IoT Connectivity Market

IoT Connectivity Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705264 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

IoT Connectivity Market Size

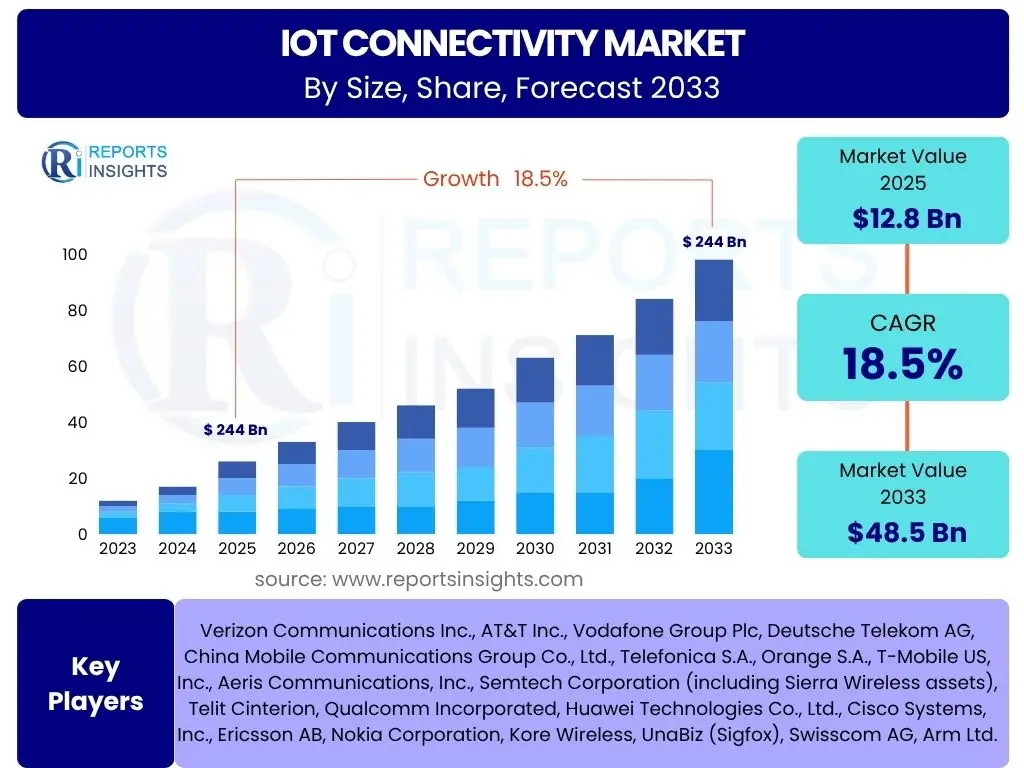

According to Reports Insights Consulting Pvt Ltd, The IoT Connectivity Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 48.5 Billion by the end of the forecast period in 2033.

Key IoT Connectivity Market Trends & Insights

User queries frequently highlight the evolving landscape of network technologies and their impact on IoT adoption. A significant trend involves the widespread deployment of 5G networks, promising enhanced bandwidth, lower latency, and greater device density, which are critical for advanced IoT applications like autonomous vehicles and smart factories. Concurrently, the proliferation of Low Power Wide Area Network (LPWAN) technologies such as LoRaWAN and NB-IoT continues to address the need for cost-effective, long-range, and energy-efficient connectivity for massive IoT deployments, particularly in smart agriculture and asset tracking. Furthermore, the increasing focus on edge computing is driving demand for connectivity solutions that can process data closer to the source, reducing backhaul costs and enabling real-time decision-making, while security concerns necessitate the integration of robust, embedded security features directly into connectivity modules and protocols.

- Proliferation of 5G and private cellular networks for high-bandwidth, low-latency IoT applications.

- Increased adoption of LPWAN technologies (LoRaWAN, NB-IoT, LTE-M) for power-efficient, long-range connectivity.

- Growing integration of edge computing with IoT connectivity to enable real-time data processing and analytics.

- Emergence of satellite IoT for ubiquitous coverage in remote and underserved areas.

- Heightened emphasis on end-to-end security and data privacy within IoT connectivity frameworks.

- Development of hybrid connectivity solutions combining multiple technologies for optimized performance.

- Expansion of IoT connectivity into new vertical markets, including smart healthcare and precision agriculture.

AI Impact Analysis on IoT Connectivity

User inquiries concerning AI's influence on IoT connectivity often revolve around optimization, automation, and enhanced security. Users seek to understand how AI can improve network efficiency, manage vast numbers of connected devices, and derive actionable insights from the immense data generated by IoT ecosystems. There is a strong expectation that AI will streamline connectivity management, automate fault detection, and enable predictive maintenance, thereby reducing operational complexities and costs. Furthermore, the role of AI in enhancing the security posture of IoT networks through anomaly detection and threat prediction is a significant area of interest, alongside its capacity to personalize and optimize connectivity services based on real-time usage patterns.

- AI-driven optimization of network resource allocation and traffic management, leading to improved connectivity reliability and efficiency.

- Enhanced predictive maintenance capabilities for IoT devices and network infrastructure through AI-powered analytics.

- Automated anomaly detection and cybersecurity threat identification, bolstering the security of IoT connectivity.

- Intelligent routing and load balancing within complex IoT networks, ensuring seamless data flow.

- AI-enabled data compression and filtering at the edge, reducing bandwidth requirements and improving data processing speed.

- Personalized and adaptive connectivity services based on real-time user behavior and environmental conditions.

- Facilitation of autonomous decision-making in IoT applications by processing data and executing actions at the edge.

Key Takeaways IoT Connectivity Market Size & Forecast

Common user questions regarding market takeaways often center on growth trajectories, key technological drivers, and significant investment areas. The IoT connectivity market is poised for substantial expansion, driven by the increasing deployment of smart devices across consumer, enterprise, and industrial sectors. This growth is significantly fueled by advancements in cellular technologies like 5G and LPWAN solutions, alongside the integration of artificial intelligence and edge computing for more efficient data handling and enhanced security. Stakeholders are keen on identifying which connectivity types will dominate specific applications and regions, as well as understanding the regulatory environment's impact on market dynamics. The shift towards more robust, scalable, and secure connectivity solutions remains a paramount focus, reflecting a maturation of the IoT ecosystem and a greater emphasis on tangible business value.

- The IoT Connectivity Market is set for robust double-digit CAGR through 2033, indicating strong investor confidence and pervasive adoption.

- 5G and LPWAN technologies are pivotal growth enablers, addressing diverse connectivity needs from high-bandwidth to low-power applications.

- Integration of AI and edge computing is transforming IoT connectivity, enabling real-time analytics and decentralized processing.

- Cybersecurity and data privacy remain critical challenges and key investment areas for sustainable market growth.

- Industrial IoT (IIoT) and smart city initiatives are key application segments driving significant demand for advanced connectivity solutions.

- North America and Asia Pacific are expected to be frontrunners in market expansion due to technological adoption and favorable infrastructure.

- Strategic partnerships and mergers among connectivity providers, module manufacturers, and platform developers are shaping competitive landscapes.

IoT Connectivity Market Drivers Analysis

The burgeoning adoption of Internet of Things devices across various sectors represents a foundational driver for the IoT connectivity market. As more devices become interconnected, the demand for reliable, efficient, and secure communication channels escalates proportionally. This proliferation is not merely confined to consumer electronics but extends profoundly into industrial applications, smart city infrastructure, and healthcare solutions, each requiring tailored connectivity paradigms. Alongside the sheer volume of devices, the increasing need for real-time data analytics and operational insights compels enterprises to invest in sophisticated connectivity frameworks that can support high data throughput and low latency. The ability to collect and analyze data instantaneously from distributed IoT endpoints is becoming a competitive imperative, driving significant investments in next-generation connectivity technologies.

Moreover, the global rollout of 5G networks is profoundly reshaping the IoT connectivity landscape, offering unprecedented speed, massive connection density, and ultra-low latency, which are critical for mission-critical IoT applications like autonomous vehicles, remote surgery, and advanced industrial automation. This technological leap is enabling entirely new use cases and significantly enhancing existing ones. Complementing 5G, government initiatives and smart city projects worldwide are actively promoting the deployment of IoT infrastructure to improve urban living, optimize resource management, and enhance public safety. These large-scale projects necessitate comprehensive and robust connectivity solutions, ranging from cellular to LPWAN and satellite, creating a substantial market pull. Furthermore, ongoing advancements in LPWAN technologies, such as NB-IoT and LoRaWAN, are democratizing IoT deployment by offering cost-effective and energy-efficient solutions for a vast array of low-bandwidth, long-range applications, thereby expanding the market's accessibility to a broader range of industries and use cases.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid proliferation of IoT devices across sectors | +5.2% | Global, particularly APAC and North America | Short to Mid-term (2025-2029) |

| Growing demand for real-time data analytics | +4.8% | North America, Europe, Asia Pacific | Mid-term (2026-2030) |

| Global rollout and adoption of 5G and private networks | +6.1% | North America, China, Europe | Short to Long-term (2025-2033) |

| Government initiatives for smart cities and industries | +3.5% | Asia Pacific, Europe, Middle East | Mid to Long-term (2027-2033) |

| Advancements in LPWAN technologies | +2.9% | Global, especially emerging economies | Short to Mid-term (2025-2029) |

IoT Connectivity Market Restraints Analysis

Despite the promising growth trajectory, the IoT connectivity market faces several significant restraints that could impede its full potential. A primary concern revolves around the high initial investment and deployment costs associated with establishing robust IoT infrastructure. Enterprises, particularly Small and Medium-sized Enterprises (SMEs), often find the upfront capital expenditure for hardware, software platforms, and network setup to be prohibitive. This financial barrier can slow down adoption rates, especially in cost-sensitive industries or developing regions where budget constraints are more prevalent. The complexity involved in integrating diverse IoT devices and systems, often from multiple vendors, further adds to these costs and operational challenges, requiring specialized expertise and considerable time investments.

Another major impediment is the pervasive issue of data security and privacy concerns. As more devices become interconnected and transmit sensitive data, the risk of cyberattacks, data breaches, and unauthorized access increases exponentially. Public and corporate anxieties regarding the vulnerability of IoT networks can deter adoption, especially in critical sectors like healthcare, finance, and defense. Regulatory bodies are increasingly imposing stringent data protection laws, such as GDPR and CCPA, which introduce compliance complexities and financial penalties for non-adherence, thereby adding a layer of burden for IoT solution providers. Furthermore, the lack of standardized protocols and interoperability issues among a vast array of IoT devices, platforms, and connectivity technologies creates fragmentation within the market. This fragmentation makes it challenging to achieve seamless communication and data exchange across different ecosystems, leading to integration headaches, vendor lock-in, and hindering the widespread scalability of IoT deployments. Addressing these interoperability gaps requires collaborative industry efforts and the development of universal standards, which can be a slow and arduous process.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial investment and deployment costs | -3.7% | Global, particularly emerging markets | Short to Mid-term (2025-2029) |

| Data security and privacy concerns | -4.5% | North America, Europe | Short to Long-term (2025-2033) |

| Interoperability challenges among diverse IoT devices | -3.2% | Global | Short to Mid-term (2025-2029) |

| Lack of standardized protocols | -2.8% | Global | Mid to Long-term (2027-2033) |

| Regulatory complexities and compliance issues | -3.0% | Europe, North America | Short to Mid-term (2025-2030) |

IoT Connectivity Market Opportunities Analysis

The IoT connectivity market is replete with significant growth opportunities, particularly stemming from the continuous technological evolution and expanding application domains. The emergence of new cellular IoT technologies such as NB-IoT and LTE-M presents a substantial opportunity by offering low-power, wide-area connectivity optimized for massive IoT deployments. These technologies enable a broader range of use cases, from smart metering to asset tracking, which were previously constrained by power or cost limitations. Their inherent efficiencies make them ideal for battery-operated devices with long lifespans, opening doors to new market segments that require minimal maintenance. Furthermore, the ongoing expansion of IoT into novel verticals, including remote patient monitoring in healthcare and precision agriculture, signifies vast untapped potential. These sectors are increasingly recognizing the transformative power of real-time data and automated processes, driving demand for specialized and robust connectivity solutions that can operate in diverse and often challenging environments.

Another crucial opportunity lies in the deeper integration of Artificial Intelligence (AI) and Machine Learning (ML) with IoT connectivity. AI/ML can unlock significant value by enabling sophisticated data analytics, predictive maintenance, and autonomous decision-making at the edge of the network. This integration enhances the efficiency and intelligence of IoT systems, moving beyond mere data collection to proactive insights and actions, which is highly attractive to enterprises seeking operational excellence. Additionally, the development of more energy-efficient connectivity solutions, encompassing both hardware and software innovations, directly addresses one of the key challenges of IoT deployment – battery life and power consumption. Innovations in chip design, power management protocols, and energy harvesting techniques will significantly extend device longevity, thereby reducing maintenance costs and fostering wider adoption of IoT devices in remote or hard-to-reach locations. The convergence of these technological advancements with growing market demand positions the IoT connectivity market for sustained expansion and diversification into high-value applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of cellular IoT (NB-IoT, LTE-M) | +4.7% | Global, particularly APAC and Europe | Short to Mid-term (2025-2029) |

| Expansion of IoT into new verticals (e.g., healthcare, agriculture) | +4.2% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Integration with Artificial Intelligence and Machine Learning | +5.5% | Global | Short to Long-term (2025-2033) |

| Development of energy-efficient connectivity solutions | +3.8% | Global | Mid-term (2026-2030) |

| Growth of hyper-converged infrastructure for IoT deployment | +3.0% | North America, Europe | Mid to Long-term (2028-2033) |

IoT Connectivity Market Challenges Impact Analysis

The IoT connectivity market faces several inherent challenges that demand innovative solutions for sustained growth and widespread adoption. One of the primary hurdles is managing the immense volume and velocity of data generated by billions of interconnected IoT devices. This data deluge strains existing network infrastructures, necessitating advanced processing capabilities at the edge and efficient backhaul solutions. Ensuring seamless and reliable connectivity across diverse geographical areas and varying environmental conditions, from dense urban settings to remote agricultural fields and harsh industrial environments, presents a significant technical challenge. Different applications require different connectivity characteristics (e.g., low latency for industrial automation, high throughput for video surveillance), leading to complex network architecture design and deployment.

Another critical challenge is addressing the power consumption and battery life limitations of many IoT devices, especially those deployed in remote or difficult-to-access locations. While LPWAN technologies offer improved energy efficiency, a universal solution remains elusive for devices requiring constant connectivity and data transmission without frequent battery replacement or external power sources. This limitation affects the total cost of ownership and feasibility for certain long-term deployments. Furthermore, navigating complex and evolving regulatory landscapes across different countries and regions poses a significant challenge for global IoT deployments. Regulations pertaining to data privacy, spectrum allocation, device certification, and cross-border data transfer can vary widely, creating compliance hurdles for businesses operating internationally. Lastly, a persistent skills gap in specialized areas such as IoT architecture, cybersecurity, and data science limits the effective deployment and management of sophisticated IoT solutions. The scarcity of professionals proficient in integrating and optimizing diverse IoT components often leads to project delays and increased operational costs, hindering market expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing data volume and velocity | -3.9% | Global | Short to Long-term (2025-2033) |

| Ensuring seamless connectivity in diverse environments | -3.5% | Global | Short to Mid-term (2025-2029) |

| Addressing power consumption and battery life limitations | -3.1% | Global | Mid-term (2026-2030) |

| Navigating complex regulatory landscapes | -2.7% | Europe, Asia Pacific, North America | Short to Long-term (2025-2033) |

| Shortage of skilled professionals in IoT deployment | -2.5% | North America, Europe | Short to Long-term (2025-2033) |

IoT Connectivity Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global IoT Connectivity Market, encompassing market size estimations, historical data, and future growth projections from 2025 to 2033. It thoroughly examines key market drivers, restraints, opportunities, and challenges that influence market dynamics. The report offers detailed segmentation analysis by connectivity technology, end-use application, enterprise size, and component, providing a granular view of market performance across various segments. It also delivers regional insights, highlighting market trends and growth prospects across major geographical areas. The competitive landscape analysis includes profiles of leading market players, offering strategic insights into their business operations and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 48.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Verizon Communications Inc., AT&T Inc., Vodafone Group Plc, Deutsche Telekom AG, China Mobile Communications Group Co., Ltd., Telefonica S.A., Orange S.A., T-Mobile US, Inc., Aeris Communications, Inc., Semtech Corporation (including Sierra Wireless assets), Telit Cinterion, Qualcomm Incorporated, Huawei Technologies Co., Ltd., Cisco Systems, Inc., Ericsson AB, Nokia Corporation, Kore Wireless, UnaBiz (Sigfox), Swisscom AG, Arm Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The IoT connectivity market is segmented across multiple dimensions to provide a comprehensive understanding of its intricate structure and diverse application areas. These segments reflect the various technologies enabling connectivity, the industries and purposes for which IoT is deployed, the size of the organizations leveraging these solutions, and the foundational components comprising the connectivity ecosystem. Such segmentation is crucial for identifying specific growth pockets, understanding competitive dynamics within sub-markets, and tailoring solutions to meet distinct user requirements. Each segment plays a vital role in the overall market landscape, contributing to the diverse needs of IoT deployments, from low-power, long-range applications to high-bandwidth, real-time industrial solutions.

The segmentation by connectivity technology highlights the array of communication protocols and standards, ranging from established cellular networks (2G, 3G, 4G, 5G, LTE-M, NB-IoT) to specialized Low Power Wide Area Networks (LPWAN) like LoRaWAN and Sigfox, as well as short-range technologies such as Wi-Fi and Bluetooth. End-use application segmentation categorizes the market based on vertical industries, including smart homes, smart cities, connected health, industrial IoT, and connected vehicles, demonstrating the widespread adoption of IoT across various sectors. Furthermore, the market is differentiated by enterprise size, acknowledging the distinct connectivity needs and resource capabilities of Small and Medium-sized Enterprises (SMEs) versus Large Enterprises. Lastly, the component segmentation dissects the market into hardware (modules, sensors, gateways), software (platforms, analytics), and services (professional services, managed services), illustrating the comprehensive ecosystem required for IoT connectivity solutions.

- By Connectivity Technology:

- Cellular: 2G, 3G, 4G, 5G, LTE-M, NB-IoT

- Low Power Wide Area Network (LPWAN): LoRaWAN, Sigfox, Weightless, Dash7

- Satellite

- Wi-Fi

- Bluetooth

- Ethernet

- NFC

- Zigbee

- By End-Use Application:

- Smart Homes: Home Automation, Smart Appliances

- Smart Cities: Smart Streetlights, Smart Parking, Waste Management

- Connected Health: Remote Patient Monitoring, Wearable Devices

- Industrial IoT (IIoT): Manufacturing, Logistics, Asset Tracking

- Connected Vehicles: Fleet Management, Infotainment

- Agriculture: Precision Farming, Livestock Monitoring

- Retail: Inventory Management, Smart Shelves

- Utilities: Smart Grids, Smart Meters

- By Enterprise Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By Component:

- Hardware: Modules, Sensors, Gateways

- Software: Platforms, Analytics

- Services: Professional Services, Managed Services

Regional Highlights

The IoT Connectivity Market exhibits diverse growth patterns and adoption rates across different geographical regions, influenced by varying levels of technological infrastructure, economic development, regulatory frameworks, and industry-specific demands. Each region presents unique opportunities and challenges, contributing distinctly to the overall market trajectory. Understanding these regional nuances is critical for stakeholders seeking to strategize market entry, expand operations, or optimize their product and service offerings.

North America currently holds a significant share of the IoT Connectivity Market, driven by high technological adoption rates, robust telecommunications infrastructure, and a strong presence of key technology developers and early adopters. The region benefits from substantial investments in 5G deployment, smart city initiatives, and the rapid expansion of Industrial IoT across manufacturing and logistics sectors. The presence of a mature market for connected devices and a culture of innovation further propel growth. Europe is also a key market, characterized by strong regulatory frameworks promoting data privacy and security, which in turn foster trust in IoT solutions. The region's focus on industrial automation, smart energy, and connected healthcare, coupled with ambitious digital transformation agendas, contributes significantly to the demand for diverse IoT connectivity solutions, including a strong uptake of LPWAN technologies for niche applications. Government support for sustainable and efficient urban development further fuels IoT adoption.

Asia Pacific (APAC) is projected to be the fastest-growing region in the IoT Connectivity Market, primarily due to rapid urbanization, burgeoning industrial sectors, and increasing government support for digital initiatives in countries like China, India, Japan, and South Korea. The region's vast population and burgeoning consumer electronics market drive the demand for smart home devices, while large-scale manufacturing bases are accelerating the adoption of IIoT. Investments in 5G infrastructure are substantial, enabling high-speed, low-latency applications that are transforming industries. Latin America and the Middle East & Africa (MEA) are emerging markets for IoT connectivity, characterized by significant potential fueled by developing digital infrastructures, smart city projects, and the need for operational efficiencies in sectors such as oil and gas, agriculture, and logistics. While these regions may face challenges related to infrastructure development and investment, the increasing awareness of IoT benefits and governmental support for digital transformation are paving the way for gradual yet steady growth in IoT connectivity deployments.

- North America: Leading market share due to advanced technological infrastructure, early adoption of 5G, significant investments in IIoT, and widespread smart city initiatives. High demand for cellular and short-range connectivity.

- Europe: Strong market for industrial IoT and smart energy solutions, driven by digital transformation agendas and robust regulatory frameworks for data privacy. Emphasis on LPWAN technologies for efficient resource management.

- Asia Pacific (APAC): Fastest-growing region, fueled by rapid urbanization, large-scale manufacturing, increasing government investments in smart infrastructure, and a booming consumer IoT market. Major investments in 5G deployment.

- Latin America: Emerging market with increasing adoption in smart agriculture, fleet management, and smart city projects, driven by the need for operational efficiency and infrastructure development.

- Middle East and Africa (MEA): Growth driven by large-scale smart city developments, oil and gas sector digitization, and increasing investments in telecommunications infrastructure, particularly for IoT in remote monitoring.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the IoT Connectivity Market.- Verizon Communications Inc.

- AT&T Inc.

- Vodafone Group Plc

- Deutsche Telekom AG

- China Mobile Communications Group Co., Ltd.

- Telefonica S.A.

- Orange S.A.

- T-Mobile US, Inc.

- Aeris Communications, Inc.

- Semtech Corporation (including Sierra Wireless assets)

- Telit Cinterion

- Qualcomm Incorporated

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Ericsson AB

- Nokia Corporation

- Kore Wireless

- UnaBiz (Sigfox)

- Swisscom AG

- Arm Ltd.

Frequently Asked Questions

What is IoT connectivity?

IoT connectivity refers to the network technologies and protocols that enable Internet of Things devices to communicate with each other, with central platforms, and with the cloud. It is the backbone that allows IoT devices to send and receive data, facilitating their core functions such as data collection, remote control, and automation.

What are the main types of IoT connectivity technologies?

The main types of IoT connectivity technologies include cellular (5G, LTE-M, NB-IoT), Low Power Wide Area Networks (LPWAN) like LoRaWAN and Sigfox, short-range wireless technologies such as Wi-Fi and Bluetooth, and satellite connectivity. Each type is optimized for different applications based on factors like range, bandwidth, power consumption, and cost.

How does 5G impact IoT connectivity?

5G significantly impacts IoT connectivity by offering higher bandwidth, ultra-low latency, and massive connection density. These capabilities enable new and advanced IoT applications, particularly in industrial automation, autonomous vehicles, and real-time critical communications, by ensuring faster and more reliable data transmission.

What are the primary security concerns in IoT connectivity?

Primary security concerns in IoT connectivity include data breaches, unauthorized device access, denial-of-service (DoS) attacks, insecure device management, and privacy violations. Robust encryption, secure authentication, regular software updates, and network segmentation are crucial for mitigating these risks.

Which industries are driving the demand for IoT connectivity?

Industries driving the demand for IoT connectivity include manufacturing (Industrial IoT), smart cities (urban infrastructure management), healthcare (remote patient monitoring, connected medical devices), automotive (connected vehicles, fleet management), and agriculture (precision farming). These sectors leverage IoT for efficiency gains, automation, and enhanced service delivery.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted