Liquid Lense Market

Liquid Lense Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709939 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

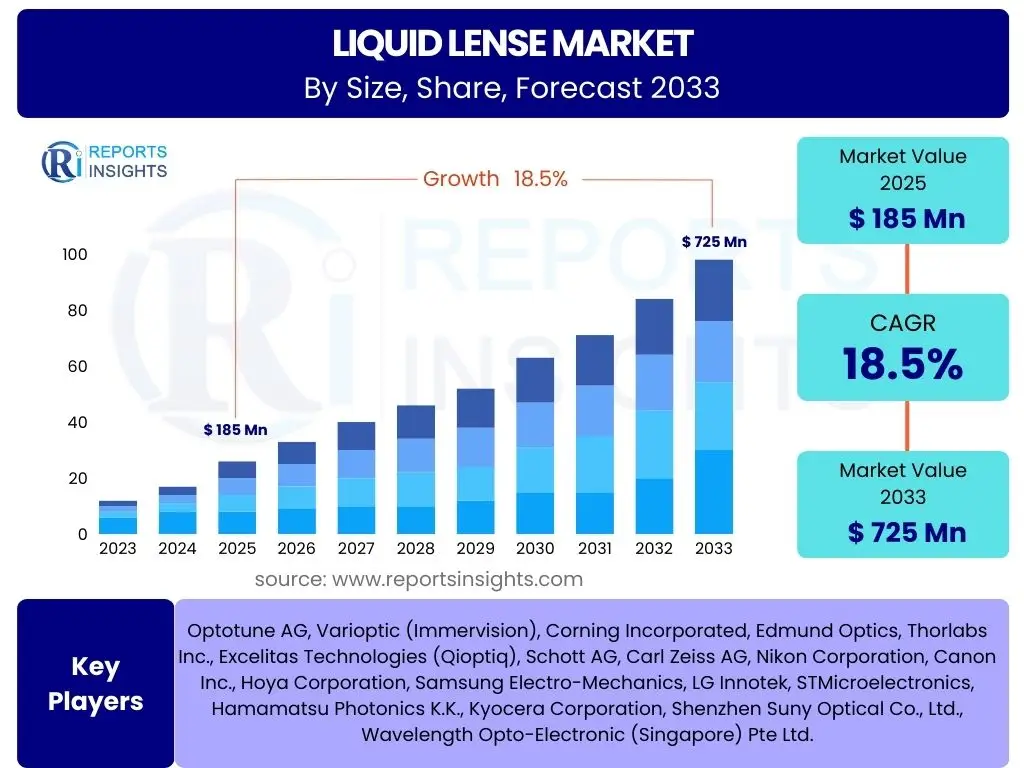

Liquid Lense Market Size

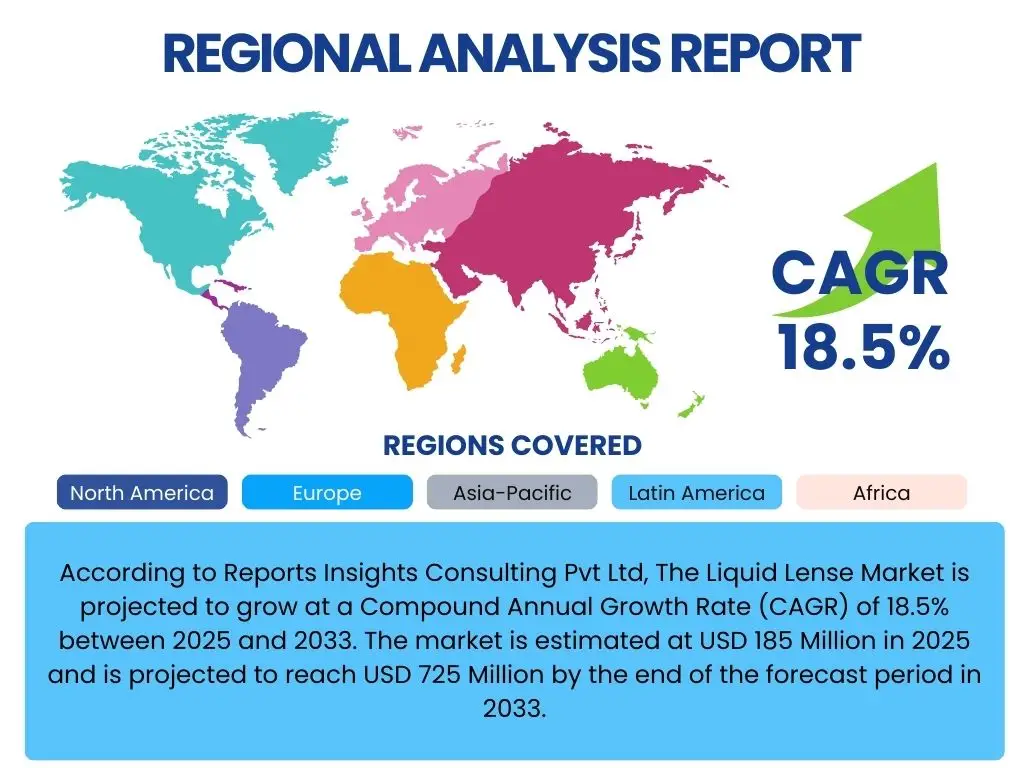

According to Reports Insights Consulting Pvt Ltd, The Liquid Lense Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 185 Million in 2025 and is projected to reach USD 725 Million by the end of the forecast period in 2033.

Key Liquid Lense Market Trends & Insights

The Liquid Lense market is undergoing significant transformation, driven by a confluence of technological advancements and expanding application landscapes. Key trends reveal a strong emphasis on miniaturization, enhanced performance, and seamless integration into diverse systems. Users are increasingly seeking information on how these lenses offer dynamic focusing capabilities, superior image stabilization, and adaptability in challenging environments, pushing manufacturers to innovate beyond traditional optical designs. The shift towards compact, energy-efficient solutions with rapid response times is a predominant theme, addressing the demand for more sophisticated imaging in consumer and industrial sectors.

Furthermore, the market is observing a growing interest in tunable optical properties, allowing for on-the-fly adjustments to focal length, aperture, and aberration correction without mechanical movement. This capability is pivotal for applications requiring high precision and flexibility, such as machine vision, medical imaging, and advanced photography. The integration of liquid lenses into complex optical modules, alongside other components like sensors and illumination systems, is also a notable trend, simplifying system design and reducing overall footprint. These developments collectively underscore a dynamic market moving towards smarter, more agile optical solutions.

- Miniaturization and compact design for seamless integration into portable devices.

- Rapid advancements in electro-wetting and electromechanical actuation technologies.

- Increasing adoption in advanced autofocus systems for consumer electronics.

- Development of liquid lenses with enhanced optical quality and wider tunable ranges.

- Growing demand for adaptive optics in industrial machine vision and medical diagnostics.

AI Impact Analysis on Liquid Lense

Artificial Intelligence (AI) is set to profoundly influence the Liquid Lense market by revolutionizing various stages from design and manufacturing to application and performance optimization. User inquiries frequently center on how AI can enhance the inherent capabilities of liquid lenses, particularly in terms of intelligent control, predictive performance, and real-time adaptability. AI algorithms can enable more precise and dynamic control over liquid lens parameters, allowing for ultra-fast and accurate focusing, zoom, and aberration correction in response to complex environmental data or user-specific requirements. This intelligence transforms static optical components into highly responsive, smart systems.

Beyond operational control, AI is also impacting the upstream processes, including the design and material selection for liquid lenses. Machine learning models can analyze vast datasets of material properties and optical performance metrics to accelerate the discovery of new liquid compositions or actuation mechanisms that offer superior characteristics, such as wider temperature ranges or improved durability. In manufacturing, AI-powered predictive maintenance and quality control systems can optimize production yields and reduce defects, ensuring consistent performance. The integration of AI thus positions liquid lenses not just as advanced optical components, but as critical elements within intelligent imaging and sensing ecosystems, capable of learning and adapting to dynamic scenarios, from autonomous vehicles to augmented reality headsets.

- AI-powered control algorithms enabling ultra-fast and precise dynamic focusing.

- Machine learning for optimizing liquid lens design and material discovery.

- Enhanced image processing and object recognition capabilities when paired with AI.

- Predictive maintenance and quality control in liquid lens manufacturing processes.

- Adaptive optics systems that learn and adjust to changing environmental conditions using AI.

Key Takeaways Liquid Lense Market Size & Forecast

The Liquid Lense market is poised for substantial expansion over the forecast period, reflecting a strong shift towards adaptive and miniature optical solutions across various industries. A primary takeaway is the impressive Compound Annual Growth Rate, indicating robust demand driven by the continuous need for innovative imaging and sensing technologies. Stakeholders frequently inquire about the underlying factors propelling this growth and the specific segments that are expected to contribute most significantly. The market's upward trajectory is firmly rooted in its ability to offer solutions that overcome the limitations of traditional optics, particularly concerning size, speed, and versatility, making it an attractive investment landscape.

Another crucial insight from the market size and forecast is the increasing penetration of liquid lenses into high-growth application areas, such as consumer electronics, industrial automation, and medical diagnostics. This broad application spectrum underscores the technology's adaptability and its potential to solve diverse optical challenges. Furthermore, the forecast highlights the ongoing innovation in material science and actuation mechanisms, which are continually improving the performance and reliability of liquid lenses, thereby sustaining market momentum. The market's strong growth prospects suggest a pivotal role for liquid lenses in the next generation of optical systems, offering transformative capabilities for both established and emerging technologies.

- The Liquid Lense market is projected for significant growth, reaching USD 725 Million by 2033.

- High CAGR of 18.5% indicates strong adoption across emerging and established applications.

- Miniaturization and dynamic optical capabilities are key drivers for market expansion.

- Consumer electronics and industrial automation are primary sectors fueling demand.

- Continuous R&D in materials and actuation will sustain market momentum and open new opportunities.

Liquid Lense Market Drivers Analysis

The expansion of the Liquid Lense market is significantly propelled by the increasing global demand for compact and versatile imaging systems across various end-use industries. As devices like smartphones, wearables, and drones become more sophisticated, there is an inherent need for optical components that can offer dynamic focusing, optical zoom, and image stabilization within extremely limited form factors. Traditional mechanical lenses often struggle to meet these requirements due to their size, weight, and inherent limitations in rapid adjustment. Liquid lenses provide a compelling alternative by achieving these functionalities electronically, without moving parts, which is a major advantage for modern device integration.

Furthermore, advancements in microfluidics and electro-wetting technologies have dramatically improved the performance, reliability, and manufacturing scalability of liquid lenses. These technological enhancements have led to the development of lenses with faster response times, broader optical ranges, and greater durability, addressing previous limitations and expanding their practical applications. The growing adoption of liquid lenses in critical sectors such as industrial automation, where precision and speed are paramount for tasks like quality inspection and robotic vision, and medical diagnostics, for advanced endoscopy and microscopy, further underscores their market-driving force. Their ability to adapt quickly to changing conditions, such as varying object distances or light levels, makes them indispensable for next-generation automated systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for compact and versatile imaging systems | +3.5% | Global | Short-to-Mid Term (2025-2029) |

| Advancements in microfluidics and electro-wetting technologies | +2.8% | North America, Europe, Asia Pacific | Mid-to-Long Term (2027-2033) |

| Growing adoption in industrial automation and medical diagnostics | +2.5% | Europe, North America, Japan | Short-to-Mid Term (2025-2030) |

| Need for fast autofocus and zoom capabilities in consumer electronics | +2.2% | Global | Short-to-Mid Term (2025-2028) |

Liquid Lense Market Restraints Analysis

Despite the promising growth trajectory, the Liquid Lense market faces several significant restraints that could impede its widespread adoption. One primary challenge is the relatively high manufacturing cost associated with liquid lenses compared to conventional fixed-focus optical elements. The precision required for fabricating microfluidic structures, integrating advanced actuation mechanisms, and ensuring reliable sealing of the liquid medium contributes to higher production expenses. This cost factor can be a barrier for mass-market applications, particularly in highly price-sensitive consumer electronics segments, where traditional lens solutions may offer a more economical, albeit less flexible, alternative.

Another critical restraint is the limited operational temperature range of certain liquid lens technologies. The physical properties of the liquids used, such as viscosity and refractive index, can be sensitive to temperature fluctuations, potentially affecting lens performance and stability in extreme hot or cold environments. This limitation restricts their deployment in applications exposed to harsh conditions, such as outdoor surveillance systems, automotive vision systems operating in diverse climates, or industrial environments with wide temperature swings. Ensuring long-term reliability and durability, especially for devices intended for extended use in varying conditions, also poses a significant engineering challenge, requiring robust materials and sealing techniques to prevent leakage or degradation over time.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High manufacturing costs and complex production processes | -2.0% | Global | Short-to-Mid Term (2025-2029) |

| Limited operational temperature range for certain liquid lens technologies | -1.5% | Extreme Environment Applications | Mid Term (2026-2031) |

| Challenges in achieving long-term reliability and durability | -1.2% | Consumer Electronics | Long Term (2028-2033) |

Liquid Lense Market Opportunities Analysis

The Liquid Lense market is ripe with opportunities, particularly driven by the emergence of new, high-growth applications that demand advanced optical capabilities. Augmented Reality (AR) and Virtual Reality (VR) headsets represent a significant avenue for expansion, as they require dynamic focal adjustment to reduce eye strain and improve user experience, known as the vergence-accommodation conflict. Liquid lenses can provide continuous and rapid focal plane adjustments, crucial for creating realistic immersive environments. Similarly, the automotive sector, especially in the context of autonomous vehicles, offers opportunities for liquid lenses in advanced driver-assistance systems (ADAS) and LiDAR, where adaptive optics can enhance object detection and ranging capabilities under varying weather conditions.

Further opportunities lie in the continuous development of novel materials and innovative actuation mechanisms. Research into new liquid compositions with enhanced optical properties, broader temperature stability, and improved electrical response characteristics can unlock new performance benchmarks. The exploration of alternative actuation methods, such as magneto-wetting or more efficient electromechanical designs, could lead to more robust, cost-effective, and energy-efficient liquid lens solutions, thereby expanding their market appeal. These advancements will enable liquid lenses to penetrate traditionally challenging sectors and address unmet needs in precision optics. Additionally, expansion into niche markets requiring highly specialized adaptive optics, such as scientific research, defense, and aerospace, provides avenues for substantial revenue growth, leveraging the unique benefits of liquid lens technology in demanding environments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of new applications in augmented/virtual reality (AR/VR) and autonomous vehicles | +3.0% | North America, Europe, Asia Pacific | Mid-to-Long Term (2027-2033) |

| Development of novel materials and actuation mechanisms for enhanced performance | +2.7% | R&D Hubs (Germany, US, Japan) | Long Term (2029-2033) |

| Expansion into niche markets requiring adaptive optics (e.g., scientific research, defense) | +2.0% | Defense, Scientific Research, Global | Mid-to-Long Term (2026-2032) |

Liquid Lense Market Challenges Impact Analysis

The Liquid Lense market faces significant challenges, particularly concerning the complexities associated with integrating these advanced optical components into existing systems. Unlike traditional fixed lenses, liquid lenses require sophisticated electronic control and often specialized power management, which can increase the design complexity and bill of materials for product developers. Compatibility issues with various sensor technologies, image processing pipelines, and mechanical housing designs present hurdles that require substantial engineering effort and customization. This integration complexity can slow down the adoption cycle, particularly for companies accustomed to more straightforward, off-the-shelf optical components.

Another substantial challenge is the enduring competition from well-established conventional optical solutions. While liquid lenses offer distinct advantages in terms of compactness and dynamic adjustability, traditional mechanical lenses are often more cost-effective for static or less demanding applications, and benefit from decades of refinement in manufacturing and material science. Convincing manufacturers and end-users to transition from proven, mature technologies to a newer, albeit more advanced, solution requires compelling demonstrations of superior performance, reliability, and cost-efficiency over the long term. Furthermore, the lack of widespread industry standardization for liquid lens interfaces, performance metrics, and form factors adds another layer of difficulty. Without common standards, interoperability between different manufacturers' products remains challenging, hindering broader market acceptance and potentially fragmenting the supply chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration complexities with existing optical and electronic systems | -1.8% | Consumer Electronics, Industrial Systems | Short-to-Mid Term (2025-2030) |

| Competition from conventional optical solutions in mass-market applications | -1.0% | Mass Market | Short-to-Mid Term (2025-2028) |

| Standardization issues and lack of universal compatibility across platforms | -0.8% | Global | Long Term (2028-2033) |

Liquid Lense Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Liquid Lense market, encompassing historical data, current market dynamics, and future projections. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report is designed to equip stakeholders with critical insights to make informed strategic decisions, identify key investment areas, and navigate the evolving market effectively. It covers detailed segmentation analysis across various types, applications, and end-users, alongside a thorough regional assessment to pinpoint growth hotspots and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185 Million |

| Market Forecast in 2033 | USD 725 Million |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Optotune AG, Varioptic (Immervision), Corning Incorporated, Edmund Optics, Thorlabs Inc., Excelitas Technologies (Qioptiq), Schott AG, Carl Zeiss AG, Nikon Corporation, Canon Inc., Hoya Corporation, Samsung Electro-Mechanics, LG Innotek, STMicroelectronics, Hamamatsu Photonics K.K., Kyocera Corporation, Shenzhen Suny Optical Co., Ltd., Wavelength Opto-Electronic (Singapore) Pte Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Liquid Lense market is comprehensively segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation allows for precise analysis of market dynamics across different technological approaches, application sectors, and end-user categories, revealing nuanced insights into demand patterns and competitive landscapes. By breaking down the market into distinct segments, the report highlights key areas of innovation and adoption, enabling stakeholders to identify specific opportunities and tailor strategies to targeted niches within the broader market. Understanding these segments is crucial for predicting future market evolution and identifying potential areas for technological disruption.

The segmentation by type reflects the various underlying physical principles and technologies employed in liquid lenses, each offering distinct advantages in terms of speed, tunability, and optical performance. Application-based segmentation underscores the vast array of industries benefiting from adaptive optics, ranging from high-volume consumer goods to specialized industrial and medical equipment. Furthermore, the segmentation by end-user provides insight into the primary consumers and integrators of liquid lens technology, showcasing how different stakeholders leverage these components to enhance their products and services. This detailed segmentation analysis is instrumental for a thorough market assessment and strategic planning.

- By Type: Electrowetting Liquid Lenses, Liquid Crystal Lenses, Tunable Acoustic Gradient (TAG) Lenses, Electromechanical Liquid Lenses.

- By Application: Consumer Electronics (Smartphones, Wearables, Cameras), Industrial Automation (Machine Vision, Robotics), Medical & Healthcare (Endoscopy, Microscopy, Ophthalmology), Automotive (ADAS, LiDAR), Aerospace & Defense, Scientific Research & Development, Augmented/Virtual Reality (AR/VR).

- By End-User: Device Manufacturers, System Integrators, Research Institutions, Healthcare Providers, Automotive OEMs.

Regional Highlights

The global Liquid Lense market demonstrates distinct regional dynamics, influenced by technological readiness, industrial infrastructure, and consumer adoption rates. Each region contributes uniquely to the market's overall growth, presenting varied opportunities and challenges for market players.

- North America: This region is a pioneer in liquid lens research and development, driven by a robust ecosystem of technology companies, advanced manufacturing capabilities, and significant investments in AR/VR and autonomous vehicle technologies. High adoption rates in industrial automation and medical diagnostics further bolster its market position.

- Europe: Characterized by strong industrial automation and a burgeoning medical devices sector, Europe exhibits substantial demand for high-precision liquid lenses. Countries like Germany and France are at the forefront of adopting these technologies in machine vision and scientific instruments, coupled with strong governmental support for R&D.

- Asia Pacific (APAC): APAC is expected to be the fastest-growing market, largely due to its dominance in consumer electronics manufacturing, particularly in countries like China, South Korea, and Japan. The region benefits from a large consumer base, rapid technological adoption in smartphones and wearables, and increasing investments in smart manufacturing and automotive sectors.

- Latin America: This region is an emerging market for liquid lenses, with growing industrialization and increasing investment in healthcare infrastructure. While adoption is currently moderate, significant potential exists as local economies develop and integrate advanced optical solutions.

- Middle East and Africa (MEA): The MEA region is witnessing gradual adoption, primarily driven by investments in smart city initiatives, defense applications, and improving healthcare facilities. The market here is expected to grow as technological awareness and infrastructure improve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Liquid Lense Market.- Optotune AG

- Varioptic (a division of Immervision)

- Corning Incorporated

- Edmund Optics

- Thorlabs Inc.

- Excelitas Technologies (Qioptiq)

- Schott AG

- Carl Zeiss AG

- Nikon Corporation

- Canon Inc.

- Hoya Corporation

- Samsung Electro-Mechanics

- LG Innotek

- STMicroelectronics

- Hamamatsu Photonics K.K.

- Kyocera Corporation

- Shenzhen Suny Optical Co., Ltd.

- Wavelength Opto-Electronic (Singapore) Pte Ltd.

Frequently Asked Questions

What is a liquid lens?

A liquid lens is an optical device that uses an electric field, pressure, or other external stimuli to change the shape of a liquid, thereby altering its focal length and optical power. Unlike traditional lenses that rely on mechanical movement of rigid glass elements, liquid lenses achieve dynamic focusing and zooming without any moving solid parts, making them compact, fast, and highly durable.

How do liquid lenses work?

Liquid lenses typically operate based on principles such as electrowetting, liquid crystal technology, or electromechanical actuation. In electrowetting, an electric voltage applied to a conductive liquid changes its surface tension, causing its shape to deform and thus altering its optical properties. Liquid crystal lenses manipulate the refractive index of liquid crystal materials to achieve tunability, while electromechanical types use external forces to physically reshape the liquid interface.

What are the main applications of liquid lenses?

Liquid lenses are widely used across various applications including consumer electronics (smartphones, cameras, wearables for fast autofocus), industrial automation (machine vision, barcode scanning for quick adjustments), medical & healthcare (endoscopy, ophthalmology for dynamic focusing), automotive (ADAS, LiDAR for adaptive sensing), scientific research, and emerging fields like augmented/virtual reality (AR/VR) headsets for mitigating vergence-accommodation conflict.

What are the advantages of liquid lenses over traditional lenses?

Liquid lenses offer several key advantages: they provide ultra-fast focusing speeds (milliseconds) compared to mechanical systems, are highly compact and lightweight due to the absence of moving parts, offer superior durability and shock resistance, consume less power for operation, and enable silent operation. Their ability to dynamically adjust focal length and other optical parameters without mechanical wear makes them ideal for demanding and miniaturized applications.

What challenges hinder the widespread adoption of liquid lenses?

Despite their benefits, liquid lenses face challenges such as higher manufacturing costs and complex production processes compared to conventional lenses, a relatively limited operational temperature range for certain technologies, and ongoing efforts to achieve long-term reliability and durability. Furthermore, integration complexities with existing optical and electronic systems and competition from well-established traditional optical solutions also pose adoption hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted