Industrial Specialty Paper Market

Industrial Specialty Paper Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707248 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

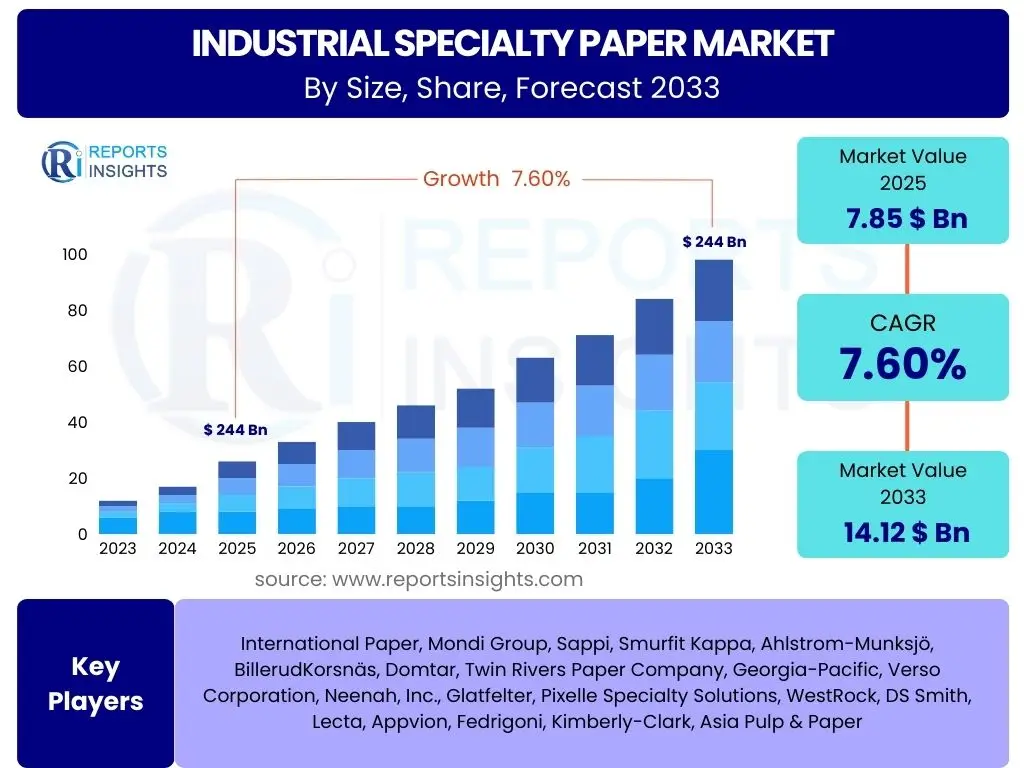

Industrial Specialty Paper Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Specialty Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.6% between 2025 and 2033. The market is estimated at 7.85 USD billion in 2025 and is projected to reach 14.12 USD billion by the end of the forecast period in 2033.

Key Industrial Specialty Paper Market Trends & Insights

The Industrial Specialty Paper market is currently experiencing dynamic shifts driven by evolving consumer demands, stringent environmental regulations, and technological advancements. A dominant trend is the increasing demand for sustainable and eco-friendly paper products, stemming from growing environmental awareness among consumers and industries. This has led to a focus on recyclable, biodegradable, and compostable paper solutions, pushing manufacturers to innovate in raw material sourcing and production processes. The e-commerce boom further amplifies this, necessitating robust and protective yet sustainable packaging solutions.

Another significant insight revolves around the customization and functionality of specialty papers. Industries are increasingly seeking papers with specific attributes such as high barrier properties, enhanced strength, heat resistance, or advanced printability. This demand is particularly strong in the food and beverage, pharmaceutical, and electronics sectors, where product integrity and protection are paramount. Moreover, the integration of smart technologies, such as RFID or NFC, into paper packaging is emerging as a novel trend, offering enhanced traceability and consumer engagement opportunities.

Furthermore, the market is witnessing regional disparities in growth and adoption. While developed economies are focusing on premium, high-performance, and sustainable papers, emerging economies are characterized by rapid industrialization and urbanization, leading to a surge in demand for basic industrial specialty papers in construction, manufacturing, and general packaging. The competitive landscape is also evolving, with established players investing heavily in R&D and strategic partnerships to maintain market leadership and capture new growth avenues, particularly in specialized and high-value applications.

- Increasing demand for sustainable and eco-friendly paper solutions.

- Rising customization and functional requirements for specialty papers.

- Growth driven by the expansion of e-commerce and packaging sector.

- Technological advancements enhancing paper properties and integration with smart solutions.

- Shifting regional consumption patterns and investment in emerging markets.

AI Impact Analysis on Industrial Specialty Paper

The integration of Artificial Intelligence (AI) and machine learning (ML) technologies is poised to significantly transform the Industrial Specialty Paper market, addressing common user concerns around efficiency, quality, and sustainability. AI algorithms can optimize manufacturing processes by analyzing vast datasets from production lines, leading to improved resource utilization, reduced waste, and enhanced operational efficiency. This includes predictive maintenance of machinery, ensuring continuous operation and minimizing costly downtime, which is a critical aspect for capital-intensive paper mills.

Furthermore, AI plays a crucial role in quality control and product development within the specialty paper sector. AI-powered vision systems can detect minute defects in paper webs at high speeds, far surpassing human capabilities, ensuring consistent product quality. In research and development, AI can accelerate the discovery of new materials and formulations for specialty papers with desired properties, such as advanced barrier functions or biodegradability, shortening innovation cycles and responding faster to market demands for high-performance and sustainable solutions.

Supply chain optimization is another area where AI is making a substantial impact. By leveraging AI to forecast demand, manage inventory, and optimize logistics, paper manufacturers can achieve greater supply chain resilience and responsiveness. This helps in mitigating the impact of raw material price volatility and supply disruptions, which are common challenges in the paper industry. The adoption of AI is still nascent in many segments of the industrial specialty paper market, but its potential to drive significant improvements in cost-effectiveness, quality, and environmental footprint is widely recognized and expected to accelerate.

- Enhanced manufacturing process optimization through data analysis and predictive maintenance.

- Improved quality control and defect detection via AI-powered vision systems.

- Accelerated research and development for novel paper formulations and properties.

- Optimized supply chain management, demand forecasting, and inventory control.

- Reduced operational costs and minimized waste through AI-driven efficiency.

Key Takeaways Industrial Specialty Paper Market Size & Forecast

The Industrial Specialty Paper market is on a robust growth trajectory, driven primarily by the escalating demand for sustainable packaging solutions and the expansion of the e-commerce sector globally. Market forecasts indicate consistent growth, underpinned by a shift towards high-performance and functional papers across diverse industrial applications. Users frequently inquire about the segments offering the most promising growth opportunities and the regional landscapes that are expected to lead this expansion, highlighting the need for granular insights into market dynamics.

A significant takeaway is the increasing importance of innovation in product development, particularly in creating papers with advanced barrier properties, biodegradability, and smart functionalities. This innovation is crucial for meeting the evolving demands of end-use industries such as food and beverage, pharmaceuticals, and electronics. The competitive environment is characterized by a focus on sustainable manufacturing processes and supply chain resilience, as companies aim to mitigate environmental impacts and navigate global economic fluctuations effectively.

Moreover, the Asia Pacific region is anticipated to be a major growth engine, fueled by rapid industrialization, urbanization, and a burgeoning consumer base. North America and Europe, while mature, will continue to innovate in high-value specialty paper segments, emphasizing circular economy principles and premium product offerings. Understanding these regional nuances and the underlying drivers is critical for stakeholders seeking to capitalize on the market's projected expansion and navigate its complexities.

- Consistent growth projected, driven by sustainable packaging and e-commerce.

- Emphasis on innovation for functional and high-performance papers.

- Asia Pacific identified as a key growth region due to industrial expansion.

- Increasing focus on circular economy principles and eco-friendly production.

- Market resilience linked to efficient supply chain management and product diversification.

Industrial Specialty Paper Market Drivers Analysis

The Industrial Specialty Paper market is propelled by a confluence of factors, each contributing significantly to its upward trajectory. A primary driver is the surging global demand for sustainable packaging solutions, as environmental consciousness among consumers and regulatory bodies intensifies. This pushes industries towards paper-based alternatives that are recyclable, biodegradable, and renewable, replacing less environmentally friendly materials.

Another crucial driver is the exponential growth of the e-commerce sector, which necessitates robust, protective, and often customized packaging for efficient delivery of goods. Specialty papers, with their unique strength, barrier properties, and printability, are ideally suited for these applications, ensuring product integrity during transit. Furthermore, the rapid industrialization and urbanization, particularly in emerging economies, are fueling demand for various industrial applications of specialty papers, including construction, filtration, and electrical insulation, further broadening the market's scope.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable Packaging | +2.1% | Global, particularly Europe & North America | Short to Long Term (2025-2033) |

| Expansion of E-commerce Sector | +1.8% | Global, especially Asia Pacific & North America | Short to Mid Term (2025-2029) |

| Rising Industrialization & Urbanization | +1.5% | Asia Pacific, Latin America, MEA | Mid to Long Term (2027-2033) |

| Technological Advancements in Paper Manufacturing | +1.2% | Global | Mid to Long Term (2028-2033) |

Industrial Specialty Paper Market Restraints Analysis

Despite its robust growth potential, the Industrial Specialty Paper market faces several significant restraints that could impede its expansion. One major challenge is the volatility of raw material prices, particularly wood pulp, which is highly susceptible to supply chain disruptions, environmental factors, and global trade dynamics. Fluctuations in these costs can directly impact production expenses and profit margins for manufacturers, making long-term planning and pricing strategies challenging.

Another key restraint is the increasing stringency of environmental regulations and sustainability mandates. While these regulations drive innovation towards eco-friendly products, they also impose higher compliance costs, necessitate significant investments in cleaner technologies, and can limit the availability of certain raw materials or production processes. This often translates to higher production costs and potentially higher end-product prices, which can affect market competitiveness. Furthermore, competition from alternative materials, such as plastics, foils, and flexible films, particularly in packaging and barrier applications, poses a continuous threat, as these materials may offer certain advantages in terms of cost or performance for specific niche applications, compelling specialty paper manufacturers to constantly innovate and differentiate their offerings.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Pulp) | -0.9% | Global | Short to Mid Term (2025-2030) |

| Stringent Environmental Regulations | -0.7% | Europe, North America | Mid to Long Term (2027-2033) |

| Competition from Alternative Materials | -0.6% | Global, particularly developed markets | Short to Long Term (2025-2033) |

| High Energy Consumption in Manufacturing | -0.5% | Global | Short to Mid Term (2025-2029) |

Industrial Specialty Paper Market Opportunities Analysis

The Industrial Specialty Paper market presents numerous lucrative opportunities driven by evolving consumer preferences and technological advancements. A significant opportunity lies in the development of innovative functional papers with enhanced barrier properties, particularly for food packaging. As consumers become more health-conscious and seek fresher, safer food products, the demand for papers that can extend shelf life, protect against moisture, oxygen, and grease, without compromising sustainability, is growing exponentially. This opens avenues for advanced coatings and composite paper materials.

Another promising area is the expansion into emerging applications and niche markets. This includes specialty papers for medical and healthcare packaging, electronic components, and advanced filtration systems, where high performance, purity, and specific technical characteristics are paramount. Furthermore, the increasing adoption of digital printing technologies offers opportunities for specialty papers optimized for high-resolution, variable data printing, catering to personalized packaging and marketing needs. Investment in biodegradable and compostable solutions, beyond mere recyclability, also presents a substantial opportunity to capture a larger share of the sustainable materials market, aligning with global efforts to reduce plastic waste and promote a circular economy, thereby unlocking new revenue streams and fostering partnerships across the value chain.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Functional & Barrier Papers | +1.5% | Global | Short to Long Term (2025-2033) |

| Expansion into Niche & High-Value Applications (e.g., Medical, Electronics) | +1.3% | North America, Europe, Developed Asia Pacific | Mid to Long Term (2027-2033) |

| Increased Adoption of Sustainable & Biodegradable Solutions | +1.1% | Global | Short to Long Term (2025-2033) |

| Growth in Digital Printing & Customized Packaging | +0.8% | Global | Mid Term (2026-2030) |

Industrial Specialty Paper Market Challenges Impact Analysis

The Industrial Specialty Paper market faces several inherent challenges that demand strategic responses from manufacturers. One significant hurdle is the persistent issue of raw material supply chain disruptions, exacerbated by geopolitical instabilities, climate events, and logistics bottlenecks. This directly affects the consistent availability and pricing of pulp, chemicals, and other essential inputs, creating uncertainty in production planning and cost management. Manufacturers must invest in diversified sourcing strategies and resilient supply chain networks to mitigate these risks and ensure stable operations.

Another challenge stems from the intense competition within the market, driven by a large number of established players and emerging entrants. This competitive pressure often leads to price wars and necessitates continuous product innovation and differentiation to maintain market share and profitability. Companies must focus on developing unique value propositions, whether through superior product performance, sustainability credentials, or enhanced customer service, to stand out. Furthermore, managing the environmental footprint of paper production, including water consumption, energy intensity, and waste generation, remains a substantial challenge. While sustainability is also an opportunity, meeting increasingly stringent environmental regulations and consumer expectations for eco-friendly products requires substantial capital investment in green technologies and process optimization, adding to operational complexities and costs. Addressing these challenges effectively will be critical for sustained growth in the dynamic industrial specialty paper landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions & Raw Material Volatility | -0.8% | Global | Short to Mid Term (2025-2029) |

| Intense Market Competition & Price Pressure | -0.6% | Global | Short to Long Term (2025-2033) |

| High Capital Investment for Sustainable Production | -0.5% | Global | Mid to Long Term (2027-2033) |

| Waste Management & Recycling Infrastructure Limitations | -0.4% | Developing Regions | Mid to Long Term (2028-2033) |

Industrial Specialty Paper Market - Updated Report Scope

This report offers a comprehensive analysis of the Industrial Specialty Paper Market, providing detailed insights into its current size, historical trends, and future growth projections up to 2033. It meticulously examines market drivers, restraints, opportunities, and challenges, along with the impact of emerging technologies like AI. The scope also includes a thorough segmentation analysis by product type, application, and end-use industry, complemented by an in-depth regional assessment across key geographies, identifying growth hotbeds and market maturity levels. Furthermore, the report profiles leading market players, offering a holistic view of the competitive landscape and strategic initiatives shaping the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 7.85 USD billion |

| Market Forecast in 2033 | 14.12 USD billion |

| Growth Rate | 7.6% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | International Paper, Mondi Group, Sappi, Smurfit Kappa, Ahlstrom-Munksjö, BillerudKorsnäs, Domtar, Twin Rivers Paper Company, Georgia-Pacific, Verso Corporation, Neenah, Inc., Glatfelter, Pixelle Specialty Solutions, WestRock, DS Smith, Lecta, Appvion, Fedrigoni, Kimberly-Clark, Asia Pulp & Paper |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Specialty Paper market is intricately segmented across various dimensions, reflecting the diverse applications and specific performance requirements of these specialized paper products. Understanding these segments is crucial for identifying key growth areas and tailoring product development strategies. The primary segmentation categories include product type, application, and end-use industry, each revealing distinct market dynamics and demand patterns. This granular analysis provides stakeholders with a comprehensive view of the market's structure and competitive landscape, enabling targeted investment and strategic positioning to maximize opportunities within specific niches.

The segmentation by type illustrates the breadth of offerings, ranging from high-strength sack papers to delicate decor papers, each engineered for specific properties like breathability, absorbency, or printability. Application-based segmentation highlights how these papers serve critical functions in sectors like packaging, filtration, and medical, underscoring their functional versatility. Finally, end-use industry segmentation maps the ultimate consumers of these papers, such as the food & beverage, pharmaceutical, or automotive sectors, revealing demand drivers specific to those industries. This multi-faceted segmentation provides a foundational understanding of the market's complexities and interconnectedness.

- By Type: Release Liner Paper, Decor Paper, Filter Paper, Thermal Paper, Sack Paper, Label Paper, Security Paper, Abrasive Backing Paper, Core Board, Corrugated Medium, Other Specialty Papers.

- By Application: Packaging, Printing & Writing, Filtration, Electrical Insulation, Building & Construction, Medical, Labels, Industrial & Automotive, Consumer Goods, Others.

- By End-Use Industry: Food & Beverage, Pharmaceuticals, Automotive, Electrical & Electronics, Healthcare, Personal Care, Construction, Retail & E-commerce, Industrial Manufacturing, Others.

Regional Highlights

- North America: This region is characterized by a mature market with high demand for premium and sustainable industrial specialty papers. Innovation in high-performance barrier papers, medical-grade papers, and specialized packaging solutions is a key focus. The presence of stringent environmental regulations also drives the adoption of eco-friendly paper products. Growth is primarily driven by technological advancements and the e-commerce sector.

- Europe: Europe is a leading market for sustainable and circular economy initiatives in specialty paper. Strong regulatory support for eco-friendly materials and a high consumer preference for sustainable products propel the demand for recycled content, biodegradable, and compostable papers. The region also exhibits significant demand for decor papers, filter papers, and high-quality packaging solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by rapid industrialization, urbanization, and a burgeoning middle-class population. Countries like China, India, Japan, and South Korea are experiencing high demand for specialty papers across diverse applications including packaging, construction, and electronics. The expanding manufacturing base and increasing disposable incomes contribute significantly to market expansion.

- Latin America: This region shows steady growth, influenced by expanding industrial activities and increasing foreign investments in manufacturing and consumer goods sectors. Demand for packaging papers, particularly for food and beverage, is a key driver. Focus on improving local production capabilities and sustainability is gaining traction, albeit at a slower pace compared to developed regions.

- Middle East and Africa (MEA): The MEA market is an emerging region for industrial specialty papers, fueled by infrastructure development projects, growth in the retail sector, and increasing awareness regarding hygiene and food safety. While smaller in market share, the region presents significant untapped potential, with increasing adoption of modern packaging solutions and industrial products, particularly in the GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Specialty Paper Market.- International Paper

- Mondi Group

- Sappi

- Smurfit Kappa

- Ahlstrom-Munksjö

- BillerudKorsnäs

- Domtar

- Twin Rivers Paper Company

- Georgia-Pacific

- Verso Corporation

- Neenah, Inc.

- Glatfelter

- Pixelle Specialty Solutions

- WestRock

- DS Smith

- Lecta

- Appvion

- Fedrigoni

- Kimberly-Clark

- Asia Pulp & Paper

Frequently Asked Questions

What is industrial specialty paper?

Industrial specialty paper refers to engineered paper products designed for specific technical or functional applications beyond conventional printing or writing. These papers possess unique properties such as high strength, barrier protection, heat resistance, filtration capabilities, or specific aesthetic qualities, tailored for various industrial processes and products, including packaging, filtration, and electrical insulation.

What are the key drivers for the Industrial Specialty Paper Market?

Key drivers include the escalating global demand for sustainable and eco-friendly packaging solutions, the rapid expansion of the e-commerce sector requiring specialized protective packaging, increasing industrialization and urbanization in emerging economies, and ongoing technological advancements in paper manufacturing processes that enable new functionalities and applications.

Which region is expected to lead the Industrial Specialty Paper Market growth?

The Asia Pacific (APAC) region is projected to lead market growth due to its rapid industrialization, burgeoning manufacturing sector, significant population growth, and increasing disposable incomes. Countries like China, India, and Southeast Asian nations are major contributors to the rising demand for diverse industrial specialty paper applications.

How does AI impact the Industrial Specialty Paper industry?

AI significantly impacts the Industrial Specialty Paper industry by optimizing manufacturing processes for efficiency and waste reduction, enhancing quality control through automated inspection systems, accelerating research and development for new paper properties, and improving supply chain management through predictive analytics and demand forecasting. AI drives innovation and operational excellence.

What are the major applications of industrial specialty paper?

Major applications include various forms of packaging (e.g., food, pharmaceutical, industrial sacks), filtration (e.g., automotive, industrial, medical), electrical insulation, building and construction materials (e.g., decor paper for laminates), labels, and specialized papers for printing and industrial manufacturing processes, each requiring specific functional characteristics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted