LF Refined Steel Market

LF Refined Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709087 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

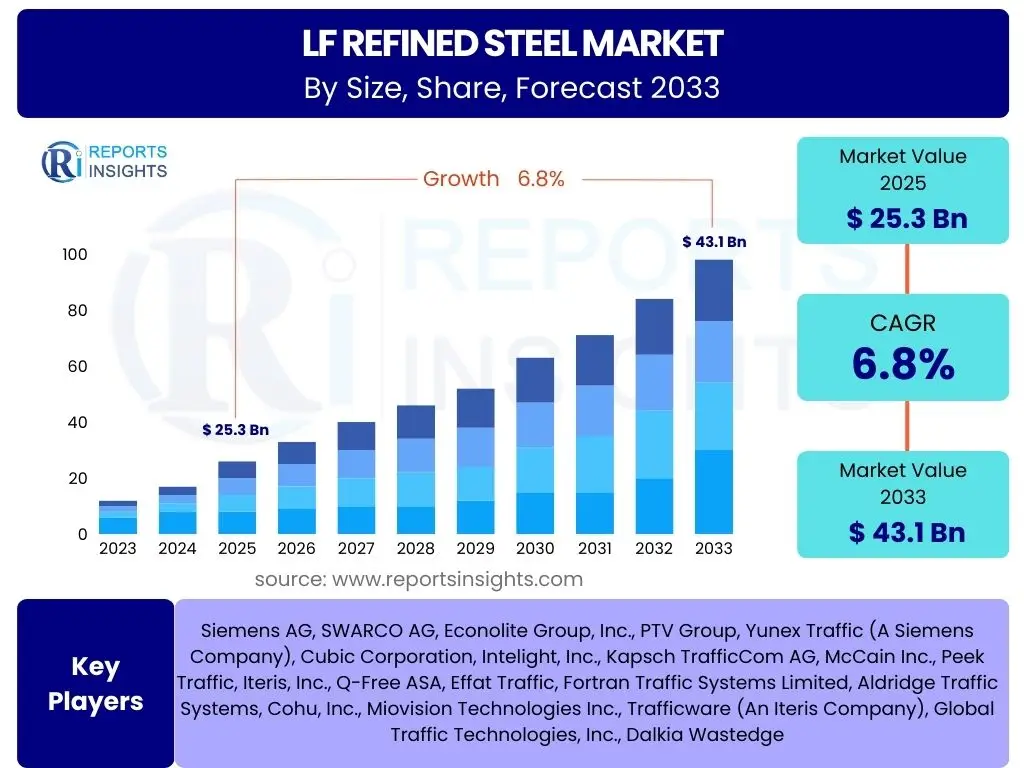

LF Refined Steel Market Size

According to Reports Insights Consulting Pvt Ltd, The LF Refined Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 25.3 Billion in 2025 and is projected to reach USD 43.1 Billion by the end of the forecast period in 2033.

Key LF Refined Steel Market Trends & Insights

The LF refined steel market is undergoing significant transformations driven by a confluence of technological advancements, evolving industry demands, and a heightened focus on sustainability. Users frequently inquire about the latest innovations in production processes, the impact of digitalization, and shifts in consumer preferences for specialized steel grades. There is a clear interest in how these trends are shaping the competitive landscape and creating new opportunities for market participants.

A prominent trend involves the increasing adoption of advanced refining techniques aimed at producing cleaner, higher-strength steel with improved metallurgical properties. This is directly linked to the growing demand from critical end-use sectors such as automotive, aerospace, and energy, which require materials capable of withstanding extreme conditions and offering enhanced performance. Furthermore, the integration of automation and data analytics into steelmaking processes is optimizing efficiency and quality control across the value chain, representing a significant shift towards Industry 4.0 paradigms within the sector.

Sustainability and circular economy principles are also exerting a powerful influence on market dynamics. Stakeholders are keen to understand the shift towards "green steel" production methods, including the use of hydrogen in steelmaking and increased recycling of scrap metal. This reflects a broader industry commitment to reducing carbon footprints and meeting stringent environmental regulations, which in turn influences investment decisions and market positioning.

- Growing demand for high-strength and ultra-high-strength steel grades in automotive and construction.

- Increased adoption of digital technologies and automation in steelmaking processes for enhanced efficiency and quality.

- Focus on sustainable production methods, including hydrogen-based steelmaking and increased scrap recycling.

- Expansion of LF refined steel applications in renewable energy infrastructure and specialized industrial machinery.

- Emphasis on supply chain resilience and localization of production to mitigate geopolitical risks.

AI Impact Analysis on LF Refined Steel

Common user questions regarding AI's impact on the LF refined steel sector often revolve around its potential to revolutionize operational efficiency, enhance product quality, and drive innovation. Users are keen to understand how artificial intelligence and machine learning algorithms are being integrated into complex metallurgical processes, from raw material procurement to final product inspection. The overarching themes include the desire for predictive capabilities, process optimization, and intelligent decision-making that can lead to significant cost savings and performance improvements.

AI is transforming the LF refined steel market by enabling advanced process control and predictive maintenance, significantly reducing downtime and operational costs. Through real-time data analysis from sensors and production lines, AI systems can anticipate equipment failures, optimize energy consumption, and fine-tune refining parameters to achieve superior steel properties consistently. This level of precision and foresight was previously unattainable, leading to more efficient resource utilization and a reduction in material waste.

Beyond operational enhancements, AI is also playing a crucial role in product development and quality assurance. Machine learning models can analyze vast datasets of material properties and performance characteristics, accelerating the design of new alloys with specific attributes. Furthermore, AI-powered vision systems are enhancing defect detection and classification, ensuring that only the highest quality LF refined steel products reach the market, thereby elevating industry standards and customer satisfaction. The strategic application of AI is thus positioning the LF refined steel sector for a new era of innovation and competitive advantage.

- Predictive maintenance for furnaces and refining equipment, minimizing unplanned downtime.

- Real-time process optimization through machine learning, improving energy efficiency and yield.

- Enhanced quality control and defect detection using AI-powered vision systems and data analytics.

- Accelerated material design and discovery for new LF refined steel alloys with desired properties.

- Improved supply chain management and demand forecasting through AI-driven analytical tools.

Key Takeaways LF Refined Steel Market Size & Forecast

Users frequently seek concise summaries of the market's trajectory, key growth drivers, and future prospects when analyzing the LF refined steel market size and forecast. The primary inquiries focus on understanding the underlying factors contributing to market expansion, identifying potential hurdles, and discerning the long-term viability of investments within the sector. There is a strong emphasis on actionable insights that highlight both the opportunities and risks associated with market participation.

The LF refined steel market is poised for robust expansion, driven by continuous industrialization, urban development, and the increasing demand for high-performance materials across diverse end-use sectors. Its projected Compound Annual Growth Rate (CAGR) of 6.8% underscores a stable and growing demand, propelled by sectors like automotive, construction, and advanced manufacturing, which increasingly require steel with superior purity, strength, and durability. This growth trajectory is also supported by ongoing technological advancements in steel production processes, making LF refined steel more accessible and cost-effective.

A critical takeaway is the market's resilience and adaptability to evolving global economic conditions and regulatory landscapes. Despite potential headwinds such as raw material price volatility or geopolitical uncertainties, the fundamental demand for high-quality steel remains strong. Investments in sustainable production methods and digitalization are further reinforcing the market's growth, offering significant opportunities for innovation and competitive differentiation. Stakeholders can anticipate sustained growth, emphasizing the strategic importance of this material in modern industrial applications.

- Consistent growth projected for the LF refined steel market, driven by industrial and infrastructure development.

- Significant demand from automotive, construction, and manufacturing sectors for high-quality, durable steel.

- Technological advancements in refining processes are enhancing efficiency and product quality.

- Emerging economies present substantial growth opportunities due to rapid urbanization and industrialization.

- Sustainability initiatives and the adoption of green steel production methods are becoming crucial market differentiators.

LF Refined Steel Market Drivers Analysis

The LF refined steel market is significantly influenced by several key drivers that contribute to its sustained growth and expansion. These drivers are primarily rooted in global industrial development, infrastructural needs, and the continuous demand for enhanced material properties in various applications. The need for steel with superior characteristics such as improved strength, ductility, and purity is a constant push factor, directly fueling the demand for LF refined steel.

One of the most prominent drivers is the accelerating pace of global infrastructure development. Countries worldwide are investing heavily in new transportation networks, urban development projects, and critical utilities, all of which require substantial volumes of high-quality steel. LF refined steel, with its enhanced mechanical properties and reliability, is ideally suited for these demanding applications, ensuring structural integrity and longevity in large-scale constructions. This sustained investment in public and private infrastructure acts as a foundational demand generator for the market.

Furthermore, the automotive sector's evolving requirements for lightweight, fuel-efficient, and safer vehicles represent another crucial driver. Modern vehicle designs incorporate advanced high-strength steels to reduce overall weight while maintaining or improving crash performance. LF refined steel meets these stringent specifications, enabling manufacturers to innovate and comply with increasingly strict emissions and safety regulations. The continuous innovation within manufacturing industries, especially those producing heavy machinery and precision components, also necessitates the use of high-purity and defect-free steel, further solidifying the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Infrastructure Development | +2.5% | Asia Pacific, North America, Europe | Short to Mid-term |

| Growing Automotive Sector Demand | +1.8% | Asia Pacific, Europe | Mid-term |

| Increasing Focus on High-Strength Steel | +1.5% | Global | Long-term |

| Technological Advancements in Steel Applications | +1.2% | North America, Europe | Mid to Long-term |

| Industrialization in Emerging Economies | +1.0% | Asia Pacific, Latin America | Long-term |

LF Refined Steel Market Restraints Analysis

While the LF refined steel market exhibits strong growth potential, it is also subject to several significant restraints that can impede its expansion and influence profitability. These challenges often stem from economic volatility, stringent regulatory frameworks, and the inherent complexities of the steel production process itself. Understanding these limitations is crucial for stakeholders to develop robust strategies and mitigate potential risks.

One of the primary restraints is the inherent volatility of raw material prices, particularly for key inputs such as iron ore, coking coal, and ferroalloys. Fluctuations in these commodity markets can directly impact production costs, making it difficult for manufacturers to maintain stable profit margins and competitive pricing. Geopolitical events, supply chain disruptions, and changes in global demand can all contribute to this price instability, posing a continuous challenge for procurement and operational planning within the LF refined steel sector.

Furthermore, the steel industry faces increasingly stringent environmental regulations and carbon emission targets, especially in developed economies. Compliance with these regulations often necessitates significant capital investments in new technologies and processes, which can increase operational expenses and potentially slow down production or expansion plans. High energy consumption associated with steelmaking also contributes to these challenges, as rising energy costs can put considerable pressure on manufacturers, particularly in regions with less competitive energy markets. These factors collectively create a complex operating environment that requires continuous adaptation and strategic investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.0% | Global | Short-term |

| Stringent Environmental Regulations | -0.8% | Europe, North America | Long-term |

| High Energy Consumption and Costs | -0.7% | Europe, Asia Pacific | Mid-term |

| Geopolitical Instability and Trade Barriers | -0.5% | Global | Short to Mid-term |

| High Capital Investment for Modernization | -0.4% | Global | Long-term |

LF Refined Steel Market Opportunities Analysis

Despite the challenges, the LF refined steel market presents numerous lucrative opportunities for growth and innovation. These opportunities stem from evolving technological landscapes, burgeoning demand in specific applications, and the increasing global emphasis on sustainable industrial practices. Identifying and capitalizing on these avenues is critical for market players aiming to expand their footprint and enhance their competitive edge.

A significant opportunity lies in the continued growth of emerging economies, particularly in Asia Pacific and Latin America. Rapid urbanization, industrialization, and infrastructure development in these regions are creating immense demand for high-quality steel. As these economies mature, their need for advanced materials for residential, commercial, and industrial construction, as well as for manufacturing sophisticated machinery and vehicles, will continue to escalate. This presents a vast untapped market for LF refined steel producers who can adapt to local market dynamics and supply chain requirements.

Furthermore, the increasing focus on sustainable and green steel production methods offers substantial opportunities for innovation and market differentiation. Companies investing in technologies like hydrogen-based steelmaking, carbon capture, utilization, and storage (CCUS), or those optimizing resource efficiency and recycling processes, stand to gain a competitive advantage. As environmental regulations tighten and consumer preferences shift towards eco-friendly products, manufacturers capable of offering certified "green" LF refined steel will likely capture a larger market share. Additionally, the expansion into specialized applications, such as aerospace, defense, and renewable energy sectors, which require ultra-high-performance and customized steel solutions, represents another high-value growth area for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Economies | +2.0% | Asia Pacific, Latin America, Middle East | Mid to Long-term |

| Development of Green Steel Technologies | +1.5% | Europe, North America, Asia Pacific | Long-term |

| Expansion into Specialized Applications | +1.0% | Global (Aerospace, Defense, Medical) | Mid-term |

| Digitalization and Industry 4.0 Integration | +0.8% | Global | Short to Mid-term |

| Increasing Demand for Customized Steel Solutions | +0.7% | North America, Europe, Asia Pacific | Mid-term |

LF Refined Steel Market Challenges Impact Analysis

The LF refined steel market, while promising, navigates a complex landscape filled with operational and strategic challenges that can influence its growth trajectory. These challenges span from intricate supply chain dynamics and workforce issues to intense market competition and the significant capital requirements for maintaining cutting-edge production facilities. Addressing these hurdles effectively is paramount for sustained success and market leadership.

One of the most persistent challenges faced by the LF refined steel market is the potential for supply chain disruptions. Global events, natural disasters, and geopolitical tensions can severely impact the availability and cost of essential raw materials and energy, leading to production delays and increased operational expenses. Managing these complexities requires robust risk mitigation strategies, including diversifying suppliers and investing in localized production capabilities to enhance resilience against external shocks. The highly integrated nature of the steel industry means that a disruption at one point in the chain can have cascading effects.

Furthermore, the steel industry, including LF refined steel production, is a capital-intensive sector that demands continuous investment in advanced technology and equipment for modernization and efficiency improvements. The high cost of adopting new environmentally compliant technologies or implementing sophisticated automation systems can be a significant barrier to entry for new players and a financial strain for existing ones. Additionally, a growing concern is the shortage of skilled labor, particularly in specialized roles requiring expertise in metallurgy, advanced manufacturing, and digital technologies. This talent gap can hinder innovation, impact operational efficiency, and drive up labor costs, posing a long-term challenge for the market's sustainable development and technological progression.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Vulnerability & Disruptions | -1.2% | Global | Short-term |

| Skilled Labor Shortage | -0.9% | North America, Europe, East Asia | Long-term |

| High Capital Intensity for R&D & Modernization | -0.7% | Global | Long-term |

| Intense Market Competition | -0.6% | Asia Pacific, Europe | Mid-term |

| Waste Management and By-product Utilization | -0.5% | Global | Mid to Long-term |

LF Refined Steel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the LF Refined Steel Market, covering historical performance, current market dynamics, and future growth projections from 2025 to 2033. It offers a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges, alongside a thorough segmentation analysis and regional insights. The report aims to equip stakeholders with critical data and strategic intelligence necessary for informed decision-making within this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.3 Billion |

| Market Forecast in 2033 | USD 43.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, POSCO, Baowu Group, HBIS Group, JFE Steel Corporation, Tata Steel, Hyundai Steel, Nucor Corporation, US Steel, JSW Steel, Gerdau S.A., Steel Dynamics Inc., Acerinox, thyssenkrupp AG, SSAB, Outokumpu, Aperam, VDM Metals, China Baowu Steel Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LF refined steel market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across various categories. This segmentation helps in identifying specific growth pockets, understanding demand patterns, and assessing competitive landscapes within each distinct segment. The market is primarily categorized by type, application, and end-use industry, reflecting the varied requirements and usage contexts of LF refined steel.

By dissecting the market into these segments, stakeholders can gain clarity on which product types are experiencing the highest demand, which applications are driving the most significant growth, and which end-use industries are the primary consumers. This structured analysis is essential for strategic planning, product development, and market entry decisions, enabling companies to tailor their offerings to specific market needs and optimize their resource allocation. Each segment is influenced by unique drivers, restraints, and opportunities, necessitating a distinct analytical approach.

The segmentation also highlights the versatility of LF refined steel, demonstrating its critical role across a wide spectrum of industries. From foundational carbon steel used in general construction to highly specialized alloy and stainless steels required for advanced technological applications, the market's segmented structure underscores its adaptability and indispensable nature in modern industrial ecosystems. Understanding these segment interactions and their individual trajectories is key to forecasting future market evolution.

- By Type:

- Carbon Steel: Primarily used in general construction and manufacturing, valued for its strength and cost-effectiveness.

- Alloy Steel: Incorporates elements like manganese, silicon, nickel, and chromium to enhance specific properties like strength, hardness, and corrosion resistance, crucial for automotive and machinery.

- Stainless Steel: Known for its corrosion resistance due to chromium content, essential in chemical processing, food industry, and architectural applications.

- By Application:

- Automotive: Used in vehicle chassis, engine components, and body panels requiring high strength-to-weight ratios.

- Construction: Structural components, rebar, and architectural elements in buildings and infrastructure projects.

- Manufacturing: Production of machinery, tools, and industrial equipment where durability and precision are paramount.

- Energy: Components for power generation plants, oil and gas pipelines, and renewable energy infrastructure.

- Aerospace: High-performance alloys for aircraft structures and engine parts, demanding extreme strength and fatigue resistance.

- Others: Includes medical instruments, defense equipment, and consumer goods.

- By End-Use Industry:

- Heavy Machinery: Used in agricultural, mining, and construction equipment.

- Consumer Goods: Appliances, cutlery, and various household items.

- Infrastructure: Bridges, roads, railways, and public utilities.

- Defense: Military vehicles, armor plating, and armaments.

- Others: Specialized industries like shipbuilding and precision engineering.

Regional Highlights

- Asia Pacific (APAC): Dominates the LF refined steel market, largely driven by rapid industrialization, extensive infrastructure development in countries like China and India, and a burgeoning automotive manufacturing sector. The region is both a major producer and consumer, characterized by high demand for various steel grades.

- Europe: A mature market characterized by stringent environmental regulations and a strong emphasis on high-quality, specialized steel for advanced manufacturing, automotive, and renewable energy sectors. Innovation in green steel production and circular economy principles are key drivers.

- North America: Exhibits significant demand from the automotive, construction, and oil & gas industries. The region focuses on technological advancements in steel production and increasing domestic capacity, with a growing emphasis on high-strength and lightweight steel for modern applications.

- Latin America: An emerging market with increasing investments in infrastructure and industrial development, particularly in Brazil and Mexico. The demand for LF refined steel is rising due to urbanization and growth in the automotive and construction sectors.

- Middle East and Africa (MEA): Growing due to large-scale construction projects, diversification initiatives away from oil, and investments in manufacturing and energy infrastructure. The region presents significant long-term growth opportunities, although geopolitical factors can influence market stability.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LF Refined Steel Market.- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Baowu Group

- HBIS Group

- JFE Steel Corporation

- Tata Steel

- Hyundai Steel

- Nucor Corporation

- US Steel

- JSW Steel

- Gerdau S.A.

- Steel Dynamics Inc.

- Acerinox

- thyssenkrupp AG

- SSAB

- Outokumpu

- Aperam

- VDM Metals

- China Baowu Steel Group

Frequently Asked Questions

What is LF refined steel?

LF refined steel refers to steel that has undergone ladle furnace (LF) treatment, a secondary metallurgical process. This process improves the steel's purity, homogeneity, and mechanical properties by removing impurities like sulfur and oxygen, adjusting alloy composition, and controlling temperature. It results in high-quality steel suitable for demanding applications.

What are the primary applications of LF refined steel?

LF refined steel is predominantly used in applications requiring high strength, durability, and specific metallurgical properties. Key applications include the automotive sector for lightweight and safe vehicles, construction for infrastructure and structural components, manufacturing for heavy machinery and precision tools, and the energy sector for demanding components in power generation and oil & gas.

How does LF refinement enhance steel quality?

Ladle furnace refinement significantly enhances steel quality by achieving precise temperature control, desulfurization (removal of sulfur), deoxidation (removal of oxygen), and homogenization of alloying elements. This leads to cleaner steel with fewer non-metallic inclusions, improved mechanical properties, better fatigue resistance, and enhanced weldability and formability compared to conventionally produced steel.

What factors are driving the growth of the LF refined steel market?

The growth of the LF refined steel market is primarily driven by increasing global infrastructure development, the expanding automotive sector's demand for high-strength-to-weight ratio materials, and rapid industrialization in emerging economies. Additionally, technological advancements requiring superior quality steel and a greater focus on material performance in critical applications also contribute significantly to market expansion.

What are the key challenges in the LF refined steel market?

Key challenges in the LF refined steel market include the volatility of raw material prices, stringent environmental regulations necessitating costly compliance, high energy consumption in production processes, and potential disruptions in global supply chains. Furthermore, the market faces challenges related to attracting and retaining skilled labor and the high capital investment required for facility modernization and technological upgrades.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted