Light Calcium Carbonate Market

Light Calcium Carbonate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708560 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

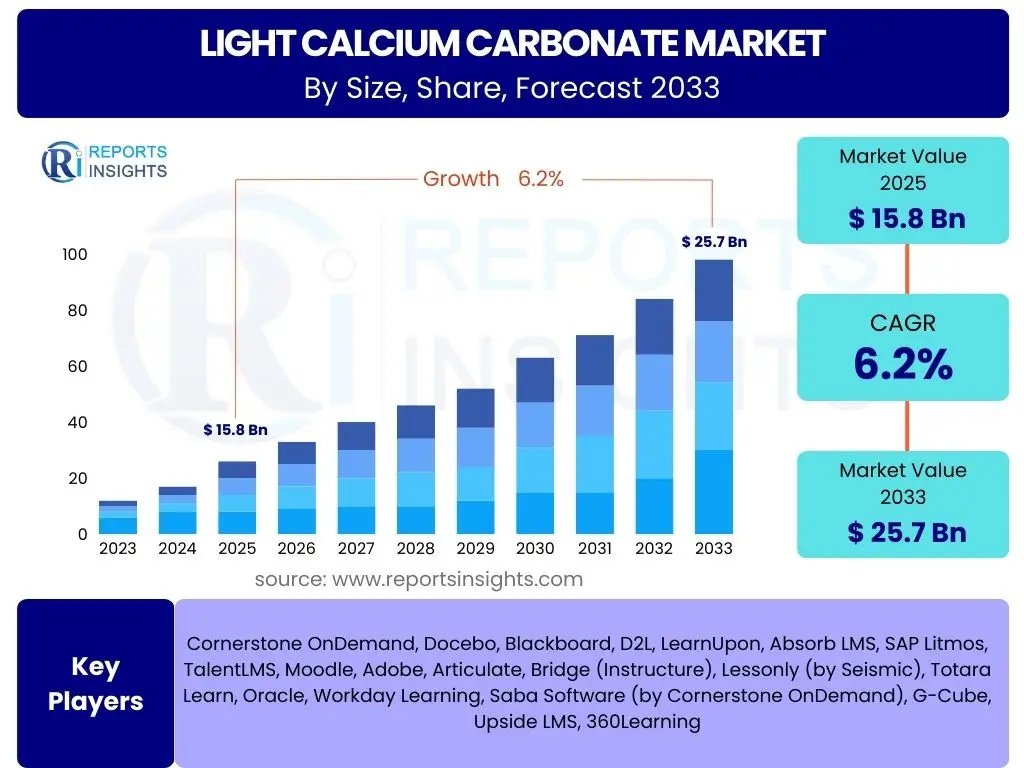

Light Calcium Carbonate Market Size

According to Reports Insights Consulting Pvt Ltd, The Light Calcium Carbonate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 15.8 Billion in 2025 and is projected to reach USD 25.7 Billion by the end of the forecast period in 2033.

Key Light Calcium Carbonate Market Trends & Insights

The Light Calcium Carbonate (LCC) market is currently undergoing significant transformations, driven by evolving industrial demands and a heightened focus on sustainability. Common user questions often revolve around how LCC's versatility is being leveraged in modern applications, particularly in sectors striving for enhanced product performance and eco-friendliness. There is a strong interest in understanding the shift towards higher-purity and specialized grades of LCC, which offer superior functional properties for advanced materials.

Furthermore, inquiries frequently highlight the impact of circular economy principles on LCC production and consumption. Users are keen to know about innovations in coating technologies that improve LCC's compatibility with various matrices, as well as the adoption of more energy-efficient manufacturing processes. The integration of LCC into novel composite materials and its role in lightweighting initiatives across industries like automotive and construction are also central themes in market trend discussions.

The market is also witnessing a trend towards regionalization of supply chains, prompted by geopolitical shifts and the desire for greater resilience against disruptions. This includes a focus on local sourcing of raw materials and decentralized production facilities to reduce transportation costs and carbon footprint. Moreover, the increasing adoption of LCC in emerging economies, fueled by rapid industrialization and infrastructure development, is a notable trend contributing to global market dynamics and shaping investment decisions.

- Increasing demand for lightweight and high-performance materials in automotive and construction.

- Growing adoption of LCC as a sustainable filler and extender in plastics and paper industries.

- Advancements in surface modification technologies enhancing LCC's functional properties.

- Shift towards specialized and ultra-fine LCC grades for high-end applications.

- Expansion of LCC applications in pharmaceutical, food, and personal care sectors.

- Focus on regionalized supply chains and local sourcing of raw materials.

AI Impact Analysis on Light Calcium Carbonate

The integration of Artificial Intelligence (AI) across industrial value chains is prompting significant user interest regarding its potential impact on the Light Calcium Carbonate (LCC) market. Common questions explore how AI can optimize LCC production processes, from raw material extraction and purification to grinding and surface treatment. Users are particularly interested in AI's role in predictive maintenance for complex machinery, aiming to reduce downtime and improve operational efficiency within LCC manufacturing facilities.

Furthermore, there is considerable curiosity about AI's capabilities in enhancing product quality control. This includes using machine learning algorithms to analyze particle size distribution, purity levels, and surface characteristics in real-time, ensuring consistency and meeting stringent application requirements. AI's potential to accelerate research and development (R&D) for new LCC grades, by simulating material properties and predicting performance in various matrices, is also a key area of inquiry, promising faster innovation cycles and customized solutions.

Beyond production and R&D, AI is expected to revolutionize supply chain management for LCC, enabling more accurate demand forecasting, optimizing logistics, and improving inventory management. This can lead to significant cost reductions and enhanced responsiveness to market fluctuations. The ability of AI to process vast amounts of market data for better strategic decision-making, including identifying emerging application areas and competitive intelligence, underscores its transformative potential across the entire LCC value chain, from raw material to end-user application.

- Optimized process control and automation in LCC manufacturing, improving energy efficiency.

- Enhanced quality control through real-time analysis of LCC particle characteristics and purity.

- Predictive maintenance for production equipment, reducing downtime and operational costs.

- Accelerated R&D for novel LCC grades and surface treatment technologies.

- Improved supply chain visibility, demand forecasting, and inventory management.

- Data-driven market analysis for identifying new application opportunities and competitive strategies.

Key Takeaways Light Calcium Carbonate Market Size & Forecast

Analyzing common user questions regarding the Light Calcium Carbonate (LCC) market size and forecast reveals a strong interest in understanding the underlying drivers of growth and the strategic implications for businesses. Users frequently inquire about the specific industries that will contribute most significantly to market expansion and the regional dynamics influencing demand. The primary takeaway is the sustained growth trajectory of the LCC market, primarily fueled by its indispensable role as a versatile filler and extender across numerous industrial applications, which are themselves experiencing growth.

A crucial insight is the increasing differentiation within the LCC market, with a clear trend towards value-added, specialized grades. This indicates that while volumetric growth is important, the higher-margin opportunities lie in LCC products engineered for specific performance enhancements, such as improved brightness, opacity, or mechanical properties in end-products. Therefore, investment in R&D and advanced processing capabilities will be paramount for stakeholders aiming to capture a larger share of the forecasted market value.

Furthermore, the forecast highlights the critical role of emerging economies in driving future demand, particularly in Asia Pacific and Latin America, where rapid industrialization, urbanization, and infrastructure development are creating vast opportunities. Companies looking to capitalize on this growth must adopt flexible strategies that address regional market specificities, including diverse regulatory landscapes and varying technological adoption rates. The market’s resilience against potential economic headwinds is also a significant takeaway, supported by the broad application base of LCC.

- Robust growth projected with a CAGR of 6.2%, reaching USD 25.7 Billion by 2033.

- Demand primarily driven by expansion in construction, automotive, paper, and plastics industries.

- Shift towards high-purity, specialized, and surface-treated LCC grades offers higher value.

- Emerging economies, particularly in Asia Pacific, will be key growth engines for the market.

- Strategic investments in R&D and advanced manufacturing processes are crucial for market players.

- LCC remains a cost-effective and performance-enhancing material, ensuring sustained demand across diverse sectors.

Light Calcium Carbonate Market Drivers Analysis

The Light Calcium Carbonate (LCC) market is propelled by a confluence of robust industrial demands and evolving material science. A primary driver is the pervasive use of LCC as a cost-effective, high-performance filler and extender across a multitude of end-use industries. Its ability to enhance properties such as brightness, opacity, strength, and processability, while simultaneously reducing formulation costs, makes it an attractive additive in applications ranging from paper and plastics to paints, coatings, and construction materials. The continuous expansion of these industries, particularly in developing regions, directly translates into increased demand for LCC.

Another significant driver is the increasing global focus on sustainability and lightweighting. LCC, being derived from abundant natural limestone, offers an environmentally friendly alternative to synthetic fillers. Its incorporation into plastics and composites helps reduce the overall weight of final products, contributing to fuel efficiency in automotive applications and lower transportation costs. This aligns with consumer and regulatory pressures for more sustainable and energy-efficient products, thereby bolstering LCC's market position. Furthermore, advancements in LCC processing technologies, leading to finer particle sizes and improved surface treatments, unlock new application possibilities and performance benefits.

The construction sector's rapid growth, especially in emerging markets, stands as a formidable driver. LCC is extensively used in concrete, mortars, sealants, and paints, improving their workability, durability, and aesthetic appeal. Similarly, the packaging industry's expansion, driven by e-commerce and changing consumer habits, fuels demand for LCC-filled plastics for films, containers, and other packaging solutions, where it contributes to stiffness, printability, and barrier properties. These macro-economic and industry-specific trends collectively provide a strong foundation for the sustained growth of the LCC market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from Paper and Plastics industries | +1.8% | Global, particularly Asia Pacific, North America | 2025-2033 |

| Expansion of the Construction Sector and Infrastructure Development | +1.5% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

| Increasing adoption in Paints, Coatings, and Adhesives | +1.2% | Europe, North America, Asia Pacific | 2025-2033 |

| Rising demand for eco-friendly and lightweight materials | +1.0% | Global | 2025-2033 |

| Technological advancements in LCC particle engineering | +0.7% | North America, Europe, Asia Pacific | 2025-2033 |

Light Calcium Carbonate Market Restraints Analysis

Despite its widespread utility, the Light Calcium Carbonate (LCC) market faces several restraints that could impede its growth trajectory. One significant restraint is the volatility in raw material prices, primarily limestone and energy. The energy-intensive nature of LCC production, involving calcination and subsequent carbonation and grinding, makes it susceptible to fluctuations in fuel costs. Additionally, the availability and quality of high-grade limestone deposits can impact production costs and overall supply, introducing an element of unpredictability for manufacturers.

Another crucial restraint stems from stringent environmental regulations concerning mining activities and industrial emissions. The extraction of limestone and the energy consumption during LCC processing contribute to environmental concerns, leading to tighter regulatory frameworks in many regions. Compliance with these regulations often requires significant investment in pollution control technologies and sustainable mining practices, which can increase operational costs and potentially slow down market expansion, especially for smaller players.

Furthermore, the availability of alternative fillers and extenders poses a competitive challenge to the LCC market. Materials such as heavy calcium carbonate (GCC), kaolin, talc, and specialty silicates can sometimes offer comparable functional properties at competitive prices, depending on the specific application requirements. While LCC often outperforms alternatives in certain attributes like brightness and opacity, the existence of a broad range of substitutes can limit LCC's market penetration in certain segments and exert downward pressure on pricing, thereby acting as a restraint on overall market growth and profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material (limestone, energy) prices | -0.9% | Global | 2025-2033 |

| Stringent environmental regulations on mining and emissions | -0.7% | Europe, North America, East Asia | 2025-2033 |

| Competition from alternative fillers (e.g., GCC, kaolin, talc) | -0.6% | Global | 2025-2033 |

| High initial capital investment for new production facilities | -0.4% | Emerging Economies | 2025-2033 |

Light Calcium Carbonate Market Opportunities Analysis

The Light Calcium Carbonate (LCC) market is poised for significant growth through various emerging opportunities driven by innovation and expanding application areas. One key opportunity lies in the development of novel applications, particularly in high-growth sectors such as electric vehicles (EVs), renewable energy infrastructure, and advanced packaging solutions. As these industries demand materials that are lightweight, durable, and sustainable, LCC can be engineered to meet these specific requirements, opening up new market segments for specialized grades and surface treatments. This allows for premium pricing and fosters innovation.

Another prominent opportunity is the increasing demand from emerging economies. Rapid industrialization, urbanization, and infrastructure development in countries across Asia Pacific, Latin America, and Africa are creating a massive need for construction materials, plastics, and paper products. As these regions continue to grow their manufacturing capabilities and consumer bases, the demand for basic and advanced LCC grades is expected to surge, providing substantial market expansion avenues for LCC producers who can establish robust supply chains and localized production facilities to cater to these markets.

Furthermore, advancements in surface modification and nanotechnology offer a lucrative avenue for LCC manufacturers. By coating LCC particles with organic or inorganic compounds, producers can significantly enhance their compatibility with various polymers, improve dispersion, and impart novel functionalities such as improved impact strength, thermal stability, or barrier properties. This focus on value-added LCC products, including nano-LCC, allows for differentiation from commodity grades and caters to the growing demand for high-performance materials in specialized applications, thereby securing competitive advantages and fostering market penetration into more sophisticated industries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of new high-performance and specialty LCC grades | +1.3% | Global | 2025-2033 |

| Expansion into emerging markets (e.g., India, Southeast Asia, Brazil) | +1.1% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Increased use in sustainable and biodegradable plastic applications | +0.9% | Europe, North America, East Asia | 2025-2033 |

| Technological advancements in surface functionalization and nano-LCC | +0.7% | North America, Europe, Asia Pacific | 2025-2033 |

Light Calcium Carbonate Market Challenges Impact Analysis

The Light Calcium Carbonate (LCC) market faces several critical challenges that require strategic navigation by industry players. One significant hurdle is the intense competitive landscape, characterized by the presence of numerous global and regional manufacturers. This high level of competition often leads to price pressures, particularly for commodity grades of LCC, which can compress profit margins for producers. Differentiating products through quality, service, and specialized grades becomes crucial in this environment, demanding continuous investment in research and development and customer relationship management.

Another pressing challenge is the complexity and potential for disruption within the global supply chain. LCC production relies heavily on the consistent supply of high-quality limestone, which is geographically concentrated. Geopolitical tensions, trade barriers, natural disasters, or logistical bottlenecks can significantly impact the availability and cost of raw materials and the distribution of finished products. Such disruptions can lead to production delays, increased transportation expenses, and an inability to meet customer demand, thereby undermining market stability and growth.

Furthermore, the market faces challenges related to technological advancements and the need for continuous innovation. While opportunities exist in developing new grades and applications, the associated R&D costs can be substantial, particularly for achieving ultra-fine particle sizes, unique surface chemistries, or functionalized LCC for high-performance applications. Companies must constantly invest in new technologies and processes to stay competitive and cater to the evolving demands of end-use industries, which require significant capital expenditure and expertise, posing a barrier to entry for new players and a challenge for existing ones to maintain their edge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense competition and price sensitivity in commodity grades | -0.8% | Global | 2025-2033 |

| Supply chain disruptions and logistics complexities | -0.7% | Global, particularly regions reliant on imports | 2025-2033 |

| High R&D costs for specialized and nano-LCC grades | -0.5% | North America, Europe, East Asia | 2025-2033 |

| Energy consumption and operational expenditure challenges | -0.4% | Global | 2025-2033 |

Light Calcium Carbonate Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Light Calcium Carbonate (LCC) market, covering historical data from 2019 to 2023, base year 2024, and projections for the forecast period from 2025 to 2033. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive primary and secondary research to deliver actionable insights into market dynamics, competitive landscape, and emerging trends impacting the LCC industry, providing a strategic blueprint for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 25.7 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Omya AG, Minerals Technologies Inc., Imerys S.A., Carmeuse, Mississippi Lime Company, Huber Engineered Materials, Sibelco, Lhoist Group, ESSECO s.r.l., Calchem, GLC Minerals, Revert Minerals, Okutama Kogyo Co., Ltd., Schaefer Kalk GmbH & Co KG, Solvay S.A., Graymont Limited, Cales de Llierca S.A., Fujian Sanmu Carbonate Co., Ltd., Longcliffe Quarries Ltd, Maruo Calcium Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Light Calcium Carbonate (LCC) market is extensively segmented to provide a granular understanding of its diverse applications and product types. This segmentation allows for precise analysis of market dynamics, growth drivers, and opportunities across various industrial verticals and product specifications. Understanding these segments is crucial for stakeholders to identify niche markets, develop targeted strategies, and optimize product portfolios in response to specific industry demands. The primary segmentation criteria include application, grade, and end-use industry, each reflecting distinct market needs and technological requirements.

By application, LCC is categorized based on its immediate use in manufacturing processes, such as its role as a filler in paper production to enhance brightness and opacity, or as an extender in plastics to improve rigidity and reduce costs. The differentiation between uncoated and coated grades highlights the importance of surface chemistry, where coated LCC offers superior dispersion and compatibility with polymers, essential for high-performance applications. These distinctions underscore the versatility of LCC and its adaptability to a wide range of material science challenges, driving innovation in product development.

The end-use industry segmentation further refines market analysis by grouping applications into broader sectors like building and construction, automotive, and food and pharmaceuticals. This allows for an assessment of how macroeconomic trends and industry-specific regulations impact LCC demand. Each segment presents unique performance requirements and regulatory landscapes, necessitating tailored LCC products and supply chain approaches. This detailed segmentation framework is vital for comprehending the complex interplay of factors shaping the LCC market and for forecasting future growth opportunities.

- By Application:

- Paper

- Plastics

- Paints & Coatings

- Adhesives & Sealants

- Rubber

- Food & Pharmaceuticals

- Building Materials

- Others (e.g., Personal Care, Agriculture)

- By Grade:

- Uncoated Light Calcium Carbonate

- Coated Light Calcium Carbonate

- Stearic Acid Coated LCC

- Resin Coated LCC

- Other Surface Treated LCC

- By End-Use Industry:

- Building & Construction

- Packaging

- Automotive

- Consumer Goods

- Healthcare

- Agriculture

- Electrical & Electronics

Regional Highlights

Geographically, the Light Calcium Carbonate (LCC) market exhibits significant variations in demand and growth dynamics, primarily influenced by regional industrial development, regulatory frameworks, and economic conditions. Asia Pacific stands as the largest and fastest-growing market, driven by rapid industrialization, extensive infrastructure projects, and the burgeoning manufacturing sectors in countries like China, India, and Southeast Asian nations. The region's robust growth in paper, plastics, construction, and automotive industries fuels a substantial and increasing demand for LCC, making it a pivotal area for market expansion and investment.

North America and Europe represent mature markets with a strong focus on high-performance and specialty LCC grades, driven by stringent environmental regulations and a demand for advanced materials in sectors such as automotive, aerospace, and premium coatings. Innovation in surface-treated LCC and nano-calcium carbonate is particularly prominent in these regions, catering to sophisticated industrial requirements and sustainability initiatives. While growth rates might be lower compared to Asia Pacific, the established industrial base and emphasis on value-added products ensure a steady and profitable market segment.

Latin America, the Middle East, and Africa are emerging markets for LCC, characterized by ongoing urbanization, growing manufacturing capabilities, and increasing investments in infrastructure and construction. Countries like Brazil, Mexico, and nations in the GCC are witnessing substantial demand for LCC in basic construction materials, paints, and packaging. These regions offer significant long-term growth potential, though they may also present challenges related to supply chain logistics, economic stability, and varying levels of technological adoption, necessitating tailored market entry strategies and localized production to capture these opportunities effectively.

- Asia Pacific: Dominates the global market due to rapid industrialization, extensive construction activities, and strong growth in the paper, plastics, and automotive sectors in China, India, Japan, and South Korea.

- Europe: A mature market characterized by demand for high-quality, specialized LCC grades for automotive, paints, and coatings, driven by stringent regulations and advanced manufacturing. Germany, France, and the UK are key contributors.

- North America: Significant market share, particularly in the plastics, paints & coatings, and building materials sectors. Focus on technological advancements and sustainable production practices. The U.S. is the primary market.

- Latin America: Emerging market with increasing demand from construction and packaging industries, especially in Brazil and Mexico, driven by urbanization and economic development.

- Middle East & Africa (MEA): Growth attributed to infrastructure development, construction boom, and expanding manufacturing base in countries like Saudi Arabia, UAE, and South Africa, although from a lower base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Light Calcium Carbonate Market.- Omya AG

- Minerals Technologies Inc.

- Imerys S.A.

- Carmeuse

- Mississippi Lime Company

- Huber Engineered Materials

- Sibelco

- Lhoist Group

- ESSECO s.r.l.

- Calchem

- GLC Minerals

- Revert Minerals

- Okutama Kogyo Co., Ltd.

- Schaefer Kalk GmbH & Co KG

- Solvay S.A.

- Graymont Limited

- Cales de Llierca S.A.

- Fujian Sanmu Carbonate Co., Ltd.

- Longcliffe Quarries Ltd

- Maruo Calcium Co., Ltd.

Frequently Asked Questions

What is Light Calcium Carbonate (LCC) and its primary uses?

Light Calcium Carbonate (LCC), also known as precipitated calcium carbonate (PCC), is a synthetic form of calcium carbonate produced by a chemical precipitation process. Its primary uses are as a high-performance filler, extender, and pigment in industries such as paper, plastics, paints, coatings, adhesives, rubber, and pharmaceuticals, where it enhances properties like brightness, opacity, strength, and processability.

What factors are driving the growth of the Light Calcium Carbonate market?

The market growth for Light Calcium Carbonate is primarily driven by the expanding demand from end-use industries like paper, plastics, paints & coatings, and construction. Other key drivers include the rising adoption of LCC as an eco-friendly and cost-effective filler, coupled with technological advancements in particle engineering that broaden its application scope and enhance performance.

Which regions are key contributors to the Light Calcium Carbonate market, and why?

Asia Pacific is the largest and fastest-growing market due to rapid industrialization, extensive construction, and robust growth in manufacturing sectors in countries like China and India. North America and Europe are significant contributors, focusing on specialty grades for advanced applications and sustainable solutions, driven by their mature industrial bases and stringent regulatory environments.

What are the main challenges facing the Light Calcium Carbonate industry?

Key challenges include intense market competition leading to price pressures, particularly for commodity grades. Additionally, the industry faces volatility in raw material and energy prices, stringent environmental regulations impacting production, and potential supply chain disruptions. High R&D costs for developing specialized, high-performance LCC grades also present a significant barrier.

How is AI expected to impact the Light Calcium Carbonate market?

AI is anticipated to significantly impact the LCC market by optimizing production processes, enhancing quality control through real-time analysis, and enabling predictive maintenance for machinery, leading to improved operational efficiency and reduced costs. AI also holds potential for accelerating R&D for new LCC grades and revolutionizing supply chain management for better forecasting and logistics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted