K 12 Education Technology Market

K 12 Education Technology Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700923 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

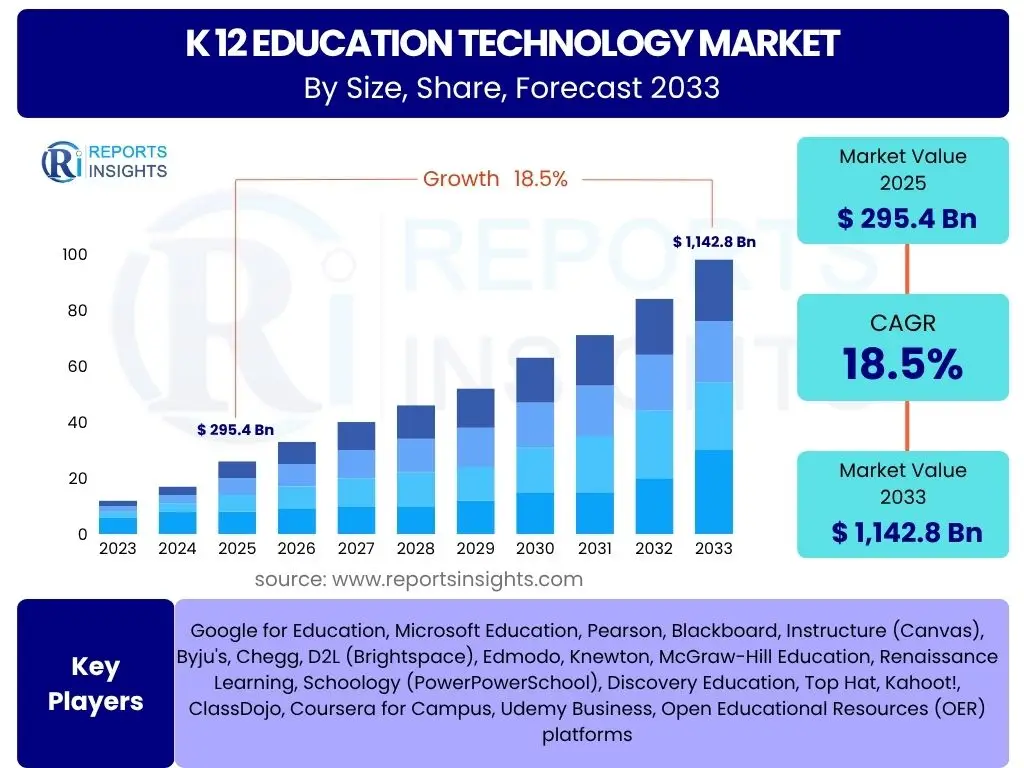

K 12 Education Technology Market Size

According to Reports Insights Consulting Pvt Ltd, The K 12 Education Technology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 295.4 Billion in 2025 and is projected to reach USD 1,142.8 Billion by the end of the forecast period in 2033. This substantial growth is driven by increasing digital transformation initiatives in education, a rising demand for personalized learning experiences, and government investments in educational infrastructure across various regions. The integration of advanced technologies such as artificial intelligence, virtual reality, and cloud computing is further accelerating market expansion, transforming traditional learning environments into dynamic, interactive spaces.

Key K 12 Education Technology Market Trends & Insights

The K 12 Education Technology market is currently shaped by several transformative trends aimed at enhancing student engagement, improving learning outcomes, and streamlining administrative processes. Users frequently inquire about the shift towards more personalized and adaptive learning experiences, recognizing the limitations of one-size-fits-all approaches. There is significant interest in how technology facilitates differentiated instruction and caters to diverse learning styles and paces. Furthermore, the pervasive adoption of hybrid and blended learning models, spurred by recent global events, continues to be a central topic of discussion. Stakeholders are keen to understand the sustainable integration of online and offline learning components, and how this impacts pedagogical strategies and infrastructure requirements.

Another prominent area of inquiry revolves around the role of data analytics in K 12 education. Educators and administrators seek insights into how student performance data can be effectively collected, analyzed, and leveraged to inform instructional decisions, identify learning gaps, and provide timely interventions. The increasing focus on digital citizenship and online safety, alongside the demand for intuitive and user-friendly educational platforms, also remains a critical trend. Users frequently ask about the development of secure and accessible solutions that support collaborative learning and foster critical thinking skills, preparing students for an increasingly digital future.

- Personalized and Adaptive Learning: Tailoring content and pace to individual student needs.

- Hybrid and Blended Learning Models: Seamless integration of in-person and remote instruction.

- Gamification and Immersive Technologies: Using game-like elements and AR/VR for engagement.

- Data Analytics for Pedagogical Insights: Leveraging data to inform teaching and student support.

- Focus on Digital Citizenship and Cybersecurity: Ensuring safe and responsible online learning environments.

- Collaborative Learning Platforms: Tools facilitating peer-to-peer interaction and group projects.

AI Impact Analysis on K 12 Education Technology

The integration of Artificial Intelligence (AI) is fundamentally reshaping the K 12 Education Technology landscape, prompting numerous questions from educators, parents, and policymakers regarding its potential and implications. Common user queries focus on AI's ability to personalize learning pathways, offering adaptive content and assessments that adjust in real-time to a student's progress and understanding. There is significant interest in how AI algorithms can identify individual learning gaps, recommend tailored resources, and provide immediate, constructive feedback, thereby fostering a more efficient and effective learning process than traditional methods allow. Furthermore, users are keen to understand AI's role in automating administrative tasks, such as grading, scheduling, and attendance tracking, which frees up educators to focus more on instruction and student interaction.

Concerns and expectations also revolve around the ethical deployment of AI, including data privacy, algorithmic bias, and the potential impact on human interaction in the classroom. Users often ask about the development of AI tools that support teachers rather than replace them, emphasizing AI's potential as a powerful assistant for differentiation and classroom management. The capacity of AI to generate diverse educational content, provide language learning support, and create virtual tutoring experiences is also a frequent area of inquiry. Overall, the discourse highlights a strong desire for AI solutions that are transparent, equitable, and designed to augment human intelligence and creativity, ensuring that technology serves to enhance learning opportunities for all students while addressing societal and pedagogical implications.

- Personalized Learning Pathways: AI adapts content and pace based on student performance.

- Automated Administrative Tasks: Streamlining grading, attendance, and scheduling for educators.

- Intelligent Tutoring Systems: Providing on-demand, individualized academic support.

- Content Creation and Curation: AI assists in generating and organizing educational materials.

- Data-driven Insights: AI analyzes student data to identify trends and predict academic needs.

- Ethical Considerations: Focus on data privacy, algorithmic bias, and responsible AI deployment.

Key Takeaways K 12 Education Technology Market Size & Forecast

The K 12 Education Technology market is poised for significant expansion, driven by a confluence of technological advancements, evolving pedagogical approaches, and increasing digital literacy. Common questions from stakeholders often center on the primary drivers underpinning this growth, such as widespread internet penetration, the proliferation of digital devices, and a global emphasis on STEM education. The forecast indicates robust growth across various segments, reflecting a comprehensive digital transformation within the education sector. This transformation extends beyond merely digitizing existing content to creating entirely new learning experiences that are interactive, immersive, and highly engaging for students from kindergarten through twelfth grade. Understanding these foundational growth catalysts is crucial for strategic planning and investment within the ecosystem.

Another key takeaway frequently inquired about is the geographical distribution of market growth and the segments that are expected to dominate. While mature markets like North America and Europe continue to innovate and adopt advanced solutions, emerging economies in Asia Pacific and Latin America are anticipated to exhibit rapid growth due to increasing government investments and a burgeoning middle class prioritizing quality education. Furthermore, solutions related to learning management systems, assessment tools, and personalized learning platforms are expected to lead the market, indicating a strong demand for integrated, data-driven educational ecosystems. The sustained growth trajectory underscores a fundamental shift in educational delivery, emphasizing efficiency, accessibility, and individualized student success.

- Robust Market Expansion: Projected CAGR of 18.5% signals strong growth from 2025 to 2033.

- Digital Transformation Catalyst: Technology is fundamental to modernizing K 12 education globally.

- Emerging Market Potential: Asia Pacific and Latin America are key growth regions.

- Solution-Centric Growth: High demand for integrated platforms, analytics, and personalized learning tools.

- Sustainability of Hybrid Models: Blended learning is cementing its role as a permanent educational paradigm.

K 12 Education Technology Market Drivers Analysis

The K 12 Education Technology market is propelled by a combination of technological advancements, policy initiatives, and shifting educational paradigms. The increasing adoption of digital learning tools and platforms, driven by the need for remote learning capabilities and enhanced classroom engagement, serves as a primary catalyst. Furthermore, government initiatives aimed at modernizing educational infrastructure and promoting digital literacy play a pivotal role in creating a conducive environment for EdTech growth. The demand for personalized and adaptive learning experiences, catering to diverse student needs, also significantly contributes to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Internet Penetration & Digital Device Adoption | +4.2% | Global, particularly APAC & LATAM | Short to Medium-term (2025-2030) |

| Government Initiatives & Funding for Digital Education | +3.8% | North America, Europe, India, China | Medium to Long-term (2025-2033) |

| Demand for Personalized & Adaptive Learning | +3.5% | Global | Short to Long-term (2025-2033) |

| Growing Emphasis on STEM & Skill-based Learning | +3.0% | North America, Europe, Asia Pacific | Medium to Long-term (2025-2033) |

K 12 Education Technology Market Restraints Analysis

Despite robust growth, the K 12 Education Technology market faces several significant restraints that could impede its full potential. A major challenge is the persistent digital divide, where disparities in access to reliable internet and digital devices hinder equitable adoption of EdTech solutions, particularly in underserved regions and low-income communities. Additionally, concerns regarding data privacy and cybersecurity pose a considerable hurdle, as educational institutions handle sensitive student information. The high initial investment costs for implementing comprehensive EdTech infrastructure and the ongoing need for teacher training and professional development also act as deterrents for many schools and districts, especially those with limited budgets and resources.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Divide & Lack of Infrastructure | -3.5% | Emerging Economies, Rural Areas | Medium-term (2025-2030) |

| Data Privacy & Cybersecurity Concerns | -2.8% | Global | Short to Long-term (2025-2033) |

| High Implementation Costs & Budgetary Constraints | -2.5% | Global, especially Public Schools | Short to Medium-term (2025-2030) |

| Resistance to Change & Lack of Teacher Training | -2.0% | Global | Short to Medium-term (2025-2030) |

K 12 Education Technology Market Opportunities Analysis

The K 12 Education Technology market presents numerous opportunities for innovation and expansion, driven by evolving educational needs and technological advancements. The increasing focus on skills-based learning and preparing students for future careers opens avenues for specialized EdTech solutions that address critical thinking, problem-solving, and collaboration. Furthermore, the burgeoning demand for immersive learning experiences, facilitated by Virtual Reality (VR) and Augmented Reality (AR) technologies, offers significant growth potential for engaging and interactive educational content. The expansion into untapped rural and semi-urban markets, particularly in developing economies, presents substantial opportunities for affordable and accessible digital learning solutions. Additionally, the continuous development of AI and machine learning promises to create more sophisticated adaptive learning platforms and intelligent tutoring systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Immersive Technologies (VR/AR) | +3.5% | Global, particularly North America, Europe | Medium to Long-term (2027-2033) |

| Untapped Markets in Rural & Semi-urban Areas | +3.0% | Asia Pacific, Africa, Latin America | Medium to Long-term (2026-2033) |

| Development of AI-powered Adaptive Learning Platforms | +2.8% | Global | Short to Long-term (2025-2033) |

| Increased Focus on Social-Emotional Learning (SEL) through Tech | +2.2% | North America, Europe | Medium-term (2026-2031) |

K 12 Education Technology Market Challenges Impact Analysis

The K 12 Education Technology market faces several inherent challenges that demand strategic responses from stakeholders. A primary challenge involves ensuring equitable access to technology and digital resources, particularly for students from disadvantaged backgrounds, to avoid exacerbating existing educational inequalities. The rapid pace of technological change often outstrips the ability of educational institutions to adapt, leading to issues with curriculum integration, teacher preparedness, and infrastructure upgrades. Furthermore, concerns regarding the efficacy of EdTech solutions in truly improving learning outcomes, coupled with the need for robust evidence-based research, remain a persistent challenge. Managing the vast amount of student data generated by EdTech platforms while adhering to stringent privacy regulations adds another layer of complexity. Overcoming these challenges requires collaborative efforts from policymakers, technology providers, educators, and parents to foster a truly inclusive and effective digital learning environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Digital Equity & Addressing the Digital Divide | +3.0% | Global, specific to socio-economic disparities | Long-term (Ongoing) |

| Teacher Training & Professional Development Gaps | +2.5% | Global | Short to Medium-term (2025-2030) |

| Integration with Existing Legacy Systems | +2.0% | Mature Markets (North America, Europe) | Short to Medium-term (2025-2030) |

| Content Quality & Efficacy Verification | +1.8% | Global | Long-term (Ongoing) |

K 12 Education Technology Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the K 12 Education Technology market, offering a detailed understanding of its size, growth trajectory, key trends, and influencing factors. It covers market segmentation by various components, learning models, end-users, and technologies, alongside a thorough regional analysis. The report also identifies significant market drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. Profiles of leading market players are included to offer competitive insights into the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 295.4 Billion |

| Market Forecast in 2033 | USD 1,142.8 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Google for Education, Microsoft Education, Pearson, Blackboard, Instructure (Canvas), Byju's, Chegg, D2L (Brightspace), Edmodo, Knewton, McGraw-Hill Education, Renaissance Learning, Schoology (PowerPowerSchool), Discovery Education, Top Hat, Kahoot!, ClassDojo, Coursera for Campus, Udemy Business, Open Educational Resources (OER) platforms |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The K 12 Education Technology market is extensively segmented to provide a granular view of its diverse landscape and to identify specific growth areas. This segmentation allows for a precise analysis of technological adoption across various educational contexts and user needs. Understanding these distinct segments is crucial for solution providers to tailor their offerings effectively and for educational institutions to make informed procurement decisions that align with their specific requirements and pedagogical goals. The market is primarily broken down by the types of components offered, the predominant learning models adopted, the specific end-user categories, and the underlying technological innovations driving the sector.

Further breakdown within these categories highlights the nuances of market demand. For instance, within solutions, specific tools like Learning Management Systems (LMS) and Assessment Tools represent significant sub-segments, reflecting their critical role in digital learning ecosystems. The distinction between synchronous and asynchronous learning models addresses the flexibility and delivery preferences in education. Analyzing these segments helps in identifying high-growth areas, understanding competitive dynamics, and forecasting future market shifts, enabling stakeholders to develop targeted strategies for product development, market entry, and resource allocation. This comprehensive segmentation framework ensures that all facets of the K 12 EdTech market are thoroughly examined, providing valuable insights for all participants.

- By Component:

- Solutions:

- Learning Management Systems (LMS)

- Content Management Systems (CMS)

- Assessment Tools

- Student Information Systems (SIS)

- Data Analytics Tools

- Others (e.g., Classroom Management, Communication Tools)

- Services:

- Professional Services (Implementation, Consulting)

- Managed Services

- Support Services (Technical Support, Training)

- By Learning Model:

- Blended Learning

- Synchronous Learning

- Asynchronous Learning

- Remote Learning

- By End-User:

- Primary Schools

- Secondary Schools

- Others (e.g., Preschools, Vocational Training Institutions)

- By Technology:

- AI and Machine Learning

- Cloud Computing

- Big Data

- Blockchain

- Internet of Things (IoT)

- Virtual Reality (VR) and Augmented Reality (AR)

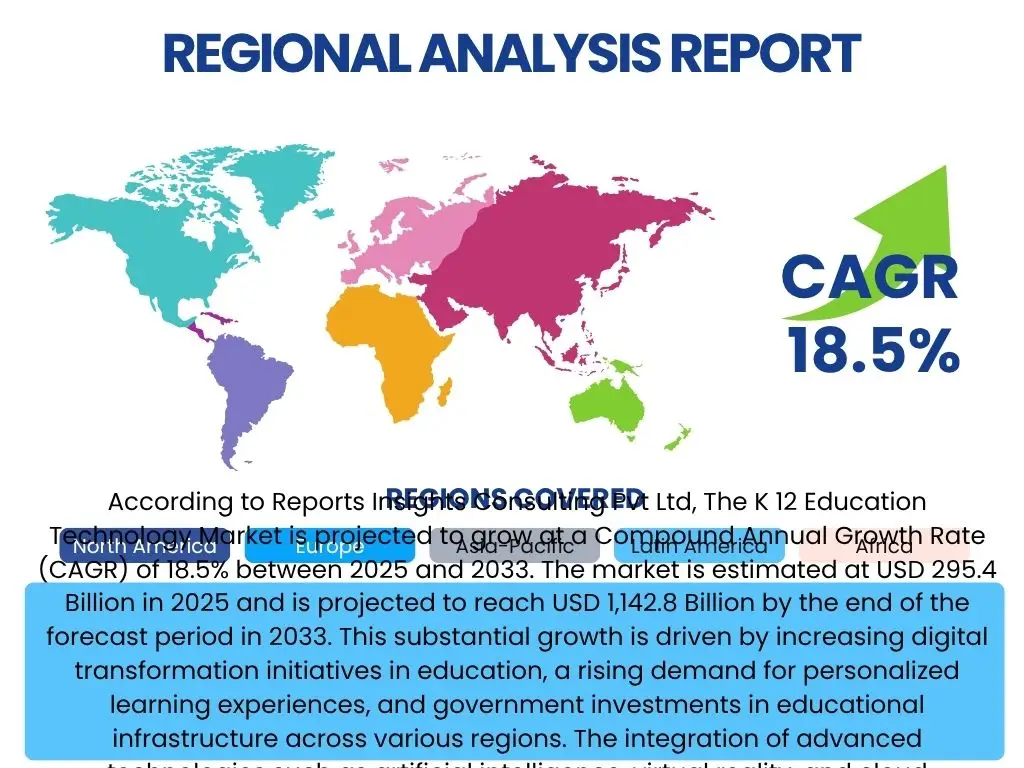

Regional Highlights

Regional analysis is critical to understanding the varied adoption rates, regulatory environments, and investment landscapes that characterize the K 12 Education Technology market globally. Each region presents a unique set of drivers and challenges, influenced by economic development, government policies, and cultural attitudes towards technology in education. This section delineates the key characteristics and market relevance of major geographical areas, offering insights into regional growth opportunities and strategic considerations for market participants. The disparities in digital infrastructure, teacher training capacities, and funding mechanisms across regions significantly impact the pace and nature of EdTech integration, necessitating localized market approaches.

The diverse regional dynamics underscore the importance of tailored strategies for market entry and expansion. While some regions benefit from robust public funding and advanced technological infrastructure, others grapple with issues such as digital exclusion and limited access to resources. This geographical breakdown provides a comprehensive overview of how market forces manifest differently across the globe, guiding stakeholders in prioritizing their efforts and investments. Understanding these regional nuances is essential for developing effective distribution channels, localized content, and culturally appropriate pedagogical solutions, ultimately contributing to more successful and sustainable market penetration in the K 12 EdTech sector.

- North America: A mature market characterized by high adoption rates, significant private and public investments, and a strong focus on personalized learning, AI integration, and data analytics. The U.S. and Canada lead in innovation and pilot new technologies rapidly.

- Europe: Driven by government digital education initiatives and a strong emphasis on data privacy (GDPR). Countries like the UK, Germany, and Nordic nations are at the forefront, focusing on blended learning, digital literacy, and equitable access.

- Asia Pacific (APAC): The fastest-growing region, fueled by large student populations, increasing disposable incomes, and substantial government spending on education modernization, particularly in China, India, and Southeast Asian countries. Focus on online learning, STEM education, and smart classrooms.

- Latin America: Emerging market with increasing internet penetration and government initiatives to bridge the digital divide. Brazil and Mexico are key markets, showing growing demand for affordable digital content and blended learning solutions.

- Middle East and Africa (MEA): A rapidly developing market with significant government investments in digital infrastructure and education reform, particularly in the GCC countries. Opportunities exist in e-learning platforms, vocational training, and basic digital tools, addressing varied levels of technological readiness.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the K 12 Education Technology Market.- Google for Education

- Microsoft Education

- Pearson

- Blackboard

- Instructure (Canvas)

- Byju's

- Chegg

- D2L (Brightspace)

- Edmodo

- Knewton

- McGraw-Hill Education

- Renaissance Learning

- Schoology (PowerSchool)

- Discovery Education

- Top Hat

- Kahoot!

- ClassDojo

- Coursera for Campus

- Udemy Business

- Open Educational Resources (OER) platforms

Frequently Asked Questions

What is K 12 Education Technology?

K 12 Education Technology refers to hardware, software, and digital tools designed to enhance learning, teaching, and administrative processes for students from kindergarten through twelfth grade. It encompasses a wide range of solutions, including learning management systems, interactive whiteboards, educational apps, and virtual reality experiences, all aimed at improving educational outcomes and efficiency.

How is AI impacting K 12 Education Technology?

AI is transforming K 12 Education Technology by enabling personalized learning pathways, automating administrative tasks, and providing data-driven insights for educators. It facilitates adaptive content delivery, intelligent tutoring systems, and predictive analytics, helping to identify student needs and tailor instruction for improved engagement and academic performance.

What are the key drivers for the K 12 EdTech market growth?

Key drivers include increasing internet penetration, widespread adoption of digital devices, supportive government initiatives and funding for digital education, and a growing demand for personalized and adaptive learning experiences. The emphasis on STEM education and skill-based learning also significantly propels market expansion.

What are the primary challenges in K 12 Education Technology adoption?

Major challenges include bridging the digital divide, addressing data privacy and cybersecurity concerns, high initial implementation costs, and the need for comprehensive teacher training and professional development. Integrating new technologies with existing legacy systems also poses a significant hurdle for many educational institutions.

Which regions are leading the K 12 Education Technology market?

North America and Europe are currently leading in K 12 Education Technology adoption due to mature infrastructure and significant investment. However, the Asia Pacific region, particularly China and India, is projected to be the fastest-growing market due to large student populations, increasing digital literacy, and strong government support for educational modernization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted