power electronics. European collaborative efforts and strong intellectual property in optics and precision engineering continue to drive advancements in lithography.

- Latin America, Middle East, and Africa (LAMEA): While smaller in market share compared to the major regions, LAMEA is an emerging market for semiconductor manufacturing and, consequently, for lithography machines. Investments in digital infrastructure, cloud computing, and smart technologies are gradually increasing the demand for localized chip production or assembly. While not leading in cutting-edge lithography adoption, the region presents opportunities for mature or specialized lithography solutions as various countries seek to develop their nascent semiconductor industries or expand existing assembly and test operations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lithography Machine Market.- ASML

- Nikon

- Canon

- Applied Materials

- Tokyo Electron (TEL)

- Lam Research

- KLA Corporation

- Screen Holdings

- JEOL

- Veeco Instruments

- Carl Zeiss SMT

- EV Group

- SUSS MicroTec

- ASM Pacific Technology

- Hitachi High-Tech

- Orbotech (KLA Subsidiary)

- Nova Measuring Instruments

- Onto Innovation

- Nextgen Lithography

- NIL Technology

Frequently Asked Questions

What is a lithography machine and its primary function?

A lithography machine is a highly complex and precise piece of equipment used in semiconductor manufacturing to create intricate patterns on silicon wafers. Its primary function is to transfer geometric patterns from a photomask onto a light-sensitive material (photoresist) coated on a wafer, forming the foundational layers of integrated circuits. This process is crucial for enabling the miniaturization and high-density integration of electronic components, making it the most critical step in chip fabrication.

How is EUV lithography different from DUV lithography?

EUV (Extreme Ultraviolet) lithography differs from DUV (Deep Ultraviolet) lithography primarily in its wavelength. EUV uses a much shorter wavelength of 13.5 nm, compared to DUV's 193 nm (ArF) or 248 nm (KrF). This shorter wavelength allows EUV machines to pattern significantly smaller features, enabling the production of advanced chips below 7nm nodes. EUV also requires a vacuum environment and reflective optics, unlike DUV which uses refractive lenses.

What factors are driving the growth of the lithography machine market?

The growth of the lithography machine market is primarily driven by the exponential demand for semiconductors across various industries, including consumer electronics, automotive, and data centers. The relentless pursuit of miniaturization and increased computational power in chips, coupled with the expansion of technologies like 5G, AI, and IoT, necessitates continuous investment in advanced lithography tools capable of producing finer features. Additionally, government initiatives to bolster domestic chip manufacturing capabilities contribute significantly to market expansion.

What are the main challenges facing the lithography machine market?

The lithography machine market faces significant challenges including the incredibly high capital expenditure required for developing and acquiring advanced machines like EUV systems, which makes them accessible to only a few leading manufacturers. The extreme technological complexity and the need for highly specialized talent to operate and maintain these systems also pose hurdles. Furthermore, geopolitical tensions affecting global supply chains and the increasing difficulty of further shrinking transistor sizes present ongoing challenges to market growth and innovation.

What role does AI play in the lithography machine industry?

AI plays an increasingly vital role in the lithography machine industry by enhancing process optimization, improving yield, and reducing operational costs. AI algorithms are used for real-time process monitoring, predictive maintenance of complex equipment, and automated defect detection and classification. By analyzing vast datasets, AI helps fine-tune exposure parameters, anticipate potential issues, and optimize throughput, ultimately contributing to more efficient and precise semiconductor manufacturing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted