Lead Acid Battery Market

Lead Acid Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702502 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Lead Acid Battery Market Size

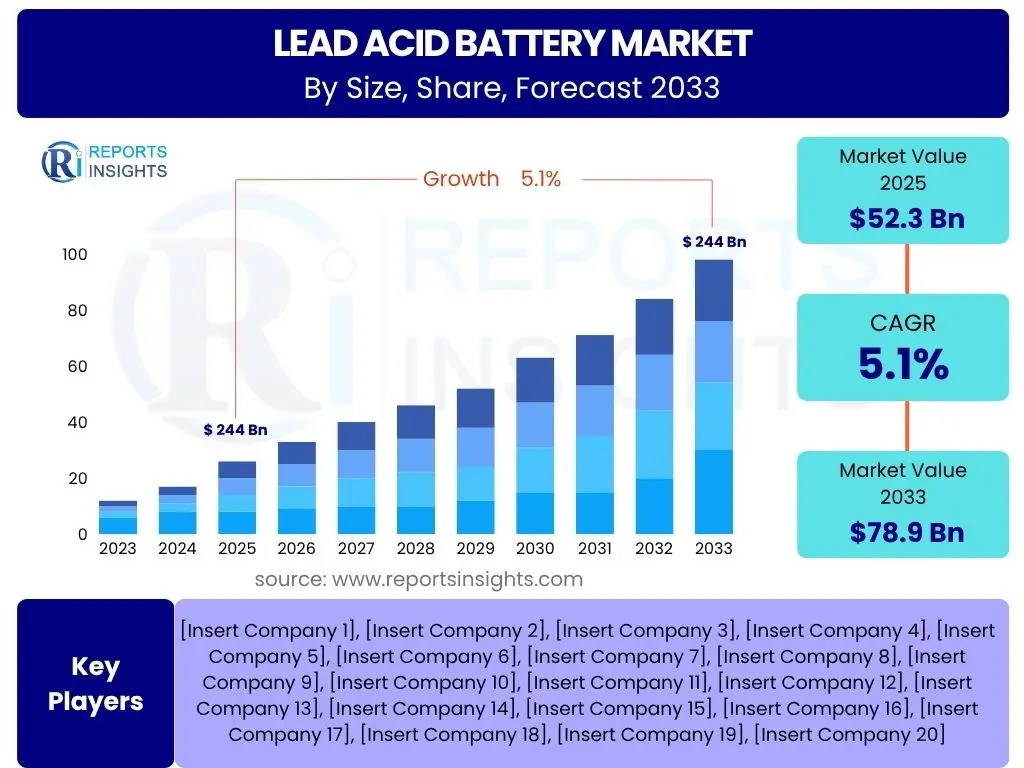

According to Reports Insights Consulting Pvt Ltd, The Lead Acid Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.1% between 2025 and 2033. The market is estimated at USD 52.3 billion in 2025 and is projected to reach USD 78.9 billion by the end of the forecast period in 2033.

Key Lead Acid Battery Market Trends & Insights

The Lead Acid Battery market is undergoing a transformative period, driven by evolving application demands and a heightened focus on sustainability. Common user inquiries often revolve around the longevity of this mature technology amidst newer alternatives, and how it continues to find relevance. Key trends indicate a significant push towards enhancing performance characteristics, such as energy density and cycle life, particularly for stationary applications like uninterruptible power supplies (UPS) and renewable energy storage. Furthermore, the market is witnessing innovation in battery designs to improve efficiency and reduce environmental impact, alongside a steady demand from its traditional automotive starting, lighting, and ignition (SLI) segment.

There is also a growing emphasis on advanced manufacturing techniques and smart monitoring systems that extend battery life and predict maintenance needs, addressing concerns about reliability and operational costs. While facing competition from emerging technologies, the lead acid battery maintains its competitive edge due to its established infrastructure, robust performance in specific conditions, and lower cost per watt-hour. The convergence of these factors suggests a market that, while mature, continues to adapt and innovate within its established niches and expand into new ones, particularly in sectors prioritizing cost-effectiveness and proven reliability.

- Increased adoption in stationary energy storage for renewable grids.

- Rising demand from the automotive sector for SLI and certain hybrid applications.

- Technological advancements improving battery lifespan and efficiency (e.g., carbon additives).

- Focus on circular economy principles and enhanced recycling processes.

- Development of sealed, maintenance-free VRLA (Valve Regulated Lead Acid) batteries for diverse applications.

AI Impact Analysis on Lead Acid Battery

User questions frequently probe the extent to which artificial intelligence (AI) can revolutionize a traditionally robust but low-tech industry like lead acid battery manufacturing. The consensus indicates that AI is increasingly pivotal in optimizing various stages of the battery lifecycle, from design and manufacturing to operational management and recycling. In manufacturing, AI-driven analytics can significantly enhance process control, leading to improved consistency, reduced defects, and increased production efficiency. This includes predictive maintenance of machinery, optimization of material mixing, and real-time quality assurance, which directly addresses concerns about production costs and battery reliability.

Beyond manufacturing, AI contributes to predictive analytics for battery health monitoring in deployed systems, extending operational lifespan and reducing unexpected failures. This is particularly valuable in critical applications like UPS and telecommunications. Furthermore, AI can accelerate research and development by simulating new material compositions and electrode designs, shortening the innovation cycle for more efficient and durable batteries. In the realm of sustainability, AI algorithms can optimize recycling processes, improving the recovery rates of lead and other valuable materials, thereby aligning with environmental regulations and resource efficiency goals. The integration of AI positions the lead acid battery industry to be more competitive, sustainable, and technologically advanced.

- AI-driven optimization of manufacturing processes for improved efficiency and quality control.

- Predictive maintenance for battery systems, enhancing reliability and extending service life.

- Accelerated research and development through AI-enabled material design and performance simulation.

- Enhanced supply chain management and logistics optimization using AI analytics.

- Improved recycling efficiency and resource recovery through AI-powered sorting and processing.

Key Takeaways Lead Acid Battery Market Size & Forecast

Analysis of common user inquiries regarding the Lead Acid Battery market size and forecast consistently points to an underlying curiosity about the longevity and growth trajectory of this established technology amidst an evolving energy landscape. A key takeaway is the market's enduring relevance, supported by its cost-effectiveness, proven reliability, and widespread existing infrastructure, particularly in automotive SLI, UPS, and various industrial applications. While newer battery chemistries garner significant attention, the lead acid market demonstrates steady, albeit moderate, growth, largely driven by increasing vehicle parc globally, expanding telecom infrastructure, and the growing need for reliable backup power solutions in developing economies. The forecast indicates continued expansion, albeit with increasing emphasis on performance improvements and sustainable practices.

Another crucial insight is the strategic pivot towards high-value applications and advancements in VRLA and enhanced flooded battery (EFB) technologies. Market players are focusing on product innovation to improve energy efficiency, cycle life, and thermal management, which directly addresses user concerns about performance limitations. The robust demand in emerging markets, coupled with the critical role lead acid batteries play in grid stabilization and renewable energy integration, reinforces its foundational position in the energy storage ecosystem. These factors collectively affirm the market's resilient growth and its continued importance in diverse sectors.

- Consistent demand from the automotive SLI sector remains a primary growth driver.

- Significant growth opportunities exist in stationary energy storage and UPS applications.

- Technological refinements, particularly in VRLA batteries, are enhancing market competitiveness.

- Emerging economies in Asia Pacific and Africa are key regions for market expansion.

- The market is adapting through improved recycling and manufacturing processes to meet environmental standards.

Lead Acid Battery Market Drivers Analysis

The Lead Acid Battery market is propelled by several key drivers that underscore its sustained relevance and growth despite the emergence of alternative battery technologies. A primary driver is the robust and continuously expanding automotive sector globally, where lead acid batteries remain the standard for Starting, Lighting, and Ignition (SLI) applications due to their cost-effectiveness and high cranking power. This segment benefits from increasing vehicle production and the vast aftermarket for replacement batteries, ensuring a constant demand baseline. The inherent reliability and relatively low manufacturing cost of lead acid batteries make them an economically viable choice for mass-market vehicle segments and heavy-duty vehicles, including trucks and buses, which continue to drive significant volumes.

Furthermore, the escalating demand for uninterruptible power supplies (UPS) and industrial motive power applications significantly contributes to market expansion. Industries such as data centers, telecommunications, and manufacturing rely heavily on lead acid batteries for reliable backup power and to operate electric forklifts and other material handling equipment. Their ability to deliver high currents for short durations, coupled with robust performance in diverse temperature conditions, positions them as a preferred choice in these critical applications. The rapid industrialization and digitalization in emerging economies are particularly boosting this segment, as the need for stable power grids and continuous operations grows exponentially.

The burgeoning renewable energy sector, specifically solar and wind power installations, also presents a substantial growth avenue. While lithium-ion batteries often capture headlines for large-scale grid storage, lead acid batteries offer a more economical solution for residential and small to medium-scale off-grid energy storage systems, especially in regions with limited access to consistent grid power. Their deep cycle capabilities in specific variants make them suitable for storing intermittent renewable energy, providing a cost-efficient and dependable energy buffer. This confluence of factors, from established automotive needs to evolving industrial and renewable energy demands, collectively underscores the dynamic drivers fueling the lead acid battery market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive SLI Demand | +1.5% | Global, especially Asia Pacific & North America | 2025-2033 |

| Increasing UPS & Industrial Applications | +1.2% | Global, strong in Asia Pacific & Europe | 2025-2033 |

| Expansion of Renewable Energy Storage | +0.8% | Developing Economies, Remote Areas | 2026-2033 |

| Cost-effectiveness & Reliability | +1.0% | Global | 2025-2033 |

Lead Acid Battery Market Restraints Analysis

Despite its enduring utility, the Lead Acid Battery market faces several significant restraints that temper its growth potential and encourage the adoption of alternative technologies. A primary challenge stems from the intense competition posed by advanced battery chemistries, particularly lithium-ion batteries. Lithium-ion technology offers superior energy density, longer cycle life, lighter weight, and faster charging capabilities, making it increasingly preferred for electric vehicles, portable electronics, and even grid-scale energy storage where these attributes are critical. This technological displacement limits the expansion of lead acid batteries into high-growth, performance-driven applications, relegating them to niches where cost-effectiveness and robustness are prioritized over advanced performance metrics.

Environmental concerns and stringent regulations regarding lead content and disposal also pose considerable hurdles. Lead is a toxic heavy metal, and improper disposal of lead acid batteries can lead to severe environmental pollution and health hazards. Consequently, governments worldwide are implementing stricter recycling mandates and environmental protection laws, increasing the operational costs for manufacturers and recyclers. While the industry has established robust recycling programs (boasting one of the highest recycling rates for any product), the perception of lead as an environmental hazard and the continuous regulatory pressure can hinder market acceptance and innovation, especially in environmentally conscious regions like Europe and North America.

Furthermore, inherent limitations such as lower energy density and shorter cycle life compared to newer alternatives, along with their larger size and heavier weight, restrict their applicability in space-constrained or weight-sensitive environments. These physical constraints make them less suitable for the evolving demands of compact electronic devices or long-range electric vehicles. The constant need for maintenance in certain traditional flooded lead acid variants also adds to the total cost of ownership and operational inconvenience for end-users. These combined factors present a complex challenge for the market, requiring continuous innovation to overcome inherent limitations and address environmental perceptions effectively.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Lithium-Ion Batteries | -1.8% | Global, particularly North America & Europe | 2025-2033 |

| Environmental Regulations & Disposal Concerns | -0.9% | Europe, North America, developing Asia Pacific | 2025-2033 |

| Lower Energy Density & Heavier Weight | -0.7% | Global, impacting new applications | 2025-2033 |

| Raw Material Price Volatility | -0.5% | Global | 2025-2030 |

Lead Acid Battery Market Opportunities Analysis

Despite facing competition and regulatory pressures, the Lead Acid Battery market is ripe with opportunities driven by innovation, strategic niche expansion, and the circular economy. One significant opportunity lies in the continuous advancement of Valve Regulated Lead Acid (VRLA) battery technology, specifically Absorbent Glass Mat (AGM) and Gel batteries. These sealed, maintenance-free variants offer improved cycle life, better performance in extreme temperatures, and enhanced safety features compared to traditional flooded batteries. This makes them increasingly appealing for critical applications like telecommunications base stations, backup power for data centers, and specific automotive start-stop systems, allowing lead acid batteries to retain and expand their market share in segments requiring reliability without extensive maintenance.

The burgeoning market for renewable energy integration, particularly for off-grid and micro-grid solutions in developing economies, presents another substantial opportunity. In regions where grid infrastructure is nascent or unreliable, lead acid batteries provide a cost-effective and robust solution for storing solar and wind energy, powering homes, small businesses, and community facilities. Their established manufacturing base and lower initial cost per kWh make them highly accessible compared to higher-cost alternatives. This aligns with global efforts to expand energy access and promote sustainable development in underserved areas, fostering new demand centers for lead acid technology.

Furthermore, the focus on circular economy principles and advanced recycling technologies offers both an opportunity for compliance and a competitive advantage. The lead acid battery industry already boasts impressive recycling rates, but continuous investment in more efficient and environmentally sound recycling processes can further enhance its sustainability credentials. This not only mitigates environmental concerns but also secures raw material supply chains and potentially reduces production costs by utilizing recycled lead. Expanding into niche applications such as golf carts, electric wheelchairs, and forklifts, where their robustness and cost-effectiveness are paramount, also provides stable, high-value growth paths. These combined factors highlight the market's capacity for strategic growth and adaptation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in VRLA (AGM/Gel) Technologies | +1.3% | Global, particularly North America & Europe | 2025-2033 |

| Growth in Off-Grid & Micro-Grid Renewable Energy Storage | +1.0% | Asia Pacific, Africa, Latin America | 2026-2033 |

| Circular Economy & Enhanced Recycling Initiatives | +0.7% | Global, driven by regulatory support | 2027-2033 |

| Expansion into Niche Motive Power Applications | +0.8% | Global, mature and emerging markets | 2025-2033 |

Lead Acid Battery Market Challenges Impact Analysis

The Lead Acid Battery market, while resilient, faces several inherent challenges that influence its growth trajectory and competitive standing. One significant challenge is the volatility of raw material prices, particularly lead. The global price of lead can fluctuate significantly due to mining output, geopolitical factors, and demand from various industries, directly impacting the manufacturing costs of lead acid batteries. Such price instability makes it difficult for manufacturers to maintain stable profit margins and can lead to increased product prices, potentially making them less competitive against alternative battery technologies whose raw material costs might be more stable or strategically managed. This creates uncertainty in market planning and investment.

Another major challenge is the persistent issue of disposal and recycling complexities, despite the industry's high recycling rates. While lead acid batteries are highly recyclable, ensuring proper collection, transportation, and processing of spent batteries remains a logistical and environmental hurdle, particularly in regions with less developed waste management infrastructures. The risk of lead contamination during improper disposal or processing poses environmental and health risks, leading to public scrutiny and stricter regulatory oversight. Although the industry has invested heavily in closed-loop recycling systems, the ongoing management of these complexities adds operational costs and regulatory burdens that can impede market expansion.

Furthermore, the rapid pace of innovation in competing battery technologies, such as various lithium-ion chemistries, solid-state batteries, and flow batteries, presents a continuous technological obsolescence challenge. While lead acid batteries offer robust performance for specific applications, their lower energy density and shorter cycle life compared to these advanced alternatives mean they are consistently evaluated for replacement in evolving applications. This forces lead acid battery manufacturers to invest in continuous, albeit incremental, improvements to their technology to remain viable, often competing on cost and reliability rather than cutting-edge performance. Addressing these challenges requires strategic investments in raw material procurement, recycling infrastructure, and targeted R&D to maintain market relevance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility (Lead) | -0.6% | Global | 2025-2030 |

| Disposal & Recycling Logistics Complexity | -0.4% | Developing Regions, Fragmented Markets | 2025-2033 |

| Technological Obsolescence from Alternatives | -0.8% | Global, impacting high-growth segments | 2025-2033 |

| Stringent Environmental & Safety Regulations | -0.5% | Europe, North America, parts of Asia | 2025-2033 |

Lead Acid Battery Market - Updated Report Scope

This report offers an in-depth analysis of the global Lead Acid Battery market, providing a comprehensive overview of market dynamics, segmentation, regional insights, and competitive landscape. It delves into the historical performance of the market, presents current trends, and projects future growth trajectories, considering various macroeconomic and industry-specific factors. The scope encompasses detailed analysis of market drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 52.3 Billion |

| Market Forecast in 2033 | USD 78.9 Billion |

| Growth Rate | 5.1% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | [Insert Company 1], [Insert Company 2], [Insert Company 3], [Insert Company 4], [Insert Company 5], [Insert Company 6], [Insert Company 7], [Insert Company 8], [Insert Company 9], [Insert Company 10], [Insert Company 11], [Insert Company 12], [Insert Company 13], [Insert Company 14], [Insert Company 15], [Insert Company 16], [Insert Company 17], [Insert Company 18], [Insert Company 19], [Insert Company 20] |

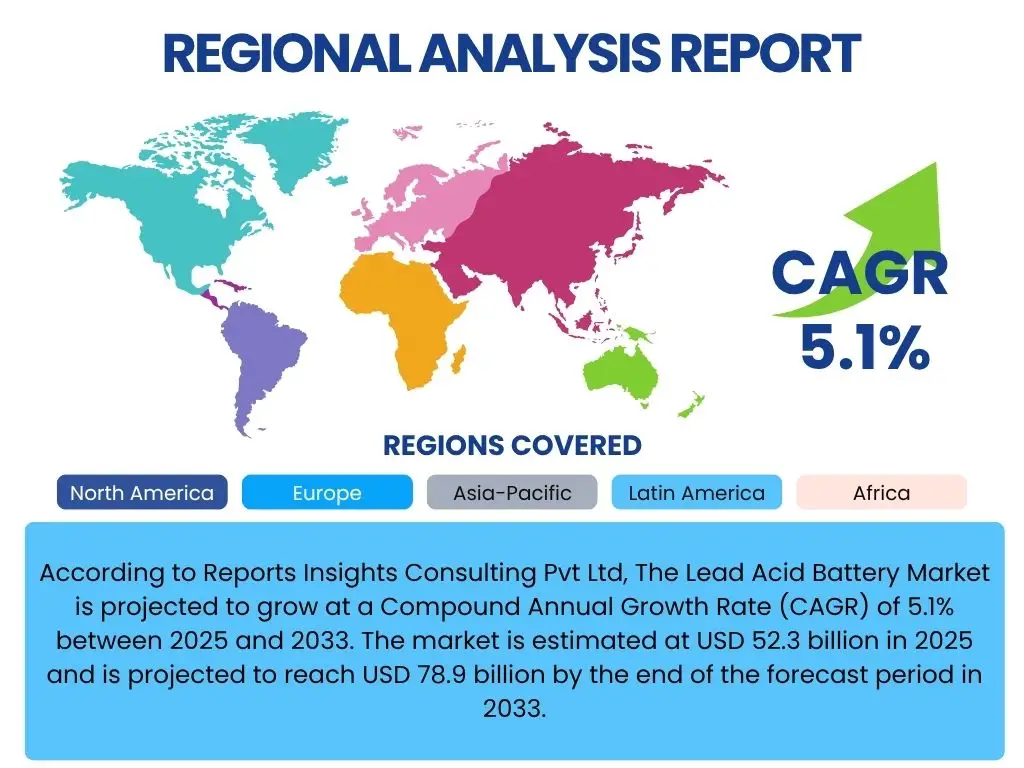

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global Lead Acid Battery market is meticulously segmented to provide a granular view of its diverse applications and technological variations, enabling stakeholders to identify specific growth areas and market dynamics. This comprehensive segmentation allows for a detailed understanding of consumer preferences, industry adoption patterns, and regional variances across the battery landscape. Analysis of these segments is crucial for strategic planning and product development, ensuring that market offerings align with specific sector demands and technological requirements.

- By Type: This segment includes Flooded (or Wet Cell) Lead Acid Batteries, which are traditional, cost-effective, and require maintenance; and Valve Regulated Lead Acid (VRLA) Batteries, which are sealed and maintenance-free, further categorized into Absorbent Glass Mat (AGM) and Gel batteries.

- By Application: This segmentation covers a wide range of end-uses including Automotive (SLI batteries for conventional vehicles, some use in Electric Vehicles/Hybrid Electric Vehicles, and the significant aftermarket for replacements), Industrial applications (Uninterruptible Power Supplies (UPS) for data centers, telecommunications, motive power for forklifts and industrial vehicles, emergency lighting, and renewable energy storage systems).

- By End-Use: This categorizes the market based on whether the batteries are supplied as Original Equipment Manufacturer (OEM) components for new installations (e.g., new vehicles, industrial equipment) or as Aftermarket replacements for existing systems.

Regional Highlights

- North America: This region is characterized by a mature automotive market and significant investments in data centers and telecommunication infrastructure, driving steady demand for SLI and UPS batteries. The emphasis on reliable power backup and stringent environmental regulations also pushes for advanced VRLA battery adoption and robust recycling frameworks.

- Europe: Europe is a key market with strong regulatory frameworks for lead recycling and environmental protection, encouraging the adoption of advanced, maintenance-free lead acid battery types. The region's automotive industry, coupled with increasing investments in renewable energy and smart grid projects, continues to fuel demand for both SLI and stationary storage applications.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by rapid industrialization, burgeoning automotive sales, and extensive infrastructure development in countries like China and India. The expanding telecommunications sector, coupled with growing investments in off-grid and distributed renewable energy solutions, creates substantial demand for cost-effective lead acid batteries across diverse applications.

- Latin America: This region presents significant growth opportunities, particularly in the automotive aftermarket and the expansion of telecommunication networks in remote areas. Economic development and urbanization are increasing the demand for reliable backup power, making lead acid batteries a favored choice due to their affordability and proven performance.

- Middle East and Africa (MEA): The MEA region is experiencing increasing demand for lead acid batteries driven by the expansion of mobile communication networks, burgeoning industrial sectors, and growing investment in renewable energy projects, particularly off-grid solutions in areas with limited grid access. The cost-effectiveness of lead acid batteries makes them highly suitable for these developing markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lead Acid Battery Market.- [Insert Company 1]

- [Insert Company 2]

- [Insert Company 3]

- [Insert Company 4]

- [Insert Company 5]

- [Insert Company 6]

- [Insert Company 7]

- [Insert Company 8]

- [Insert Company 9]

- [Insert Company 10]

- [Insert Company 11]

- [Insert Company 12]

- [Insert Company 13]

- [Insert Company 14]

- [Insert Company 15]

- [Insert Company 16]

- [Insert Company 17]

- [Insert Company 18]

- [Insert Company 19]

- [Insert Company 20]

Frequently Asked Questions

Analyze common user questions about the Lead Acid Battery market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Lead Acid Battery and its primary uses?

A Lead Acid Battery is a rechargeable battery type that uses lead and sulfuric acid to generate electrical energy. Its primary uses include automotive Starting, Lighting, and Ignition (SLI) systems, uninterruptible power supplies (UPS), industrial motive power for forklifts, and stationary energy storage for renewable power systems and telecommunications.

How long do Lead Acid Batteries typically last?

The lifespan of a Lead Acid Battery varies significantly based on its type, application, usage patterns, and maintenance. Automotive SLI batteries typically last 3-5 years, while deep-cycle lead acid batteries used in renewable energy or motive power applications can last 5-10 years or more with proper care, depending on the number of charge/discharge cycles.

Are Lead Acid Batteries environmentally friendly?

While lead is a toxic heavy metal, the lead acid battery industry boasts one of the highest recycling rates globally, with over 99% of batteries being recycled in many regions. This closed-loop recycling process significantly reduces environmental impact by recovering lead and plastics for new batteries, making them a more sustainable option than often perceived, provided they are properly recycled.

What are the main advantages of Lead Acid Batteries over other battery types?

The main advantages of Lead Acid Batteries include their high reliability, robust performance in various temperature conditions, established manufacturing infrastructure, and significantly lower cost per kilowatt-hour compared to many advanced battery chemistries like lithium-ion. They are also highly recyclable and offer excellent surge current capabilities, making them ideal for applications requiring high power delivery.

What is the future outlook for the Lead Acid Battery market?

The Lead Acid Battery market is expected to demonstrate steady growth, driven by continued demand from the automotive SLI sector and expanding industrial applications such as UPS, telecom, and motive power. Innovations in VRLA technology and increasing adoption in cost-sensitive renewable energy storage in emerging markets will also contribute to its resilience and expansion, despite competition from newer technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted