LEO Satellite Market

LEO Satellite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710087 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

LEO Satellite Market Size

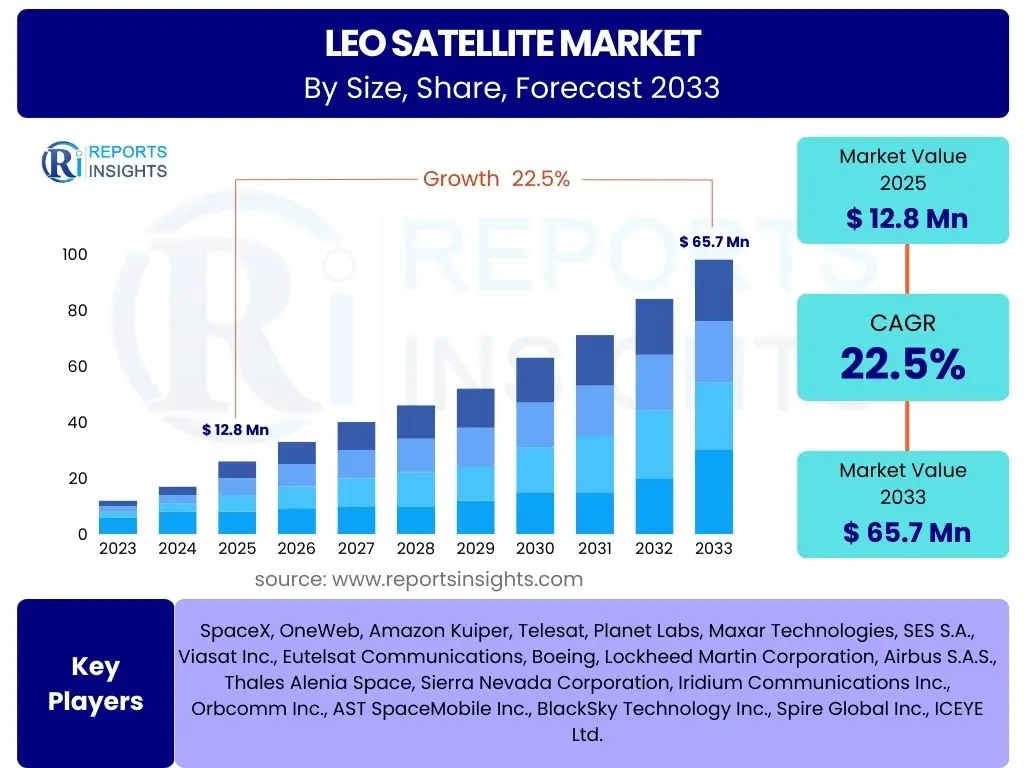

According to Reports Insights Consulting Pvt Ltd, The LEO Satellite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 65.7 Billion by the end of the forecast period in 2033.

The burgeoning demand for global high-speed, low-latency internet connectivity, especially in remote and underserved areas, is a primary catalyst for this robust growth. LEO satellite constellations offer a viable and often superior alternative to traditional terrestrial infrastructure, driving significant investment and deployment initiatives worldwide. This includes expanding broadband access, enabling advanced Internet of Things (IoT) applications, and supporting next-generation communication standards.

Furthermore, the decreasing costs associated with satellite manufacturing and launch services, coupled with advancements in miniaturization and reusability, are making LEO satellite deployment more economically feasible. These factors are attracting a diverse range of players, from established aerospace giants to innovative startups, fostering a highly competitive and dynamic market landscape that is set to redefine global communication and observation capabilities over the next decade.

Key LEO Satellite Market Trends & Insights

The LEO Satellite market is experiencing transformative trends driven by the imperative for ubiquitous global connectivity and the increasing demand for high-resolution Earth observation data. Users frequently inquire about the primary technological and commercial developments shaping this sector, focusing on the evolution of satellite design, operational models, and application diversification. Key themes emerging from these inquiries include the shift towards mega-constellations, the integration of advanced data processing capabilities, and the growing importance of satellite-enabled services in various industries.

Another significant area of interest revolves around the economic viability and scalability of LEO systems. The market is seeing a sustained effort towards reducing the cost per bit and per image, making satellite services more accessible and competitive. This trend is fueled by innovations in manufacturing processes, such as mass production techniques for satellites, and the proliferation of more cost-effective and frequent launch options. The emphasis is on building resilient, high-capacity networks that can support diverse applications, from consumer broadband to sophisticated governmental operations.

Moreover, the strategic importance of LEO satellites in national security and defense continues to grow, prompting increased investment from government entities. This includes the development of secure communication links, enhanced intelligence, surveillance, and reconnaissance (ISR) capabilities, and resilient positioning, navigation, and timing (PNT) services. The confluence of these technological advancements, economic drivers, and strategic imperatives underscores a dynamic market poised for substantial expansion and innovation.

- Proliferation of Mega-Constellations for Global Broadband: Large-scale deployment of thousands of LEO satellites aiming to provide high-speed, low-latency internet access worldwide.

- Miniaturization and Standardization of Satellites: Development of smaller, more cost-effective satellites enabled by advanced component integration and modular designs.

- Increased Demand for Earth Observation and Remote Sensing: Growing applications in environmental monitoring, climate change tracking, precision agriculture, and disaster management.

- Advancements in On-orbit Processing and AI Integration: Shifting data processing capabilities to the satellites themselves to reduce latency and bandwidth requirements.

- Growing Role of LEO Satellites in 5G Backhaul and IoT Connectivity: Enabling pervasive connectivity for remote IoT devices and extending the reach of 5G networks to underserved areas.

- Development of Direct-to-Device (DtD) Communication Capabilities: Enabling direct satellite connectivity to standard smartphones and other mobile devices.

AI Impact Analysis on LEO Satellite

The integration of Artificial Intelligence (AI) across the LEO satellite ecosystem is a frequent topic of user inquiry, highlighting expectations for enhanced operational efficiency, data utility, and autonomous capabilities. Users are particularly interested in how AI can address the complexities of managing vast constellations, processing immense volumes of data, and ensuring the longevity and reliability of satellite assets. AI's role in optimizing resource allocation, predictive maintenance, and real-time decision-making for constellation management is consistently a central point of discussion.

Furthermore, the application of AI extends significantly into the realm of data processing and analytics, especially for Earth observation missions. With LEO satellites generating petabytes of imagery and sensor data daily, AI-powered algorithms are crucial for automated feature extraction, anomaly detection, and rapid insights generation. This capability transforms raw data into actionable intelligence for various sectors, from environmental monitoring to defense, allowing for quicker responses and more informed strategic planning.

The future impact of AI on LEO satellites is also seen in the development of more autonomous and resilient satellite systems. AI can enable satellites to self-diagnose issues, autonomously navigate to avoid debris, and even reconfigure payloads to adapt to changing mission requirements or environmental conditions. This shift towards greater autonomy is expected to reduce operational costs, extend mission lifespans, and enhance the overall robustness of LEO networks, addressing key concerns about the scalability and sustainability of these advanced space systems.

- Enhanced Constellation Management: AI optimizes satellite orbits, collision avoidance, and resource allocation for large LEO constellations, improving network efficiency and longevity.

- Advanced Data Processing and Analytics: AI algorithms accelerate the analysis of vast amounts of Earth observation data, enabling real-time insights for various applications like weather forecasting, agriculture, and defense.

- Predictive Maintenance and Anomaly Detection: AI monitors satellite health, predicts potential failures, and identifies anomalies, reducing downtime and extending operational lifespans.

- Autonomous Operations: AI enables satellites to perform tasks such as autonomous navigation, self-healing, and adaptive payload management with minimal human intervention.

- Optimized Communication Links: AI-driven beamforming and routing optimize signal transmission, enhancing bandwidth utilization and network performance.

- Cybersecurity Enhancements: AI strengthens security protocols against cyber threats targeting LEO satellite networks and ground infrastructure.

Key Takeaways LEO Satellite Market Size & Forecast

User queries regarding the LEO Satellite market size and forecast consistently seek a concise understanding of the market's trajectory, its underlying growth drivers, and the most significant implications for stakeholders. The overarching takeaway is the market's exceptionally high growth potential, fueled by an insatiable global demand for connectivity and an accelerating pace of technological innovation. This expansion is not merely incremental but represents a fundamental shift in how global communication and Earth observation services are delivered.

A critical insight is the transformational impact of reduced costs and increased accessibility. The ability to deploy large constellations of smaller, more affordable satellites has democratized access to space-based services, moving them from niche government or large enterprise applications to broader commercial and consumer markets. This shift is creating new business models and fostering intense competition, driving down service costs and expanding market reach globally.

Ultimately, the LEO satellite market is poised to become a foundational component of the global digital infrastructure, enabling previously unimaginable levels of connectivity and data insights. Its rapid growth signifies not just a technological advancement, but a strategic imperative for nations and corporations seeking to leverage the full potential of a connected world, making it a pivotal area for investment and development over the coming decade.

- Robust Market Expansion: The LEO satellite market is poised for significant growth, projected to reach USD 65.7 Billion by 2033, driven by increasing demand for global connectivity.

- Connectivityเป็น Catalyst: Universal access to high-speed, low-latency internet, particularly in remote areas, is the primary growth driver, revolutionizing telecommunications.

- Technological Innovation and Cost Reduction: Advancements in miniaturization, mass production, and reusable launch vehicles are making LEO satellite deployment more economical and scalable.

- Diversification of Applications: Beyond broadband, LEO satellites are critical for Earth observation, IoT, defense, and scientific research, expanding their market utility.

- Strategic Global Importance: LEO constellations are becoming vital for national security, economic development, and bridging the digital divide, attracting substantial government and private investment.

LEO Satellite Market Drivers Analysis

The LEO satellite market is propelled by a confluence of powerful drivers that underscore its increasing strategic and commercial importance. The foundational driver is the escalating global demand for ubiquitous high-speed and low-latency internet connectivity, particularly in regions where terrestrial infrastructure is underdeveloped or economically unviable. LEO constellations offer a compelling solution to bridge this digital divide, enabling access to broadband services for billions.

Technological advancements also play a crucial role. Innovations in satellite miniaturization, payload capabilities, and manufacturing processes have significantly reduced the cost and complexity of building and deploying LEO satellites. Concurrently, the emergence of more frequent and cost-effective launch options, including reusable rockets and ride-share services, has made it feasible to deploy and replenish large constellations, accelerating market growth and lowering barriers to entry for new players.

Furthermore, the expanding range of applications beyond traditional communication, such as advanced Earth observation, precision agriculture, maritime and aviation tracking, and critical infrastructure monitoring, is creating new revenue streams and driving demand across diverse industry verticals. Government and defense sectors are also increasing their investment in LEO capabilities for secure communications, surveillance, and resilient positioning, further solidifying the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Global Broadband Connectivity | +8.0-10.0% | Global, particularly Emerging Economies (Africa, Latin America, Southeast Asia) | Long-term (2025-2033) |

| Technological Advancements in Satellite Miniaturization & Manufacturing | +5.0-7.0% | Global, especially North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Declining Satellite Launch Costs & Reusability | +4.0-6.0% | Global, especially US (SpaceX), China, Europe | Mid to Long-term (2025-2033) |

| Growing Adoption of LEO Satellites for Earth Observation & IoT | +3.0-5.0% | Global, particularly North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Government Initiatives & Defense Spending on Space-Based Assets | +2.0-4.0% | North America (US), Europe, China, India | Long-term (2025-2033) |

LEO Satellite Market Restraints Analysis

Despite its significant growth potential, the LEO satellite market faces several notable restraints that could temper its expansion. One of the most pressing concerns is the exponential increase in space debris. The deployment of mega-constellations significantly raises the risk of collisions, which can generate more debris and endanger operational satellites, leading to higher insurance costs and potential regulatory interventions. This challenge necessitates robust debris mitigation strategies and international cooperation, which can be complex and time-consuming.

Another substantial restraint is the high initial capital investment required for developing, launching, and maintaining large LEO satellite constellations and their associated ground infrastructure. While per-satellite costs are decreasing, the sheer scale of these projects demands billions of dollars in funding, which can be a significant barrier for new entrants and can strain even established players. The financial risk is compounded by the long payback periods and the need for continuous technological upgrades to remain competitive.

Furthermore, regulatory complexities and spectrum allocation issues pose ongoing challenges. The assignment of radio frequencies for satellite communication is governed by international bodies, and with more players entering the LEO space, competition for limited spectrum resources intensifies. Navigating diverse national and international regulatory frameworks for satellite operations, data privacy, and intellectual property adds layers of complexity that can slow down deployment and market entry. These restraints require sustained attention and innovative solutions to ensure the market's sustainable growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Concerns Over Space Debris & Orbital Congestion | -3.0-4.5% | Global, affecting all regions with LEO satellite deployments | Mid to Long-term (2025-2033) |

| High Initial Capital Investment & Operating Costs | -2.5-4.0% | Global, impacting new entrants and smaller players | Long-term (2025-2033) |

| Regulatory Hurdles & Spectrum Allocation Challenges | -2.0-3.5% | Global, particularly in regions with complex regulatory environments | Mid-term (2025-2030) |

| Cybersecurity Threats & Data Security Concerns | -1.5-3.0% | Global, impacting critical infrastructure and data-sensitive applications | Long-term (2025-2033) |

| Technical Complexity in Ground Segment Infrastructure Development | -1.0-2.5% | Global, especially regions with less developed ground infrastructure | Mid-term (2025-2030) |

LEO Satellite Market Opportunities Analysis

The LEO satellite market is rich with opportunities, driven by unmet global demand and ongoing technological innovation. A primary opportunity lies in serving the vast, untapped markets for internet connectivity in rural and remote areas globally. These regions, often underserved by traditional terrestrial infrastructure, represent a significant customer base for LEO satellite broadband services, offering a chance to bridge the digital divide and foster economic development. The capability to provide seamless, high-speed access to remote communities, maritime vessels, and aircraft opens up new frontiers for service providers.

Another substantial opportunity is the integration of LEO satellite networks with emerging technologies such as 5G and future 6G systems, as well as the rapidly expanding Internet of Things (IoT) ecosystem. LEO satellites can provide essential backhaul for 5G networks in areas lacking fiber connectivity and enable pervasive connectivity for billions of IoT devices worldwide, from smart agriculture sensors to environmental monitoring equipment. This synergy positions LEO systems as critical enablers for the next generation of global digital infrastructure.

Furthermore, the development of direct-to-device (DtD) communication capabilities, allowing standard smartphones and other mobile devices to connect directly to LEO satellites, presents a revolutionary market opportunity. This innovation could eliminate the need for specialized ground terminals for basic connectivity, significantly expanding the addressable market and transforming personal communication and emergency services. Additionally, the increasing focus on national security and defense applications, including enhanced intelligence, surveillance, and reconnaissance (ISR), and resilient communication for military operations, offers lucrative long-term contracts and strategic partnerships for LEO satellite providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding Broadband Connectivity in Rural & Remote Areas | +6.0-8.0% | Global, particularly Africa, Latin America, Southeast Asia, Arctic regions | Long-term (2025-2033) |

| Integration with 5G & Future 6G Networks for Backhaul | +5.0-7.0% | Global, especially North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Growth in Direct-to-Device (DtD) Satellite Communication | +4.0-6.0% | Global, high adoption potential in developed markets first | Mid to Long-term (2027-2033) |

| Development of Specialized Services for IoT & M2M Communication | +3.0-5.0% | Global, strong growth in industrial, agriculture, logistics sectors | Mid-term (2025-2030) |

| Increasing Demand for High-Resolution Earth Observation Data | +2.0-4.0% | Global, especially government, environmental, commercial sectors | Mid-term (2025-2030) |

LEO Satellite Market Challenges Impact Analysis

The LEO satellite market, while promising, is not without its significant challenges that could impede its projected growth and operational efficiency. One major challenge is the intense and escalating competition among a growing number of players. With numerous companies vying for market share in both satellite manufacturing and service provision, there is constant pressure on pricing, innovation, and speed of deployment. This competitive landscape can lead to market saturation in certain segments, making it difficult for some operators to achieve profitability or differentiate their offerings effectively.

Another critical challenge lies in managing the technical complexities associated with deploying and maintaining large-scale LEO constellations. This includes ensuring the reliability and longevity of thousands of satellites in a harsh space environment, developing sophisticated ground infrastructure capable of managing massive data traffic, and seamlessly integrating satellite services with existing terrestrial networks. Technical failures, software glitches, or unexpected operational issues can significantly impact service quality and incur substantial financial losses, demanding continuous research and development efforts.

Moreover, the evolving regulatory environment and geopolitical considerations present ongoing hurdles. International agreements on spectrum use and orbital slots are constantly being debated and revised, creating uncertainty for operators. National security concerns and export controls on satellite technology can also restrict market access and collaborations. The need to navigate these complex technical, commercial, and political landscapes requires substantial expertise, resources, and adaptability from market participants to sustain growth and mitigate risks effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition Among Multiple LEO Constellation Operators | -3.5-5.0% | Global, particularly North America, Europe, China | Long-term (2025-2033) |

| Complexity of Ground Infrastructure & Interoperability | -2.0-3.5% | Global, higher impact in regions with less developed digital infrastructure | Mid-term (2025-2030) |

| Cybersecurity Vulnerabilities & Threat Landscape | -1.5-3.0% | Global, impacting all sectors utilizing LEO services | Long-term (2025-2033) |

| Maintaining Satellite Reliability & Longevity in Harsh Environments | -1.0-2.5% | Global, affecting all LEO operators | Mid to Long-term (2025-2033) |

| Talent Shortage in Aerospace Engineering & Satellite Technology | -0.5-1.5% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

LEO Satellite Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global LEO Satellite market, offering granular insights into market dynamics, segmentation, regional trends, and competitive landscapes. The scope extends beyond historical data to provide robust forecasts, enabling stakeholders to make informed strategic decisions. The report addresses key industry trends, drivers, restraints, opportunities, and challenges, synthesizing complex market information into actionable intelligence for investors, manufacturers, service providers, and end-users.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 65.7 Billion |

| Growth Rate | 22.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SpaceX, OneWeb, Amazon Kuiper, Telesat, Planet Labs, Maxar Technologies, SES S.A., Viasat Inc., Eutelsat Communications, Boeing, Lockheed Martin Corporation, Airbus S.A.S., Thales Alenia Space, Sierra Nevada Corporation, Iridium Communications Inc., Orbcomm Inc., AST SpaceMobile Inc., BlackSky Technology Inc., Spire Global Inc., ICEYE Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LEO satellite market is meticulously segmented across various critical parameters to provide a detailed understanding of its diverse components and growth avenues. This segmentation allows for a granular analysis of how different technological, application, and end-use categories contribute to the overall market landscape and where future growth is most likely to originate. By dissecting the market into these specialized areas, stakeholders can identify niche opportunities and tailor their strategies to specific market demands, optimizing resource allocation and maximizing return on investment.

The segmentation also reflects the dynamic evolution of the LEO satellite ecosystem, from the types and sizes of satellites being deployed to the diverse services they enable. Understanding these categories is crucial for comprehending the competitive environment, evaluating technological maturity, and forecasting future market shifts. This detailed breakdown ensures that all facets of the LEO satellite industry, from hardware manufacturers to service providers, are comprehensively covered, offering a holistic view of the market's structure and potential.

- By Type: Mini/Micro-satellites, Small Satellites (100-500 kg), Medium Satellites (500-1000 kg), Large Satellites (>1000 kg)

- By Application: Communication and Internet Services, Earth Observation and Remote Sensing, Navigation and Global Positioning, Scientific Research and Exploration, Defense and Security

- By End-Use Industry: Commercial, Government & Military, Maritime, Aviation, Academic & Research

- By Offering: Hardware (Satellite Platforms, Payload, Ground Equipment), Services (Launch Services, Satellite Operations, Data Processing, Managed Services)

- By Frequency Band: Ku-band, Ka-band, S-band, C-band, X-band, V-band, Q-band

- By Orbit Altitude: Very Low Earth Orbit (VLEO), Low Earth Orbit (LEO)

- By Payload Type: Communication Transponders, Optical Instruments, Radar, GPS/GNSS Receivers, Scientific Instruments

- By Satellite Mass: Picosatellite (0.1-1 kg), Nanosatellite (1-10 kg), Microsatellite (10-100 kg), Minisatellite (100-500 kg)

Regional Highlights

- North America: Dominates the LEO satellite market due to significant investments from private companies (e.g., SpaceX, Amazon Kuiper) and government agencies (e.g., DoD, NASA). Strong R&D capabilities, advanced manufacturing, and a robust ecosystem of startups and established players drive innovation and deployment.

- Europe: A key player with substantial public and private investments in LEO constellations (e.g., OneWeb, Eutelsat) for broadband connectivity and Earth observation. European Space Agency (ESA) initiatives and national programs foster technological development and market expansion.

- Asia Pacific (APAC): Emerging as a high-growth region driven by increasing demand for connectivity in underserved areas, government-backed space programs (e.g., China, India, Japan), and rapid digital transformation. Countries like China and India are developing their own LEO constellations for strategic and commercial purposes.

- Latin America: Expected to witness significant growth in LEO satellite adoption, primarily for bridging the digital divide and enabling internet access in remote regions. Demand for satellite-based agricultural monitoring and disaster management services is also rising.

- Middle East and Africa (MEA): A high potential market due to extensive geographical areas with limited terrestrial infrastructure, driving demand for LEO-based broadband and communication services. Government interest in enhancing national security and economic development through space technology is also a key factor.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LEO Satellite Market.- SpaceX

- OneWeb

- Amazon Kuiper

- Telesat

- Planet Labs

- Maxar Technologies

- SES S.A.

- Viasat Inc.

- Eutelsat Communications

- Boeing

- Lockheed Martin Corporation

- Airbus S.A.S.

- Thales Alenia Space

- Sierra Nevada Corporation

- Iridium Communications Inc.

- Orbcomm Inc.

- AST SpaceMobile Inc.

- BlackSky Technology Inc.

- Spire Global Inc.

- ICEYE Ltd.

Frequently Asked Questions

What is a LEO satellite?

A Low Earth Orbit (LEO) satellite is a spacecraft that orbits the Earth at an altitude typically between 160 km and 2,000 km. These satellites are crucial for providing low-latency, high-speed communication services and high-resolution Earth observation data, due to their proximity to the Earth's surface.

What are the main applications of LEO satellites?

LEO satellites are primarily used for global broadband internet connectivity, enhancing 5G networks, enabling the Internet of Things (IoT), Earth observation for environmental monitoring and remote sensing, scientific research, and defense and security applications like intelligence gathering.

How fast is the LEO satellite market growing?

The LEO Satellite market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033, reaching an estimated USD 65.7 Billion by the end of the forecast period.

What are the primary challenges facing the LEO satellite market?

Key challenges include managing the increasing amount of space debris, navigating complex regulatory frameworks for spectrum allocation, mitigating high initial capital investment requirements, and addressing intense competition among a growing number of operators.

Which regions are key players in the LEO satellite market?

North America currently leads the market due to significant private and government investment. Europe and Asia Pacific (especially China and India) are also major and rapidly growing regions, driven by their own space programs and increasing demand for satellite services.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted