Industrial Vacuum Valve Market

Industrial Vacuum Valve Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703011 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

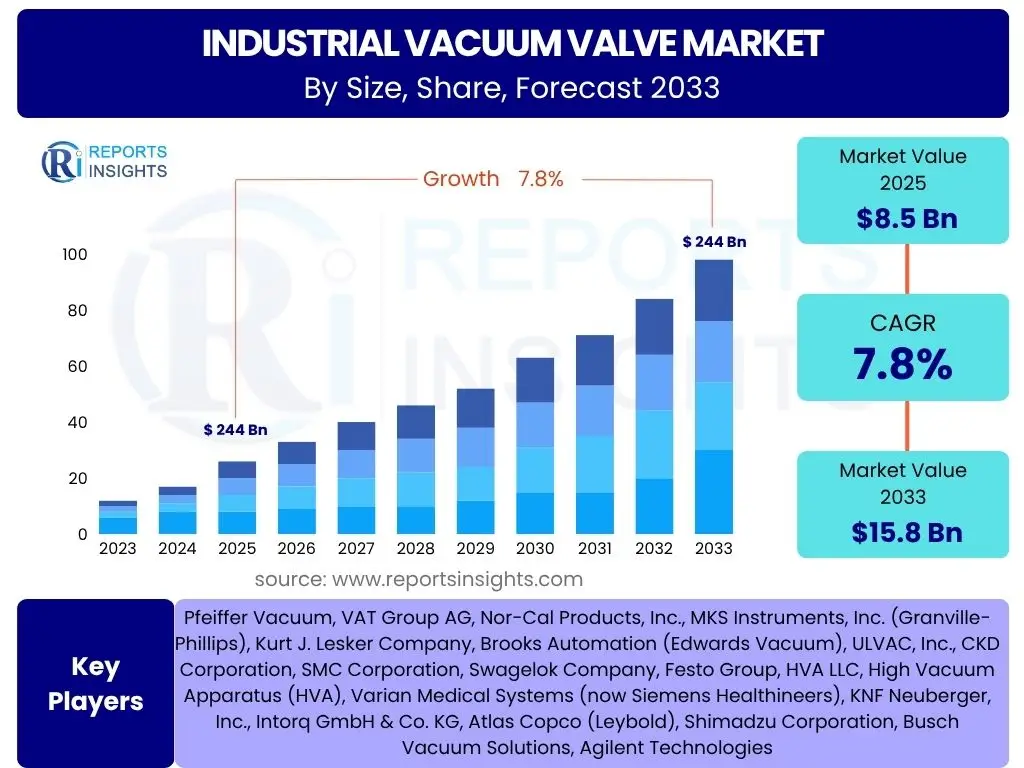

Industrial Vacuum Valve Market Size

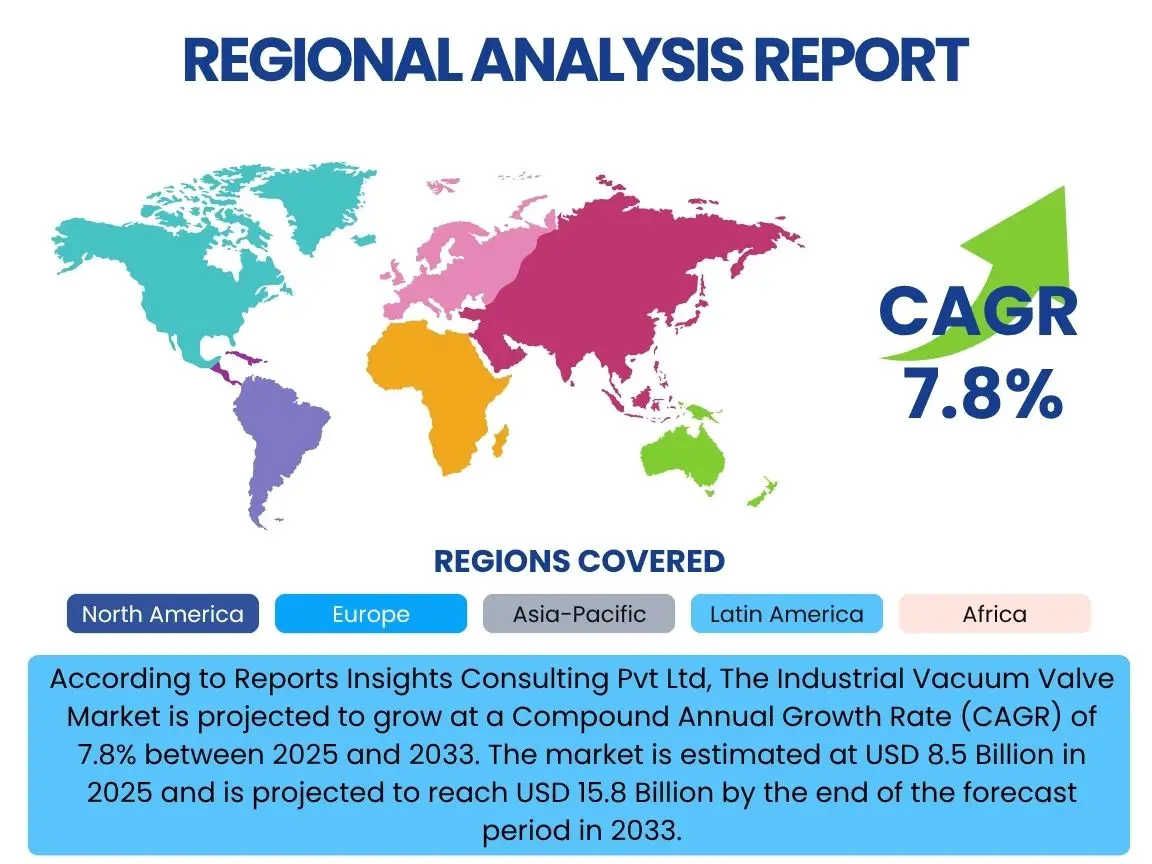

According to Reports Insights Consulting Pvt Ltd, The Industrial Vacuum Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 15.8 Billion by the end of the forecast period in 2033.

Key Industrial Vacuum Valve Market Trends & Insights

The industrial vacuum valve market is experiencing significant evolution driven by several key technological and industrial shifts. Users frequently inquire about the latest innovations, market dynamics, and how these valves are adapting to new industrial demands. A prominent trend is the increasing demand for ultra-high vacuum (UHV) and extreme ultra-high vacuum (XUHV) systems, particularly from the semiconductor and research sectors, which necessitates the development of valves capable of maintaining exceptionally low pressures with minimal leakage and contamination. This push for higher performance extends to material science, where advanced alloys and specialized sealing mechanisms are being employed to withstand harsh operating environments, corrosive media, and extreme temperatures. Another notable trend is the integration of smart technologies and automation capabilities into vacuum valve systems.

Manufacturers are focusing on developing valves with enhanced sensor integration, remote monitoring, and predictive maintenance features. This not only improves operational efficiency and reduces downtime but also addresses the growing need for precision control and data analytics in complex industrial processes. The drive towards energy efficiency and sustainability is also shaping the market, with a focus on designing valves that consume less power and contribute to reduced environmental impact. Furthermore, the expansion of new application areas, such as advanced manufacturing, additive manufacturing, and emerging clean energy technologies like fusion research, is creating novel opportunities and driving specific design requirements for industrial vacuum valves. Users are keenly interested in how these trends translate into more reliable, efficient, and adaptable vacuum solutions.

- Growing demand for Ultra-High Vacuum (UHV) and Extreme Ultra-High Vacuum (XUHV) systems.

- Integration of smart technologies, sensors, and automation for enhanced control and monitoring.

- Development of advanced materials and sealing solutions for improved performance in harsh environments.

- Increasing focus on energy efficiency and sustainable manufacturing practices.

- Expansion into new application areas such as advanced manufacturing and clean energy research.

AI Impact Analysis on Industrial Vacuum Valve

The integration of Artificial Intelligence (AI) into industrial processes is a topic of considerable interest, and users frequently inquire about its specific impact on the industrial vacuum valve sector. AI’s influence is primarily observed in enhancing operational efficiency, predictive maintenance, and quality control. By analyzing sensor data from vacuum valve systems, AI algorithms can detect subtle anomalies that might indicate impending failures, allowing for proactive maintenance before a critical breakdown occurs. This capability significantly reduces unscheduled downtime, optimizes maintenance schedules, and extends the lifespan of expensive equipment. Furthermore, AI can optimize valve performance in real-time by analyzing process parameters and adjusting valve operation for optimal throughput and energy consumption, leading to more efficient and precise control over vacuum environments.

Beyond maintenance and operational optimization, AI also plays a crucial role in improving the design and manufacturing processes of industrial vacuum valves. Generative design, powered by AI, can explore a vast array of design possibilities to create lighter, more robust, and more efficient valve structures that meet specific performance criteria. In manufacturing, AI-driven quality inspection systems can identify defects with greater accuracy and speed than traditional methods, ensuring higher product quality and reliability. The collective impact of AI is transforming industrial vacuum valve systems from purely mechanical components into intelligent, interconnected parts of a broader smart factory ecosystem. While the direct application of AI within the valve itself might be limited to smart sensors, its overarching influence on system management, data analytics, and operational intelligence is profound.

- Enabling predictive maintenance through data analysis, reducing downtime and optimizing schedules.

- Optimizing valve performance and process control in real-time for improved efficiency.

- Enhancing quality control and defect detection during manufacturing processes.

- Facilitating generative design for improved valve structures and performance.

- Integrating vacuum valve systems into broader industrial IoT and smart factory ecosystems.

Key Takeaways Industrial Vacuum Valve Market Size & Forecast

Users are particularly interested in the overarching conclusions and future outlook derived from the industrial vacuum valve market analysis, seeking concise insights into its growth trajectory and influencing factors. A key takeaway is the consistent and robust growth projected for the market, driven by persistent demand from high-tech industries. The semiconductor manufacturing sector remains a primary catalyst, with ongoing investments in new fabrication plants and advanced chip technologies requiring sophisticated vacuum solutions. This foundational demand ensures market stability and provides a strong base for continued expansion. Additionally, the increasing complexity of industrial processes across various sectors necessitates higher performance and reliability from vacuum valves, pushing manufacturers to innovate and provide more specialized solutions.

Another critical insight is the expanding scope of applications beyond traditional industries. Emerging fields such as renewable energy, advanced materials research, and specialized pharmaceutical manufacturing are increasingly adopting vacuum technologies, thereby diversifying the market's revenue streams and reducing dependency on any single sector. The forecast indicates that while established regions will continue to be significant contributors, rapid industrialization and technological advancements in emerging economies, particularly in Asia Pacific, will drive substantial new growth. This geographical shift, coupled with the ongoing technological advancements in valve design and smart integration, positions the industrial vacuum valve market for sustained expansion, characterized by a focus on precision, automation, and adaptability to evolving industrial needs.

- Robust and consistent market growth primarily fueled by the semiconductor industry.

- Diversification of applications into emerging sectors like renewable energy and advanced materials.

- Strong demand for high-performance, precision, and reliable vacuum valve solutions.

- Significant growth opportunities in rapidly industrializing economies, particularly Asia Pacific.

- Ongoing technological advancements in smart valve integration and sustainable designs.

Industrial Vacuum Valve Market Drivers Analysis

The industrial vacuum valve market is significantly propelled by several fundamental drivers that stem from global industrial advancements and technological innovation. One primary driver is the accelerating expansion of the semiconductor manufacturing industry. The continuous miniaturization of electronic components, coupled with the escalating demand for high-performance computing and communication devices, necessitates ultra-clean and ultra-high vacuum environments in fabrication processes. Industrial vacuum valves are indispensable for maintaining these precise conditions, controlling gas flow, and isolating various process chambers during chip production, thus directly correlating their market growth with semiconductor industry investments.

Another crucial driver is the increasing adoption of vacuum technologies in various research and development (R&D) sectors and advanced manufacturing processes. Fields such as nanotechnology, material science, surface engineering, and thin-film deposition heavily rely on controlled vacuum environments for experimental precision and product quality. As these R&D efforts yield new applications and scale up to industrial production, the demand for sophisticated industrial vacuum valves capable of handling diverse pressures and media continues to rise. Furthermore, the growing emphasis on automation and process optimization across industries, including pharmaceuticals, food and beverage, and chemical processing, drives the need for reliable, automated, and high-efficiency vacuum valve systems that minimize human intervention and maximize operational throughput.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Semiconductor Manufacturing | +2.5% | Asia Pacific (China, Taiwan, South Korea), North America | Long-term (2025-2033) |

| Increasing R&D Investments & Advanced Manufacturing | +1.8% | North America, Europe, Asia Pacific | Mid-to-Long-term (2025-2033) |

| Rising Demand for Automation & Process Control | +1.5% | Global | Mid-term (2025-2030) |

| Expansion of Pharma & Biotech Industries | +1.0% | North America, Europe, Asia Pacific | Mid-to-Long-term (2025-2033) |

| Emergence of New Vacuum-Dependent Technologies (e.g., Fusion Energy) | +0.8% | Europe, North America, Japan | Long-term (2030-2033) |

Industrial Vacuum Valve Market Restraints Analysis

Despite robust growth drivers, the industrial vacuum valve market faces several significant restraints that could impede its expansion. One prominent factor is the high initial cost associated with advanced vacuum valve systems. These specialized valves, particularly those designed for ultra-high vacuum or extreme conditions, involve complex manufacturing processes, precision engineering, and often utilize expensive, high-performance materials. This high upfront investment can be a barrier for smaller enterprises or those in industries with tighter budget constraints, potentially limiting market penetration in certain segments or regions. The cost factor extends beyond acquisition to installation and maintenance, which also contribute to the total cost of ownership.

Another substantial restraint is the highly specialized and niche nature of the industrial vacuum valve market. Unlike general-purpose valves, vacuum valves require deep technical expertise for design, manufacturing, selection, and application. This specialization translates into a relatively limited pool of manufacturers and suppliers, which can lead to less competitive pricing and longer lead times for custom solutions. Furthermore, the stringent quality and performance requirements, particularly in critical applications like semiconductor manufacturing and scientific research, necessitate meticulous testing and certification processes, adding to the complexity and cost of bringing products to market. These high barriers to entry and the specialized demand base can constrain rapid market expansion and diversification.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Vacuum Valve Systems | -1.2% | Global, particularly emerging economies | Long-term (2025-2033) |

| Niche Market & Technical Specialization | -0.9% | Global | Long-term (2025-2033) |

| Stringent Quality Standards & Certification | -0.7% | Global, particularly developed regions | Mid-term (2025-2030) |

| Fluctuations in Raw Material Prices | -0.5% | Global | Short-to-Mid-term (2025-2028) |

| Geopolitical Tensions Affecting Supply Chains | -0.6% | Global, especially Asia Pacific | Short-to-Mid-term (2025-2027) |

Industrial Vacuum Valve Market Opportunities Analysis

The industrial vacuum valve market is poised to capitalize on several significant opportunities that promise to drive future growth and innovation. A primary opportunity lies in the burgeoning demand for vacuum technologies in emerging industrial applications beyond traditional sectors. This includes the rapidly expanding field of additive manufacturing (3D printing) for specialized materials, which often requires controlled vacuum environments. Additionally, the development of new energy technologies, such as advanced battery manufacturing, hydrogen production, and fusion energy research, presents novel and large-scale applications for high-performance vacuum valves. These emerging areas offer fresh revenue streams and reduce the market's reliance on a few dominant industries, fostering greater resilience and diversification.

Another substantial opportunity resides in the continuous technological advancements in valve design, materials science, and smart integration. The development of more durable, corrosion-resistant, and contamination-free materials for valve construction, coupled with innovations in sealing technologies, can unlock new market segments and improve performance in demanding environments. Furthermore, the increasing trend towards Industry 4.0 and the Industrial Internet of Things (IIoT) offers immense potential for integrating smart sensors, actuators, and AI-driven control systems into vacuum valves. This connectivity enables predictive maintenance, real-time performance optimization, and remote monitoring, creating added value for end-users seeking greater efficiency and reduced operational costs. The demand for customized solutions that cater to highly specific application requirements, particularly in UHV and XUHV environments, also represents a lucrative niche for specialized manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications (e.g., Additive Manufacturing, New Energy) | +1.5% | Global | Long-term (2027-2033) |

| Technological Advancements (Smart Valves, New Materials) | +1.3% | Global | Mid-to-Long-term (2025-2033) |

| Expansion in Developing Economies (Industrialization) | +1.0% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Retrofit & Upgrade Market for Existing Installations | +0.8% | North America, Europe | Mid-term (2025-2030) |

| Growing Demand for High-Purity Applications | +0.7% | Global | Mid-to-Long-term (2025-2033) |

Industrial Vacuum Valve Market Challenges Impact Analysis

The industrial vacuum valve market, while experiencing growth, faces distinct challenges that require strategic navigation. One significant challenge is the intense competition and market fragmentation. Despite the niche nature, the market comprises numerous players, ranging from large, established corporations to smaller, specialized manufacturers. This competitive landscape can lead to price pressures, reduce profit margins, and necessitate continuous innovation to maintain market share. Companies must differentiate their offerings through superior performance, reliability, and customer service to stand out in a crowded field, making it difficult for new entrants to gain traction without substantial investment and technological superiority.

Another critical challenge revolves around the complexity of supply chain management for high-precision components and specialized materials. Industrial vacuum valves often require rare metals, advanced ceramics, and intricate manufacturing processes, making them susceptible to supply chain disruptions, raw material price volatility, and geopolitical instabilities. Maintaining a consistent supply of high-quality components while managing costs and lead times is a continuous balancing act for manufacturers. Furthermore, the rapid pace of technological change in end-user industries, particularly semiconductors, demands that vacuum valve manufacturers constantly adapt and innovate their products. Failure to keep pace with evolving industry standards, higher vacuum requirements, or new process chemistries can quickly render existing product lines obsolete, posing a significant challenge to long-term market relevance and profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Market Fragmentation | -1.0% | Global | Long-term (2025-2033) |

| Complex Supply Chain Management & Raw Material Volatility | -0.8% | Global | Mid-to-Long-term (2025-2033) |

| Rapid Technological Obsolescence in End-user Industries | -0.7% | Global | Mid-to-Long-term (2025-2033) |

| Skilled Labor Shortages for Niche Manufacturing | -0.6% | North America, Europe, Japan | Long-term (2025-2033) |

| Regulatory Compliance & Environmental Standards | -0.5% | Global, especially Europe | Mid-term (2025-2030) |

Industrial Vacuum Valve Market - Updated Report Scope

This comprehensive report delves into the dynamics of the Industrial Vacuum Valve market, offering an in-depth analysis of its current size, historical performance, and future growth projections. It provides detailed insights into market trends, key drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope encompasses a thorough segmentation analysis by valve type, material, application, and end-use industry, providing a granular view of market dynamics across diverse sectors. Furthermore, the report offers a detailed regional analysis, identifying key growth regions and countries, alongside a competitive landscape assessment profiling major market players to provide a holistic understanding of the market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 15.8 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Pfeiffer Vacuum, VAT Group AG, Nor-Cal Products, Inc., MKS Instruments, Inc. (Granville-Phillips), Kurt J. Lesker Company, Brooks Automation (Edwards Vacuum), ULVAC, Inc., CKD Corporation, SMC Corporation, Swagelok Company, Festo Group, HVA LLC, High Vacuum Apparatus (HVA), Varian Medical Systems (now Siemens Healthineers), KNF Neuberger, Inc., Intorq GmbH & Co. KG, Atlas Copco (Leybold), Shimadzu Corporation, Busch Vacuum Solutions, Agilent Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial vacuum valve market is meticulously segmented to provide a granular understanding of its diverse applications and technological requirements. This segmentation allows for precise analysis of market dynamics, growth opportunities, and competitive landscapes across different product types, materials, pressure ranges, and end-use industries. Understanding these distinct segments is crucial for stakeholders to identify specific market niches, tailor product development strategies, and target appropriate customer bases effectively. Each segment represents unique operational demands and technological specifications, reflecting the varied needs of industries utilizing vacuum processes.

- By Valve Type: Gate Valves, Angle Valves, Butterfly Valves, Ball Valves, Diaphragm Valves, Check Valves, and Others.

- By Material: Stainless Steel, Aluminum Alloys, Ceramics, Plastics/Polymers, and Others.

- By Pressure Range: Rough Vacuum, Medium Vacuum, High Vacuum (HV), Ultra-High Vacuum (UHV), and Extreme Ultra-High Vacuum (XUHV).

- By Application: Vacuum Furnaces, Thin-Film Deposition Systems, Semiconductor Processing, Analytical Instruments, Research & Development, Space Simulation Chambers, Medical Devices, Particle Accelerators, Leak Detection Systems, and Others.

- By End-Use Industry: Semiconductor & Electronics, Aerospace & Defense, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Food & Beverage, Power Generation, Automotive, Research & Academia, Metallurgy, and Others.

Regional Highlights

- North America: A mature market with significant demand from the aerospace & defense, pharmaceutical, and advanced research sectors. Strong presence of key technology companies and consistent investment in R&D drive the need for high-performance vacuum valves. The United States remains a dominant player due to its robust semiconductor industry and extensive research infrastructure.

- Europe: Characterized by stringent quality standards and a focus on precision engineering, Europe is a key market for industrial vacuum valves, especially in scientific research, automotive, and metallurgy. Germany and France are notable contributors, driven by their strong manufacturing bases and emphasis on sustainable industrial practices.

- Asia Pacific (APAC): The fastest-growing region, propelled by rapid industrialization and massive investments in semiconductor manufacturing, electronics, and emerging technologies in countries like China, Taiwan, South Korea, and Japan. This region is a major hub for both demand and supply of vacuum components.

- Latin America: An emerging market with growing industrialization, particularly in chemical, food and beverage, and some manufacturing sectors. While smaller in scale compared to other regions, it offers long-term growth potential as industries mature and adopt more sophisticated processes.

- Middle East & Africa (MEA): Gradually increasing adoption of vacuum technologies driven by diversification efforts in industries like oil & gas, pharmaceuticals, and some advanced manufacturing. Growth is more gradual but consistent, with investments in infrastructure contributing to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Vacuum Valve Market.- Pfeiffer Vacuum

- VAT Group AG

- Nor-Cal Products, Inc.

- MKS Instruments, Inc. (Granville-Phillips)

- Kurt J. Lesker Company

- Brooks Automation (Edwards Vacuum)

- ULVAC, Inc.

- CKD Corporation

- SMC Corporation

- Swagelok Company

- Festo Group

- HVA LLC

- High Vacuum Apparatus (HVA)

- Varian Medical Systems (now Siemens Healthineers)

- KNF Neuberger, Inc.

- Intorq GmbH & Co. KG

- Atlas Copco (Leybold)

- Shimadzu Corporation

- Busch Vacuum Solutions

- Agilent Technologies

Frequently Asked Questions

Analyze common user questions about the Industrial Vacuum Valve market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Industrial Vacuum Valve Market?

The Industrial Vacuum Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, reaching an estimated USD 15.8 Billion by 2033.

Which industries are the primary drivers of demand for industrial vacuum valves?

The semiconductor manufacturing and electronics industry is the primary driver. Other significant drivers include aerospace & defense, pharmaceutical & biotechnology, research & development, and emerging advanced manufacturing processes.

What are the key technological trends influencing the industrial vacuum valve market?

Key trends include increasing demand for Ultra-High Vacuum (UHV) and Extreme Ultra-High Vacuum (XUHV) systems, the integration of smart technologies and automation, and the development of advanced materials for improved performance and contamination control.

What are the main challenges faced by the industrial vacuum valve market?

Major challenges include the high initial cost of advanced systems, the highly specialized and niche nature of the market, intense competition, complex supply chain management, and the rapid pace of technological obsolescence in end-user industries.

Which geographical region is expected to lead market growth?

Asia Pacific (APAC) is projected to be the fastest-growing region, driven by significant investments in semiconductor manufacturing, electronics, and rapid industrialization across countries like China, Taiwan, and South Korea.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted