Industrial Silica Sand Market

Industrial Silica Sand Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708625 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

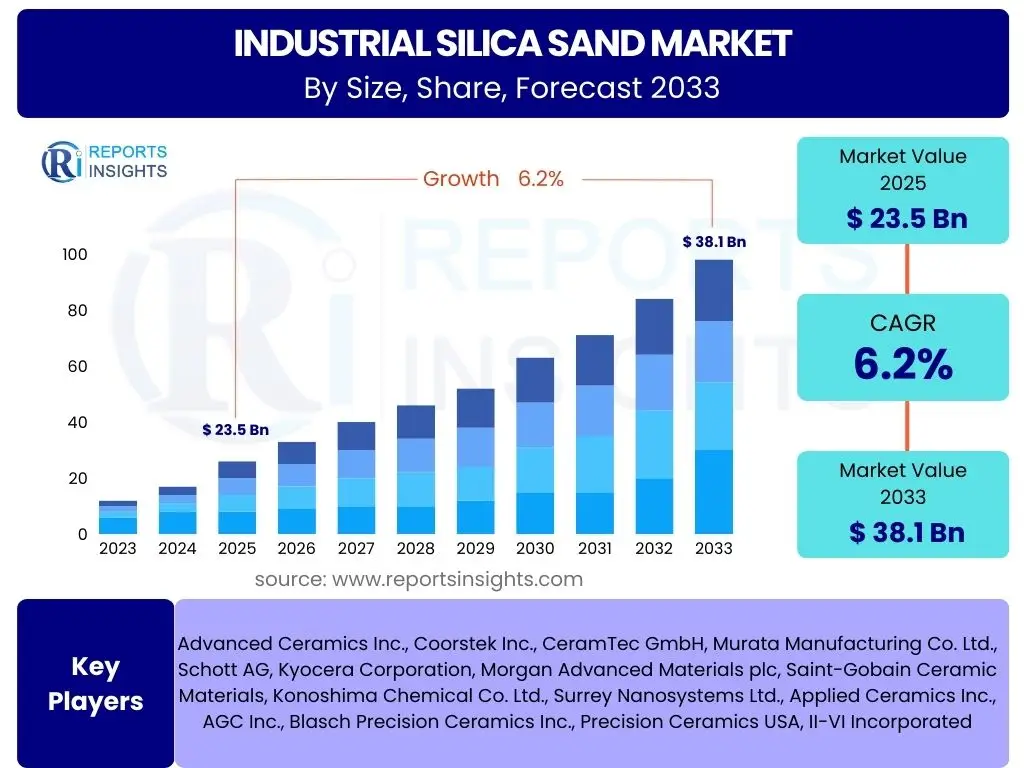

Industrial Silica Sand Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Silica Sand Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 23.5 billion in 2025 and is projected to reach USD 38.1 billion by the end of the forecast period in 2033.

Key Industrial Silica Sand Market Trends & Insights

User queries regarding industrial silica sand market trends frequently highlight the impact of evolving end-use industry demands and the increasing focus on sustainable practices. The market is currently experiencing significant shifts driven by advancements in construction materials, the ongoing expansion of the glass manufacturing sector, and the fluctuating dynamics of the oil and gas industry, particularly concerning hydraulic fracturing. Furthermore, there is a growing emphasis on high-purity silica sand for specialized applications, indicating a premium segment development.

Consumers are increasingly interested in how environmental regulations and technological innovations are shaping the supply chain and production processes. Questions often revolve around the adoption of advanced extraction and processing technologies that can reduce environmental footprints and improve product quality. The integration of recycled materials and the development of alternative resources are also emerging themes, reflecting a broader industry push towards circular economy principles and resource efficiency. These trends collectively underscore a market characterized by both traditional demand drivers and modern sustainability imperatives.

- Growing demand from the construction industry for concrete, mortar, and asphalt applications.

- Expansion of glass manufacturing, including flat glass, container glass, and specialty glass for solar panels and electronics.

- Increased application in the oil and gas sector for hydraulic fracturing, despite market volatility.

- Rising adoption in foundry applications for metal casting due to its high thermal stability.

- Technological advancements in extraction and processing to enhance purity and reduce environmental impact.

- Emergence of high-purity silica sand for specialized applications in electronics, chemicals, and filtration.

- Heightened focus on sustainable sourcing and reduced carbon footprint in production.

AI Impact Analysis on Industrial Silica Sand

User inquiries concerning AI's impact on the industrial silica sand sector often center on operational efficiency, resource optimization, and supply chain resilience. Stakeholders are keen to understand how artificial intelligence and machine learning can streamline mining processes, from geological surveying and resource mapping to extraction and processing. The potential for AI to predict equipment failures, optimize energy consumption in beneficiation plants, and improve overall operational safety through real-time data analysis is a recurring theme in these discussions.

Furthermore, there is significant interest in AI's role in enhancing quality control and market forecasting. AI-driven analytics can monitor silica sand purity levels more precisely, reducing waste and ensuring product specifications are met consistently. In terms of market dynamics, AI can analyze vast datasets to predict demand fluctuations, optimize inventory management, and identify emerging market opportunities or supply chain vulnerabilities, thereby enabling more agile and data-informed decision-making across the value chain. This integration promises a future where operations are not only more efficient but also more responsive to market changes and environmental considerations.

- Optimization of mining operations through predictive analytics for equipment maintenance and resource extraction.

- Enhanced quality control in processing plants using AI for real-time impurity detection and sorting.

- Improved supply chain management and logistics planning, reducing transportation costs and lead times.

- Demand forecasting and market trend analysis to optimize production schedules and inventory levels.

- Automation of hazardous tasks, improving worker safety and reducing operational risks.

Key Takeaways Industrial Silica Sand Market Size & Forecast

Analyzing common user questions regarding the industrial silica sand market's size and forecast reveals a strong interest in understanding the primary growth catalysts and the longevity of current demand trends. Users are keen to identify which end-use sectors will exert the most significant influence on market expansion over the next decade, with particular attention paid to the interplay between traditional industries like construction and glass, and emerging or volatile sectors such as hydraulic fracturing. The focus is on the sustainability of this growth and potential factors that could either accelerate or decelerate its trajectory.

Moreover, inquiries frequently touch upon the geographic distribution of market growth, highlighting a desire to understand regional disparities in demand and supply. The impact of regulatory frameworks, environmental concerns, and technological innovations on the market's overall health and future prospects are also central to user understanding. These questions collectively point to a market that is not only growing steadily but is also undergoing a complex evolution driven by diverse industrial applications and increasing scrutiny on responsible resource management.

- The market exhibits robust growth, primarily fueled by sustained demand from construction and glass industries.

- High-purity silica sand segment is anticipated to witness accelerated growth due to specialized applications.

- Asia Pacific is expected to remain the dominant region, driven by infrastructural development and industrialization.

- Technological advancements in mining and processing are crucial for meeting stringent quality requirements and environmental standards.

- Fluctuations in the oil and gas sector, particularly hydraulic fracturing, represent a significant variable impacting market dynamics.

Industrial Silica Sand Market Drivers Analysis

The industrial silica sand market is predominantly propelled by its indispensable role across a multitude of end-use industries. The global surge in construction activities, encompassing both residential and commercial infrastructure projects, represents a foundational driver, as silica sand is a critical component in concrete, mortar, and various building materials. This construction boom, particularly evident in developing economies, underpins a consistent and growing demand for high-quality sand. Concurrently, the robust expansion of the glass manufacturing sector, driven by increasing consumption of flat glass for architectural purposes, container glass for packaging, and specialized glass for solar panels and electronics, further amplifies market growth.

Beyond these traditional heavy-consuming sectors, the hydraulic fracturing industry continues to be a significant, albeit volatile, driver. Silica sand, specifically frac sand, is essential for maintaining proppant conductivity in oil and gas extraction, directly linking its demand to energy market dynamics. Moreover, the foundry industry's sustained reliance on silica sand for metal casting cores and molds, owing to its excellent thermal stability and refractory properties, contributes substantially to the market's overall expansion. These diverse applications ensure a broad demand base, insulating the market against downturns in any single sector to some extent, while collectively pushing for continued innovation in supply and quality.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Construction Activities | +1.5% | Asia Pacific, North America, Middle East | Long-term |

| Expanding Glass Manufacturing | +1.2% | Asia Pacific, Europe, North America | Medium-term |

| Demand from Hydraulic Fracturing (Frac Sand) | +1.0% | North America, Russia, Middle East | Short to Medium-term |

| Applications in Foundry Industry | +0.8% | Europe, Asia Pacific, North America | Medium-term |

| Rising Demand for Specialty Silica (Electronics, Solar) | +0.7% | Asia Pacific, Europe, North America | Long-term |

Industrial Silica Sand Market Restraints Analysis

Despite its widespread utility, the industrial silica sand market faces several significant restraints that could temper its growth trajectory. Environmental regulations pose a primary challenge, particularly concerning mining permits, land use restrictions, and the environmental impact of extraction and processing activities. Stricter mandates regarding dust emissions, water usage, and biodiversity preservation can increase operational costs, limit new site development, and complicate expansion efforts for market participants. These regulatory hurdles often necessitate substantial investments in compliance technologies and sustainable practices, which can be a barrier for smaller players.

Furthermore, the high cost and logistical complexities associated with transportation represent another considerable restraint. Silica sand is a bulk commodity, and its low value-to-weight ratio makes long-distance shipping expensive, especially for inland operations. This factor can significantly inflate the final product cost, thereby impacting market competitiveness and limiting market reach for producers far from key consumption centers. Coupled with the potential for depletion of high-quality reserves in accessible locations and the emergence of substitute materials in certain niche applications, these restraints collectively present an intricate landscape that demands innovative solutions and strategic planning from industry stakeholders.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -0.9% | Europe, North America, Australia | Long-term |

| High Transportation Costs | -0.8% | Global, particularly landlocked regions | Medium to Long-term |

| Depletion of High-Quality Reserves | -0.6% | Global, specific mining regions | Long-term |

| Competition from Substitute Materials | -0.5% | Specific end-use sectors (e.g., ceramics, abrasives) | Medium-term |

Industrial Silica Sand Market Opportunities Analysis

The industrial silica sand market is poised for significant opportunities driven by emerging applications and a global shift towards technological advancement and sustainable development. One major opportunity lies in the burgeoning demand for high-purity silica sand in advanced technological sectors. The expansion of the electronics industry, requiring ultra-high purity silica for semiconductors and specialized glass substrates, along with the rapid growth of the solar energy sector for photovoltaic panels, creates a premium market segment with higher value realization. These applications demand stringent quality specifications, fostering innovation in processing and beneficiation techniques.

Furthermore, geographical market expansion into developing regions presents substantial growth avenues. Countries in Asia Pacific, Latin America, and Africa are undergoing rapid urbanization and industrialization, leading to increased demand for construction materials, glass products, and industrial foundries. Establishing supply chains and mining operations in these underserved markets can unlock significant untapped potential. Additionally, advancements in sustainable mining practices and the development of value-added products, such as coated sands or tailored blends for specific industrial processes, offer avenues for differentiation and market penetration, addressing both environmental concerns and specialized client needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in High-Purity Silica Demand (Electronics, Solar) | +1.3% | Asia Pacific, Europe, North America | Long-term |

| Expansion into Emerging Markets | +1.0% | Asia Pacific (Southeast Asia), Latin America, Africa | Medium to Long-term |

| Technological Advancements in Processing and Value Addition | +0.8% | Global | Medium-term |

| Recycling and Reuse of Industrial Silica Sand | +0.6% | Europe, North America | Long-term |

Industrial Silica Sand Market Challenges Impact Analysis

The industrial silica sand market encounters various challenges that can hinder its operational efficiency and long-term sustainability. Supply chain disruptions, whether caused by geopolitical events, natural disasters, or labor strikes, pose a significant risk, leading to volatility in raw material availability and pricing. Given the bulk nature of silica sand and its reliance on extensive transportation networks, any interruption can have ripple effects across multiple dependent industries, causing production delays and escalating costs. The globalized nature of industrial supply chains means that localized disruptions can have far-reaching consequences.

Another prominent challenge is the fluctuating energy and raw material prices, which directly impact the cost of extraction, processing, and transportation. Energy-intensive operations like drying and grinding are particularly vulnerable to energy price volatility, squeezing profit margins for producers. Moreover, the industry faces increasing scrutiny over its environmental footprint, including concerns about dust pollution, habitat destruction, and water usage. Compliance with evolving environmental standards and managing public perception regarding these impacts necessitate continuous investment in mitigation strategies and sustainable practices, adding to the operational complexities and financial burden for market players. Addressing these challenges requires strategic foresight, technological investment, and robust risk management frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions | -0.7% | Global | Short to Medium-term |

| Fluctuating Energy and Raw Material Prices | -0.6% | Global | Medium-term |

| Environmental and Social License to Operate | -0.5% | Local communities, Global regulatory bodies | Long-term |

| Skilled Labor Shortages in Mining and Processing | -0.4% | North America, Europe | Medium-term |

Industrial Silica Sand Market - Updated Report Scope

This report provides an in-depth analysis of the industrial silica sand market, covering historical data, current market dynamics, and future projections. The comprehensive scope includes detailed insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. Special emphasis is placed on the impact of technological advancements, particularly artificial intelligence, and evolving regulatory landscapes on market trends and competitive strategies. The objective is to offer stakeholders a strategic overview and actionable intelligence for informed decision-making within the industrial silica sand ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 23.5 billion |

| Market Forecast in 2033 | USD 38.1 billion |

| Growth Rate | 6.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mineral Resources Group, Global Sands Corporation, Industrial Minerals Inc., Quartzite Solutions LLC, SilicaTech Co., The Proppant Producers, Advanced Materials Corp., Foundry Sands Ltd., Construction Aggregates Inc., Glass Grade Sand Works, Chemical Sands Pvt. Ltd., Filtration Media Group, Eco Sand Innovations, High Purity Quartz Corp., Regional Mining Alliance, Integrated Silica Solutions, Premier Sands & Aggregates, Specialty Minerals Group, Universal Silica Products, Future Materials Enterprise |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial silica sand market is extensively segmented to provide a granular understanding of its diverse applications and quality requirements. Segmentation by type differentiates between varieties such as white silica sand and red silica sand, which are typically characterized by their mineral composition and iron content, influencing their suitability for different industrial processes. Further critical segmentation occurs by grade, which is defined by the silicon dioxide (SiO2) purity level, ranging from less than 99% to ultra-high purity grades above 99.9%. This grade-based classification is paramount as it directly correlates with the end-use application, where high-purity sand is crucial for electronics and specialty glass, while lower grades suffice for construction.

Application-based segmentation is perhaps the most diverse, encompassing major sectors like glass manufacturing, foundry operations, building & construction, and hydraulic fracturing. Each application demands specific particle sizes, shapes, and chemical compositions of silica sand. For instance, frac sand requires high crush strength, while glass manufacturing necessitates low iron content. The end-use industry segmentation then groups these applications into broader categories such as Construction, Oil & Gas, Glass, Foundry, and Electronics & Solar, allowing for a comprehensive analysis of market demand drivers from an industrial perspective. This multi-faceted segmentation helps stakeholders understand market niches, identify growth opportunities, and tailor product offerings to specific industry needs.

- By Type: White Silica Sand, Red Silica Sand, Others

- By Grade: Less than 99% SiO2, 99% to 99.5% SiO2, 99.5% to 99.9% SiO2, Above 99.9% SiO2 (High Purity)

- By Application: Glass Manufacturing, Foundry, Building & Construction, Hydraulic Fracturing, Ceramics & Refractories, Filtration, Chemicals & Abrasives, Electronics, Others

- By End-Use Industry: Construction, Oil & Gas, Glass, Foundry, Chemicals, Electronics & Solar, Others

Regional Highlights

The global industrial silica sand market exhibits significant regional variations in demand, supply, and growth dynamics, primarily influenced by local industrial development, resource availability, and regulatory environments. Asia Pacific stands out as the largest and fastest-growing market, driven by rapid urbanization, extensive infrastructure projects in countries like China and India, and the burgeoning electronics and glass manufacturing sectors. The region's robust economic growth fuels demand across construction, automotive, and consumer goods industries, all of which are major consumers of silica sand. Investments in manufacturing capabilities and a large population base further solidify its market dominance, though environmental regulations are increasingly influencing mining practices.

North America holds a substantial share, largely due to its prominent oil and gas industry, particularly the demand for frac sand in hydraulic fracturing operations. While this segment experiences volatility, steady demand from the construction and glass industries continues to underpin regional market stability. Europe, with its mature industrial base and stringent environmental standards, focuses on high-quality and specialty silica sand for applications in advanced ceramics, filtration, and specialized glass. The region also emphasizes sustainable sourcing and recycling initiatives. Latin America, the Middle East, and Africa are emerging markets, driven by infrastructural development and industrialization, though they often face challenges related to logistics and less developed industrial frameworks. Each region presents a unique set of opportunities and challenges for industrial silica sand suppliers, requiring tailored market strategies.

- Asia Pacific: Dominant market, fueled by construction boom, electronics manufacturing, and glass industry expansion in China, India, and Southeast Asian countries.

- North America: Significant market share, primarily driven by hydraulic fracturing activities and stable demand from construction and glass manufacturing in the United States and Canada.

- Europe: Mature market characterized by demand for high-purity silica for specialty glass, filtration, and ceramics, with a strong emphasis on environmental compliance and sustainable practices.

- Latin America: Emerging market with increasing demand from construction and industrial development, particularly in Brazil and Mexico.

- Middle East & Africa: Growing market spurred by infrastructure projects, industrialization, and potentially expanding oil and gas activities in select countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Silica Sand Market.- Mineral Resources Group

- Global Sands Corporation

- Industrial Minerals Inc.

- Quartzite Solutions LLC

- SilicaTech Co.

- The Proppant Producers

- Advanced Materials Corp.

- Foundry Sands Ltd.

- Construction Aggregates Inc.

- Glass Grade Sand Works

- Chemical Sands Pvt. Ltd.

- Filtration Media Group

- Eco Sand Innovations

- High Purity Quartz Corp.

- Regional Mining Alliance

- Integrated Silica Solutions

- Premier Sands & Aggregates

- Specialty Minerals Group

- Universal Silica Products

- Future Materials Enterprise

Frequently Asked Questions

Analyze common user questions about the Industrial Silica Sand market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is industrial silica sand and what are its primary uses?

Industrial silica sand is a high-purity quartz sand with specific physical and chemical properties, vital for various industrial applications. Its primary uses include glass manufacturing, foundry molds, building and construction materials, hydraulic fracturing (frac sand), and filtration systems.

Which factors are driving the growth of the industrial silica sand market?

The market's growth is primarily driven by the escalating demand from the construction industry for concrete and mortars, the expanding glass manufacturing sector, and the consistent need for frac sand in the oil and gas industry. Specialized applications in electronics and solar panels also contribute significantly.

What are the key challenges facing the industrial silica sand market?

Key challenges include stringent environmental regulations impacting mining and processing, high transportation costs due to the bulk nature of the material, potential depletion of high-quality reserves, and fluctuations in energy and raw material prices.

How is AI impacting the industrial silica sand industry?

AI is transforming the industry by optimizing mining operations, enhancing quality control through real-time analysis, improving supply chain logistics, and enabling more accurate demand forecasting, leading to increased efficiency and reduced operational costs.

Which region is expected to dominate the industrial silica sand market?

Asia Pacific is projected to dominate the industrial silica sand market. This dominance is attributed to extensive infrastructure development, rapid industrialization, and robust growth in glass and electronics manufacturing industries across countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted