Inflight Connectivity Equipment Market

Inflight Connectivity Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706523 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Inflight Connectivity Equipment Market Size

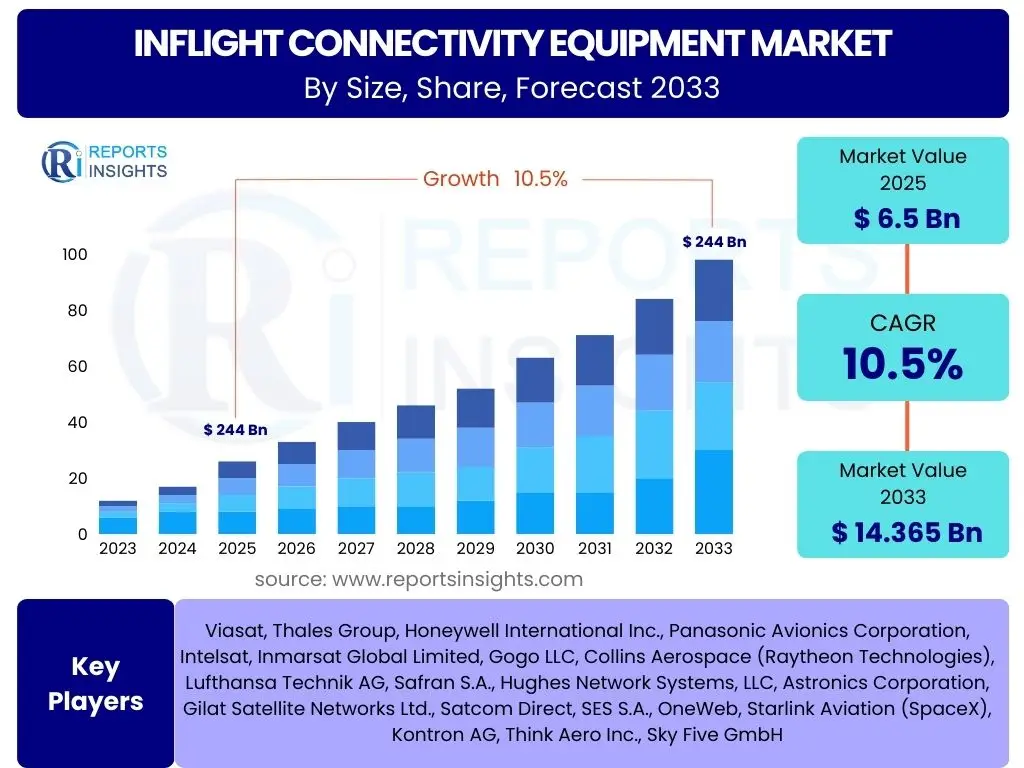

According to Reports Insights Consulting Pvt Ltd, The Inflight Connectivity Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 6.5 billion in 2025 and is projected to reach USD 14.365 billion by the end of the forecast period in 2033.

Key Inflight Connectivity Equipment Market Trends & Insights

The Inflight Connectivity Equipment market is currently experiencing significant shifts driven by evolving passenger expectations and rapid technological advancements. Users are increasingly demanding seamless, high-speed internet access similar to their home or office environments, pushing airlines to upgrade their existing connectivity infrastructure. This trend is further amplified by the proliferation of personal electronic devices and the growing consumption of streaming content onboard. As a result, the industry is witnessing a robust adoption of advanced satellite technologies and a strong focus on enhancing the overall passenger experience through reliable and fast internet services.

Airlines are recognizing inflight connectivity not just as a luxury but as a crucial differentiator and a potential source of ancillary revenue. The market is thus trending towards more sophisticated systems that can support a wide range of applications, from basic browsing to high-definition video streaming and even corporate VPN access. The integration of 5G technologies and the expansion of Low Earth Orbit (LEO) satellite constellations are pivotal in addressing the growing bandwidth demands, promising unprecedented speeds and reduced latency. This push towards enhanced performance and broader coverage is shaping the competitive landscape and driving innovation within the market.

- Deployment of High-Throughput Satellites (HTS) and Non-Geostationary Orbit (NGSO) constellations (LEO, MEO) for increased bandwidth and lower latency.

- Integration of 5G technology into existing and future inflight connectivity systems to enhance speed and reliability.

- Growing demand for personalized inflight entertainment and connectivity (IFEC) services, leveraging passenger data.

- Rise of hybrid connectivity solutions combining satellite and air-to-ground (ATG) technologies for optimized performance and cost efficiency.

- Emphasis on cybersecurity measures to protect passenger data and aircraft operational systems from potential threats.

AI Impact Analysis on Inflight Connectivity Equipment

Artificial Intelligence (AI) is poised to revolutionize the Inflight Connectivity Equipment market by optimizing network performance and enhancing the passenger experience. Users are curious about how AI can lead to more stable connections, predictive maintenance, and personalized services. AI algorithms can dynamically manage network traffic, allocate bandwidth more efficiently, and anticipate potential connectivity issues before they impact service quality. This proactive approach ensures a more reliable and consistent internet experience for passengers, reducing complaints and improving overall satisfaction.

Beyond network optimization, AI's influence extends to personalization and operational efficiency. AI-powered analytics can process vast amounts of passenger data to offer tailored content, advertisements, and service recommendations, transforming the inflight experience into a highly customized journey. Furthermore, AI contributes significantly to predictive maintenance of connectivity hardware, allowing airlines to identify and address potential equipment failures before they occur, thereby minimizing downtime and maintenance costs. The integration of AI tools promises a smarter, more resilient, and user-centric future for inflight connectivity.

- Predictive maintenance of inflight connectivity hardware, reducing downtime and operational costs.

- Dynamic bandwidth allocation and network traffic management for optimized performance and stability.

- Personalized content delivery and advertising based on passenger preferences and browsing history.

- Enhanced cybersecurity through AI-driven threat detection and anomaly identification.

- Automated fault diagnosis and self-healing capabilities for connectivity systems, improving reliability.

Key Takeaways Inflight Connectivity Equipment Market Size & Forecast

The Inflight Connectivity Equipment market is set for robust expansion, driven by the escalating demand for seamless digital experiences onboard aircraft. Common user questions highlight a keen interest in understanding the primary forces behind this growth and the long-term outlook. The market's significant Compound Annual Growth Rate (CAGR) underscores the critical role connectivity now plays in passenger satisfaction and airline operational strategies. This trajectory is supported by continuous advancements in satellite and ground-based communication technologies, which are making high-speed, reliable internet accessible even at cruising altitudes.

A key insight is the shift from connectivity as a premium amenity to an expected standard, influencing aircraft purchasing decisions and cabin modernization efforts. Airlines are increasingly viewing inflight connectivity as an essential component of their competitive strategy, allowing them to differentiate services, generate ancillary revenue, and enhance operational efficiency through real-time data exchange. The forecast indicates sustained investment in next-generation systems, emphasizing higher bandwidth, lower latency, and expanded global coverage to meet the ever-growing needs of both passengers and airline operations.

- Strong market growth fueled by increasing passenger expectations for continuous connectivity.

- Technological advancements, particularly in satellite communications (HTS, LEO), are pivotal in expanding bandwidth and reducing latency.

- Airlines are prioritizing inflight connectivity as a core service offering to enhance passenger satisfaction and generate ancillary revenue.

- The market is transitioning towards more sophisticated, high-performance systems capable of supporting data-intensive applications.

- Significant investment is anticipated in infrastructure upgrades and the adoption of hybrid connectivity solutions across commercial and business aviation sectors.

Inflight Connectivity Equipment Market Drivers Analysis

The Inflight Connectivity Equipment market is primarily driven by the escalating demand for a connected experience among air travelers, mirroring the pervasive connectivity they experience on the ground. Passengers increasingly expect uninterrupted access to internet services, including social media, email, and streaming platforms, throughout their journey. This surge in demand compels airlines to invest in advanced connectivity solutions to enhance passenger satisfaction and maintain a competitive edge. The proliferation of personal electronic devices (PEDs) among passengers further amplifies this need, as individuals rely on their smartphones, tablets, and laptops for entertainment, work, and communication while flying.

Technological advancements, particularly in satellite communication, represent another critical driver. The deployment of High-Throughput Satellites (HTS) and the emergence of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations are revolutionizing the capabilities of inflight connectivity. These technologies offer significantly higher bandwidth, lower latency, and broader global coverage compared to traditional systems, enabling airlines to provide a more robust and reliable internet service. Additionally, the continuous increase in global air traffic and the delivery of new aircraft equipped with factory-installed connectivity solutions are expanding the addressable market, creating a sustained demand for modern inflight connectivity equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Passenger Demand for Seamless Connectivity | +2.3% | Global, particularly North America, Europe, Asia Pacific | Short-term to Long-term |

| Technological Advancements in Satellite Communication (HTS, LEO/MEO) | +2.0% | Global | Medium-term to Long-term |

| Growing Number of Aircraft Deliveries and Fleet Modernization | +1.8% | Asia Pacific, North America | Medium-term |

| Airlines' Focus on Enhancing Passenger Experience and Ancillary Revenue | +1.5% | Global | Short-term to Medium-term |

| Proliferation of Personal Electronic Devices (PEDs) | +1.2% | Global | Short-term |

Inflight Connectivity Equipment Market Restraints Analysis

Despite significant growth prospects, the Inflight Connectivity Equipment market faces several formidable restraints. One of the primary inhibitors is the high initial investment cost associated with installing and upgrading inflight connectivity systems. Equipping an entire fleet with state-of-the-art hardware, including antennas, modems, and routing equipment, along with the necessary software and integration services, represents a substantial capital expenditure for airlines. This financial burden can be particularly challenging for smaller airlines or those operating with tighter budgets, potentially delaying the adoption of advanced connectivity solutions and limiting market penetration in certain segments.

Another significant restraint is the complex regulatory environment and spectrum availability issues across different regions. Airlines must navigate a patchwork of national and international regulations concerning the use of communication frequencies, equipment certification, and data privacy. Obtaining the necessary licenses and ensuring compliance can be a lengthy and intricate process, adding to the operational complexities and costs. Furthermore, the limited availability of suitable spectrum in certain areas or the need for constant updates to comply with evolving standards can hinder the deployment and optimize performance of inflight connectivity services, thereby impacting the market's overall growth trajectory.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Installation and Maintenance Costs | -1.1% | Global, particularly emerging markets | Short-term to Medium-term |

| Complex Regulatory Environment and Spectrum Availability Challenges | -0.9% | Global, varies by region | Medium-term |

| Cybersecurity Concerns and Data Privacy Risks | -0.8% | Global | Short-term to Long-term |

| Limited Bandwidth and Latency Issues in Remote Areas | -0.6% | Specific remote routes | Short-term |

| Competitive Pressure from Ground-Based Connectivity Solutions | -0.5% | Global | Medium-term |

Inflight Connectivity Equipment Market Opportunities Analysis

The Inflight Connectivity Equipment market is ripe with opportunities, particularly in underserved regions and the burgeoning low-cost carrier segment. While premium airlines in developed markets have largely adopted connectivity solutions, significant potential exists in emerging economies where air travel is expanding rapidly but connectivity services are nascent. Airlines in these regions are increasingly looking to implement cost-effective and scalable connectivity solutions to attract new passengers and enhance their service offerings. This presents a substantial growth avenue for providers capable of offering flexible and regionally optimized deployment models, driving market penetration in previously untapped areas.

Another compelling opportunity lies in the development of highly personalized inflight services and the integration of the Internet of Things (IoT) onboard. As connectivity becomes ubiquitous, airlines can leverage data analytics to offer bespoke entertainment, duty-free shopping, and destination-specific information, creating new revenue streams and deeper passenger engagement. Furthermore, connecting various onboard systems through IoT can lead to improved operational efficiencies, such as real-time monitoring of aircraft performance, predictive maintenance, and optimized cabin services. The expansion of these advanced applications beyond basic internet access provides a pathway for sustained innovation and market differentiation, encouraging further investment in robust connectivity infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Untapped Regional Markets (e.g., Africa, parts of Asia Pacific) | +1.8% | Emerging Markets | Medium-term to Long-term |

| Development of Personalized Inflight Entertainment & Services | +1.5% | Global | Medium-term |

| Growth in Low-Cost Carrier (LCC) Adoption of Connectivity Solutions | +1.3% | Asia Pacific, Europe, Latin America | Short-term to Medium-term |

| Integration of Internet of Things (IoT) for Operational Efficiency | +1.1% | Global | Medium-term to Long-term |

| Increasing Ancillary Revenue Generation through Connectivity Services | +1.0% | Global | Short-term to Medium-term |

Inflight Connectivity Equipment Market Challenges Impact Analysis

The Inflight Connectivity Equipment market faces significant challenges, notably the complexities involved in integrating sophisticated connectivity systems with existing aircraft avionics and IT infrastructure. Modern aircraft are designed with highly integrated systems, and adding new connectivity hardware requires meticulous planning, stringent certification processes, and seamless compatibility with a multitude of onboard components. This integration can be time-consuming and costly, often requiring significant downtime for aircraft, which directly impacts airline operations and revenue. Ensuring interoperability across diverse aircraft types and ages adds another layer of complexity for equipment providers.

Another persistent challenge is managing passenger expectations versus the actual performance of inflight connectivity. Despite technological advancements, passengers often compare airborne internet speeds and reliability to their ground-based broadband experiences, leading to potential dissatisfaction when performance falls short, especially on crowded flights or over remote areas. Factors such as fluctuating satellite signals, limited bandwidth allocation per user, and high latency can lead to service interruptions or slow speeds, negatively impacting the perceived value of the service. Addressing these performance gaps and effectively communicating service limitations while striving for continuous improvement remains a critical hurdle for market players to overcome.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex System Integration with Existing Aircraft Infrastructure | -1.2% | Global | Medium-term |

| Managing Passenger Expectations vs. Actual Performance | -1.0% | Global | Short-term to Medium-term |

| Rapid Technological Obsolescence and Need for Continuous Upgrades | -0.9% | Global | Long-term |

| High Operating Costs and Return on Investment (ROI) Justification for Airlines | -0.7% | Global | Short-term |

| Regulatory Harmonization Across Different Airspaces and Jurisdictions | -0.6% | Global, specific regions (e.g., EU) | Medium-term |

Inflight Connectivity Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Inflight Connectivity Equipment market, covering historical trends from 2019 to 2023 and forecasting market dynamics from 2025 to 2033. It offers a detailed breakdown of market size, growth drivers, restraints, opportunities, and challenges, incorporating the latest technological advancements and their impact. The report also includes extensive segmentation analysis by technology, aircraft type, component, and application, alongside a thorough regional assessment to provide a holistic view of the market landscape and competitive strategies of key industry players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 billion |

| Market Forecast in 2033 | USD 14.365 billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Viasat, Thales Group, Honeywell International Inc., Panasonic Avionics Corporation, Intelsat, Inmarsat Global Limited, Gogo LLC, Collins Aerospace (Raytheon Technologies), Lufthansa Technik AG, Safran S.A., Hughes Network Systems, LLC, Astronics Corporation, Gilat Satellite Networks Ltd., Satcom Direct, SES S.A., OneWeb, Starlink Aviation (SpaceX), Kontron AG, Think Aero Inc., Sky Five GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Inflight Connectivity Equipment market is segmented to provide a granular understanding of its diverse components and applications, enabling a more precise analysis of market dynamics and growth opportunities. This segmentation helps in identifying specific growth pockets, understanding technological preferences, and tailoring strategies for different aviation sectors. The market is broadly categorized by technology, aircraft type, component, and application, reflecting the varied needs of airlines and passengers across the globe.

Each segment offers unique insights into demand patterns and technological adoption. For instance, the technology segment highlights the shift from traditional ATG systems to advanced satellite-based solutions and the emergence of hybrid models. The aircraft type segmentation reveals the differing connectivity requirements across commercial, business, and general aviation. Furthermore, breaking down the market by component provides clarity on hardware versus service revenue streams, while application-based segmentation showcases the growing importance of connectivity not just for passengers but also for crew operations and overall aircraft efficiency. This detailed breakdown ensures a comprehensive view of the market's structure and evolution.

- By Technology: Satellite-based connectivity (Ku-band, Ka-band, L-band), Air-to-Ground (ATG) systems, and Hybrid solutions combining both satellite and ATG for optimal performance.

- By Aircraft Type: Commercial Aviation (including narrow-body, wide-body, and regional jets), Business Jets, and General Aviation.

- By Component: Hardware (antennas, modems, routers, servers, wireless access points) and Services (internet service provision, content streaming, maintenance and support, managed services).

- By Application: Primarily Passenger Connectivity for entertainment and communication, Crew Connectivity for operational communication, and Aircraft Operations for real-time data exchange and monitoring.

Regional Highlights

The global Inflight Connectivity Equipment market exhibits distinct regional dynamics, influenced by varying levels of technological adoption, air traffic growth, and regulatory frameworks. North America and Europe continue to be dominant markets due to early adoption of advanced IFEC systems, high passenger expectations, and the presence of major airlines and connectivity providers. However, the Asia Pacific region is rapidly emerging as a significant growth hub, driven by increasing air travel demand, fleet expansion by low-cost carriers, and substantial investments in modern aviation infrastructure. Latin America, the Middle East, and Africa are also showing promising growth as air travel becomes more accessible and airlines in these regions strive to enhance their competitiveness through improved passenger services.

Each region presents unique opportunities and challenges. North America and Europe focus on upgrading existing fleets to next-generation high-bandwidth systems and leveraging connectivity for personalized services. Asia Pacific's growth is propelled by new aircraft deliveries and a strong demand for basic to premium connectivity across a diverse range of airlines. Meanwhile, the Middle East benefits from its strategic location as a global transit hub, with major airlines investing heavily in cutting-edge IFEC. Latin America and Africa represent developing markets with immense untapped potential, where cost-effectiveness and scalability of solutions will be key drivers of adoption.

- North America: Dominant market share due to high passenger demand, significant airline investments in advanced connectivity, and the presence of key technology providers. Early adoption of HTS and upcoming LEO services.

- Europe: Mature market with a focus on upgrading existing fleets and enhancing passenger experience. Regulatory landscape and diverse airline models influence adoption rates.

- Asia Pacific (APAC): Fastest-growing region driven by burgeoning middle-class populations, rapid air traffic growth, and large aircraft orders. Significant potential for new installations and upgrades, especially in emerging economies like India and China.

- Latin America: Emerging market with increasing penetration of inflight connectivity, driven by growing air travel and a desire to match global service standards. Focus on cost-effective solutions.

- Middle East and Africa (MEA): Steady growth propelled by major airlines investing in luxury and advanced connectivity offerings to attract premium passengers. Africa presents long-term growth potential with improving air infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Inflight Connectivity Equipment Market.- Viasat

- Thales Group

- Honeywell International Inc.

- Panasonic Avionics Corporation

- Intelsat

- Inmarsat Global Limited

- Gogo LLC

- Collins Aerospace (Raytheon Technologies)

- Lufthansa Technik AG

- Safran S.A.

- Hughes Network Systems, LLC

- Astronics Corporation

- Gilat Satellite Networks Ltd.

- Satcom Direct

- SES S.A.

- OneWeb

- Starlink Aviation (SpaceX)

- Kontron AG

- Think Aero Inc.

- Sky Five GmbH

Frequently Asked Questions

Analyze common user questions about the Inflight Connectivity Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is inflight connectivity equipment?

Inflight connectivity equipment refers to the hardware and software systems installed on aircraft that enable internet access, communication, and digital services for passengers, crew, and aircraft operations. This includes antennas, modems, routers, and satellite ground infrastructure, facilitating a range of services from basic web browsing to streaming and real-time data exchange.

What technologies primarily drive inflight connectivity?

The market is primarily driven by satellite communication technologies, including Ku-band, Ka-band, and L-band satellites, alongside air-to-ground (ATG) systems. Newer advancements feature High-Throughput Satellites (HTS) and emerging Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations, which offer significantly increased bandwidth and lower latency, as well as the integration of 5G capabilities.

How does inflight connectivity benefit airlines?

Inflight connectivity offers multiple benefits to airlines, including enhanced passenger satisfaction and loyalty by providing sought-after services. It also creates new ancillary revenue opportunities through paid Wi-Fi, personalized content, and e-commerce. Operationally, it enables real-time data transmission for aircraft monitoring, predictive maintenance, and optimized flight routes, leading to increased efficiency and cost savings.

What are the future trends in inflight connectivity?

Future trends indicate a move towards hyper-personalized inflight experiences driven by AI and data analytics, deeper integration of IoT for operational efficiency and predictive maintenance, and the widespread adoption of LEO satellite networks for global, high-speed, low-latency connectivity. Hybrid solutions combining various technologies will also become more prevalent to ensure seamless and reliable service across all flight paths.

Which regions are leading the market growth for inflight connectivity equipment?

North America and Europe currently hold significant market shares due to high demand and advanced infrastructure. However, the Asia Pacific region is rapidly emerging as a key growth driver, propelled by a surge in air travel, substantial new aircraft deliveries, and increasing investments by airlines in modern connectivity solutions to cater to a growing passenger base.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted