LCD Backlight Module Market

LCD Backlight Module Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710174 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

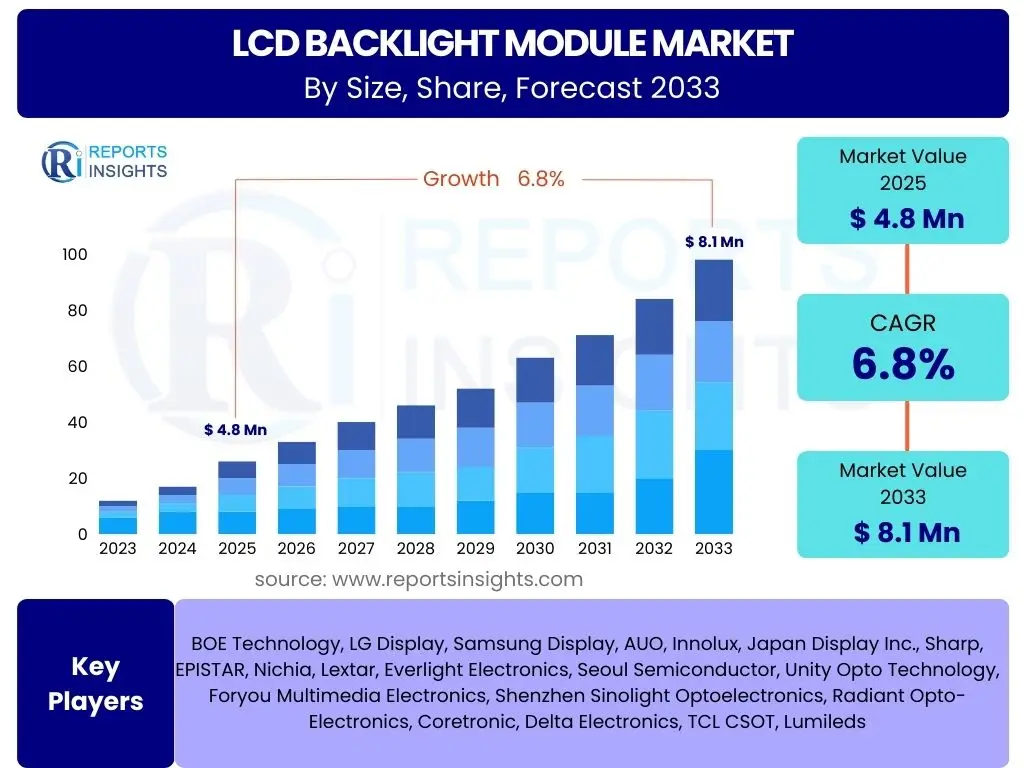

LCD Backlight Module Market Size

According to Reports Insights Consulting Pvt Ltd, The LCD Backlight Module Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 8.1 Billion by the end of the forecast period in 2033.

Key LCD Backlight Module Market Trends & Insights

User inquiries frequently focus on the evolving technological landscape and consumer preferences influencing the LCD Backlight Module market. A prominent trend involves the increasing adoption of Mini-LED and Micro-LED backlight technologies, which are perceived as offering superior contrast, brightness, and power efficiency compared to traditional LED backlights. This technological advancement addresses the growing consumer demand for higher display quality, particularly in premium televisions, professional monitors, and high-end automotive displays. Additionally, the market is seeing a push towards thinner, lighter, and more energy-efficient modules to align with the design aesthetics and sustainability goals of modern electronic devices.

Another significant insight revolves around the diversification of application areas. While consumer electronics like smartphones, tablets, and televisions remain primary drivers, there is a notable expansion into specialized segments such as automotive infotainment systems, medical imaging equipment, and industrial control panels. These applications demand robust, reliable, and highly customizable backlight solutions, fostering innovation in areas like optical design, thermal management, and durability. The integration of advanced optical films and intelligent dimming zones is also gaining traction, enhancing display performance and overall user experience across a wide range of devices.

- Mini-LED and Micro-LED adoption for enhanced contrast and brightness.

- Increased demand for energy-efficient and ultra-thin backlight modules.

- Growing integration of local dimming technologies for improved picture quality.

- Diversification of applications beyond consumer electronics, into automotive, medical, and industrial sectors.

- Advancements in optical film technology and light guide plate (LGP) design for superior uniformity.

- Focus on sustainable materials and manufacturing processes to reduce environmental impact.

AI Impact Analysis on LCD Backlight Module

Users are keen to understand how artificial intelligence is transforming the design, manufacturing, and quality control processes within the LCD Backlight Module industry. AI's primary impact is observed in optimizing complex manufacturing parameters. AI-driven algorithms can analyze vast datasets from production lines, identifying inefficiencies, predicting equipment failures, and fine-tuning processes for greater yield and reduced waste. This leads to more precise control over component placement, bonding, and optical film alignment, crucial for achieving uniform brightness and color accuracy in backlight modules.

Furthermore, AI is instrumental in accelerating the design and simulation phases of new backlight module architectures. Generative design tools powered by AI can explore numerous design iterations for light guide plates, diffuser films, and LED arrays, predicting their optical performance before physical prototyping. This significantly reduces development cycles and costs, enabling manufacturers to quickly respond to market demands for smaller, brighter, and more efficient modules. AI also enhances quality assurance through automated optical inspection (AOI) systems that can detect minute defects, ensuring higher product reliability and consistency in the market.

- Optimization of manufacturing processes through AI-driven analytics for higher yield and efficiency.

- Predictive maintenance of production equipment, minimizing downtime and operational costs.

- AI-powered generative design for accelerated development of novel optical structures and module layouts.

- Enhanced quality control with automated optical inspection systems for defect detection.

- Supply chain optimization through AI forecasting and intelligent inventory management.

- Personalized display calibration and adaptive brightness features in end-user devices, indirectly influencing backlight module design requirements.

Key Takeaways LCD Backlight Module Market Size & Forecast

Analysis of user questions regarding the market's future reveals a strong interest in understanding the underlying factors driving sustained growth and the potential for technological disruption. A key takeaway is the market's resilience and adaptability, particularly with the continuous innovation in backlight technologies such as Mini-LED and Micro-LED. These advancements are not only maintaining the competitiveness of LCDs against emerging display technologies like OLED but are also expanding their applications into premium segments, ensuring a stable growth trajectory over the forecast period. The increasing demand for high-performance displays across various sectors underscores this sustained market vitality.

Another significant insight is the critical role of regional manufacturing hubs, especially in Asia Pacific, in shaping the global supply chain and market dynamics. These regions are central to both the production and consumption of LCD backlight modules, influencing pricing strategies and technological adoption rates. Furthermore, the market forecast indicates a shift towards more customized and application-specific backlight solutions, moving beyond a one-size-fits-all approach. This customization capability, coupled with an emphasis on energy efficiency and environmental sustainability, will be pivotal for companies aiming to capture market share and achieve long-term success in this evolving landscape.

- Market demonstrates consistent growth driven by technological advancements and application diversification.

- Mini-LED and Micro-LED technologies are key growth accelerators, enhancing LCD competitiveness.

- Asia Pacific remains a dominant region for both production and consumption, influencing global market trends.

- Increasing focus on energy efficiency and sustainable manufacturing practices for backlight modules.

- Customization and application-specific solutions are becoming critical for market differentiation.

- The market's future will be shaped by ongoing research and development into next-generation optical materials and designs.

LCD Backlight Module Market Drivers Analysis

The global demand for high-definition and energy-efficient displays across consumer electronics and industrial applications serves as a primary driver for the LCD backlight module market. Consumers consistently seek devices with superior visual performance, including higher contrast ratios, vibrant colors, and improved brightness, which are directly influenced by the quality and technology of the backlight. This push for enhanced display quality fuels innovation in backlight technologies such as Mini-LED, which offers granular local dimming and higher peak brightness, making LCDs competitive with advanced display types.

Additionally, the burgeoning automotive display market, characterized by large, multi-screen infotainment systems, digital instrument clusters, and head-up displays, presents a significant growth impetus. These applications demand robust, durable, and highly reliable backlight modules capable of operating under varying environmental conditions and providing excellent visibility. The integration of advanced driver-assistance systems (ADAS) and connected car technologies further necessitates high-resolution, responsive displays, thereby boosting the adoption of sophisticated LCD backlight solutions. The expansion of industrial monitors, medical imaging devices, and public information displays also contributes to the market's growth, requiring specialized backlight modules tailored for specific performance and longevity requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for high-definition and energy-efficient displays | +1.9% | Global, particularly APAC (China, Korea) | Short to Medium Term (2025-2029) |

| Rapid expansion of the automotive display market | +1.5% | Europe, North America, APAC (Japan, Germany, US) | Medium to Long Term (2027-2033) |

| Technological advancements in Mini-LED and Micro-LED backlights | +1.7% | Global, R&D focused countries (Korea, Japan, Taiwan) | Short to Medium Term (2025-2030) |

| Increasing adoption in industrial and medical applications | +1.0% | North America, Europe, APAC | Medium Term (2026-2031) |

LCD Backlight Module Market Restraints Analysis

One significant restraint on the LCD backlight module market is the intense competition from alternative display technologies, primarily Organic Light Emitting Diodes (OLEDs). OLED displays offer self-emissive pixels, eliminating the need for a backlight entirely, which results in perfect blacks, infinite contrast, and thinner form factors. While LCDs with advanced backlights have significantly improved, OLEDs continue to capture market share in premium smartphone, television, and wearable segments, particularly where display thickness and absolute contrast are paramount. This technological rivalry pressures LCD backlight manufacturers to innovate continuously to maintain competitive edge, often requiring substantial R&D investments.

Another challenge stems from the increasing complexity and cost associated with advanced backlight solutions, such as Mini-LED. These technologies involve a greater number of LED chips, more sophisticated optical films, and intricate manufacturing processes, which can elevate the overall production cost of the display module. While the performance benefits are undeniable, the higher price point can deter adoption in cost-sensitive segments, particularly in emerging markets or for entry-level devices. Furthermore, the supply chain for specific optical materials and specialized LED chips can be volatile, leading to price fluctuations and potential delays, impacting the profitability and market stability for backlight module manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from OLED and other emerging display technologies | -1.2% | Global, particularly premium segments | Short to Long Term (2025-2033) |

| Rising manufacturing complexity and cost of advanced backlights (e.g., Mini-LED) | -0.8% | Global, impacting cost-sensitive markets | Short to Medium Term (2025-2030) |

| Supply chain volatility and material price fluctuations | -0.5% | Global, especially for key components | Short Term (2025-2027) |

| Environmental regulations and disposal challenges for display components | -0.3% | Europe, North America | Medium Term (2027-2032) |

LCD Backlight Module Market Opportunities Analysis

The development and commercialization of next-generation backlight technologies, particularly Mini-LED and Micro-LED, represent a significant growth opportunity for the LCD backlight module market. These technologies allow LCDs to achieve performance metrics—such as high contrast ratios, deep blacks, and superior brightness—that were previously exclusive to OLEDs. By integrating hundreds or thousands of miniature LEDs with precise local dimming zones, manufacturers can create displays with exceptional image quality, making them highly attractive for premium televisions, professional monitors, and virtual reality (VR) headsets. This innovation opens up new revenue streams and allows LCDs to reclaim market share in high-end segments.

Furthermore, the increasing demand for large-format displays in diverse applications, including digital signage, public information displays, and advanced automotive dashboards, offers substantial opportunities. These segments often prioritize brightness, durability, and cost-effectiveness, where LCDs with robust backlight modules excel. The rise of flexible and curved display designs also presents an avenue for innovative backlight solutions that can conform to non-planar surfaces, pushing the boundaries of traditional display aesthetics. Strategic partnerships with automotive OEMs and industrial equipment manufacturers will be crucial for capitalizing on these specialized, high-growth application areas, leveraging customized backlight solutions for specific operational requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Commercialization of Mini-LED and Micro-LED backlights | +2.1% | Global, major display manufacturing regions | Short to Medium Term (2025-2030) |

| Expansion into large-format displays (digital signage, automotive) | +1.8% | APAC, North America, Europe | Medium to Long Term (2026-2033) |

| Development of specialized backlights for niche applications (medical, industrial, VR) | +1.3% | North America, Europe, East Asia | Medium Term (2027-2032) |

| Growing focus on eco-friendly and energy-efficient backlight designs | +0.9% | Global, driven by sustainability initiatives | Long Term (2028-2033) |

LCD Backlight Module Market Challenges Impact Analysis

One primary challenge facing the LCD backlight module market is the rapid pace of technological evolution and the potential for obsolescence. With significant investments being made in OLED, Micro-LED, and other self-emissive display technologies, there is constant pressure on LCD backlight manufacturers to innovate rapidly and cost-effectively. Failure to keep pace with these advancements, particularly in areas like power efficiency, slimness, and contrast, could render traditional backlight technologies less competitive. This necessitates continuous research and development cycles, which require substantial financial and human resources, adding to operational complexities.

Another significant challenge involves managing the environmental impact throughout the product lifecycle, from manufacturing to disposal. Backlight modules often contain various materials, including plastics, metals, and rare earth elements in LEDs, which can pose disposal challenges. Additionally, the manufacturing processes can be energy-intensive. Increasing global regulatory scrutiny on electronic waste and carbon emissions requires manufacturers to invest in more sustainable materials, energy-efficient production methods, and robust recycling programs. Balancing these environmental responsibilities with cost-effectiveness and performance demands represents a complex hurdle for the industry, especially in highly regulated markets.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological obsolescence due to rapid advancements in display industry | -1.0% | Global, particularly R&D intensive regions | Short to Medium Term (2025-2030) |

| High research and development costs for next-generation backlight technologies | -0.7% | Global | Short to Medium Term (2025-2029) |

| Stringent environmental regulations and e-waste management concerns | -0.6% | Europe, North America, parts of APAC | Medium to Long Term (2027-2033) |

| Balancing cost-effectiveness with performance and sustainability goals | -0.5% | Global, particularly emerging markets | Short to Long Term (2025-2033) |

LCD Backlight Module Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global LCD Backlight Module market, offering strategic insights into its current landscape, growth trajectories, and future outlook. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges that influence market expansion across various regions and application sectors. The report also details market segmentation, competitive analysis, and strategic profiles of prominent industry players, enabling stakeholders to make informed business decisions and identify lucrative investment avenues within the display technology ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BOE Technology, LG Display, Samsung Display, AUO, Innolux, Japan Display Inc., Sharp, EPISTAR, Nichia, Lextar, Everlight Electronics, Seoul Semiconductor, Unity Opto Technology, Foryou Multimedia Electronics, Shenzhen Sinolight Optoelectronics, Radiant Opto-Electronics, Coretronic, Delta Electronics, TCL CSOT, Lumileds |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LCD Backlight Module market is intricately segmented to provide a granular view of its various facets, enabling a deeper understanding of market dynamics and targeted opportunities. These segmentations are critical for identifying key growth areas, understanding technological preferences, and analyzing the competitive landscape. The market is primarily broken down by the core technology employed, the specific components that constitute a backlight module, the diverse applications in which these modules are utilized, and the end-use industries they serve, each with distinct requirements and growth drivers.

Further analysis of these segments reveals shifts in market share and technological preferences. For instance, while conventional Edge-lit and Direct-lit (DLED) technologies maintain a significant base, the Mini-LED and Micro-LED segments are experiencing rapid growth due to their superior performance characteristics and increasing adoption in high-end devices. Similarly, the consumer electronics sector remains the largest application area, but the automotive and industrial segments are demonstrating robust expansion, demanding specialized, more resilient, and customizable backlight solutions. This detailed segmentation allows stakeholders to accurately gauge market size and forecast growth across these varied categories, fostering strategic planning and investment decisions.

- By Technology:

- Edge-lit

- Direct-lit (DLED)

- Mini-LED

- Micro-LED

- By Component:

- LED Chips

- Diffuser Plates

- Light Guide Plates (LGPs)

- Optical Films (Reflector, Prism, etc.)

- Inverter Boards

- Frames/Chassis

- By Application:

- Smartphones

- Tablets

- Laptops

- Monitors

- Televisions

- Automotive Displays

- Industrial Displays

- Medical Devices

- Digital Signage

- Avionics

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- Retail & Advertising

- Aerospace & Defense

- Others

Regional Highlights

The Asia Pacific (APAC) region stands as the dominant force in the LCD Backlight Module market, driven by the presence of major display panel manufacturers, extensive consumer electronics production capabilities, and a large consumer base for display-equipped devices. Countries such as China, South Korea, Japan, and Taiwan are at the forefront of both backlight module innovation and manufacturing, leveraging advanced technological infrastructure and robust supply chains. This region is not only a key production hub but also a significant market for high-definition and next-generation display technologies, fueling continuous investment in R&D and capacity expansion.

North America and Europe represent mature markets characterized by high demand for premium and specialized display applications, including automotive, medical, and high-end professional monitors. These regions prioritize energy efficiency, environmental compliance, and advanced display features, driving the adoption of Mini-LED and other high-performance backlight solutions. While their manufacturing footprint may be smaller compared to APAC, their strong R&D ecosystems and significant purchasing power make them crucial for market development and the adoption of cutting-edge technologies. Latin America, the Middle East, and Africa (MEA) are emerging markets, showing increasing adoption of display technologies driven by urbanization and rising disposable incomes, presenting future growth opportunities for more cost-effective and mainstream backlight modules.

- Asia Pacific (APAC): Dominates the market due to leading display panel manufacturers (e.g., in China, South Korea, Taiwan, Japan), high production capacity, and a vast consumer electronics market. The region leads in the adoption and development of Mini-LED and Micro-LED technologies.

- North America: Significant market for high-end consumer electronics, automotive displays, and specialized industrial/medical applications. Focus on advanced features, energy efficiency, and regulatory compliance drives adoption of premium backlight solutions.

- Europe: Strong demand for automotive, industrial, and digital signage displays. Emphasis on sustainability and high-quality visual performance fosters innovation and market growth in advanced backlight technologies.

- Latin America & MEA: Emerging markets with growing demand for consumer electronics. Opportunities for mainstream and cost-effective LCD backlight modules as regional economies expand and technology adoption increases.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LCD Backlight Module Market.- BOE Technology

- LG Display

- Samsung Display

- AUO

- Innolux

- Japan Display Inc.

- Sharp

- EPISTAR

- Nichia

- Lextar

- Everlight Electronics

- Seoul Semiconductor

- Unity Opto Technology

- Foryou Multimedia Electronics

- Shenzhen Sinolight Optoelectronics

- Radiant Opto-Electronics

- Coretronic

- Delta Electronics

- TCL CSOT

- Lumileds

Frequently Asked Questions

What is an LCD backlight module?

An LCD backlight module is an essential component of a Liquid Crystal Display (LCD) that provides the illumination necessary for the display to produce an image. Unlike self-emissive displays, LCDs do not generate their own light, so a backlight module, typically composed of LEDs, light guide plates, diffuser sheets, and optical films, is required to uniformly light the LCD panel from behind.

How does Mini-LED technology differ from traditional LED backlights?

Mini-LED technology uses significantly smaller LED chips, allowing thousands of LEDs to be packed into a backlight module, creating numerous local dimming zones. This provides much more precise control over brightness and contrast compared to traditional LED backlights, which have fewer, larger LEDs and fewer dimming zones, leading to superior picture quality, deeper blacks, and higher peak brightness.

What are the primary drivers for the growth of the LCD Backlight Module market?

Key drivers include the increasing global demand for high-definition and energy-efficient displays in consumer electronics, the rapid expansion of automotive infotainment systems, and the ongoing technological advancements in backlight solutions like Mini-LED and Micro-LED. These innovations enhance LCD performance, maintaining its competitiveness and extending its applications.

What is the impact of OLED technology on the LCD backlight market?

OLED technology poses a significant competitive restraint as OLED displays are self-emissive and do not require a backlight, offering perfect blacks and thinner form factors. This drives LCD backlight manufacturers to innovate continuously, particularly with Mini-LED and Micro-LED, to improve performance and cost-effectiveness to retain market share against OLED's premium appeal.

What are the future trends for LCD backlight technology?

Future trends focus on enhancing display performance through advanced technologies like Mini-LED and Micro-LED for better contrast and brightness, improving energy efficiency for longer battery life and reduced power consumption, and designing thinner and more flexible modules. There is also a growing emphasis on sustainable materials and manufacturing processes to meet environmental regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted