Laser Direct Imaging Equipment Market

Laser Direct Imaging Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706398 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

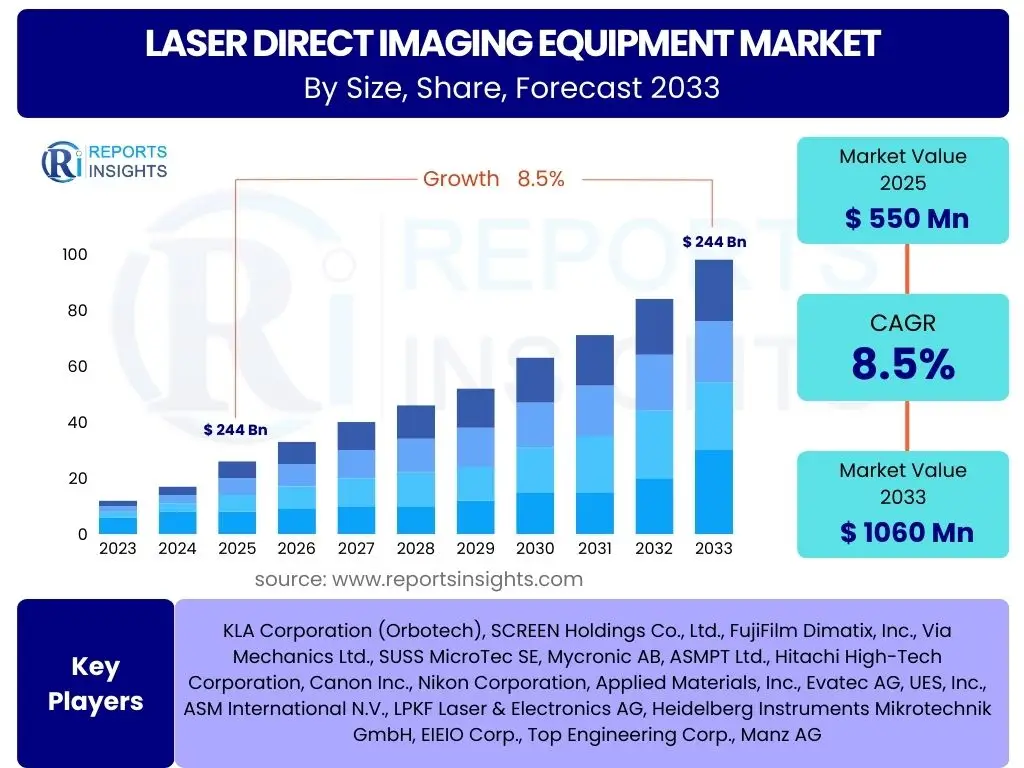

Laser Direct Imaging Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Laser Direct Imaging Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 550 Million in 2025 and is projected to reach USD 1060 Million by the end of the forecast period in 2033.

Key Laser Direct Imaging Equipment Market Trends & Insights

The Laser Direct Imaging (LDI) equipment market is undergoing significant transformation, driven by an escalating demand for miniaturized and high-performance electronic components. Users frequently inquire about how the continuous push for greater component density and complex circuit designs influences the evolution of LDI technology. This trend necessitates imaging solutions that offer higher precision, faster throughput, and enhanced flexibility to accommodate intricate patterns on diverse substrates, ranging from traditional PCBs to advanced packaging structures.

Furthermore, there is keen interest in how LDI is adapting to the burgeoning fields of advanced packaging, such as System-in-Package (SiP) and Fan-Out Wafer Level Packaging (Fo-WLP), which demand ultra-fine pitch interconnections. The integration of LDI into Industry 4.0 paradigms, emphasizing automation, real-time data analysis, and intelligent manufacturing workflows, is another area of significant user inquiry. These advancements are critical for improving manufacturing efficiency, yield rates, and overall operational scalability in the electronics industry.

- Increasing demand for miniaturization and higher circuit density in consumer electronics.

- Shift towards advanced packaging technologies requiring ultra-fine line and space capabilities.

- Growing adoption in flexible electronics and advanced display manufacturing (e.g., OLED, MicroLED).

- Integration of LDI systems with automation and Industry 4.0 principles for smart factories.

- Emphasis on enhanced resolution, faster imaging speeds, and improved process control.

AI Impact Analysis on Laser Direct Imaging Equipment

Common user questions regarding AI's influence on Laser Direct Imaging Equipment revolve around its potential to revolutionize manufacturing processes, enhance precision, and optimize operational efficiencies. Users are keen to understand how artificial intelligence can move LDI beyond mere imaging to become an intelligent component of the production line. AI's capabilities in advanced data analytics, pattern recognition, and machine learning are being leveraged to address critical challenges such as defect detection, process optimization, and predictive maintenance in LDI systems.

The integration of AI into LDI equipment facilitates a shift towards more autonomous and adaptive manufacturing environments. For instance, AI algorithms can analyze vast datasets of imaging results to identify subtle defects that human operators might miss, significantly improving quality control. Furthermore, AI-driven predictive maintenance can forecast equipment failures, minimizing downtime and extending the lifespan of costly LDI machinery. This intelligent oversight not only boosts productivity but also contributes to higher yield rates and reduced operational costs, fundamentally transforming the economic landscape of LDI operations.

- Enhanced defect detection and classification through machine vision and deep learning algorithms.

- Predictive maintenance for LDI systems, reducing unplanned downtime and optimizing service intervals.

- Optimization of exposure parameters and process flows based on real-time data analysis.

- Automated quality control and yield management through intelligent feedback loops.

- Accelerated research and development by analyzing complex imaging data and simulating outcomes.

Key Takeaways Laser Direct Imaging Equipment Market Size & Forecast

Users frequently inquire about the primary factors driving and shaping the Laser Direct Imaging Equipment market's future trajectory. The market's robust growth trajectory is fundamentally propelled by the insatiable global demand for advanced electronic devices, which continually require higher performance within smaller form factors. This pervasive trend across consumer electronics, automotive, and industrial sectors underscores the critical role of LDI technology in enabling the next generation of electronic components, making it a pivotal investment for manufacturers aiming for precision and efficiency.

A significant takeaway is the strong correlation between LDI market expansion and innovation in display technology, advanced packaging, and flexible electronics. These specialized applications demand the ultra-high resolution and fine-line capabilities inherent to LDI. The forecast indicates sustained growth, signifying that manufacturers are increasingly prioritizing LDI solutions to overcome the limitations of traditional imaging methods, thereby enhancing production yield, reducing material waste, and accelerating product development cycles in a highly competitive global landscape.

- The market is poised for significant growth, driven by the increasing complexity and miniaturization of electronic devices.

- High-density interconnects (HDIs) and advanced packaging are key application areas fueling LDI adoption.

- Technological advancements in display manufacturing, especially for OLED and MicroLED, are major growth catalysts.

- Growing investments in smart manufacturing and automation further support LDI equipment integration.

- Efficiency gains and yield improvements offered by LDI technology are critical for competitive manufacturing.

Laser Direct Imaging Equipment Market Drivers Analysis

The LDI equipment market is significantly propelled by several robust drivers rooted in the relentless evolution of the electronics industry. A primary force is the global demand for miniaturized and high-performance electronic devices, spanning from smartphones and wearables to advanced automotive systems. This pervasive need for smaller, more powerful, and feature-rich components directly translates into a requirement for imaging technologies capable of producing finer lines and more intricate patterns on substrates, a core competency of LDI. The precision and speed offered by LDI are becoming indispensable as circuit densities continue to increase across various applications.

Furthermore, the burgeoning fields of advanced packaging, such as System-in-Package (SiP) and Fan-Out Wafer Level Packaging (Fo-WLP), are intensifying the adoption of LDI technology. These advanced packaging methods necessitate ultra-fine pitch interconnections and multi-layer structures, where the precision and flexibility of LDI offer significant advantages over traditional photolithography. The expansion of 5G infrastructure and the Internet of Things (IoT) ecosystem also contribute substantially, as these technologies demand higher component density and reliability, fueling investment in advanced manufacturing equipment like LDI systems. This convergence of demand for high-performance, compact, and reliable electronics drives continuous innovation and investment in LDI solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of electronic devices and increasing circuit density | +1.5% | Global | Short to Mid-term |

| Growth in advanced packaging technologies (e.g., SiP, Fo-WLP) | +1.2% | Asia Pacific, North America | Mid-term |

| Proliferation of IoT devices and 5G infrastructure deployment | +1.0% | Global, Europe | Mid to Long-term |

| Increasing demand for flexible and wearable electronics | +0.8% | Asia Pacific, North America | Mid-term |

| Advancements in display manufacturing (e.g., OLED, MicroLED) | +0.7% | Asia Pacific | Mid to Long-term |

Laser Direct Imaging Equipment Market Restraints Analysis

Despite its technological advantages, the Laser Direct Imaging equipment market faces certain restraints that could temper its growth trajectory. One significant barrier is the substantial initial capital investment required for acquiring LDI systems. These machines are highly sophisticated, incorporating advanced optics, laser technology, and precision mechanics, making them considerably more expensive than traditional lithography equipment. This high entry cost can be prohibitive for smaller manufacturers or those operating with tighter capital expenditure budgets, potentially limiting widespread adoption, particularly in emerging markets where capital availability might be constrained.

Another notable restraint pertains to the technological complexities involved in operating and maintaining LDI equipment. The precision required for fine-line imaging necessitates highly skilled technicians and engineers, both for operation and for troubleshooting complex issues. The availability of such specialized labor is often a challenge, particularly in developing regions. Moreover, the steep learning curve associated with integrating LDI systems into existing manufacturing workflows can also act as a deterrent, requiring significant training and adjustment periods that can impact immediate production efficiency and overall operational costs. Competition from evolving alternative technologies also presents a restraint, as manufacturers constantly evaluate the most cost-effective and efficient solutions for their specific needs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment and operational costs | -0.7% | Global | Short to Mid-term |

| Technical complexities and requirement for highly skilled labor | -0.5% | Global | Mid-term |

| Competition from advanced traditional photolithography in some segments | -0.3% | Europe, North America | Short-term |

| Longer integration and qualification cycles for new systems | -0.2% | Global | Short-term |

Laser Direct Imaging Equipment Market Opportunities Analysis

The Laser Direct Imaging equipment market is ripe with opportunities driven by emerging technological applications and expanding industrial requirements. A significant avenue for growth lies in the increasing demand for LDI solutions in the manufacturing of Micro-Electro-Mechanical Systems (MEMS). As MEMS devices become more integrated into various applications, from sensors in automotive to medical diagnostics, the need for high-precision, intricate patterning that LDI offers becomes paramount. This niche but rapidly expanding sector presents a lucrative growth segment for LDI manufacturers, enabling the creation of devices with unprecedented functionalities and compact designs.

Furthermore, the continuous innovation in display technologies, specifically the rise of advanced displays like OLED, MicroLED, and flexible displays, provides substantial opportunities. These next-generation displays often require extremely fine pixel pitch and complex circuitry, which LDI technology is uniquely positioned to address due to its non-contact, high-resolution capabilities. Additionally, the automotive electronics sector, with its increasing reliance on sophisticated ADAS (Advanced Driver-Assistance Systems) and infotainment systems, demands highly reliable and dense circuitry, opening new frontiers for LDI adoption. The ongoing global push for sustainable manufacturing practices also creates an opportunity for LDI, as its maskless process reduces material consumption and waste compared to traditional methods.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging applications in Micro-Electromechanical Systems (MEMS) | +0.9% | North America, Asia Pacific | Long-term |

| Expansion into advanced automotive and aerospace electronics | +0.7% | Europe, North America | Mid-term |

| Growth in advanced display manufacturing (e.g., MicroLED, flexible displays) | +0.6% | Asia Pacific | Long-term |

| Increasing adoption in semiconductor packaging and advanced materials processing | +0.5% | Global | Mid to Long-term |

| Potential for sustainable manufacturing due to maskless process | +0.4% | Global | Long-term |

Laser Direct Imaging Equipment Market Challenges Impact Analysis

The Laser Direct Imaging equipment market is not without its challenges, which can impact innovation and market penetration. A primary challenge is the rapid pace of technological advancements, leading to potential obsolescence of existing equipment. As research and development continuously push the boundaries of resolution, speed, and automation, manufacturers face pressure to frequently upgrade or replace their systems to remain competitive, entailing significant ongoing investment. This rapid evolution also demands continuous R&D expenditure from LDI equipment providers to stay ahead of the curve, requiring substantial financial commitment and strategic foresight.

Supply chain vulnerabilities also pose a considerable challenge, especially for highly specialized optical components, laser sources, and rare earth materials critical to LDI system manufacturing. Geopolitical tensions, trade disputes, and unforeseen global events can disrupt these supply chains, leading to delays, increased costs, and production bottlenecks, thereby affecting the timely delivery and pricing of LDI systems. Moreover, the market faces intense competition from alternative imaging technologies or hybrid approaches that may offer cost efficiencies for certain applications, necessitating LDI manufacturers to continuously demonstrate superior performance, versatility, and cost-effectiveness to justify the premium associated with their advanced technology and maintain market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid technological advancements and potential obsolescence of equipment | -0.6% | Global | Short to Mid-term |

| Supply chain disruptions and availability of specialized components | -0.4% | Global | Short-term |

| High research and development expenditure required to innovate | -0.3% | Global | Long-term |

| Intense competition and pricing pressure from alternative technologies | -0.2% | Global | Mid-term |

Laser Direct Imaging Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Laser Direct Imaging Equipment Market, offering crucial insights into its current state, historical performance, and future growth trajectory. It meticulously covers market size estimations, growth drivers, restraints, opportunities, and challenges, providing a holistic view of the market dynamics. The report further delves into key market trends, the transformative impact of Artificial Intelligence, and detailed segmentation analysis across various product types, applications, and end-use industries, alongside a thorough regional assessment. It aims to equip stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 550 Million |

| Market Forecast in 2033 | USD 1060 Million |

| Growth Rate | 8.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | KLA Corporation (Orbotech), SCREEN Holdings Co., Ltd., FujiFilm Dimatix, Inc., Via Mechanics Ltd., SUSS MicroTec SE, Mycronic AB, ASMPT Ltd., Hitachi High-Tech Corporation, Canon Inc., Nikon Corporation, Applied Materials, Inc., Evatec AG, UES, Inc., ASM International N.V., LPKF Laser & Electronics AG, Heidelberg Instruments Mikrotechnik GmbH, EIEIO Corp., Top Engineering Corp., Manz AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Laser Direct Imaging Equipment market is segmented to provide a granular understanding of its diverse applications and technological nuances, reflecting the varied demands across different end-use industries. This detailed segmentation allows for a precise evaluation of market potential within specific verticals and technological domains, highlighting areas of high growth and emerging opportunities. Understanding these segments is crucial for stakeholders to tailor strategies, optimize product development, and target specific market needs effectively, ensuring solutions align with evolving industry requirements. Each segment provides unique insights into where LDI technology is gaining traction and its specific value proposition.

- By Application: This segment categorizes LDI equipment based on its primary use cases, including Printed Circuit Boards (PCBs) for traditional and advanced electronics, Flat Panel Displays (FPDs) for screens across devices, Advanced Packaging for semiconductor integration, MEMS for micro-scale devices, Flexible Electronics for bendable devices, and Other specialized applications like semiconductor masks and photomasks.

- By Product Type: This segmentation differentiates LDI systems by their resolution capabilities, typically divided into High-Resolution LDI Systems, designed for ultra-fine patterning, and Standard Resolution LDI Systems, used for less demanding applications but still offering advantages over traditional methods.

- By End-Use Industry: This segment examines the market based on the industries that utilize LDI equipment, such as Consumer Electronics (smartphones, laptops), Automotive (ADAS, infotainment systems), Industrial (automation, power electronics), Healthcare (medical devices, diagnostics), and Aerospace & Defense (high-reliability components).

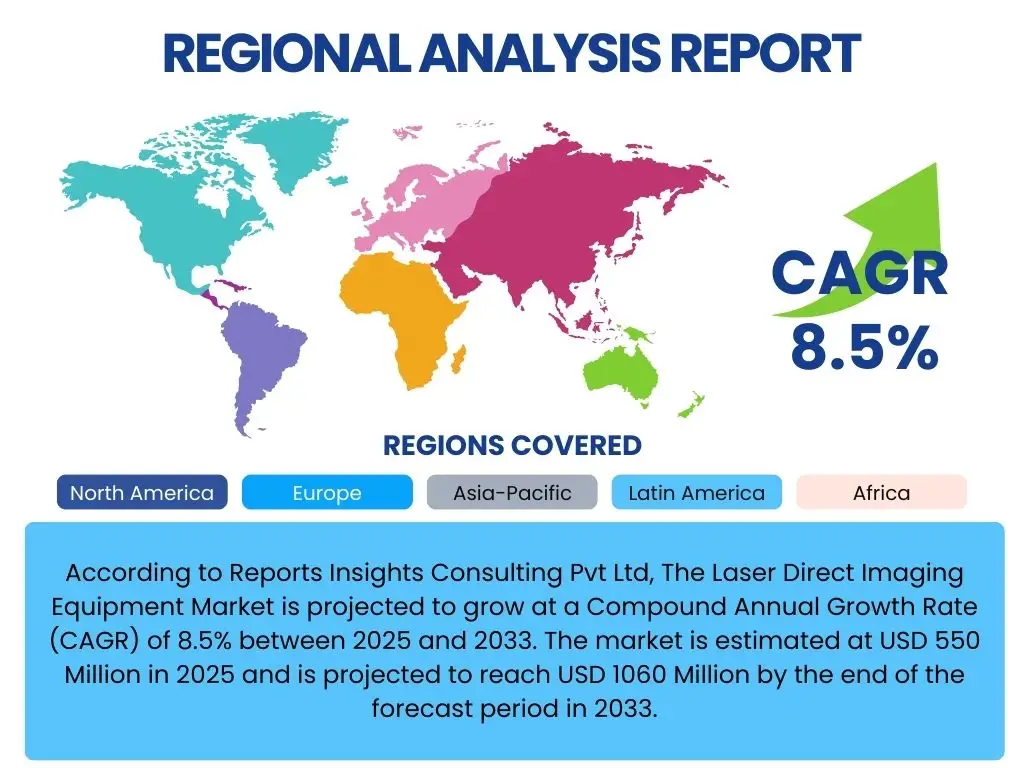

Regional Highlights

The global Laser Direct Imaging Equipment market exhibits distinct regional dynamics driven by varying levels of industrial development, technological adoption, and manufacturing capabilities. The Asia Pacific region stands as the dominant force, primarily owing to its robust electronics manufacturing ecosystem. Countries like China, Taiwan, South Korea, and Japan are global hubs for PCB, FPD, and semiconductor manufacturing, driving a consistently high demand for advanced imaging solutions. The continuous expansion of consumer electronics production, coupled with significant investments in advanced packaging and display technologies across these nations, ensures APAC's leading position, with strong government support for high-tech manufacturing further bolstering growth.

North America and Europe also represent significant markets for LDI equipment, driven by innovation, stringent quality requirements, and specialized applications. North America's growth is often linked to its strong presence in aerospace, defense, and high-end computing, where precision and reliability are paramount, alongside a burgeoning advanced packaging sector. European adoption is propelled by advancements in automotive electronics, industrial automation, and the development of niche technologies requiring high-precision patterning, supported by strong R&D infrastructure. Emerging markets in Latin America and the Middle East & Africa are gradually increasing their adoption as local manufacturing capabilities expand and industries modernize, though they currently hold smaller market shares.

- Asia Pacific (APAC): Dominant market share due to its extensive electronics manufacturing base, including China, Taiwan, South Korea, and Japan, which are major producers of PCBs, FPDs, and advanced semiconductor packages.

- North America: Significant market for high-end LDI equipment driven by innovation in defense, aerospace, medical devices, and advanced semiconductor R&D.

- Europe: Strong adoption in automotive electronics, industrial automation, and specialized electronics manufacturing, with a focus on high-reliability and precision applications.

- Latin America: Emerging market with growing electronics assembly and manufacturing capabilities, gradually increasing adoption of LDI technology.

- Middle East & Africa (MEA): Nascent market with potential growth driven by increasing industrialization and investment in local electronics manufacturing infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Laser Direct Imaging Equipment Market.- KLA Corporation (Orbotech)

- SCREEN Holdings Co., Ltd.

- FujiFilm Dimatix, Inc.

- Via Mechanics Ltd.

- SUSS MicroTec SE

- Mycronic AB

- ASMPT Ltd.

- Hitachi High-Tech Corporation

- Canon Inc.

- Nikon Corporation

- Applied Materials, Inc.

- Evatec AG

- UES, Inc.

- ASM International N.V.

- LPKF Laser & Electronics AG

- Heidelberg Instruments Mikrotechnik GmbH

- EIEIO Corp.

- Top Engineering Corp.

- Manz AG

- A.B.C. Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Laser Direct Imaging Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Laser Direct Imaging (LDI) equipment?

Laser Direct Imaging (LDI) equipment is an advanced, maskless lithography technology that uses a highly focused laser beam to directly "write" circuit patterns onto photosensitive materials, such as those used in printed circuit boards (PCBs), flat panel displays (FPDs), and semiconductor packages, eliminating the need for physical photomasks.

What are the primary applications of LDI technology?

LDI technology is primarily applied in the manufacturing of high-density interconnect (HDI) PCBs, advanced packaging for semiconductors (e.g., SiP, Fo-WLP), flat panel displays (OLED, MicroLED), MEMS devices, and flexible electronics, where high precision and fine line resolution are critical.

How does LDI improve manufacturing processes compared to traditional methods?

LDI offers significant improvements by eliminating photomask production, reducing material waste, enabling faster design changes, increasing yield rates through higher precision, and facilitating rapid prototyping. Its maskless nature also lowers operational costs and reduces environmental impact.

Which regions are leading the adoption of Laser Direct Imaging equipment?

The Asia Pacific region, particularly countries like China, Taiwan, South Korea, and Japan, leads the adoption of LDI equipment due to its established and expanding electronics manufacturing ecosystem and continuous investment in advanced production technologies.

What are the future trends influencing the LDI equipment market?

Future trends influencing the LDI market include continued miniaturization, the rise of AI integration for enhanced automation and defect detection, increased demand for advanced packaging, growth in flexible and wearable electronics, and a focus on sustainable manufacturing practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted