Liquid Metal Battery Market

Liquid Metal Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708456 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

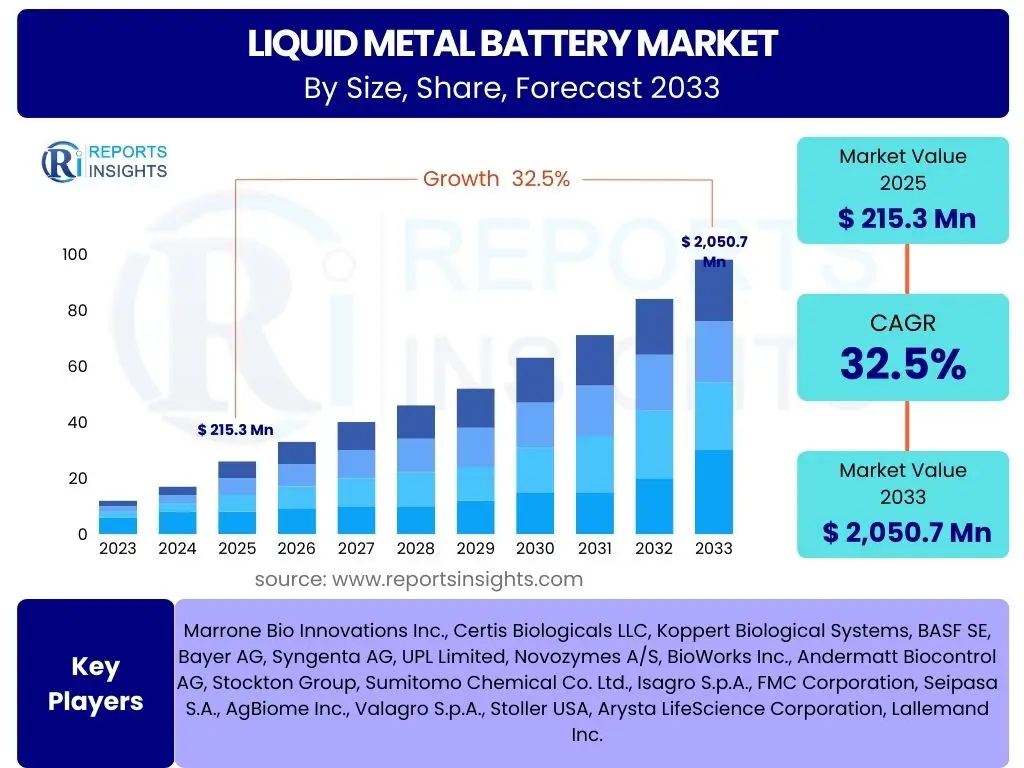

Liquid Metal Battery Market Size

According to Reports Insights Consulting Pvt Ltd, The Liquid Metal Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 32.5% between 2025 and 2033. The market is estimated at USD 215.3 Million in 2025 and is projected to reach USD 2,050.7 Million by the end of the forecast period in 2033.

Key Liquid Metal Battery Market Trends & Insights

The Liquid Metal Battery market is witnessing significant advancements driven by the escalating global demand for efficient, long-duration energy storage solutions. A primary trend is the intensified focus on grid-scale applications, where these batteries can address the intermittency of renewable energy sources such as solar and wind. This shift necessitates battery technologies capable of reliably storing and dispatching large amounts of energy over extended periods, a niche perfectly suited for liquid metal batteries due to their inherent scalability and robust operational characteristics. Consequently, research and development efforts are increasingly geared towards optimizing performance for these demanding grid environments.

Another crucial insight lies in the continuous pursuit of cost reduction and enhanced material science. Developers are exploring more abundant and less expensive raw materials, alongside innovative cell designs and manufacturing processes, to lower the overall capital expenditure and operational costs. This focus on economic viability is paramount for widespread commercial adoption. Furthermore, the modular design capabilities of liquid metal battery systems are emerging as a key trend, allowing for flexible deployment and scalability across various project sizes, from utility-scale plants to smaller industrial applications. This adaptability, combined with an emphasis on improved safety features and environmental sustainability, positions liquid metal batteries as a leading contender in the future energy storage landscape.

- Accelerated adoption in grid-scale energy storage projects.

- Increased focus on long-duration energy storage capabilities.

- Advancements in material science for cost reduction and efficiency.

- Development of modular and scalable battery system designs.

- Emphasis on enhancing safety profiles and environmental sustainability.

AI Impact Analysis on Liquid Metal Battery

Artificial Intelligence (AI) is poised to revolutionize the development and deployment of Liquid Metal Batteries (LMBs) by significantly accelerating material discovery and optimizing manufacturing processes. Users frequently inquire about how AI can enhance the performance and reduce the cost of LMBs. Machine learning algorithms, for instance, can analyze vast datasets from experimental designs, identifying optimal electrode and electrolyte compositions with unprecedented speed and precision, thereby drastically reducing research and development cycles. This intelligent approach allows for the rapid exploration of novel chemistries and structural designs, bringing more efficient and robust battery technologies to market faster than traditional trial-and-error methods.

Furthermore, AI can dramatically enhance the operational efficiency, predictive maintenance, and overall lifespan of deployed LMB systems. Common user concerns include the reliability and longevity of these high-temperature batteries. By continuously monitoring real-time performance data, AI models can detect subtle anomalies, predict potential failures before they occur, and dynamically optimize charging and discharging cycles to maximize battery health and extend operational life. This intelligent management contributes to lower operational costs, increased reliability, and more efficient integration into smart grids, making LMBs a more attractive and viable option for large-scale energy storage applications. The ability of AI to learn from operational data also supports continuous improvement in battery management strategies, further solidifying the technology's long-term potential.

- Accelerated discovery of novel and efficient battery materials.

- Optimization of manufacturing processes for improved consistency and reduced costs.

- Enhanced predictive maintenance and fault detection in operational systems.

- Intelligent management of charge/discharge cycles to extend battery lifespan.

- Improved energy management and seamless integration into smart grid infrastructures.

Key Takeaways Liquid Metal Battery Market Size & Forecast

The Liquid Metal Battery market is entering a pivotal growth phase, with its substantial projected Compound Annual Growth Rate (CAGR) underscoring its critical role in the global energy transition. User inquiries often highlight the importance of understanding the market's underlying growth drivers and future potential. This robust expansion is primarily fueled by the escalating demand for reliable, long-duration energy storage solutions necessary to support the increasing integration of intermittent renewable energy sources into national grids. The unique properties of liquid metal batteries, such as their scalability, long cycle life, and inherent safety, position them as an ideal candidate to address these modern energy challenges, offering grid stability and enhanced energy security.

A key takeaway from the market forecast is the strong correlation between technological maturation, cost reduction efforts, and widespread commercial viability. The market's trajectory indicates that ongoing research and development, coupled with strategic investments in manufacturing and deployment infrastructure, will significantly lower the barriers to adoption. This includes advancements in materials science to utilize more abundant and less expensive elements, as well as innovations in system design to reduce installation and operational costs. The market's projected growth signifies increasing confidence from investors, utilities, and governments in the long-term potential of liquid metal battery technology to deliver a sustainable and resilient energy future.

- The market is on a robust growth trajectory, driven by the global energy transition.

- Liquid Metal Batteries are crucial for integrating intermittent renewable energy sources.

- Long-duration energy storage requirements are the primary market accelerator.

- Technological advancements and cost reductions are enhancing commercial viability.

- Significant investment and policy support underpin future market expansion.

Liquid Metal Battery Market Drivers Analysis

The primary driver for the Liquid Metal Battery market is the escalating global demand for long-duration energy storage solutions. As renewable energy sources like solar and wind become more prevalent, the need for reliable, grid-scale storage to manage intermittency and ensure a stable power supply grows exponentially. Liquid metal batteries, with their inherent ability to store large amounts of energy for extended periods (typically 4-12 hours or more), are uniquely positioned to meet this demand, providing crucial support for grid stability and reliability when renewable generation fluctuates or during peak demand.

Furthermore, grid modernization initiatives and the pursuit of energy independence and security are compelling factors. Many regions are investing heavily in upgrading their electricity grids to integrate more diverse energy sources and improve resilience against outages. Liquid metal batteries offer a robust solution for balancing supply and demand, providing ancillary services such as frequency regulation and voltage support, and creating more flexible and robust energy systems. This reduces reliance on fossil fuels for grid balancing and enhances national energy security by diversifying storage technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Long-Duration Energy Storage | +1.8% | Global | Mid-Long Term |

| Integration of Renewable Energy Sources (Solar, Wind) | +1.5% | Europe, North America, APAC | Short-Mid Term |

| Grid Modernization and Infrastructure Development | +1.2% | North America, Europe, China | Mid Term |

| Growing Need for Energy Security and Reliability | +0.9% | Global, especially Geopolitically Sensitive Regions | Long Term |

| Favorable Government Policies and Incentives for Storage | +0.7% | US, Germany, Australia, India | Short-Mid Term |

Liquid Metal Battery Market Restraints Analysis

Despite their promising potential, the Liquid Metal Battery market faces several significant restraints, notably the high upfront capital expenditure associated with initial deployment. While operational costs can be competitive due to long cycle life and durable components, the initial investment required for establishing large-scale LMB installations can be substantial. This high CAPEX often poses a barrier to widespread adoption, particularly for nascent projects or regions with limited access to capital, making it challenging for LMBs to compete purely on cost with more established, albeit less suitable for long-duration, storage technologies.

Another critical restraint involves the perceived technological immaturity and the supply chain complexities of some key materials. Although significant advancements have been made, some liquid metal battery chemistries are still considered nascent compared to widely deployed lithium-ion batteries. This perception can lead to a cautious approach from investors and utilities. Additionally, ensuring a stable and cost-effective supply of specific metals and high-purity materials required for electrodes and electrolytes can present logistical and economic challenges. Volatility in raw material prices and the need for specialized processing facilities can impact scalability, increase manufacturing costs, and potentially slow down market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Expenditure (CAPEX) | -1.3% | Global | Short-Mid Term |

| Perceived Technological Immaturity/Lack of Large-Scale Track Record | -1.0% | Global | Mid Term |

| Supply Chain Volatility and Material Costs | -0.8% | Global, especially regions dependent on specific imports | Short-Mid Term |

| High Operating Temperatures and Thermal Management Complexity | -0.5% | Global | Short Term |

| Competition from Established Battery Technologies (e.g., Li-ion) | -0.7% | Global | Mid Term |

Liquid Metal Battery Market Opportunities Analysis

The Liquid Metal Battery market is ripe with opportunities, particularly in emerging markets where energy infrastructure is rapidly developing and renewable energy adoption is accelerating. These regions often lack extensive legacy grid systems, making them ideal candidates for integrating cutting-edge storage technologies that can leapfrog traditional energy solutions. The demand for reliable, off-grid, and microgrid solutions in remote areas, particularly in developing economies, also presents a substantial growth avenue, as LMBs can provide stable power independent of centralized grids, fostering economic growth and improving quality of life.

Moreover, continuous advancements in materials science and battery chemistry offer significant opportunities for innovation. Research into new electrode materials that are more abundant and less toxic, more efficient and stable electrolytes, and novel cell designs can lead to batteries with enhanced performance, lower costs, and improved safety profiles. Strategic partnerships between research institutions, material suppliers, and energy companies can accelerate the commercialization of these innovations, unlocking new applications beyond grid storage, such as niche industrial processes requiring specific power profiles. Furthermore, the growing focus on circular economy principles and sustainable manufacturing practices provides an opportunity for LMB developers to design systems with high recyclability and minimal environmental impact, gaining a competitive edge.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets and Developing Economies | +1.6% | Africa, Southeast Asia, Latin America | Mid-Long Term |

| Further Advancements in Materials Science and Battery Chemistry | +1.4% | Global (R&D Hubs) | Mid Term |

| Development of Niche Industrial and Commercial Applications | +1.1% | North America, Europe, East Asia | Mid Term |

| Strategic Partnerships and Collaborations Across the Value Chain | +0.9% | Global | Short-Mid Term |

| Focus on Circular Economy and Sustainable Manufacturing | +0.6% | Europe, North America | Long Term |

Liquid Metal Battery Market Challenges Impact Analysis

The Liquid Metal Battery market confronts significant challenges related to scaling manufacturing processes to meet anticipated demand. Transitioning from laboratory-scale prototypes and pilot projects to mass production requires substantial investment in infrastructure, process optimization, and stringent quality control. Ensuring consistent performance, reliability, and safety across millions of individual battery cells, particularly when dealing with high-temperature molten materials and complex electrochemical interactions, poses intricate engineering and logistical hurdles. These scaling complexities can impact production timelines and increase initial manufacturing costs, potentially slowing market penetration.

Additionally, long-term performance validation and public perception represent crucial challenges. Demonstrating the sustained efficiency, safety, and durability of liquid metal batteries over decades of continuous operation is essential for gaining widespread industry trust, securing significant investment, and achieving regulatory approval. Addressing potential safety concerns associated with high-temperature operation and the handling of molten materials through robust design, rigorous testing, and transparent communication is paramount. Overcoming market skepticism and fostering public confidence, especially in comparison to more commonly understood battery technologies, will require comprehensive data, successful demonstration projects, and clear articulation of the technology's benefits and safety features.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scaling Manufacturing and Production to Commercial Levels | -1.5% | Global | Short-Mid Term |

| Ensuring Long-Term Performance and Reliability Validation | -1.2% | Global | Mid Term |

| Addressing Safety Concerns and Public Perception | -1.0% | Global | Short-Mid Term |

| Navigating Complex Regulatory and Permitting Frameworks | -0.7% | Specific Countries/Regions | Mid Term |

| Attracting Sufficient Investment for R&D and Deployment | -0.9% | Global | Short-Mid Term |

Liquid Metal Battery Market - Updated Report Scope

This comprehensive market insights report meticulously analyzes the Liquid Metal Battery sector, providing an in-depth assessment of market dynamics, growth trajectories, and competitive landscapes. It offers a detailed breakdown of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographic regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making, enabling them to navigate the evolving market, identify key investment areas, and capitalize on emerging opportunities within the energy storage ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 215.3 Million |

| Market Forecast in 2033 | USD 2,050.7 Million |

| Growth Rate | 32.5% |

| Number of Pages | 256 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ambri Inc., Form Energy Inc., ESS Inc., Sumitomo Electric Industries, Ltd., Fluence Energy, Inc., Aceleron Ltd., EOS Energy Storage LLC, Primus Power, SimpliPhi Power, Inc., Storion Energy, Redflow Limited, Aquion Energy (acquired by SimpliPhi Power), Urban Electric Power, Enel Green Power, Vionx Energy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Liquid Metal Battery market is comprehensively segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for targeted analysis of specific product types, technological approaches, and end-use sectors, enabling a detailed examination of market drivers and inhibitors within each sub-segment. Such a structured approach facilitates a clearer view of market potential and competitive dynamics across the entire value chain, from material science innovations to deployment in various energy landscapes.

- By Type: Sodium-Antimony Battery, Zinc-Antimony Battery, Magnesium-Antimony Battery, Lead-Antimony Battery, Others.

- By Application: Grid-scale Energy Storage, Renewable Energy Integration, Industrial Backup Power, Commercial Energy Storage, Remote/Off-Grid Solutions.

- By End-Use: Utilities, Independent Power Producers, Commercial & Industrial Enterprises, Data Centers, Telecommunications.

Regional Highlights

- North America: This region is a major hub for Liquid Metal Battery research and development, driven by significant government funding for grid modernization and renewable energy initiatives. The U.S. and Canada are actively investing in long-duration storage to enhance grid resilience and integrate variable renewable output, making them key markets for early adoption and technological innovation.

- Europe: Driven by ambitious climate targets and high renewable energy penetration, Europe is a crucial market. Countries like Germany and the UK are prioritizing energy storage solutions to balance their grids and reduce carbon emissions, leading to substantial investments in pilot projects and commercial deployments of advanced battery technologies.

- Asia Pacific (APAC): APAC represents a rapidly expanding market due to surging energy demand, rapid industrialization, and significant investments in renewable energy infrastructure, particularly in China, India, and Australia. These countries offer immense potential for large-scale energy storage solutions to support economic growth and address energy security concerns.

- Latin America: This region presents emerging opportunities, especially with its abundant renewable energy resources (hydro, solar, wind) and the need for improved grid reliability and access in remote areas. Development of microgrids and off-grid solutions is expected to drive demand for robust storage technologies like LMBs.

- Middle East and Africa (MEA): The MEA region is increasingly focusing on diversifying its energy mix away from fossil fuels, with significant solar energy potential. Investments in utility-scale renewable projects and a growing need for energy access in underserved areas are creating a fertile ground for long-duration energy storage solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Liquid Metal Battery Market.- Ambri Inc.

- Form Energy Inc.

- ESS Inc.

- Sumitomo Electric Industries, Ltd.

- Fluence Energy, Inc.

- Aceleron Ltd.

- EOS Energy Storage LLC

- Primus Power

- SimpliPhi Power, Inc.

- Storion Energy

- Redflow Limited

- Aquion Energy

- Urban Electric Power

- Enel Green Power

- Vionx Energy

- Hydrostor Inc.

- SaltX Technology Holding AB

- Invinity Energy Systems plc

- Advanced Energy Materials LLC

- Battery Energy Power Solutions Pty Ltd

Frequently Asked Questions

What is a liquid metal battery?

A liquid metal battery is an electrochemical energy storage device that uses molten salt electrolytes and two different molten metals as electrodes. These batteries typically operate at elevated temperatures to maintain the liquid state of their components, allowing for unique performance characteristics.

How do liquid metal batteries work?

Liquid metal batteries function by exploiting the density differences between the molten electrodes and the molten salt electrolyte. During discharge, ions move from one liquid metal electrode through the electrolyte to the other, creating an electric current, while charge reversal occurs during the charging process. This mechanism allows for high current density and long cycle life.

What are the primary advantages of liquid metal batteries?

Key advantages include long cycle life, high current density, fast charge and discharge rates, the use of non-flammable molten salt components, and inherent scalability for large-scale, grid-level storage applications. They are also designed using earth-abundant materials, contributing to sustainability.

Where are liquid metal batteries primarily used?

Liquid metal batteries are predominantly designed for large-scale, long-duration energy storage applications. This includes integrating intermittent renewable energy sources into the electrical grid, providing grid stabilization and ancillary services, and supporting industrial processes that require reliable, sustained power.

What are the main challenges facing liquid metal battery adoption?

Challenges include the high operating temperatures requiring robust thermal management systems, the significant upfront capital costs associated with large-scale deployment, and the ongoing need for further technological maturation and long-term performance validation to achieve widespread commercial acceptance and trust.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted