Industrial Water Heater Market

Industrial Water Heater Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705741 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

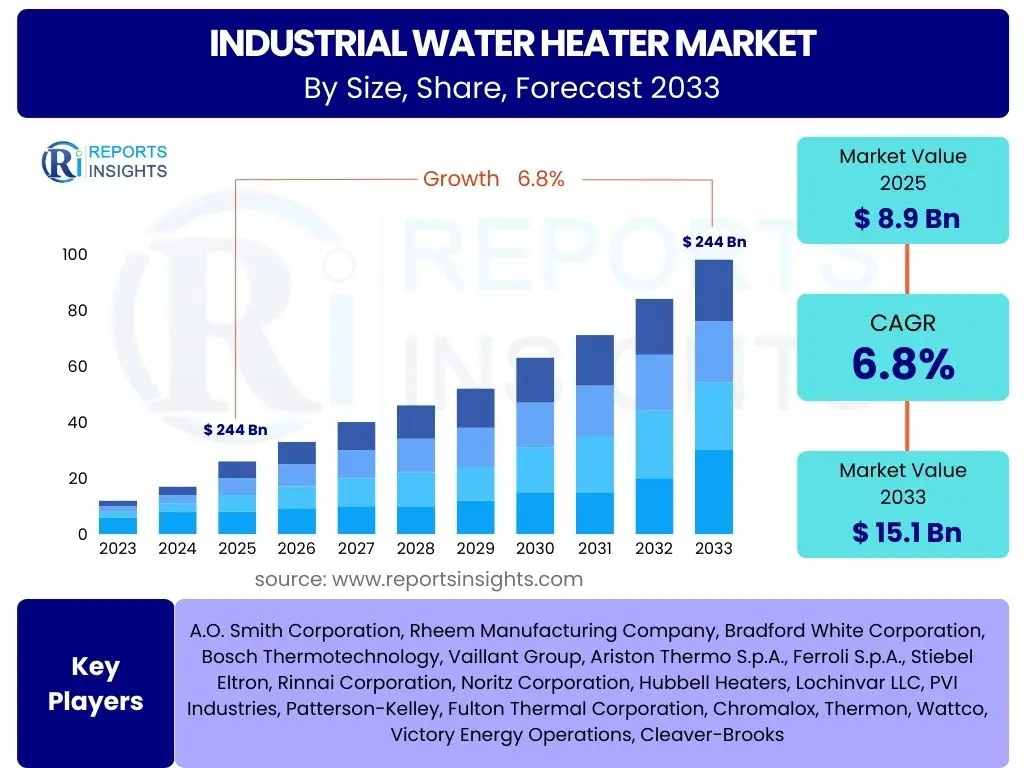

Industrial Water Heater Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Water Heater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 8.9 Billion in 2025 and is projected to reach USD 15.1 Billion by the end of the forecast period in 2033.

Key Industrial Water Heater Market Trends & Insights

The industrial water heater market is experiencing a significant transformation driven by a confluence of technological advancements, evolving regulatory landscapes, and increasing global emphasis on sustainability. Key user inquiries often revolve around the adoption of energy-efficient technologies, the integration of smart systems, and the shift towards cleaner energy sources. These trends are shaping product development and market dynamics, pushing manufacturers to innovate and offer solutions that reduce operational costs and environmental footprints.

Furthermore, the expanding industrial base in emerging economies and the ongoing modernization of infrastructure in developed regions are creating sustained demand for reliable and efficient heating solutions. There is a discernible trend towards modular and compact designs, which offer greater flexibility in installation and better space utilization within industrial facilities. Users are increasingly seeking insights into how these design innovations impact efficiency and overall system longevity.

Another prominent area of interest concerns the long-term viability of different fuel types, given fluctuating energy prices and geopolitical uncertainties. The market is observing a gradual but steady transition away from traditional fossil fuel-dependent systems towards electric, solar, and heat pump technologies, reflecting a broader industry-wide commitment to decarbonization and energy independence. This shift is not only driven by environmental mandates but also by the economic incentives and operational benefits associated with newer, more sustainable heating methods.

- Growing adoption of energy-efficient technologies, including condensing and heat pump systems.

- Increased integration of smart controls, IoT, and AI for enhanced operational efficiency and predictive maintenance.

- Shift towards modular and compact industrial water heater designs for space optimization and flexibility.

- Rising demand for solutions powered by renewable energy sources, such as solar thermal and electric heat pumps.

- Strict environmental regulations driving the development and adoption of low-emission heating solutions.

- Expansion of industrial infrastructure in emerging economies, fueling new installations and upgrades.

AI Impact Analysis on Industrial Water Heater

User questions frequently explore the practical applications and benefits of Artificial Intelligence (AI) within the industrial water heater sector, focusing on how AI can enhance efficiency, reduce costs, and improve system reliability. AI's primary impact lies in its ability to analyze vast amounts of operational data from sensors, enabling sophisticated predictive maintenance capabilities. This allows industrial facilities to anticipate equipment failures before they occur, scheduling maintenance proactively and significantly reducing costly downtime and unexpected repairs. AI algorithms can identify subtle deviations in performance, optimizing heating cycles and energy consumption in real-time based on fluctuating demand and external conditions, leading to substantial energy savings.

Moreover, AI contributes to improved safety protocols by continuously monitoring system parameters and alerting operators to potential hazards. Its integration with Internet of Things (IoT) devices allows for seamless remote monitoring and control, providing operators with comprehensive insights into system health and performance from anywhere. This capability is particularly valuable for large industrial complexes with numerous heating units, enabling centralized management and rapid response to operational issues. The precision offered by AI in managing complex heating systems ensures optimal performance and extends the lifespan of the equipment.

Looking ahead, AI is expected to play a crucial role in the design and development of next-generation industrial water heaters. AI-driven simulations can optimize component design for maximum efficiency and durability, accelerating the innovation cycle. Furthermore, AI can assist in demand forecasting, helping industries to right-size their heating systems and reduce overprovisioning. The ongoing evolution of AI and machine learning will continue to unlock new efficiencies and functionalities, transforming industrial water heating from a static utility into a dynamically optimized, intelligent system that significantly contributes to operational excellence and sustainability goals.

- Enables predictive maintenance by analyzing operational data, reducing downtime and maintenance costs.

- Optimizes energy consumption through real-time adjustments based on demand and environmental factors.

- Enhances operational safety by continuously monitoring system parameters and identifying anomalies.

- Facilitates remote monitoring and control through integration with IoT platforms.

- Supports intelligent diagnostics, streamlining troubleshooting and repair processes.

- Aids in the design and simulation of more efficient and durable water heater components.

Key Takeaways Industrial Water Heater Market Size & Forecast

Common user questions regarding the industrial water heater market forecast frequently center on the underlying drivers of growth, the resilience of the market against economic fluctuations, and the long-term investment prospects. The market's projected growth from USD 8.9 Billion in 2025 to USD 15.1 Billion by 2033, at a robust CAGR of 6.8%, underscores a healthy and expanding sector. This significant expansion is primarily fueled by consistent industrialization efforts, particularly in rapidly developing economies, coupled with an increasing global emphasis on upgrading existing infrastructure to meet contemporary energy efficiency and environmental standards. The forecast signals a strong demand trajectory that is less susceptible to short-term economic headwinds due to the critical nature of heating processes across various industries.

A key insight from the forecast is the dual emphasis on both new installations and the modernization of legacy systems. Industries are not only expanding their operational capacities but are also keenly focused on replacing older, less efficient units with advanced models that incorporate smart technologies and renewable energy integration. This dual-pronged demand strategy ensures sustained growth across diverse market segments. Moreover, the increasing stringency of environmental regulations worldwide is compelling industries to invest in cleaner, more sustainable heating solutions, thereby creating a continuous cycle of innovation and adoption within the market.

Overall, the market forecast reflects a strategic shift towards smart, efficient, and environmentally conscious heating solutions. Stakeholders can anticipate a fertile landscape for technological innovation, with ample opportunities for market penetration through offerings that address both economic and ecological concerns. The consistent growth trajectory indicates that the industrial water heater market remains a vital component of global industrial infrastructure, positioned for substantial expansion driven by efficiency mandates, sustainability goals, and ongoing industrial development across various sectors.

- The market exhibits strong growth potential, projected to reach USD 15.1 Billion by 2033, driven by industrial expansion and modernization.

- Energy efficiency and environmental compliance are major catalysts for new installations and upgrades.

- Technological advancements, including smart controls and AI integration, are enhancing market value and competitiveness.

- Emerging economies present significant opportunities for market penetration due to rapid industrialization.

- The market is resilient, supported by essential demand for process heating across diverse industrial sectors.

Industrial Water Heater Market Drivers Analysis

The industrial water heater market is propelled by several robust drivers that reflect global economic and environmental shifts. Foremost among these is the escalating pace of industrialization and infrastructure development across both developed and emerging economies. As manufacturing capabilities expand and new industrial facilities are established, there is a commensurate rise in demand for reliable and efficient process heating solutions. This foundational driver is complemented by a growing imperative for energy efficiency and cost reduction across all industrial sectors, pushing businesses to invest in modern heating systems that consume less energy and offer superior performance. Furthermore, the increasing stringency of environmental regulations worldwide, particularly concerning carbon emissions and air quality, is compelling industries to adopt cleaner, more sustainable water heating technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Industrialization and Infrastructure Development | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Increasing Focus on Energy Efficiency and Cost Reduction | +1.2% | Global, particularly North America, Europe | Medium-term |

| Stringent Environmental Regulations and Decarbonization Goals | +1.0% | Europe, North America, parts of Asia Pacific | Medium-term |

| Technological Advancements in Heating Solutions | +0.9% | Global | Medium-term |

| Growing Demand from Process Industries (e.g., Food & Beverage, Chemical) | +1.3% | Global | Long-term |

Industrial Water Heater Market Restraints Analysis

Despite significant growth drivers, the industrial water heater market faces several restraints that could impede its expansion. A primary challenge is the high initial investment cost associated with advanced and energy-efficient industrial water heating systems. While these systems offer long-term operational savings, the upfront capital expenditure can be a barrier for smaller businesses or those with limited budgets. Additionally, the volatility of raw material prices, such as steel, copper, and specialized components, can impact manufacturing costs and, consequently, the final price of industrial water heaters, leading to market uncertainties. Furthermore, the availability and adoption of alternative heating technologies, which might be perceived as more cost-effective or suited for specific niche applications, could divert demand away from conventional industrial water heaters.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs for Advanced Systems | -1.0% | Global, particularly developing regions | Short-to-Medium Term |

| Volatile Raw Material Prices | -0.7% | Global | Short-term |

| Availability of Alternative Heating Technologies (e.g., CHP, direct heating) | -0.8% | North America, Europe | Medium-term |

| Complexity of Installation and Maintenance for Sophisticated Systems | -0.6% | Developing regions, smaller enterprises | Medium-term |

Industrial Water Heater Market Opportunities Analysis

Numerous opportunities exist within the industrial water heater market, presenting avenues for significant growth and innovation. The increasing global emphasis on sustainable energy solutions creates a substantial opportunity for the integration of renewable energy sources, such as solar thermal and heat pump technologies, into industrial water heating systems. This aligns with corporate sustainability goals and government incentives for green energy adoption. Furthermore, a vast installed base of older, less efficient industrial water heaters worldwide presents a significant opportunity for retrofitting and modernization projects. Industries are increasingly looking to upgrade their existing infrastructure to improve energy efficiency, reduce operational costs, and comply with evolving environmental standards. The development and widespread adoption of smart, IoT-enabled water heaters offer enhanced monitoring, control, and predictive maintenance capabilities, creating new value propositions and driving demand for technologically advanced solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Renewable Energy Sources | +1.3% | Europe, North America, parts of Asia Pacific | Long-term |

| Retrofitting and Modernization of Existing Systems | +1.1% | Developed Regions (North America, Europe) | Medium-to-Long Term |

| Development of Smart and IoT-Enabled Water Heaters | +1.0% | Global | Medium-to-Long Term |

| Expansion into Emerging Industrial Sectors | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

Industrial Water Heater Market Challenges Impact Analysis

The industrial water heater market faces several significant challenges that can impact its growth trajectory. One key challenge is the fluctuating prices of energy, particularly natural gas and electricity, which directly influence the operational costs of industrial water heaters and can affect investment decisions. Industries might delay upgrades or new installations if energy costs are unpredictable, seeking to defer capital expenditure. Another challenge arises from the rapid pace of technological innovation and the potential for disruption from entirely new heating methodologies or entrants offering novel solutions that could quickly capture market share. This necessitates continuous research and development to remain competitive. Furthermore, securing a skilled workforce for the specialized installation, maintenance, and troubleshooting of complex industrial water heating systems can be a persistent challenge, particularly in regions with labor shortages. This affects deployment efficiency and system reliability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Energy Prices (Gas, Electricity) | -0.9% | Global | Short-to-Medium Term |

| Rapid Technological Advancements and Disruptive Innovations | -0.7% | Global | Medium-to-Long Term |

| Shortage of Skilled Labor for Installation and Maintenance | -0.6% | Developed Regions (North America, Europe) | Medium-term |

| Cybersecurity Risks for Connected Smart Systems | -0.5% | Global | Medium-to-Long Term |

Industrial Water Heater Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Industrial Water Heater Market, covering market size estimations, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis across various parameters and highlights regional dynamics, competitive landscape, and crucial insights for stakeholders seeking to understand market potential and strategic positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.9 Billion |

| Market Forecast in 2033 | USD 15.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | A.O. Smith Corporation, Rheem Manufacturing Company, Bradford White Corporation, Bosch Thermotechnology, Vaillant Group, Ariston Thermo S.p.A., Ferroli S.p.A., Stiebel Eltron, Rinnai Corporation, Noritz Corporation, Hubbell Heaters, Lochinvar LLC, PVI Industries, Patterson-Kelley, Fulton Thermal Corporation, Chromalox, Thermon, Wattco, Victory Energy Operations, Cleaver-Brooks |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial water heater market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across different product types, capacities, end-use industries, and applications. This segmentation is critical for identifying specific growth pockets, understanding demand patterns, and formulating targeted market strategies. The varied requirements across different industrial sectors necessitate a broad range of heating solutions, from high-capacity systems for heavy manufacturing to specialized units for sensitive pharmaceutical processes. Analyzing these segments helps in pinpointing key areas of innovation and investment.

- By Type: This segment includes Electric Water Heaters, Gas Water Heaters, Solar Water Heaters, Heat Pump Water Heaters, Oil-Fired Water Heaters, Biomass Water Heaters, and Others. The type of fuel source and heating technology is a primary differentiator, influencing efficiency, environmental impact, and operational costs.

- By Capacity: Categorized into Small (Up to 100 gallons), Medium (100-500 gallons), and Large (Above 500 gallons). Capacity segmentation reflects the scale of industrial operations and their specific heating demands, from small-scale commercial applications to large-scale industrial processes.

- By End-Use Industry: Encompasses sectors such as Food and Beverage, Chemical and Petrochemical, Pharmaceutical, Automotive, Manufacturing, Pulp and Paper, Textile, Healthcare, Hospitality, Power Generation, and Others. Each industry has unique requirements concerning water temperature, purity, and volume, driving demand for tailored heating solutions.

- By Application: Covers diverse applications including Process Heating, Space Heating, Water Treatment, Sanitation, and Commercial Laundry. This segmentation highlights the functional uses of industrial water heaters, illustrating their broad utility across various operational needs within industrial settings.

Regional Highlights

- North America: This region represents a mature market characterized by stringent energy efficiency regulations and a strong emphasis on modernization and replacement of aging infrastructure. The market here is driven by the adoption of advanced, energy-saving technologies and smart systems, as industries seek to reduce operational costs and comply with environmental standards. Significant investments in manufacturing and process industries contribute to sustained demand, with a growing interest in renewable energy integration.

- Europe: Europe is a highly progressive market, leading in the adoption of sustainable and low-carbon industrial heating solutions. The region is heavily influenced by ambitious decarbonization targets and robust environmental policies, fostering innovation in heat pump technology, solar thermal systems, and highly efficient electric heaters. Countries like Germany and the UK are at the forefront of this transition, driving demand for greener technologies and advanced control systems.

- Asia Pacific (APAC): APAC stands as the fastest-growing market for industrial water heaters due to rapid industrialization, urbanization, and significant infrastructure development, particularly in countries such as China, India, and Southeast Asian nations. The expansion of manufacturing bases, increasing foreign direct investment, and rising energy demands are fueling new installations and substantial market growth. While cost-effectiveness remains a key factor, there is a growing inclination towards energy-efficient and technologically advanced solutions.

- Latin America: This region presents emerging opportunities, driven by industrial expansion, particularly in sectors like food and beverage, chemicals, and mining. Economic growth and increasing industrial output in countries like Brazil and Mexico are contributing to a steady demand for industrial water heating solutions. The market is evolving, with a gradual shift towards more energy-efficient models and a growing awareness of environmental considerations, though traditional heating methods still hold a significant share.

- Middle East and Africa (MEA): The MEA region is experiencing growth spurred by diversification efforts away from oil and gas, leading to investments in manufacturing, infrastructure, and hospitality sectors. While energy abundance has historically favored conventional fuel sources, there is a growing recognition of the need for energy efficiency and sustainable practices. Large-scale construction projects and industrial development initiatives, particularly in Gulf Cooperation Council (GCC) countries, are key market drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Water Heater Market.- A.O. Smith Corporation

- Rheem Manufacturing Company

- Bradford White Corporation

- Bosch Thermotechnology

- Vaillant Group

- Ariston Thermo S.p.A.

- Ferroli S.p.A.

- Stiebel Eltron

- Rinnai Corporation

- Noritz Corporation

- Hubbell Heaters

- Lochinvar LLC

- PVI Industries

- Patterson-Kelley

- Fulton Thermal Corporation

- Chromalox

- Thermon

- Wattco

- Victory Energy Operations

- Cleaver-Brooks

Frequently Asked Questions

What drives the growth of the industrial water heater market?

The industrial water heater market is primarily driven by rapid industrialization, increasing demand for energy-efficient solutions, stringent environmental regulations, and ongoing infrastructure development across various end-use industries globally. The need for precise and reliable process heating in sectors like food and beverage, chemical, and pharmaceuticals significantly contributes to market expansion.

How is AI impacting the industrial water heater industry?

AI is transforming the industrial water heater industry by enabling predictive maintenance, optimizing energy consumption through real-time data analysis, and enhancing operational safety. It facilitates remote monitoring and control when integrated with IoT, leading to reduced downtime, lower operational costs, and improved system reliability. AI also aids in the design of more efficient heating components.

What are the key types of industrial water heaters available in the market?

The main types of industrial water heaters include electric, gas, solar, and heat pump water heaters. Other types comprise oil-fired and biomass water heaters. The choice of type depends on factors such as fuel availability, energy costs, environmental regulations, capacity requirements, and specific industry applications.

Which region is expected to dominate the industrial water heater market?

The Asia Pacific (APAC) region is projected to dominate the industrial water heater market, primarily due to rapid industrialization, significant infrastructure investments, and increasing manufacturing activities in countries like China and India. This region exhibits the highest growth potential for new installations and upgrades compared to more mature markets.

What are the primary challenges facing the industrial water heater market?

Key challenges for the industrial water heater market include high initial investment costs for advanced systems, volatility in raw material and energy prices, the presence of alternative heating technologies, and the need for a skilled workforce for complex installations and maintenance. Cybersecurity risks for connected smart systems also present a growing concern.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted