Less than Truckload Market

Less than Truckload Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705926 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

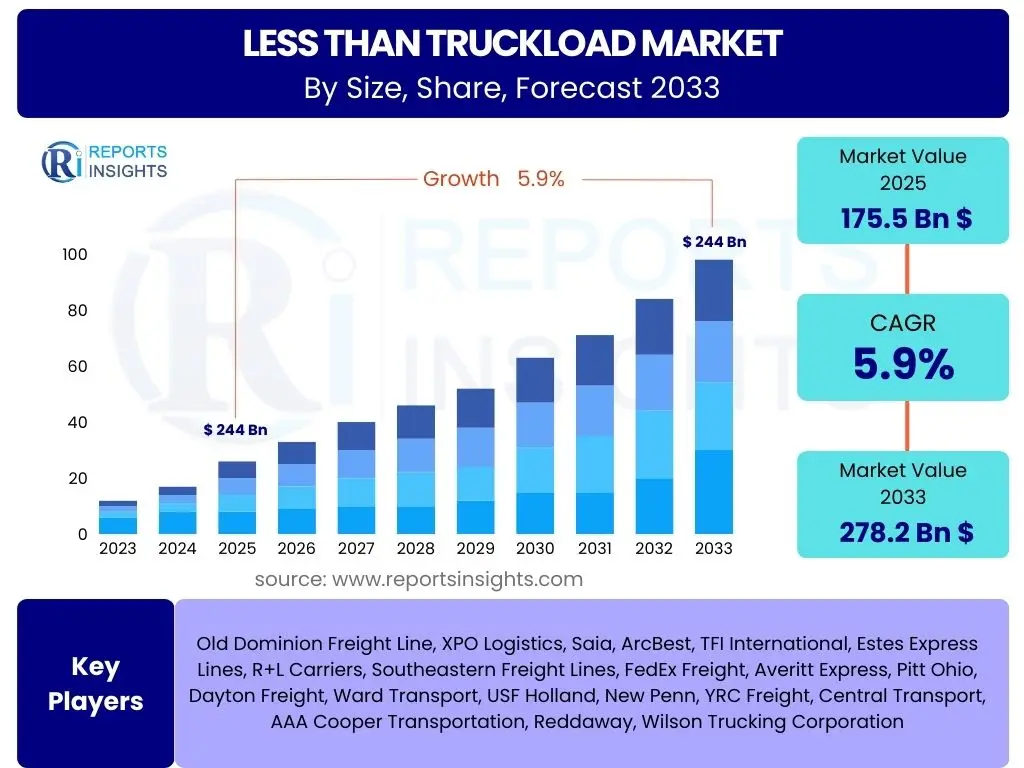

Less than Truckload Market Size

According to Reports Insights Consulting Pvt Ltd, The Less than Truckload Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.9% between 2025 and 2033. The market is estimated at 175.5 Billion USD in 2025 and is projected to reach 278.2 Billion USD by the end of the forecast period in 2033.

Key Less than Truckload Market Trends & Insights

The Less than Truckload (LTL) market is currently experiencing a dynamic period, driven by evolving shipper demands and technological advancements. User inquiries frequently center on how e-commerce growth is reshaping LTL services, the increasing demand for expedited and specialized shipping options, and the pervasive influence of digital tools like Transportation Management Systems (TMS) and real-time tracking. Shippers are increasingly looking for efficiency and transparency, pushing carriers to adopt more sophisticated operational models.

Another significant trend involves the optimization of freight networks and consolidation strategies. As businesses strive to reduce shipping costs and improve delivery times, the ability of LTL carriers to efficiently consolidate diverse shipments from multiple customers into single trailers becomes paramount. This often involves intricate hub-and-spoke models and advanced route planning software. Furthermore, there is a growing emphasis on sustainability, with companies seeking LTL partners who can demonstrate a commitment to reducing carbon emissions through optimized logistics and greener fleets.

Finally, the market is witnessing a notable shift towards greater service customization and premium offerings. While cost-effectiveness remains a core appeal of LTL, a segment of the market is willing to pay more for guaranteed delivery times, white-glove services, or specialized handling for sensitive goods. This trend is particularly pronounced in industries with high-value or time-critical products, creating new revenue streams and competitive differentiators for LTL providers.

- Accelerated adoption of e-commerce driving increased LTL volumes and last-mile complexities.

- Rising demand for expedited, guaranteed, and specialized LTL services.

- Enhanced focus on digital transformation, including TMS, IoT, and real-time visibility.

- Strategic optimization of freight consolidation and network density.

- Growing emphasis on sustainability and environmentally friendly logistics practices.

- Persistent challenges with driver shortages and capacity management.

AI Impact Analysis on Less than Truckload

User queries regarding the impact of Artificial Intelligence (AI) on the Less than Truckload (LTL) sector primarily revolve around efficiency gains, predictive capabilities, and the automation of complex processes. Shippers and carriers are keen to understand how AI can optimize route planning, improve load consolidation, and enhance demand forecasting, thereby reducing operational costs and improving service reliability. There is also significant interest in AI's role in predictive maintenance for vehicle fleets and its potential to streamline administrative tasks through automation.

AI's influence extends deeply into operational analytics, enabling LTL carriers to process vast amounts of data from various sources, including GPS, sensor data, weather patterns, and historical traffic. This data-driven insight allows for more accurate estimations of transit times, proactive identification of potential delays, and dynamic adjustment of routes. Consequently, AI contributes to higher asset utilization and reduced empty miles, directly impacting profitability and environmental footprint.

Moreover, AI is poised to revolutionize customer service and supply chain visibility within the LTL domain. AI-powered chatbots can handle routine customer inquiries, providing instant updates on shipment status and addressing common issues, thereby freeing up human agents for more complex tasks. Furthermore, AI algorithms can analyze customer behavior and market trends to predict future demand, enabling LTL providers to proactively allocate resources and optimize pricing strategies. This intelligent automation not only improves operational fluidity but also significantly enhances the overall customer experience.

- Route optimization: AI algorithms dynamically identify the most efficient routes, considering real-time traffic, weather, and delivery windows, minimizing fuel consumption and transit times.

- Load consolidation: AI enhances the ability to combine multiple LTL shipments effectively, maximizing trailer utilization and reducing per-parcel shipping costs.

- Predictive maintenance: AI analyzes telematics data to predict equipment failures, allowing for proactive maintenance and reducing unexpected breakdowns and delays.

- Demand forecasting: AI improves accuracy in predicting future freight volumes, enabling carriers to optimize staffing, equipment allocation, and network capacity.

- Automated pricing: AI tools analyze market conditions, historical data, and real-time demand to offer dynamic and competitive pricing strategies.

- Enhanced security: AI-powered surveillance and anomaly detection systems can improve cargo security and identify potential threats during transit.

Key Takeaways Less than Truckload Market Size & Forecast

Common user questions about the Less than Truckload (LTL) market forecast frequently touch upon its growth trajectory, the primary drivers sustaining this growth, and the factors that could potentially impede it. Users are keen to understand if the market is stable for investment, what technological shifts are most impactful, and how external economic conditions might shape its future. The overarching sentiment points towards an interest in both the quantitative growth projections and the qualitative strategic insights necessary for navigating this complex logistics sector.

The LTL market is expected to demonstrate robust growth through 2033, primarily fueled by the sustained expansion of e-commerce, the increasing fragmentation of supply chains, and the imperative for businesses to find cost-effective shipping solutions for smaller, more frequent orders. This growth is not uniform across all segments; specialized services and technologically advanced providers are poised for higher gains. The forecast underscores the resilience of LTL as a critical component of the broader logistics ecosystem, adapting to evolving trade patterns and consumer expectations.

A significant takeaway is the dual importance of both technological adoption and operational excellence. While digital tools, including AI and advanced analytics, will be crucial for optimizing efficiency and visibility, the fundamental strength of LTL carriers will continue to depend on strong network density, reliable last-mile capabilities, and skilled labor. Companies that can seamlessly integrate cutting-edge technology with traditional operational expertise will be best positioned to capitalize on the projected market growth and maintain competitive advantage.

- The Less than Truckload market is poised for steady expansion, driven by continuous e-commerce growth and evolving supply chain needs.

- Technological integration, particularly AI and advanced digital platforms, will be pivotal for operational efficiency, cost reduction, and service enhancement.

- Shippers increasingly prioritize reliable, transparent, and flexible LTL services, influencing carrier investment in real-time tracking and customer communication.

- Capacity management and labor availability will remain critical challenges, requiring strategic planning and investment from LTL providers.

- The market will see a greater demand for specialized LTL services and sustainable logistics solutions.

Less than Truckload Market Drivers Analysis

The Less than Truckload (LTL) market is propelled by a confluence of macroeconomic and industry-specific factors that collectively foster its expansion. A primary driver is the relentless growth of the e-commerce sector, which generates a high volume of smaller, more frequent shipments that are ideally suited for LTL services. As online retail continues to penetrate new markets and diversify product offerings, the demand for efficient LTL consolidation and distribution networks escalates. This paradigm shift in consumer purchasing habits necessitates robust LTL infrastructure to support last-mile delivery and regional fulfillment centers.

Another significant driver is the increasing complexity and fragmentation of global supply chains. Businesses are adopting leaner inventory strategies and just-in-time delivery models, leading to smaller, more frequent orders rather than large, bulk shipments. This trend naturally favors LTL, as it offers a cost-effective alternative to Full Truckload (FTL) for partial loads, reducing warehousing costs and improving supply chain agility. Additionally, the expansion of manufacturing and industrial activities globally contributes to increased freight movement, much of which falls within the optimal size and weight for LTL services.

Furthermore, technological advancements within the logistics sector itself are acting as powerful market drivers. Innovations in Transportation Management Systems (TMS), real-time tracking, and predictive analytics enable LTL carriers to optimize their networks, improve operational efficiency, and offer enhanced visibility to shippers. These technological improvements make LTL services more reliable and attractive, fostering greater adoption across various industries. The drive for cost efficiency among businesses also consistently pushes them towards LTL as a viable solution for managing freight expenditures without compromising on service quality for smaller consignments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Boom & Parcelization of Shipments | +1.8% | Global, particularly North America, Asia Pacific | Short-term to Long-term (2025-2033) |

| Growing Manufacturing & Industrial Output | +1.5% | Asia Pacific, North America, Europe | Mid-term to Long-term (2026-2033) |

| Increased Demand for Cost-Effective & Flexible Shipping | +1.2% | Global | Short-term to Long-term (2025-2033) |

| Technological Advancements in Logistics | +1.0% | Global | Short-term to Mid-term (2025-2029) |

| Supply Chain Optimization & Inventory Management Trends | +0.8% | Global | Mid-term (2027-2031) |

Less than Truckload Market Restraints Analysis

Despite its inherent advantages and growth drivers, the Less than Truckload (LTL) market faces several significant restraints that can impede its expansion and operational efficiency. One prominent restraint is the volatility of fuel prices. LTL operations involve extensive routing and frequent stops, making them highly susceptible to fluctuations in diesel costs. While carriers attempt to mitigate this through fuel surcharges, consistently high or unpredictable fuel expenses can squeeze profit margins and translate into higher shipping costs for customers, potentially leading some to seek alternative shipping methods or consolidate shipments to qualify for Full Truckload (FTL) rates.

Another critical restraint is the persistent shortage of qualified commercial drivers. The LTL segment, similar to the broader trucking industry, struggles with recruiting and retaining drivers due to demanding schedules, long hours, and an aging workforce. This shortage directly impacts carrier capacity, leading to potential service delays, higher labor costs, and reduced ability to handle increased freight volumes. The issue is exacerbated by regulatory pressures and the need for specialized endorsements, making it challenging to expand the driver pool quickly enough to meet growing demand.

Furthermore, infrastructure limitations and traffic congestion in urban areas pose substantial operational challenges. As LTL freight often involves pickups and deliveries in densely populated regions, congested roads and limited loading dock access can significantly slow down operations, increase transit times, and raise labor costs. This inefficiency not only impacts carrier profitability but also affects customer satisfaction due to delayed deliveries. The capital-intensive nature of maintaining a comprehensive LTL network, including terminals, trucks, and technology, also acts as a financial barrier for new entrants and limits the rapid expansion capabilities of existing players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuating Fuel Prices | -0.9% | Global | Short-term to Long-term (2025-2033) |

| Shortage of Qualified Drivers and Labor | -0.8% | North America, Europe | Short-term to Mid-term (2025-2029) |

| Intense Competition and Pricing Pressures | -0.7% | Global | Long-term (2028-2033) |

| Infrastructure Limitations & Traffic Congestion | -0.6% | Urban areas globally, particularly North America, Europe | Mid-term to Long-term (2027-2033) |

| High Operational Costs (Maintenance, Insurance, etc.) | -0.5% | Global | Short-term to Long-term (2025-2033) |

Less than Truckload Market Opportunities Analysis

Despite the inherent challenges, the Less than Truckload (LTL) market is rich with opportunities for growth and innovation. One significant opportunity lies in the continued investment in and adoption of advanced digital technologies. The integration of Artificial Intelligence (AI) for predictive analytics, machine learning for optimal route planning, and blockchain for enhanced supply chain transparency can revolutionize LTL operations, leading to unprecedented levels of efficiency and customer satisfaction. Carriers who proactively embrace these technologies can differentiate themselves and capture a larger market share by offering superior service and reduced costs.

Another promising area is the expansion into specialized LTL services. As industries evolve, there is an increasing demand for the transportation of delicate, temperature-sensitive, hazardous, or high-value goods that require specialized handling and equipment. Developing capabilities in areas such as temperature-controlled LTL, white-glove delivery, or hazmat certified transport allows carriers to tap into niche markets with higher profit margins and less price sensitivity. This diversification strengthens a carrier's portfolio and reduces reliance on general freight volumes.

Furthermore, strategic partnerships and consolidations present significant opportunities for market expansion and increased network density. Smaller LTL carriers can leverage partnerships with larger logistics providers or technology firms to extend their reach, enhance their technological capabilities, and improve operational efficiencies. Conversely, larger players can acquire smaller regional carriers to expand their geographic footprint and absorb existing customer bases. The drive for sustainability also offers an opportunity for LTL providers to invest in eco-friendly fleets and optimize their logistics processes to reduce carbon emissions, appealing to environmentally conscious shippers and potentially qualifying for green incentives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Advanced Logistics Technologies (AI, IoT, Big Data) | +1.5% | Global | Short-term to Long-term (2025-2033) |

| Expansion into Specialized & Value-Added LTL Services | +1.3% | Global, particularly developed markets | Mid-term to Long-term (2027-2033) |

| Growth in Cross-Border E-commerce Shipments | +1.0% | Asia Pacific, North America, Europe | Short-term to Long-term (2025-2033) |

| Strategic Partnerships, Mergers & Acquisitions for Network Expansion | +0.9% | Global | Mid-term (2026-2030) |

| Focus on Sustainable Logistics & Green Initiatives | +0.7% | Europe, North America | Mid-term to Long-term (2028-2033) |

Less than Truckload Market Challenges Impact Analysis

The Less than Truckload (LTL) market is subject to several complex challenges that necessitate strategic navigation for sustained growth and profitability. One primary challenge is the inherent complexity of managing LTL networks. Unlike Full Truckload (FTL), LTL operations involve the intricate consolidation and deconsolidation of multiple shipments from various customers, requiring sophisticated routing, scheduling, and terminal management. Mismanagement in any part of this process can lead to inefficiencies, increased costs, and compromised service quality, directly impacting customer satisfaction and carrier reputation. This complexity scales significantly with network size and freight volume.

Another critical challenge stems from the increasing customer expectations for speed, transparency, and flexibility. The Amazon effect has raised the bar across all logistics sectors, with LTL customers now demanding faster transit times, real-time tracking visibility, and more flexible pickup and delivery options. Meeting these heightened expectations requires significant investment in technology, infrastructure, and human capital, placing a considerable burden on LTL carriers, especially in a competitive pricing environment. Failure to adapt to these demands can result in loss of market share and customer churn.

Furthermore, economic volatility and fluctuating freight demand cycles pose a constant threat to LTL stability. Economic downturns can lead to reduced shipping volumes, intensifying competition and driving down rates. Conversely, sudden spikes in demand can strain existing capacity and exacerbate driver shortages. Managing these unpredictable cycles requires agile operational models, flexible pricing strategies, and robust financial planning. Cybersecurity threats and the need for continuous technological upgrades to combat these threats also represent an ongoing challenge, as LTL carriers handle sensitive data and rely heavily on interconnected digital systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Network Management & Freight Consolidation | -1.0% | Global | Short-term to Long-term (2025-2033) |

| Rising Customer Expectations for Speed & Transparency | -0.9% | Global, particularly North America, Europe | Short-term to Mid-term (2025-2029) |

| Economic Volatility & Fluctuations in Freight Demand | -0.8% | Global | Short-term (2025-2026) |

| High Entry Barriers & Capital Expenditure for Network Development | -0.7% | Global | Long-term (2028-2033) |

| Cybersecurity Threats & Data Protection Requirements | -0.6% | Global | Short-term to Long-term (2025-2033) |

Less than Truckload Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Less than Truckload (LTL) market, offering detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. The scope includes a thorough examination of key market trends, an impact assessment of Artificial Intelligence on LTL operations, and a granular analysis of market drivers, restraints, opportunities, and challenges. The report further dissects the market by various segments and highlights regional dynamics, offering a holistic view for stakeholders seeking to understand and strategize within this vital logistics sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 175.5 Billion USD |

| Market Forecast in 2033 | 278.2 Billion USD |

| Growth Rate | 5.9% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Old Dominion Freight Line, XPO Logistics, Saia, ArcBest, TFI International, Estes Express Lines, R+L Carriers, Southeastern Freight Lines, FedEx Freight, Averitt Express, Pitt Ohio, Dayton Freight, Ward Transport, USF Holland, New Penn, YRC Freight, Central Transport, AAA Cooper Transportation, Reddaway, Wilson Trucking Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Less than Truckload (LTL) market is broadly segmented to provide a granular understanding of its diverse components and cater to specific shipping needs. This segmentation allows for a more precise analysis of market dynamics, competitive landscapes, and growth opportunities within distinct operational categories. By dividing the market based on service type, industry vertical, and end-user, stakeholders can identify key trends, tailor service offerings, and develop targeted marketing strategies.

Segmentation by service type differentiates between various levels of speed, reliability, and handling requirements, ranging from standard LTL, which prioritizes cost-effectiveness for non-urgent shipments, to expedited and guaranteed services that cater to time-sensitive deliveries. Specialized LTL services further cater to niche demands such as temperature control for perishable goods or hazardous material handling, reflecting the evolving complexities of modern supply chains. Understanding these distinctions is crucial for carriers to optimize their operational models and for shippers to select the most appropriate service for their freight.

Moreover, segmenting the market by industry vertical and end-user provides insights into specific sector demands and purchasing behaviors. Different industries, such as retail, manufacturing, automotive, or healthcare, have unique shipping profiles, freight characteristics, and regulatory requirements that influence their choice of LTL services. Similarly, the needs of Small & Medium Enterprises (SMEs) often differ significantly from those of Large Enterprises, impacting volume, frequency, and service expectations. This multi-faceted segmentation helps to reveal the underlying drivers of demand and potential areas for market penetration or specialization within the LTL ecosystem.

- By Service Type:

- Standard LTL

- Expedited LTL

- Guaranteed LTL

- Cross-border LTL

- Specialized LTL (e.g., Temperature-controlled, Hazardous Materials, High-Value Goods)

- By Industry Vertical:

- Retail & E-commerce

- Manufacturing (Industrial Goods, Machinery)

- Automotive

- Food & Beverages

- Healthcare & Pharmaceutical

- Chemicals

- Others (e.g., Construction, Electronics, Consumer Goods)

- By End-User:

- Small & Medium Enterprises (SMEs)

- Large Enterprises

Regional Highlights

The Less than Truckload (LTL) market exhibits distinct dynamics across various global regions, influenced by economic development, infrastructure quality, regulatory frameworks, and the prevalence of e-commerce. North America, particularly the United States, stands as the largest and most mature LTL market. This dominance is attributed to its vast geographical expanse, a highly developed logistics infrastructure, robust e-commerce penetration, and a strong manufacturing base that generates significant LTL volumes. The region benefits from established carriers with extensive networks, but also faces challenges such as driver shortages and high operational costs.

Europe represents another significant LTL market, characterized by dense population centers, complex cross-border regulations within the European Union, and a strong emphasis on intermodal transportation. The demand for efficient LTL services is driven by a sophisticated manufacturing sector and a growing e-commerce landscape. However, navigating diverse national regulations, language barriers, and varied infrastructure quality across member states presents unique challenges. The focus on sustainability and green logistics is also more pronounced in Europe, influencing carrier investments in eco-friendly fleets and optimized consolidation practices.

Asia Pacific is projected to be the fastest-growing region in the LTL market, primarily fueled by rapid industrialization, burgeoning e-commerce platforms, and a large consumer base, particularly in China and India. The region is witnessing significant investment in logistics infrastructure development, though challenges such as fragmented supply chains, varying road quality, and customs complexities persist. Latin America and the Middle East & Africa (MEA) are emerging markets for LTL, driven by increasing trade activities, urbanization, and improving connectivity. These regions present opportunities for market expansion, though they often contend with nascent infrastructure, political instability, and lower adoption rates of advanced logistics technologies.

- North America: Dominant market, driven by robust e-commerce growth, expansive manufacturing, and a mature logistics infrastructure. Faces challenges like driver shortages and high labor costs. The United States accounts for the largest share within this region.

- Europe: Characterized by a highly competitive market, intricate cross-border logistics, and a strong focus on sustainability. Demand is high from manufacturing and retail sectors, with Germany, France, and the UK as key contributors.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid urbanization, booming e-commerce, and increasing industrialization in countries like China, India, Japan, and Australia. Infrastructure development and supply chain modernization are ongoing.

- Latin America: Emerging market with growing demand for LTL services, particularly in Brazil and Mexico, fueled by increasing trade and consumer spending. Faces challenges related to infrastructure, security, and economic volatility.

- Middle East & Africa (MEA): Gradually developing LTL market, supported by investments in logistics hubs (e.g., UAE, Saudi Arabia) and increasing e-commerce adoption. Growth is steady but often impacted by geopolitical factors and varying economic conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Less than Truckload Market.- Old Dominion Freight Line

- XPO Logistics

- Saia

- ArcBest

- TFI International

- Estes Express Lines

- R+L Carriers

- Southeastern Freight Lines

- FedEx Freight

- Averitt Express

- Pitt Ohio

- Dayton Freight

- Ward Transport

- USF Holland

- New Penn

- YRC Freight

- Central Transport

- AAA Cooper Transportation

- Reddaway

- Wilson Trucking Corporation

Frequently Asked Questions

Analyze common user questions about the Less than Truckload market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Less than Truckload (LTL) shipping?

LTL shipping involves transporting relatively small freight, generally weighing between 150 to 15,000 pounds. Multiple shippers share space on a single truck, making it a cost-effective option for shipments too large for parcel services but not big enough to fill an entire truck.

Why should businesses choose LTL over other shipping methods?

Businesses choose LTL for its cost efficiency, as they only pay for the space their freight occupies. It also offers flexibility for smaller, more frequent shipments, reduces warehousing needs, and minimizes environmental impact by consolidating loads.

What factors influence LTL freight rates?

LTL rates are primarily influenced by freight class (density, stowability, handling, liability), weight, distance, and any accessorial services required (e.g., liftgate, residential delivery, limited access). Market demand and fuel surcharges also play a significant role.

How is technology improving LTL logistics?

Technology is enhancing LTL through Transportation Management Systems (TMS) for optimization, real-time tracking for visibility, Artificial Intelligence (AI) for predictive analytics and route planning, and automation for operational efficiency, leading to faster and more reliable services.

What is the future outlook for the Less than Truckload market?

The LTL market is projected for steady growth, driven by continued e-commerce expansion and demand for flexible, cost-effective shipping. Future success will depend on technological adoption, network optimization, and adapting to evolving customer expectations for speed and transparency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted