interposer and fan out wlp Market

interposer and fan out wlp Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700135 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

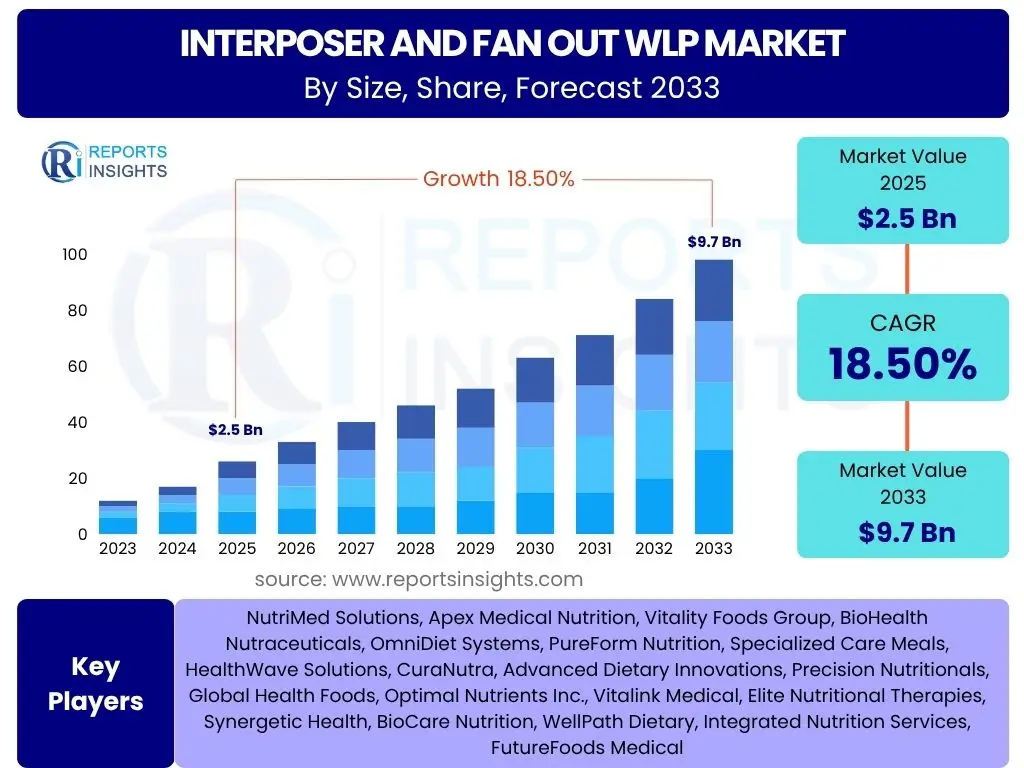

interposer and fan out wlp Market is projected to grow at a Compound annual growth rate (CAGR) of 18.5% between 2025 and 2033, reaching an estimated USD 2.5 billion in 2025 and is projected to grow to approximately USD 9.7 billion by 2033, the end of the forecast period.

Key interposer and fan out wlp Market Trends & Insights

The interposer and fan out Wafer Level Packaging (WLP) market is currently undergoing significant transformation, driven by an insatiable demand for enhanced semiconductor performance, miniaturization, and power efficiency across diverse applications. Key trends shaping this dynamic landscape include the relentless pursuit of heterogeneous integration, where multiple disparate semiconductor components are combined into a single, high-density package to achieve superior functionality and performance. This approach is critical for next-generation computing architectures, including those powering artificial intelligence and high-performance computing.

Furthermore, the market is witnessing a strong shift towards advanced materials and manufacturing processes aimed at improving yield, reducing costs, and enabling finer pitch interconnects. Innovations in interposer materials, such as the increasing exploration of glass and organic interposers alongside traditional silicon, are opening new avenues for improved electrical performance and thermal management. Similarly, the evolution from wafer-level to panel-level fan-out packaging signifies a critical development for scaling production and achieving greater cost efficiencies, making these advanced packaging solutions more accessible for high-volume consumer electronics and automotive applications.

- Miniaturization and ultra-high-density packaging are paramount for compact, powerful devices.

- Heterogeneous integration is accelerating, combining diverse chips for system-in-package solutions.

- Demand for improved power efficiency and thermal management is driving material innovation.

- Adoption of advanced materials like glass and organic interposers is gaining traction.

- Transition from wafer-level to panel-level fan-out packaging aims for cost-effective scaling.

- Increasing complexity of chip designs necessitates advanced interconnect solutions.

- Growth in artificial intelligence, 5G, and automotive electronics fuels market expansion.

AI Impact Analysis on interposer and fan out wlp

Artificial Intelligence (AI) is exerting a profound and transformative impact on the interposer and fan-out WLP market, fundamentally altering demand patterns and technological requirements. The exponential growth in AI and machine learning applications, from data centers and edge computing to autonomous vehicles and advanced consumer electronics, necessitates unprecedented levels of computational power, data throughput, and energy efficiency. Traditional two-dimensional chip architectures are increasingly insufficient to meet these rigorous demands, making advanced packaging solutions like interposers and fan-out WLP indispensable for integrating complex AI accelerators, high-bandwidth memory (HBM), and other critical components into compact, high-performance modules.

The unique capabilities of interposers, particularly their ability to facilitate high-density interconnects between processors and multiple HBM stacks in a 2.5D configuration, are directly enabling the performance breakthroughs required for AI training and inference workloads. Similarly, fan-out WLP solutions provide superior electrical performance, reduced package size, and enhanced thermal dissipation, making them ideal for AI-enabled edge devices and mobile AI applications where space and power consumption are critical constraints. Beyond the direct demand for packaging AI chips, AI is also being leveraged within the semiconductor industry itself for design automation, yield optimization, and predictive maintenance in advanced packaging processes, further accelerating innovation and efficiency in the interposer and fan-out WLP domain.

- AI drives significant demand for high-performance, high-density packaging solutions.

- Interposers are crucial for integrating AI processors with High-Bandwidth Memory (HBM).

- Fan-out WLP supports compact and power-efficient packaging for edge AI devices.

- AI workloads necessitate improved thermal management and signal integrity offered by these technologies.

- The complexity of AI chip architectures mandates heterogeneous integration enabled by interposers.

- AI is increasingly used in optimizing interposer and fan-out WLP design and manufacturing processes.

- Increased data center investment for AI infrastructure directly boosts market demand.

Key Takeaways interposer and fan out wlp Market Size & Forecast

- The interposer and fan out WLP market is poised for robust expansion, projected to achieve a Compound Annual Growth Rate (CAGR) of 18.5% from 2025 to 2033.

- Starting from an estimated market size of USD 2.5 billion in 2025, the market is forecasted to reach approximately USD 9.7 billion by 2033.

- Significant growth drivers include the escalating demand for high-performance computing (HPC), artificial intelligence (AI), and advanced consumer electronics.

- Technological advancements in packaging, such as heterogeneous integration and miniaturization, are key accelerators for market value.

- The shift towards cost-effective panel-level packaging is expected to broaden adoption across various end-use sectors.

- Emerging applications in automotive electronics, 5G infrastructure, and the Internet of Things (IoT) will contribute substantially to market expansion.

- Regional growth will be prominently led by Asia Pacific due to its dominant semiconductor manufacturing ecosystem.

interposer and fan out wlp Market Drivers Analysis

The interposer and fan out WLP market is propelled by a confluence of powerful drivers stemming from the evolving demands of the digital era. A primary catalyst is the relentless pursuit of higher performance and greater functionality in electronic devices, which necessitates advanced packaging solutions capable of accommodating more transistors and integrating diverse components within increasingly smaller footprints. Traditional packaging methods are reaching their physical and electrical limits, making interposers and fan-out WLP critical for achieving the density and interconnectivity required for next-generation processors, memory, and specialized accelerators.

Another significant driver is the explosive growth of data-intensive applications, including artificial intelligence, machine learning, and high-performance computing. These applications demand unprecedented bandwidth and low latency, which interposers facilitate by enabling 2.5D and 3D integration of logic and high-bandwidth memory (HBM). Concurrently, the proliferation of 5G connectivity, the Internet of Things (IoT), and advanced automotive electronics also fuels market expansion. These sectors require highly integrated, power-efficient, and compact modules that fan-out WLP readily provides, enabling smaller form factors and enhanced thermal management crucial for their widespread deployment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Computing (HPC) and AI | +6.5% | North America, Asia Pacific (China, South Korea, Taiwan) | Short to Long-term |

| Miniaturization and Heterogeneous Integration Requirements | +5.0% | Global, especially Asia Pacific | Short to Mid-term |

| Growth in Advanced Consumer Electronics and 5G Connectivity | +3.5% | Asia Pacific, Europe, North America | Short to Mid-term |

| Rising Adoption in Automotive Electronics and ADAS | +2.0% | Europe, North America, Asia Pacific (Japan, South Korea) | Mid to Long-term |

| Demand for Improved Power Efficiency and Thermal Management | +1.5% | Global | Short to Mid-term |

interposer and fan out wlp Market Restraints Analysis

Despite the robust growth trajectory, the interposer and fan out WLP market faces several notable restraints that could temper its expansion. A significant hurdle is the inherently high manufacturing cost associated with these advanced packaging technologies. The intricate processes involved, including high-precision lithography, micro-bumping, and complex bonding techniques, require substantial capital investment in specialized equipment and highly skilled labor. This elevated cost per package, particularly for interposers, can make them economically unfeasible for certain price-sensitive applications, thus limiting broader adoption in segments where conventional packaging solutions still offer a more favorable cost-performance ratio.

Furthermore, the complexity of design and fabrication processes presents another formidable challenge. Yield management remains a critical concern, as defects at any stage of the multi-step packaging process can significantly impact overall profitability. Integrating multiple chips on an interposer or within a fan-out structure requires meticulous design optimization for signal integrity, power delivery, and thermal dissipation, demanding extensive research and development efforts. Additionally, the nascent stage of some advanced materials and the lack of universal standardization across different manufacturing platforms can slow down broader market penetration and create interoperability issues, further acting as a restraint on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital Expenditure | -3.0% | Global, particularly emerging economies | Short to Mid-term |

| Complexity of Design and Fabrication Processes | -2.5% | Global, especially smaller players | Short to Mid-term |

| Yield Management Challenges and Defect Rates | -2.0% | Global | Short to Mid-term |

| Supply Chain Vulnerabilities and Geopolitical Tensions | -1.5% | Global, with emphasis on Asia Pacific | Short-term |

| Limited Adoption in Price-Sensitive Mass-Market Applications | -1.0% | Global | Mid-term |

interposer and fan out wlp Market Opportunities Analysis

The interposer and fan out WLP market is brimming with promising opportunities driven by technological advancements and the expansion of new application areas. A significant opportunity lies in the continued proliferation of artificial intelligence and machine learning technologies, which inherently demand high-density, low-latency packaging solutions. As AI models become more complex and sophisticated, the need for efficient integration of specialized AI accelerators with high-bandwidth memory will surge, creating a sustained demand for interposers that enable these performance gains. Furthermore, the ongoing global rollout of 5G and future 6G networks presents another vast opportunity, as these require compact, high-frequency modules that benefit immensely from the superior electrical performance and reduced form factor offered by fan-out WLP.

Beyond telecommunications, the burgeoning automotive electronics sector, particularly advancements in autonomous driving and advanced driver-assistance systems (ADAS), represents a compelling growth avenue. These applications require robust, high-reliability packaging for complex sensor fusion, AI processors, and communication modules, areas where interposer and fan-out WLP excel. Moreover, the evolution of panel-level packaging, which promises to significantly reduce the cost per chip compared to traditional wafer-level processes, stands as a transformative opportunity. This cost reduction could unlock new mass-market applications and accelerate the mainstream adoption of these advanced packaging technologies across a wider range of consumer devices and industrial IoT solutions, fostering long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI and Machine Learning Hardware | +4.0% | North America, Asia Pacific, Europe | Short to Long-term |

| Advancements in 5G and Future 6G Infrastructure | +3.0% | Asia Pacific, North America, Europe | Short to Mid-term |

| Expansion into Automotive ADAS and Autonomous Driving | +2.5% | Europe, North America, Asia Pacific | Mid to Long-term |

| Development of Panel-Level Packaging (PLP) for Cost Reduction | +2.0% | Asia Pacific, Global | Mid to Long-term |

| Growth in IoT Devices and Edge Computing | +1.5% | Global | Short to Mid-term |

interposer and fan out wlp Market Challenges Impact Analysis

The interposer and fan out WLP market, while experiencing significant growth, must navigate several inherent challenges that demand continuous innovation and strategic responses. One prominent challenge is effective thermal management, particularly as packaging densities continue to increase with more integrated components and higher power dissipation. The ability to efficiently dissipate heat from these highly concentrated chip architectures is crucial to ensuring device reliability and performance, requiring sophisticated thermal solutions and innovative material science. Maintaining signal integrity at extremely high frequencies and data rates across complex interposer and fan-out structures also poses a considerable technical hurdle, necessitating advanced simulation and design techniques to mitigate signal loss and crosstalk.

Another significant challenge revolves around the standardization of manufacturing processes and materials across the diverse ecosystem of foundries, outsourced semiconductor assembly and test (OSAT) providers, and integrated device manufacturers (IDMs). The lack of universal standards can lead to interoperability issues, complicate supply chain management, and potentially slow down the adoption of these technologies. Furthermore, the substantial investment required for establishing and upgrading manufacturing facilities with the necessary precision equipment for interposer and fan-out WLP poses a barrier to entry for new players and represents a continuous financial commitment for existing ones. Overcoming these challenges will be critical for the sustained and broad-based expansion of the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management Issues in High-Density Packaging | -2.8% | Global | Short to Mid-term |

| Maintaining Signal Integrity at High Frequencies | -2.3% | Global | Short to Mid-term |

| Lack of Industry Standardization and Interoperability | -1.8% | Global, particularly cross-platform | Mid-term |

| High R&D Investment and Time-to-Market Pressures | -1.3% | Global | Short to Mid-term |

| Competition from Alternative Packaging Technologies | -0.8% | Global | Long-term |

interposer and fan out wlp Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the interposer and fan out WLP market, providing stakeholders with crucial insights into its current state, growth trajectory, and future potential. The report meticulously covers key market dynamics, including detailed drivers, restraints, opportunities, and challenges that are shaping the industry landscape. It delves into strategic recommendations for market players, enabling informed decision-making and competitive advantage. The scope encompasses a detailed segmentation analysis, offering a granular view of the market across various types, applications, and end-use industries, alongside a thorough regional and country-level examination to highlight key growth pockets and investment opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 billion |

| Market Forecast in 2033 | USD 9.7 billion |

| Growth Rate | 18.5% CAGR from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Packaging Solutions Inc., Global Semiconductor Packaging Group, Precision Interconnects Ltd., Integrated Wafer Services, Fan-Out Technologies Corp., NextGen Packaging Solutions, Advanced Micro-Devices Packaging, High-Density Integration Co., Wafer Level Innovations, Silicon Interposer Systems, Enabling Technologies Group, Universal Packaging Services, Quantum Packaging Labs, Frontier Semiconductor Solutions, Innovative Microelectronics, Elite Packaging Systems, MegaChips Advanced Packaging, Zenith Interconnect Solutions, Apex Advanced Packaging, CoreTech Semiconductor |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The interposer and fan out WLP market is intricately segmented to provide a granular understanding of its diverse components and their respective growth dynamics. This segmentation facilitates targeted analysis, enabling stakeholders to identify specific niches and opportunities within the broader market landscape. Understanding these segments is crucial for strategic planning, product development, and market entry strategies, as each segment is influenced by unique technological requirements, application demands, and competitive dynamics. The report details these segments across type, application, and end-use industry, providing a comprehensive framework for market assessment.

- By Type: This segment categorizes the market based on the specific packaging technology or interposer material utilized.

- Silicon Interposer: Traditional and widely adopted, silicon interposers provide a robust platform for 2.5D/3D integration, particularly for high-performance computing and AI applications requiring high-density interconnects.

- Glass Interposer: Emerging as an alternative, glass interposers offer advantages such as lower dielectric constant, potential for larger panel sizes, and better electrical performance, making them suitable for high-frequency applications.

- Organic Interposer: These interposers leverage organic laminate materials, offering flexibility, lower cost, and compatibility with various substrate technologies, often used in applications where cost-efficiency and moderate performance are key.

- Fan-out Wafer Level Packaging (FoWLP): A proven packaging solution that redistributes the die to a larger area at the wafer level, enabling more I/O pins, better thermal performance, and smaller package footprints, highly adopted in mobile and automotive sectors.

- Fan-out Panel Level Packaging (FoPLP): An advanced evolution of FoWLP, utilizing larger square or rectangular panels instead of circular wafers to achieve significant cost reductions and higher throughput, poised for mass-market adoption.

- By Application: This segment analyzes the market based on the end-use applications where interposer and fan out WLP technologies are deployed, reflecting the diverse industries benefiting from these advanced packaging solutions.

- High-Performance Computing (HPC): Includes supercomputers, servers, and data center applications demanding extreme processing power and bandwidth, heavily reliant on interposers for integrating CPUs, GPUs, and HBM.

- Artificial Intelligence (AI) and Machine Learning (ML): Dedicated hardware for AI training and inference, requiring advanced packaging for accelerators and high-bandwidth memory to manage massive data flows.

- Consumer Electronics: Encompasses a wide range of devices such as smartphones, tablets, wearables, and gaming consoles, where miniaturization, power efficiency, and performance are paramount, often utilizing fan-out WLP.

- Automotive: Includes components for Advanced Driver-Assistance Systems (ADAS), infotainment systems, and power electronics, demanding high reliability, robust performance, and compact size in harsh environments.

- Networking and Telecommunications: Covers equipment for 5G infrastructure, network routers, switches, and data center networking, requiring high-speed data transmission and integrated solutions.

- Industrial: Applications in industrial automation, robotics, and smart manufacturing, where ruggedness, reliability, and high-performance processing are essential for control systems and sensors.

- Medical Devices: Specialized applications in medical imaging, diagnostics, and implantable devices, where miniaturization, low power consumption, and high reliability are critical.

- By End-use Industry: This segment categorizes the market based on the primary entities involved in the design, manufacturing, and assembly of semiconductor devices, showcasing the ecosystem of advanced packaging.

- Semiconductor Foundries: Companies that manufacture integrated circuits for other companies, increasingly offering advanced packaging services like interposer and fan-out WLP to their clients.

- Outsourced Semiconductor Assembly and Test (OSAT) Companies: Specialized firms providing semiconductor assembly, packaging, and test services, playing a crucial role in the supply chain for advanced packaging.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and market their own integrated circuits, often integrating advanced packaging capabilities in-house.

- Fabless Semiconductor Companies: Firms that design semiconductor devices but outsource the manufacturing and often the packaging, relying heavily on foundries and OSATs for advanced packaging needs.

Regional Highlights

The global interposer and fan out WLP market exhibits distinct regional dynamics, with certain geographies playing pivotal roles due to their established semiconductor ecosystems, technological leadership, and significant end-use application demand. Asia Pacific stands as the undisputed leader, driven by the presence of major semiconductor manufacturing hubs and a robust supply chain for advanced packaging. North America and Europe also contribute significantly, primarily due to strong research and development initiatives, demand from high-performance computing sectors, and advancements in automotive electronics.

- Asia Pacific (APAC):

- Dominates the market share due to the concentration of leading semiconductor foundries, OSATs, and integrated device manufacturers (IDMs) in countries like Taiwan, South Korea, China, and Japan.

- High demand from consumer electronics manufacturing, particularly smartphones and other portable devices, drives the adoption of fan-out WLP.

- Increasing investments in AI data centers and 5G infrastructure across the region further fuel the demand for high-performance interposer-based solutions.

- Government support and favorable policies for semiconductor industry development contribute significantly to market growth.

- North America:

- A significant hub for advanced research and development in semiconductor technology and packaging, particularly for high-performance computing (HPC) and artificial intelligence applications.

- Presence of major fabless semiconductor companies and leading technology innovators drives the demand for cutting-edge interposer and fan-out solutions.

- Strong investment in data centers, cloud computing infrastructure, and defense sectors necessitates robust and high-density packaging.

- Growth in the automotive sector, especially in autonomous vehicle development, is contributing to regional market expansion.

- Europe:

- Known for its strong automotive industry and growing focus on industrial automation, driving the demand for reliable and compact semiconductor packaging.

- Increasing investment in R&D for advanced materials and packaging technologies, particularly in countries like Germany and France.

- Development of regional semiconductor manufacturing capabilities and initiatives to strengthen the domestic supply chain contribute to market growth.

- Demand from telecommunications and medical device sectors also plays a role in the adoption of advanced packaging solutions.

- Latin America & Middle East and Africa (MEA):

- Currently represent smaller market shares but are expected to witness gradual growth driven by increasing industrialization, digital transformation initiatives, and growing adoption of consumer electronics and telecommunication infrastructure.

- While not leading in manufacturing, these regions are significant consumers of packaged semiconductors, creating opportunities for market expansion in the long term.

Top Key Players:

The market research report covers the analysis of key stake holders of the interposer and fan out wlp Market. Some of the leading players profiled in the report include -

- Advanced Packaging Solutions Inc.

- Global Semiconductor Packaging Group

- Precision Interconnects Ltd.

- Integrated Wafer Services

- Fan-Out Technologies Corp.

- NextGen Packaging Solutions

- Advanced Micro-Devices Packaging

- High-Density Integration Co.

- Wafer Level Innovations

- Silicon Interposer Systems

- Enabling Technologies Group

- Universal Packaging Services

- Quantum Packaging Labs

- Frontier Semiconductor Solutions

- Innovative Microelectronics

- Elite Packaging Systems

- MegaChips Advanced Packaging

- Zenith Interconnect Solutions

- Apex Advanced Packaging

- CoreTech Semiconductor

Frequently Asked Questions:

What is an interposer in semiconductor packaging?

An interposer is a passive substrate used in advanced semiconductor packaging to provide an electrical interface between multiple integrated circuits (ICs) and a larger package or circuit board. It enables high-density, fine-pitch interconnections between chips, typically in 2.5D or 3D stacking configurations, facilitating superior performance, power efficiency, and reduced form factors for complex electronic systems.

How does fan-out Wafer Level Packaging (WLP) differ from traditional packaging?

Fan-out WLP is an advanced packaging technology where the semiconductor die is redistributed onto a larger area before molding and creating interconnects. Unlike traditional packaging, it allows for more input/output (I/O) connections directly from the chip, eliminates the need for a substrate, offers better thermal performance, and achieves a smaller overall package size, making it ideal for compact and high-performance devices.

What are the primary applications of interposer and fan-out WLP technologies?

Interposer and fan-out WLP technologies are primarily used in applications demanding high performance, miniaturization, and power efficiency. Key applications include high-performance computing (HPC), artificial intelligence (AI) and machine learning (ML) accelerators, advanced consumer electronics (e.g., smartphones, wearables), automotive electronics (e.g., ADAS, autonomous driving), and 5G/telecommunications infrastructure.

What are the key drivers for the growth of the interposer and fan out WLP market?

The key drivers for market growth include the increasing demand for high-performance computing (HPC) and AI, the continuous trend of miniaturization in electronic devices, the necessity for heterogeneous integration of diverse chip functionalities, and the rapid expansion of advanced consumer electronics, 5G networks, and automotive electronics requiring sophisticated packaging solutions.

What is the projected market size and growth rate for interposer and fan out WLP?

The interposer and fan out WLP market is projected to reach approximately USD 9.7 billion by 2033, growing from an estimated USD 2.5 billion in 2025. This represents a robust Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, driven by sustained demand for advanced semiconductor packaging across multiple high-growth industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted