Lithium Ion Secondary Battery Cathode Material Market

Lithium Ion Secondary Battery Cathode Material Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706889 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

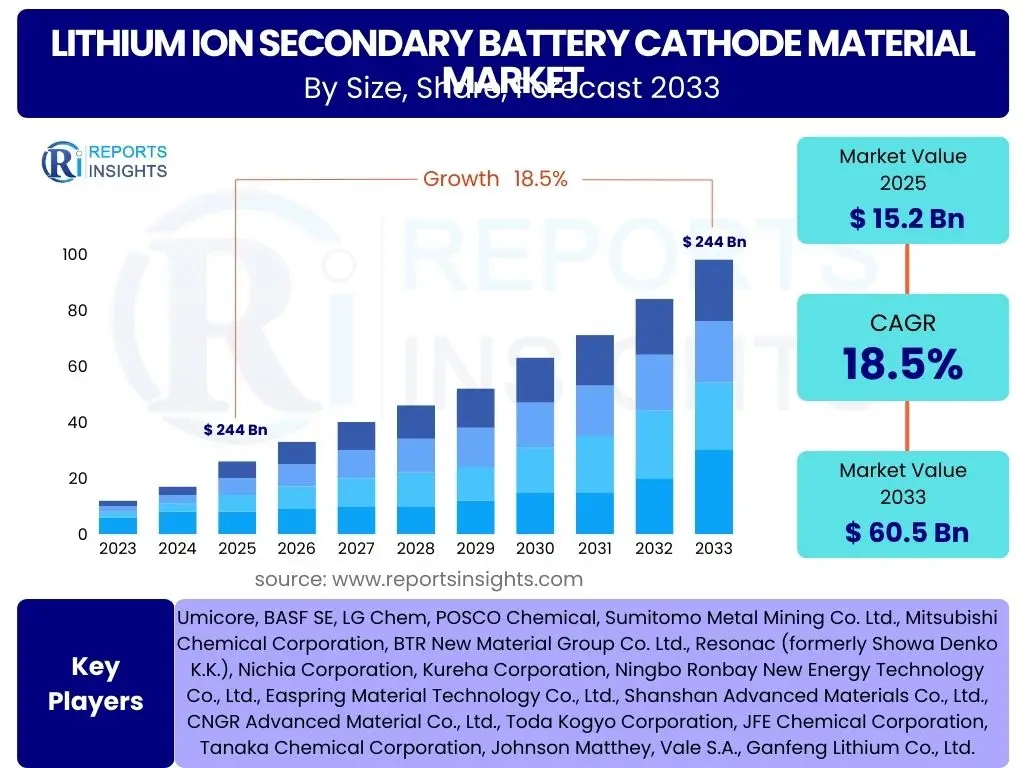

Lithium Ion Secondary Battery Cathode Material Market Size

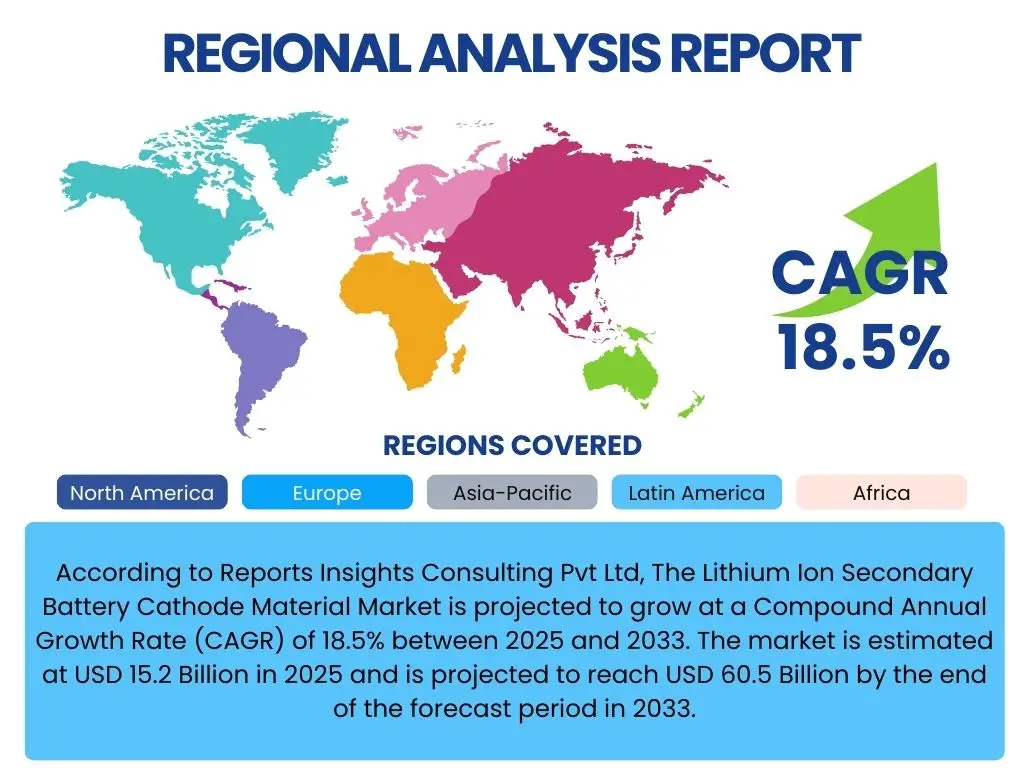

According to Reports Insights Consulting Pvt Ltd, The Lithium Ion Secondary Battery Cathode Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 60.5 Billion by the end of the forecast period in 2033.

Key Lithium Ion Secondary Battery Cathode Material Market Trends & Insights

User inquiries frequently highlight the rapid evolution of battery technology and its profound implications for cathode materials. A significant trend involves the increasing demand for higher energy density and longer cycle life, driven primarily by the automotive sector's shift towards electric vehicles (EVs). This has spurred extensive research and development into advanced cathode chemistries, particularly high-nickel content materials like NMC 811 and NCA, which offer superior performance characteristics essential for EV applications. Concurrently, the market is observing a strong emphasis on supply chain diversification and localization to mitigate geopolitical risks and ensure stable access to critical raw materials such as lithium, cobalt, and nickel.

Another prominent trend centers on sustainability and ethical sourcing. Consumers and regulatory bodies are increasingly demanding environmentally responsible production processes and transparent supply chains, pushing manufacturers to invest in responsible mining practices and innovative recycling technologies for end-of-life batteries. The re-emergence and optimization of lithium iron phosphate (LFP) batteries, especially for entry-level and commercial EVs, represent a notable shift, driven by their enhanced safety, lower cost, and longer lifespan, despite their lower energy density compared to nickel-rich counterparts. This diversification in cathode material adoption reflects a dynamic market responding to varied application requirements and cost pressures.

- Growing adoption of high-nickel cathode materials (NMC 811, NCA) for enhanced energy density in EVs.

- Increased market share for Lithium Iron Phosphate (LFP) due to cost-effectiveness, safety, and longevity, particularly in mainstream EVs and energy storage systems.

- Intensified focus on sustainable sourcing, recycling, and circular economy initiatives for critical raw materials.

- Development of silicon-anode composites and solid-state electrolytes influencing future cathode material requirements.

- Regionalization of supply chains and manufacturing capabilities to reduce dependence on single-source regions.

AI Impact Analysis on Lithium Ion Secondary Battery Cathode Material

User questions regarding the impact of Artificial Intelligence (AI) on the Lithium Ion Secondary Battery Cathode Material market frequently revolve around its potential to accelerate material discovery, optimize manufacturing processes, and enhance battery performance. There is a strong expectation that AI will significantly reduce the time and cost associated with developing new cathode chemistries by enabling high-throughput computational screening of vast material libraries. This predictive capability allows researchers to identify promising candidates with desired properties more efficiently, moving beyond traditional trial-and-error methods. Furthermore, AI's role in simulating material behavior under various conditions can lead to breakthroughs in understanding degradation mechanisms and improving the overall stability and longevity of cathode materials.

Beyond material discovery, AI is anticipated to revolutionize the manufacturing of cathode materials. Users are keen to understand how AI can optimize synthesis parameters, improve quality control, and predict equipment failures, thereby enhancing production efficiency and reducing waste. AI-driven predictive maintenance and real-time process adjustments can ensure consistent product quality and lower operational costs. As the demand for lithium-ion batteries scales exponentially, the ability of AI to streamline production, ensure material uniformity, and manage complex supply chains will be crucial for meeting global requirements and driving down the cost of battery production, ultimately making electric mobility and renewable energy storage more accessible.

- Acceleration of novel cathode material discovery through AI-driven computational screening and simulation.

- Optimization of manufacturing processes for improved efficiency, yield, and quality control.

- Predictive analytics for material performance, degradation, and lifecycle management.

- Enhanced supply chain management and raw material sourcing through AI-powered logistics and forecasting.

- Development of smarter battery management systems (BMS) that interact optimally with advanced cathode materials.

Key Takeaways Lithium Ion Secondary Battery Cathode Material Market Size & Forecast

Common user inquiries about the market's key takeaways reveal a primary focus on growth drivers, technological shifts, and the long-term sustainability of the industry. The most significant insight is the market's robust growth trajectory, primarily fueled by the accelerating global transition to electric vehicles and the increasing deployment of renewable energy storage solutions. This demand surge necessitates continuous innovation in cathode materials to meet evolving performance requirements, such as higher energy density, faster charging capabilities, and improved safety profiles, while simultaneously addressing cost efficiency and environmental concerns. The forecast indicates sustained expansion, emphasizing the critical role of cathode materials as the heart of advanced battery technology.

Another crucial takeaway is the strategic importance of supply chain resilience and diversification. Geopolitical factors and volatility in raw material prices underscore the need for manufacturers to secure stable and ethical sourcing channels for lithium, nickel, cobalt, and manganese. The rise of region-specific manufacturing hubs and increased investment in domestic production capacities reflect efforts to mitigate supply risks and foster greater self-sufficiency. Furthermore, the market is poised for significant shifts in material chemistries, with a dynamic interplay between established high-nickel NMC/NCA, cost-effective LFP, and emerging solid-state or cobalt-free alternatives, each addressing specific market niches and performance benchmarks.

- Market growth primarily driven by electric vehicle proliferation and grid-scale energy storage.

- Significant investments in R&D for advanced cathode chemistries promising higher energy density and improved safety.

- Increasing strategic focus on diversified and localized supply chains for critical raw materials.

- Balancing acts between performance (high-nickel), cost (LFP), and sustainability (recycling, ethical sourcing).

- Long-term market stability hinges on technological innovation, sustainable practices, and resilient supply networks.

Lithium Ion Secondary Battery Cathode Material Market Drivers Analysis

The Lithium Ion Secondary Battery Cathode Material market is experiencing robust growth, primarily propelled by the burgeoning demand for electric vehicles (EVs) worldwide. Governments globally are implementing stringent emission regulations and offering significant incentives for EV adoption, directly stimulating the need for high-performance and cost-effective battery solutions. Concurrently, the increasing deployment of renewable energy sources such as solar and wind power necessitates advanced energy storage systems to ensure grid stability and reliability. This fundamental shift towards electrification in transportation and energy sectors underpins the sustained expansion of the cathode material market, as these materials are the core components determining battery performance.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth in Electric Vehicle (EV) Production & Sales | +5.0-6.5% | Global, particularly China, Europe, North America | 2025-2033 (Mid to Long-term) |

| Increasing Deployment of Grid-Scale Energy Storage Systems | +3.0-4.0% | North America, Europe, Asia Pacific (China, India, Australia) | 2025-2033 (Mid to Long-term) |

| Technological Advancements in Cathode Material Chemistries | +2.5-3.5% | Global R&D Hubs (Japan, South Korea, USA, Germany) | 2025-2033 (Continuous) |

| Supportive Government Policies & Subsidies for E-mobility | +2.0-3.0% | Europe, North America, China, India | 2025-2030 (Short to Mid-term) |

| Expanding Applications in Consumer Electronics & Portable Devices | +1.5-2.0% | Asia Pacific (China, South Korea, Japan), North America | 2025-2033 (Stable Growth) |

Lithium Ion Secondary Battery Cathode Material Market Restraints Analysis

Despite significant growth prospects, the Lithium Ion Secondary Battery Cathode Material market faces notable restraints that could temper its expansion. One primary concern is the volatility and scarcity of raw materials essential for cathode production, such as lithium, cobalt, and nickel. Price fluctuations and supply chain concentration, particularly for cobalt mining, pose significant challenges to manufacturers in maintaining stable production costs and ensuring consistent supply. This dependence on limited geographical sources for critical minerals introduces geopolitical risks and can lead to cost inflation, impacting the overall profitability and competitiveness of the battery industry.

Furthermore, inherent safety concerns associated with lithium-ion batteries, including the risk of thermal runaway and fire, continue to be a restraint, particularly for high-energy density applications. While advancements in battery management systems and cell design have mitigated these risks to a degree, public perception and regulatory scrutiny remain high. Environmental regulations regarding mining practices and waste disposal for battery components also present hurdles, requiring significant investment in sustainable practices and recycling infrastructure, which can add to the operational costs for cathode material producers. These factors collectively contribute to a complex operational environment that must be navigated for sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (Lithium, Cobalt, Nickel) | -2.0-3.0% | Global | 2025-2033 (Continuous) |

| Supply Chain Concentration & Geopolitical Risks for Key Minerals | -1.5-2.5% | Global, especially Congo (Cobalt), South America (Lithium) | 2025-2033 (Long-term structural issue) |

| Safety Concerns (Thermal Runaway, Fire Risks) | -1.0-1.8% | Global (Consumer confidence & regulatory bodies) | 2025-2030 (Mid-term, as tech evolves) |

| Environmental Regulations & Waste Management Challenges | -0.8-1.5% | Europe, North America, China | 2025-2033 (Increasingly strict) |

| High Capital Expenditure for Production Facility Setup | -0.5-1.0% | Global (New entrants, expansion) | 2025-2030 (Short to Mid-term for investment) |

Lithium Ion Secondary Battery Cathode Material Market Opportunities Analysis

Significant opportunities are emerging in the Lithium Ion Secondary Battery Cathode Material market, particularly driven by advancements in battery chemistry and the expanding scope of battery applications. The push towards developing solid-state batteries presents a transformative opportunity, as these batteries promise enhanced safety, higher energy density, and faster charging capabilities, potentially necessitating new cathode material formulations or optimizing existing ones for solid electrolytes. Similarly, the growing focus on cobalt-free or low-cobalt cathode materials, such as high-manganese or lithium-rich chemistries, offers a strategic avenue to mitigate reliance on ethically sensitive and volatile cobalt supplies, addressing both cost and sustainability concerns.

Another crucial opportunity lies in the development and scaling of battery recycling technologies. As millions of batteries reach their end-of-life, the efficient recovery of valuable cathode materials will establish a circular economy, reducing dependence on virgin raw materials and enhancing environmental sustainability. Furthermore, the diversification of lithium-ion battery applications beyond EVs and consumer electronics into areas like electric aviation, marine vessels, and heavy-duty industrial machinery opens new, high-growth market segments for specialized cathode materials. Regional initiatives to establish localized battery production and supply chains also present opportunities for domestic material manufacturers to capture significant market share and reduce logistical complexities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Solid-State Batteries & Advanced Chemistries | +3.5-4.5% | Global R&D Hubs, particularly Japan, USA, Germany | 2028-2033 (Mid to Long-term) |

| Growth in Battery Recycling & Circular Economy Initiatives | +2.8-3.8% | Europe, North America, Asia Pacific | 2025-2033 (Increasingly significant) |

| Expansion into New Application Areas (E-aviation, Marine, Heavy Industry) | +2.0-3.0% | Global (Niche markets developing) | 2027-2033 (Emerging) |

| Focus on Cobalt-Free or Low-Cobalt Cathode Materials | +1.5-2.5% | Global (All regions seeking alternatives) | 2025-2030 (Short to Mid-term) |

| Establishment of Regional Battery Production Hubs | +1.0-2.0% | Europe, North America, India, Southeast Asia | 2025-2033 (Strategic localization) |

Lithium Ion Secondary Battery Cathode Material Market Challenges Impact Analysis

The Lithium Ion Secondary Battery Cathode Material market faces several critical challenges that demand strategic responses from industry participants. One significant hurdle is the intense competition and price pressure from various established and emerging manufacturers. As battery production scales, the drive to reduce costs permeates the entire supply chain, putting considerable pressure on cathode material producers to lower per-unit costs without compromising performance or quality. This competitive landscape necessitates continuous innovation in manufacturing efficiency and material formulations to maintain market relevance and profitability.

Moreover, the industry grapples with the complexities of scaling up production of advanced cathode materials while maintaining stringent quality and consistency standards. Ensuring uniform material properties across large batches is crucial for battery performance and safety, yet it presents technical difficulties, particularly for novel chemistries. Additionally, intellectual property rights and patent disputes surrounding innovative material compositions and manufacturing processes pose significant legal and financial risks, potentially hindering market entry for new players or slowing down technological dissemination. Addressing these challenges requires substantial investment in R&D, robust quality assurance, and navigating a complex regulatory and intellectual property landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition & Cost Reduction Pressure | -2.0-3.0% | Global | 2025-2033 (Continuous) |

| Scaling Production of Advanced Cathode Materials | -1.5-2.5% | Global (Especially new production facilities) | 2025-2030 (Short to Mid-term) |

| Intellectual Property Rights & Patent Disputes | -1.0-1.8% | Global (Major R&D regions) | 2025-2033 (Ongoing) |

| Maintaining Quality & Consistency Across Large-Scale Production | -0.8-1.5% | Global (All manufacturers) | 2025-2033 (Operational) |

| Talent Shortage in Battery Material Science & Engineering | -0.5-1.0% | North America, Europe, parts of Asia | 2025-2030 (Mid-term) |

Lithium Ion Secondary Battery Cathode Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Lithium Ion Secondary Battery Cathode Material Market, offering a detailed assessment of its current status, historical performance, and future growth projections. The scope includes an examination of market size, trends, drivers, restraints, opportunities, and challenges influencing industry dynamics. The report segments the market by material type, application, and end-use industry, providing granular insights into each category. Furthermore, it delivers a thorough regional analysis, highlighting key market developments and competitive landscapes across major geographical regions, making it an essential resource for stakeholders seeking strategic market intelligence and investment opportunities within the battery materials ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 60.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Umicore, BASF SE, LG Chem, POSCO Chemical, Sumitomo Metal Mining Co. Ltd., Mitsubishi Chemical Corporation, BTR New Material Group Co. Ltd., Resonac (formerly Showa Denko K.K.), Nichia Corporation, Kureha Corporation, Ningbo Ronbay New Energy Technology Co., Ltd., Easpring Material Technology Co., Ltd., Shanshan Advanced Materials Co., Ltd., CNGR Advanced Material Co., Ltd., Toda Kogyo Corporation, JFE Chemical Corporation, Tanaka Chemical Corporation, Johnson Matthey, Vale S.A., Ganfeng Lithium Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lithium Ion Secondary Battery Cathode Material market is comprehensively segmented to provide detailed insights into its various facets, enabling a granular understanding of market dynamics and opportunities across different material types, applications, and end-use industries. This segmentation highlights the diverse demands placed on cathode materials, ranging from high-performance requirements in electric vehicles to cost-efficiency in grid-scale energy storage, and compact power needs in consumer electronics. Analyzing these segments reveals shifting preferences, technological advancements, and the competitive landscape for specific material chemistries.

By dissecting the market based on these critical parameters, stakeholders can identify niche markets, understand demand patterns, and tailor their product development strategies to meet specific industry needs. For instance, the demand for high-nickel NMC is strongly correlated with EV growth, while LFP materials are gaining traction in cost-sensitive applications. This structured approach to segmentation provides a clear framework for assessing market attractiveness, identifying growth pockets, and formulating effective market penetration and expansion strategies for cathode material manufacturers and suppliers.

- By Material Type:

- Lithium Nickel Manganese Cobalt Oxide (NMC)

- Lithium Cobalt Oxide (LCO)

- Lithium Iron Phosphate (LFP)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Lithium Manganese Oxide (LMO)

- Other advanced chemistries (e.g., lithium-rich, cobalt-free variations)

- By Application:

- Electric Vehicles (EVs) including BEVs, PHEVs, and HEVs

- Consumer Electronics (smartphones, laptops, wearables, power tools)

- Energy Storage Systems (ESS) encompassing grid-scale, residential, and commercial storage

- Industrial & Other Applications (e-bikes, drones, medical devices, robotics)

- By End-Use Industry:

- Automotive (passenger and commercial EVs)

- Consumer Goods (portable electronic devices)

- Energy & Power (grid stabilization, renewable energy integration)

- Industrial (heavy machinery, forklifts, specialized equipment)

- Aerospace & Defense (drones, specialized vehicles)

Regional Highlights

The global Lithium Ion Secondary Battery Cathode Material market exhibits significant regional disparities in terms of production, consumption, and technological leadership, primarily influenced by local government policies, raw material accessibility, and the maturity of electric vehicle and energy storage markets. Asia Pacific currently dominates the market, largely due to the presence of major battery manufacturers and cathode material producers in countries like China, South Korea, and Japan. China, in particular, leads in both production capacity and domestic demand, driven by its expansive EV market and substantial investments in battery manufacturing. South Korea and Japan continue to be critical hubs for advanced cathode material R&D and high-quality production, supplying leading battery cell manufacturers globally.

Europe and North America are rapidly increasing their market share through aggressive investments in localized battery supply chains and gigafactories. Government incentives, such as the European Green Deal and the Inflation Reduction Act (IRA) in the United States, are fostering domestic production capabilities for cathode materials to reduce reliance on Asian suppliers and enhance energy independence. These regions are witnessing a surge in new plant constructions and strategic partnerships aimed at securing raw material supplies and establishing integrated battery ecosystems. Latin America and the Middle East & Africa, while currently smaller markets, hold significant potential due to their abundant reserves of critical raw materials like lithium and cobalt, positioning them as future key players in the raw material supply chain for cathode materials.

- Asia Pacific: Dominant market share driven by robust EV production and strong battery manufacturing bases in China, South Korea, and Japan. China leads in both demand and supply of various cathode types, especially LFP and high-nickel NMC.

- Europe: Rapidly growing market with significant investments in gigafactories and localized supply chains, propelled by stringent emission regulations and strong government support for electric mobility and energy storage. Germany, France, and Nordic countries are key players.

- North America: Experiencing substantial growth due to the Inflation Reduction Act (IRA) and increasing EV adoption, leading to new cathode material production facilities and raw material processing investments, primarily in the United States and Canada.

- Latin America: Emerging region with significant lithium reserves (Chile, Argentina, Bolivia), positioned to become a crucial supplier of raw materials for global cathode material production.

- Middle East & Africa (MEA): Key region for cobalt and other critical minerals (e.g., nickel in Indonesia, Australia which are often included in broader APAC discussions but have distinct mining landscapes), attracting investments in raw material extraction and processing for the global battery supply chain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lithium Ion Secondary Battery Cathode Material Market.- Umicore

- BASF SE

- LG Chem

- POSCO Chemical

- Sumitomo Metal Mining Co. Ltd.

- Mitsubishi Chemical Corporation

- BTR New Material Group Co. Ltd.

- Resonac (formerly Showa Denko K.K.)

- Nichia Corporation

- Kureha Corporation

- Ningbo Ronbay New Energy Technology Co., Ltd.

- Easpring Material Technology Co., Ltd.

- Shanshan Advanced Materials Co., Ltd.

- CNGR Advanced Material Co., Ltd.

- Toda Kogyo Corporation

- JFE Chemical Corporation

- Tanaka Chemical Corporation

- Johnson Matthey

- Vale S.A.

- Ganfeng Lithium Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Lithium Ion Secondary Battery Cathode Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a lithium ion secondary battery cathode material?

A lithium ion secondary battery cathode material is a key component within a rechargeable lithium-ion battery. It is the positive electrode material that determines the battery's energy density, power capability, and safety characteristics. Common types include NMC, LFP, LCO, and NCA, each offering different performance profiles for various applications.

Which cathode material chemistry is currently most widely used?

While high-nickel Lithium Nickel Manganese Cobalt Oxide (NMC) and Lithium Iron Phosphate (LFP) are currently the most widely used cathode chemistries. NMC is favored for its high energy density in electric vehicles and premium consumer electronics, while LFP is gaining significant traction due to its lower cost, superior safety, and longer cycle life, especially in mainstream EVs and energy storage systems.

What are the primary drivers for the growth of this market?

The market's growth is primarily driven by the surging global demand for electric vehicles (EVs) and the increasing deployment of renewable energy storage systems. Supportive government policies, technological advancements leading to higher energy density materials, and expanding applications in consumer electronics further propel market expansion.

What challenges does the Lithium Ion Secondary Battery Cathode Material market face?

Key challenges include the volatile prices and concentrated supply chains of critical raw materials like lithium, cobalt, and nickel. Other significant challenges are intense price competition among manufacturers, the complexities of scaling up production while maintaining quality, and navigating stringent environmental regulations for material sourcing and waste disposal.

How is AI impacting the development of new cathode materials?

Artificial Intelligence (AI) is transforming cathode material development by accelerating the discovery of novel chemistries through computational screening and simulation. AI also optimizes manufacturing processes for improved efficiency and quality control, and enhances supply chain management, thereby reducing development cycles and production costs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted