Isocyanate Market

Isocyanate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703973 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

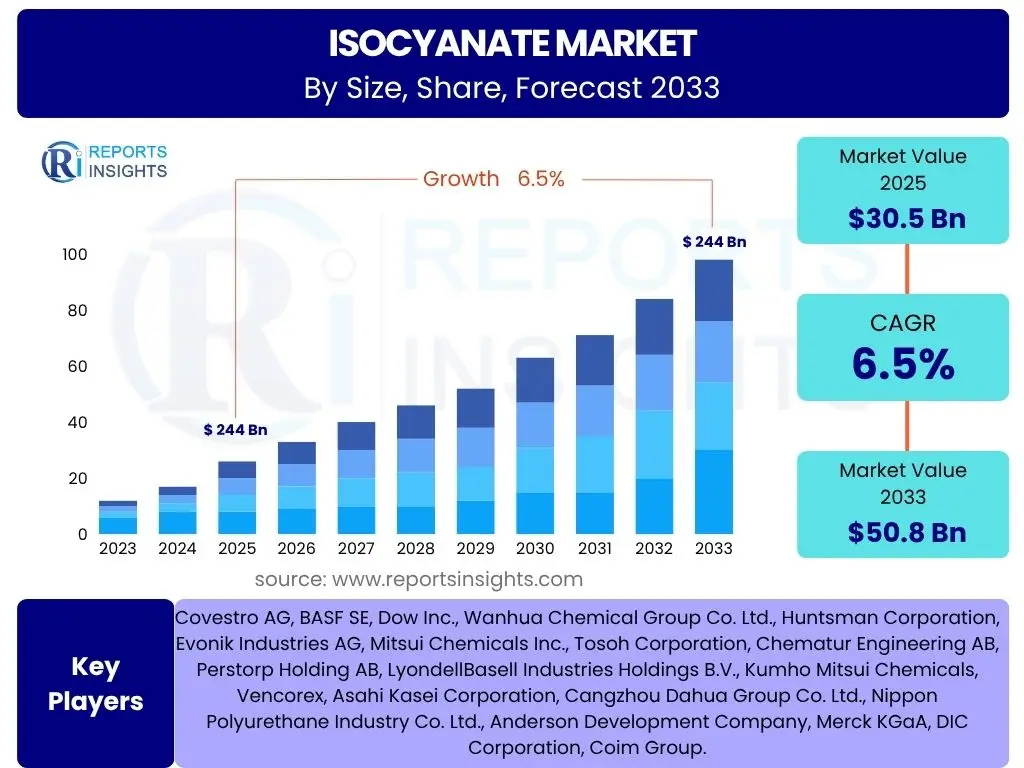

Isocyanate Market Size

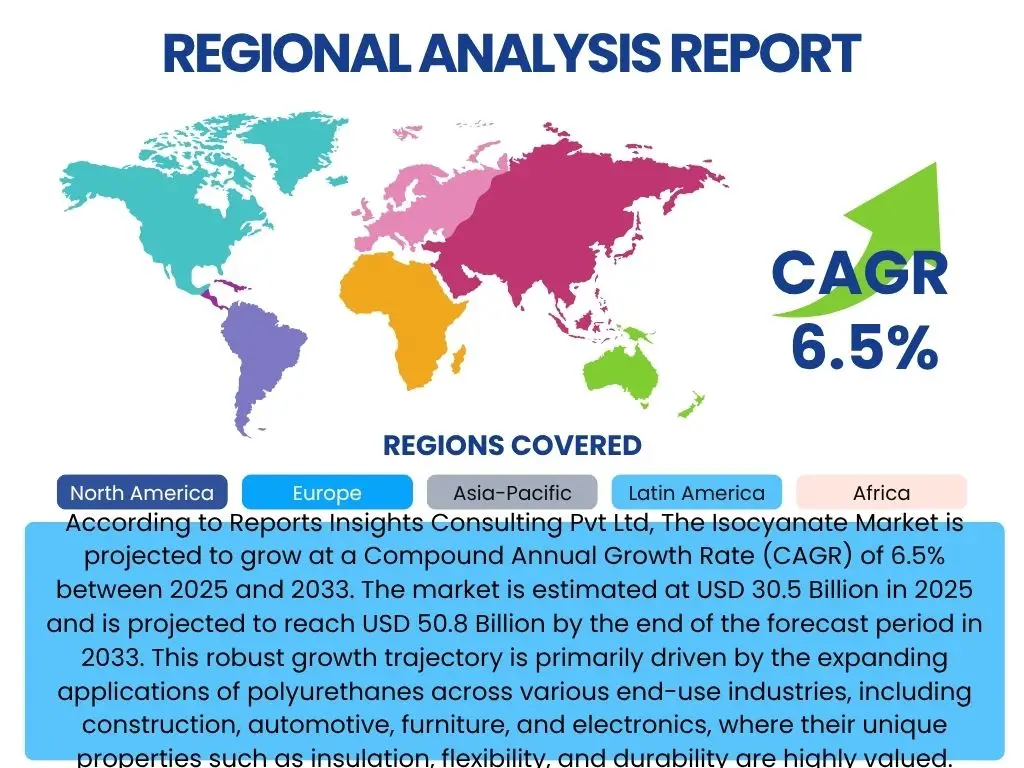

According to Reports Insights Consulting Pvt Ltd, The Isocyanate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 30.5 Billion in 2025 and is projected to reach USD 50.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the expanding applications of polyurethanes across various end-use industries, including construction, automotive, furniture, and electronics, where their unique properties such as insulation, flexibility, and durability are highly valued.

The market's expansion is further fueled by increasing urbanization, particularly in emerging economies, which translates into higher demand for residential and commercial infrastructure. This directly boosts the consumption of rigid and flexible foams, coatings, adhesives, and sealants, all of which heavily rely on isocyanates as key raw materials. Additionally, advancements in material science leading to new polyurethane formulations for specialized applications also contribute significantly to market expansion, ensuring sustained demand throughout the forecast period.

Key Isocyanate Market Trends & Insights

User queries regarding the Isocyanate market frequently revolve around its evolutionary trajectory, particularly concerning sustainability, technological advancements, and shifts in regional demand. There is a discernible interest in how the industry is adapting to environmental regulations and the adoption of greener chemistry. Furthermore, stakeholders often seek information on innovations in application areas and the strategic imperatives driving market participants.

A prominent trend in the Isocyanate market is the increasing focus on sustainability and the development of bio-based or renewable isocyanates. This push is driven by growing environmental concerns, stringent regulatory frameworks, and consumer demand for eco-friendly products. Companies are investing heavily in research and development to produce alternatives to conventional petroleum-derived isocyanates, aiming to reduce carbon footprint and reliance on fossil fuels. This shift is not merely compliance-driven but also an opportunity for differentiation and market leadership.

Another significant trend is the continuous innovation in polyurethane applications, particularly in high-performance segments. This includes the development of more durable coatings for automotive and construction, lightweight foams for improved energy efficiency, and advanced adhesives for complex manufacturing processes. The versatility of polyurethanes allows for customization to specific performance requirements, driving demand across diverse industries. The market is also witnessing a rise in consolidation activities and strategic collaborations, as companies seek to expand their geographical reach, diversify their product portfolios, and enhance their technological capabilities.

- Growing demand for bio-based and sustainable isocyanates.

- Increased adoption of Isocyanates in energy-efficient building insulation.

- Rising demand for lightweight materials in the automotive industry.

- Technological advancements in high-performance polyurethane formulations.

- Shift towards specialized and customized isocyanate solutions.

- Expansion of application areas in electronics and medical devices.

- Stringent regulatory landscape influencing product development and manufacturing processes.

AI Impact Analysis on Isocyanate

Common user questions regarding AI's impact on the Isocyanate market often explore its potential to revolutionize manufacturing processes, enhance supply chain efficiency, and accelerate research and development. Stakeholders are keen to understand how artificial intelligence can optimize production, improve product quality, and contribute to the development of novel Isocyanate derivatives. There is also interest in AI's role in predictive maintenance, safety protocols, and sustainability initiatives within the chemical industry.

Artificial Intelligence (AI) and Machine Learning (ML) are poised to significantly transform the Isocyanate market by optimizing various stages of the value chain. In manufacturing, AI algorithms can analyze vast datasets from production lines to predict equipment failures, optimize reaction conditions for higher yields and purity, and reduce energy consumption. This leads to enhanced operational efficiency, lower production costs, and improved product consistency. Predictive maintenance, powered by AI, minimizes downtime and extends the lifespan of critical machinery, ensuring continuous production flow.

Furthermore, AI is accelerating research and development efforts in the Isocyanate sector. AI-driven computational chemistry can simulate molecular interactions, predict material properties, and screen potential new formulations much faster than traditional laboratory methods. This enables the discovery of novel isocyanate structures, including sustainable and bio-based alternatives, and the development of polyurethanes with enhanced performance characteristics. In supply chain management, AI can optimize logistics, predict demand fluctuations, and manage inventory more effectively, mitigating risks associated with raw material price volatility and supply disruptions, thereby contributing to a more resilient and responsive market.

- Optimization of chemical synthesis and production processes for higher yield and purity.

- Predictive maintenance of manufacturing equipment to reduce downtime and operational costs.

- Acceleration of R&D for novel isocyanate formulations, including bio-based alternatives.

- Enhanced quality control and assurance through real-time data analysis.

- Improved supply chain management, forecasting, and logistics efficiency.

- Development of smart sensors for real-time monitoring of chemical reactions and safety.

- AI-driven sustainability initiatives, such as waste reduction and energy optimization.

Key Takeaways Isocyanate Market Size & Forecast

User inquiries about the key takeaways from the Isocyanate market size and forecast consistently highlight the market's robust growth potential, the critical role of specific end-use industries, and the persistent influence of sustainability and regulatory factors. Stakeholders are particularly interested in understanding the primary drivers sustaining this growth and the emerging opportunities that will shape the market's future trajectory. There is also a focus on identifying the pivotal technological advancements and regional dynamics contributing to the overall market expansion.

The Isocyanate market is set for substantial expansion, driven predominantly by the escalating demand for polyurethanes across diverse applications. The construction sector, with its continuous need for insulation and structural materials, along with the automotive industry's pursuit of lightweight and durable components, will remain primary growth engines. This indicates a sustained fundamental demand for isocyanate chemistries.

A crucial insight is the accelerating shift towards sustainable and bio-based Isocyanate solutions. This transition is not merely a regulatory imperative but a strategic market differentiator, presenting significant opportunities for companies investing in green chemistry. While the market demonstrates resilience, it remains susceptible to raw material price fluctuations and stringent environmental regulations, necessitating strategic adaptation and innovation from market participants to maintain competitive advantage and foster long-term growth.

- The Isocyanate market is projected for significant growth, exceeding USD 50 billion by 2033.

- Polyurethane demand from construction and automotive industries is a primary growth catalyst.

- Sustainability initiatives and bio-based Isocyanate development are critical emerging trends.

- Asia Pacific is expected to remain the dominant and fastest-growing region.

- Technological advancements in high-performance polyurethane will drive new applications.

- Raw material price volatility and regulatory pressures pose notable challenges.

- Strategic collaborations and M&A activities are shaping the competitive landscape.

Isocyanate Market Drivers Analysis

The Isocyanate market is primarily driven by the burgeoning demand from its key end-use industries, most notably construction, automotive, and furniture. The construction sector's sustained growth, fueled by rapid urbanization and infrastructure development, particularly in emerging economies, leads to a high uptake of rigid and flexible polyurethane foams for insulation, roofing, and flooring applications. These materials offer superior thermal efficiency and structural integrity, aligning with global energy conservation efforts and building codes.

In the automotive industry, the increasing emphasis on lightweight vehicle components to improve fuel efficiency and reduce emissions is a significant driver for isocyanates. Polyurethanes provide lightweighting solutions in seating, interior components, and structural parts, without compromising on safety or durability. Furthermore, the rising global population and improving living standards contribute to an increased demand for comfortable and durable furniture, where flexible foams derived from isocyanates are extensively used, ensuring consistent market pull.

Beyond these, the demand for high-performance coatings, adhesives, and sealants (CASE) across various industries such as electronics, marine, and aerospace, further propels the market. These applications require specific properties like chemical resistance, strong adhesion, and weatherability, which polyurethanes effectively provide. Innovation in these specialty applications, coupled with expanding manufacturing activities globally, ensures a broad and diversified demand base for isocyanates.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Construction and Infrastructure Development | +1.8% | Asia Pacific, North America, Europe | Short to Medium-term (2025-2030) |

| Increasing Demand for Lightweight Automotive Components | +1.5% | Europe, North America, China, Japan | Medium to Long-term (2025-2033) |

| Expansion of Furniture and Bedding Industries | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

| Rising Adoption in Coatings, Adhesives, Sealants & Elastomers (CASE) | +1.0% | Global, particularly developed economies | Medium to Long-term (2025-2033) |

| Focus on Energy Efficiency and Green Building Initiatives | +0.8% | Europe, North America, China | Long-term (2028-2033) |

Isocyanate Market Restraints Analysis

Despite robust growth drivers, the Isocyanate market faces significant restraints that can impede its expansion. One of the primary challenges is the volatility of raw material prices, particularly those derived from crude oil, such as benzene and toluene. Fluctuations in crude oil prices directly impact the cost of producing key Isocyanates like MDI and TDI, leading to unstable profit margins for manufacturers and potential price increases for end-users, which can dampen demand or lead to substitution by alternative materials.

Another major restraint involves the stringent environmental regulations and health concerns associated with Isocyanate handling and exposure. Isocyanates are reactive chemicals that can cause respiratory and dermal sensitization upon exposure, leading to occupational health hazards. Regulatory bodies worldwide have imposed strict limits on exposure levels and emissions, necessitating significant investments in safety equipment, ventilation systems, and specialized training, which increases operational costs for manufacturers and end-users alike. These regulations can also limit the expansion of manufacturing facilities in certain regions and push for more capital-intensive, safer production methods.

Furthermore, the availability of substitutes in certain applications, along with public perception and awareness regarding the potential hazards of Isocyanates, can act as a restraint. While polyurethanes offer unique performance advantages, ongoing research into non-isocyanate polyurethanes (NIPUs) and other alternative materials could pose a long-term threat to traditional Isocyanate market dominance in specific niches. The market also grapples with supply chain disruptions, which, while temporary, can lead to raw material shortages and impact production schedules, affecting market stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (e.g., Crude Oil Derivatives) | -1.3% | Global, particularly Asia Pacific (major manufacturing hub) | Short to Medium-term (2025-2030) |

| Stringent Environmental Regulations and Health Concerns | -1.0% | Europe, North America, Japan | Medium to Long-term (2025-2033) |

| Availability of Substitutes and Development of NIPUs | -0.7% | Global, driven by R&D in developed countries | Long-term (2028-2033) |

| High Capital Investment and Production Costs | -0.5% | Global, affecting new market entrants | Short to Medium-term (2025-2030) |

Isocyanate Market Opportunities Analysis

The Isocyanate market is ripe with opportunities driven by innovation, sustainability trends, and expanding applications. A significant opportunity lies in the burgeoning demand for bio-based and sustainable Isocyanates. With increasing environmental consciousness and regulatory pressures, there is a strong impetus for manufacturers to develop and commercialize Isocyanates derived from renewable resources, such as biomass. This not only addresses sustainability concerns but also reduces reliance on fossil fuels, opening new market segments and attracting environmentally conscious consumers and industries. Investment in this area positions companies at the forefront of green chemistry initiatives, offering a competitive advantage.

Another key opportunity stems from the expanding applications of polyurethanes in high-growth industries like renewable energy (wind turbine blades), electronics (encapsulants), and healthcare (medical devices). The unique properties of polyurethanes, such as versatility, durability, and customization capabilities, make them ideal for these specialized and technologically advanced applications. This diversification of end-use industries provides new revenue streams and buffers the market against potential slowdowns in traditional sectors. Furthermore, the development of advanced recycling technologies for polyurethane waste offers a circular economy opportunity, reducing landfill waste and creating a valuable secondary raw material stream.

Emerging economies, particularly in Asia Pacific, Latin America, and Africa, present substantial growth opportunities due to rapid urbanization, industrialization, and improving living standards. These regions are experiencing significant growth in construction, automotive, and consumer goods manufacturing, leading to increased demand for polyurethane products. Strategic investments in manufacturing capacities and distribution networks in these regions can unlock substantial market potential. Collaborations between Isocyanate producers and downstream industries to co-develop innovative solutions tailored to specific market needs also represent a promising avenue for growth and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Commercialization of Bio-based Isocyanates | +1.5% | Europe, North America, Japan | Medium to Long-term (2026-2033) |

| Expanding Applications in Emerging Industries (e.g., Wind Energy, Electronics) | +1.3% | Global, with focus on innovation hubs | Medium to Long-term (2027-2033) |

| Growth in Emerging Economies (Infrastructure, Automotive, Construction) | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

| Advancements in Recycling Technologies for Polyurethane Waste | +0.8% | Europe, North America | Long-term (2029-2033) |

Isocyanate Market Challenges Impact Analysis

The Isocyanate market faces several significant challenges that can impede its growth and stability. One prominent challenge is the complexity of complying with evolving and increasingly stringent environmental, health, and safety (EHS) regulations globally. These regulations govern everything from manufacturing processes, emissions, and waste disposal to the safe handling and transportation of Isocyanates. Meeting these standards often requires substantial capital investments in abatement technologies, process improvements, and employee training, which can inflate operational costs and reduce profitability, particularly for smaller manufacturers or those operating with older infrastructure.

Another critical challenge is the inherent volatility and uncertainty within the global supply chain for raw materials. The production of Isocyanates relies heavily on petrochemical derivatives, whose supply and pricing can be affected by geopolitical events, trade disputes, natural disasters, and global economic fluctuations. Such disruptions can lead to raw material shortages, price spikes, and delays in production, impacting delivery schedules and the overall market equilibrium. The long lead times for certain specialty Isocyanates further exacerbate this challenge, making effective inventory management and strategic sourcing paramount.

Furthermore, managing the public perception and addressing safety concerns related to Isocyanate exposure remains a continuous challenge. Despite industry efforts to promote safe handling practices and personal protective equipment, the association of Isocyanates with potential health risks can deter adoption in sensitive applications or prompt stricter regulatory scrutiny. The industry must continuously invest in education, advocacy, and robust safety protocols to mitigate these concerns. The emergence of new chemical entities and evolving material science also presents a challenge, as the market must adapt to potential shifts in demand towards non-isocyanate alternatives or more sustainable chemical pathways, requiring ongoing innovation and adaptability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Stringent Environmental, Health, and Safety Regulations | -1.2% | Europe, North America, China | Ongoing (2025-2033) |

| Volatile Raw Material Supply Chain and Geopolitical Risks | -1.0% | Global, impacting major manufacturing regions | Short to Medium-term (2025-2030) |

| Public Perception and Safety Concerns Regarding Isocyanate Exposure | -0.8% | Global, influencing consumer-facing applications | Long-term (2028-2033) |

| Need for High Capital Expenditure for Capacity Expansion & Technology Upgrades | -0.6% | Global, affecting new investments | Short to Medium-term (2025-2030) |

Isocyanate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Isocyanate market, offering a detailed understanding of its current landscape, historical performance, and future projections. The scope encompasses market sizing, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages extensive primary and secondary research to deliver actionable insights for stakeholders, including manufacturers, suppliers, end-users, and investors, enabling informed strategic decision-making in a dynamic global chemical industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 30.5 Billion |

| Market Forecast in 2033 | USD 50.8 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Covestro AG, BASF SE, Dow Inc., Wanhua Chemical Group Co. Ltd., Huntsman Corporation, Evonik Industries AG, Mitsui Chemicals Inc., Tosoh Corporation, Chematur Engineering AB, Perstorp Holding AB, LyondellBasell Industries Holdings B.V., Kumho Mitsui Chemicals, Vencorex, Asahi Kasei Corporation, Cangzhou Dahua Group Co. Ltd., Nippon Polyurethane Industry Co. Ltd., Anderson Development Company, Merck KGaA, DIC Corporation, Coim Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Isocyanate market is comprehensively segmented based on type, application, and end-use industry to provide a granular view of its dynamics and growth prospects. This detailed segmentation allows for a precise analysis of demand patterns, technological preferences, and market penetration across various sectors. Each segment exhibits unique characteristics and growth drivers, reflecting the diverse utility of Isocyanates in modern industrial applications. Understanding these segmentations is crucial for identifying niche opportunities and developing targeted market strategies.

By dissecting the market into these segments, stakeholders can discern which Isocyanate types are gaining traction due to specific performance requirements or regulatory advantages, and which applications are experiencing the most significant growth. For instance, the MDI segment dominates due to its widespread use in rigid foams for insulation, driven by global energy efficiency mandates. Conversely, the flexible foam application, largely fueled by the furniture and automotive seating industries, predominantly utilizes TDI. This detailed breakdown highlights the interconnectedness of product chemistry with end-use demand, offering a clear roadmap for investment and product development decisions.

- By Type:

- MDI (Methylene Diphenyl Diisocyanate)

- Polymeric MDI

- Monomeric MDI

- TDI (Toluene Diisocyanate)

- TDI-80/20

- TDI-65/35

- HDI (Hexamethylene Diisocyanate)

- Others (Isophorone Diisocyanate (IPDI), Naphthalene Diisocyanate (NDI), Xylene Diisocyanate (XDI), etc.)

- MDI (Methylene Diphenyl Diisocyanate)

- By Application:

- Rigid Foam

- Building & Construction

- Refrigeration

- Packaging

- Appliances

- Flexible Foam

- Furniture & Bedding

- Automotive Seating

- Packaging

- Coatings

- Automotive

- Industrial

- Wood

- Protective

- Adhesives & Sealants

- Construction

- Automotive

- Packaging

- Footwear

- Elastomers

- Automotive

- Industrial

- Footwear

- Medical

- Binders

- Others

- Rigid Foam

- By End-Use Industry:

- Construction

- Automotive

- Furniture & Bedding

- Packaging

- Electronics & Appliances

- Footwear

- Others (Marine, Medical, Textile, Energy)

Regional Highlights

- Asia Pacific: This region is anticipated to maintain its dominance in the global Isocyanate market, primarily due to rapid industrialization, burgeoning construction activities, and a robust manufacturing base, especially in countries like China, India, and Southeast Asian nations. The increasing demand for affordable housing, infrastructure development, and growing automotive production are key drivers. The region also benefits from lower manufacturing costs and abundant raw material availability, attracting significant investment from global players.

- North America: The North American market for Isocyanates is characterized by a mature but innovation-driven landscape. Growth is propelled by the ongoing demand for energy-efficient building materials, lightweight automotive components, and increasing adoption of specialty polyurethanes in diverse applications. Stringent environmental regulations also drive research into sustainable and bio-based Isocyanate solutions, fostering a market for high-performance and greener products.

- Europe: Europe represents a significant market, distinguished by its strong focus on sustainability, advanced regulatory framework, and emphasis on circular economy initiatives. The demand for Isocyanates is driven by the automotive industry's electrification trend, the construction sector's push for energy-efficient insulation, and a highly developed furniture market. European manufacturers are at the forefront of developing bio-based Isocyanates and advanced recycling technologies for polyurethanes, positioning the region as a leader in green chemistry.

- Latin America: The Latin American Isocyanate market is experiencing steady growth, fueled by urbanization, infrastructure development, and expanding automotive and construction sectors in countries such as Brazil and Mexico. While economic volatility can be a challenge, the region offers long-term growth potential as its industrial base continues to expand and living standards improve, leading to increased demand for polyurethane-based products.

- Middle East and Africa (MEA): The MEA region is poised for substantial growth in the Isocyanate market, primarily due to large-scale construction projects, diversification efforts away from oil-dependent economies, and increasing investments in industrial and manufacturing sectors. The demand for insulation materials in extreme climates and the development of new manufacturing hubs contribute significantly to market expansion, albeit with varying growth rates across different countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Isocyanate Market.- Covestro AG

- BASF SE

- Dow Inc.

- Wanhua Chemical Group Co. Ltd.

- Huntsman Corporation

- Evonik Industries AG

- Mitsui Chemicals Inc.

- Tosoh Corporation

- Chematur Engineering AB

- Perstorp Holding AB

- LyondellBasell Industries Holdings B.V.

- Kumho Mitsui Chemicals

- Vencorex

- Asahi Kasei Corporation

- Cangzhou Dahua Group Co. Ltd.

- Nippon Polyurethane Industry Co. Ltd.

- Anderson Development Company

- Merck KGaA

- DIC Corporation

- Coim Group

Frequently Asked Questions

Analyze common user questions about the Isocyanate market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Isocyanates primarily used for?

Isocyanates are primarily used as essential building blocks for producing polyurethanes, which are versatile polymers found in a wide array of products. Their main applications include rigid and flexible foams for insulation, furniture, and automotive seating; coatings for automotive, industrial, and wood surfaces; adhesives and sealants; and elastomers for various industrial and consumer goods. They are crucial for delivering properties like insulation, durability, flexibility, and strong adhesion.

What are the main types of Isocyanates in the market?

The main types of Isocyanates in the market are Methylene Diphenyl Diisocyanate (MDI), Toluene Diisocyanate (TDI), and Hexamethylene Diisocyanate (HDI). MDI is predominantly used in rigid foams, while TDI is a key component for flexible foams. HDI is primarily utilized in high-performance coatings and elastomers due to its superior weatherability and chemical resistance. Other types, such as IPDI and NDI, serve niche, specialty applications.

What drives the growth of the Isocyanate market?

The growth of the Isocyanate market is primarily driven by the expanding demand for polyurethanes across key end-use industries. These include significant growth in construction and infrastructure development (for insulation and structural materials), the increasing need for lightweight components in the automotive industry (for fuel efficiency), and robust demand from the furniture and bedding sectors. Additionally, advancements in coatings, adhesives, and sealants applications contribute substantially to market expansion.

Are Isocyanates considered hazardous, and how is safety managed?

Yes, Isocyanates are reactive chemicals and can pose health risks, primarily respiratory and dermal sensitization, upon exposure. Safety is managed through stringent environmental, health, and safety (EHS) regulations globally. Manufacturers and users adhere to strict occupational exposure limits, employ engineering controls like ventilation systems, utilize personal protective equipment (PPE), and implement rigorous training programs to ensure safe handling, processing, and disposal of Isocyanates.

What role does sustainability play in the Isocyanate market?

Sustainability is playing an increasingly crucial role in the Isocyanate market. There is a growing focus on developing bio-based or renewable Isocyanates derived from non-fossil resources to reduce environmental footprint and improve resource efficiency. Additionally, efforts are being made to advance recycling technologies for polyurethane waste, contributing to a circular economy. These initiatives are driven by regulatory pressures, corporate sustainability goals, and evolving consumer preferences for greener products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted