Industrial Sensor Market

Industrial Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705430 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

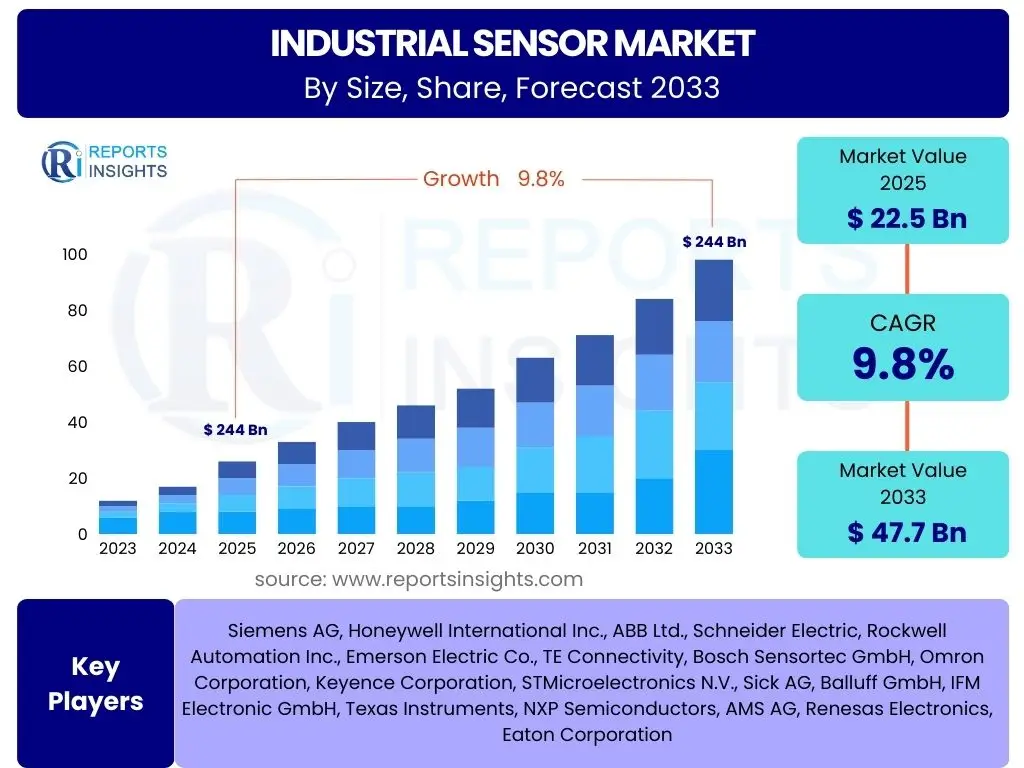

Industrial Sensor Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 22.5 Billion in 2025 and is projected to reach USD 47.7 Billion by the end of the forecast period in 2033.

Key Industrial Sensor Market Trends & Insights

The industrial sensor market is currently undergoing a significant transformation, driven by the escalating demand for advanced automation and the pervasive integration of digital technologies across various industries. Common inquiries from users highlight a keen interest in understanding the underlying forces reshaping this sector, including the shift towards smart manufacturing, the integration of Artificial intelligence (AI) and Machine Learning (ML), and the imperative for real-time data acquisition and analysis. Key trends revolve around enhancing operational efficiency, improving safety protocols, and enabling predictive maintenance capabilities, all critical for modern industrial environments. The focus is increasingly on connectivity, miniaturization, and the ability of sensors to operate reliably in challenging conditions, reflecting a market moving towards more intelligent and adaptive solutions.

The market also observes a strong trend towards the adoption of wireless sensor networks, which significantly reduce installation complexities and costs while offering greater flexibility in deployment. This shift is crucial for retrofitting existing industrial infrastructure and for new installations where wired solutions are impractical. Furthermore, the development of multi-sensor systems, capable of collecting diverse data points simultaneously, is gaining traction. This holistic data collection approach supports more comprehensive monitoring and analysis, enabling businesses to derive deeper insights and make more informed decisions. These advancements are not merely incremental but represent a fundamental evolution in how industrial processes are monitored, controlled, and optimized, underpinning the transition to Industry 4.0.

- Pervasive integration of Industrial Internet of Things (IIoT) and Industry 4.0 principles.

- Significant advancements in miniaturization and the proliferation of wireless sensor technologies.

- Increasing adoption of AI and Machine Learning for enhanced data analytics and predictive capabilities.

- Growing emphasis on energy-efficient and sustainable sensor solutions.

- Development of multi-sensor fusion systems for comprehensive data acquisition.

AI Impact Analysis on Industrial Sensor

The integration of Artificial Intelligence (AI) into industrial sensor technology is a pivotal development, addressing common user questions regarding how intelligence can be embedded at the edge and how data can be leveraged for advanced analytics. Users are seeking to understand how AI enhances sensor capabilities beyond basic data collection, focusing on improved accuracy, predictive analytics, and autonomous operation. AI enables sensors to perform complex computations locally, reducing latency and bandwidth requirements, and facilitating real-time decision-making. This shift from mere data capture to intelligent data processing transforms sensors into critical components of smart, self-optimizing industrial systems.

AI's influence extends to enabling predictive maintenance, anomaly detection, and optimizing operational parameters, addressing key concerns about operational uptime and efficiency. Through machine learning algorithms, industrial sensors can learn from historical data, identify patterns indicative of impending failures, and even self-calibrate or adapt to changing environmental conditions, significantly improving reliability and reducing human intervention. Furthermore, AI-powered sensors contribute to better resource utilization and energy management by providing granular insights into process performance. The ability of AI to derive actionable insights from vast amounts of sensor data is fundamentally reshaping industrial automation, promising higher productivity and more resilient operations.

- Enhanced data processing and real-time analytics at the sensor edge.

- Enabling predictive maintenance through AI-driven anomaly detection and pattern recognition.

- Facilitating autonomous decision-making and self-optimization of industrial processes.

- Improving sensor accuracy and reliability through AI-powered calibration and drift compensation.

- Optimizing resource utilization and energy efficiency by processing complex sensor data.

Key Takeaways Industrial Sensor Market Size & Forecast

The Industrial Sensor market is poised for robust growth, reflecting significant interest in its future trajectory and the underlying factors driving its expansion. User queries frequently center on understanding the most impactful growth drivers, the longevity of current trends, and the overall market stability in the face of technological evolution. A primary takeaway is the indispensable role industrial sensors play in the global shift towards advanced automation and digital transformation, positioning them as fundamental components for achieving operational excellence across diverse industries. The forecast indicates a sustained high growth rate, underscoring the market's resilience and its capacity for continuous innovation in response to evolving industrial demands.

Another crucial insight is the increasing complexity and sophistication of industrial sensor applications, moving beyond basic measurement to integrated systems capable of advanced diagnostics and predictive functions. This evolution is underpinned by the convergence of sensor technology with AI, IoT, and edge computing, enabling smarter factories and more efficient processes. The market's future growth is intrinsically linked to the expanding adoption of Industry 4.0 initiatives globally, as industries strive for greater efficiency, safety, and productivity. This strategic importance ensures a dynamic and competitive landscape, with continuous opportunities for technological advancements and market penetration in both established and emerging industrial sectors.

- The market is experiencing a significant and sustained growth trajectory, driven by industrial automation and digitization.

- Technological integration, particularly with AI and IoT, is a primary catalyst for market expansion and innovation.

- Industrial sensors are critical enablers for Industry 4.0 initiatives, facilitating smart manufacturing and predictive maintenance.

- The market's future is characterized by evolving applications across diverse sectors, demanding versatile and intelligent sensor solutions.

- Continued investment in R&D for advanced sensor capabilities is expected, fostering a highly competitive and innovative environment.

Industrial Sensor Market Drivers Analysis

The industrial sensor market is primarily driven by the accelerating pace of digital transformation and the widespread adoption of automation technologies across various industrial sectors. The global push towards Industry 4.0 and the Industrial Internet of Things (IIoT) mandates the deployment of intelligent sensors to collect and transmit vast amounts of data, essential for real-time monitoring, control, and optimization of industrial processes. This paradigm shift requires sensors capable of providing high accuracy, reliability, and seamless connectivity, thus fueling market demand. Furthermore, the increasing emphasis on improving operational efficiency, reducing downtime, and enhancing worker safety compels industries to invest in advanced sensor solutions that can offer predictive insights and enable proactive maintenance strategies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Adoption of Industry 4.0 and IIoT | +2.5% | Global, particularly APAC (China, India), North America, Europe | 2025-2033 (Long-term) |

| Increasing Demand for Automation in Manufacturing | +2.0% | Global, especially automotive, electronics, food & beverage sectors | 2025-2033 (Long-term) |

| Growing Focus on Predictive Maintenance and Asset Monitoring | +1.8% | North America, Europe, Asia Pacific (developed economies) | 2025-2030 (Mid-term) |

| Miniaturization and Advancement in Sensor Technologies | +1.5% | Global, R&D intensive regions like North America, Europe, East Asia | 2025-2033 (Long-term) |

| Government Initiatives Supporting Smart Manufacturing | +1.0% | Germany (Industry 4.0), China (Made in China 2025), USA (Advanced Manufacturing Partnership) | 2025-2030 (Mid-term) |

Industrial Sensor Market Restraints Analysis

Despite significant growth prospects, the industrial sensor market faces several restraints that could impede its expansion. One prominent challenge is the substantial initial investment required for adopting advanced sensor systems, particularly for Small and Medium-sized Enterprises (SMEs) that may have limited capital. The cost associated with purchasing, installing, and integrating complex sensor networks, along with the necessary IT infrastructure, can be prohibitive. Another significant concern revolves around cybersecurity risks. As industrial sensors become increasingly connected to networks and the cloud, they become potential entry points for cyber threats, leading to data breaches or operational disruptions. Addressing these vulnerabilities requires robust security measures and continuous vigilance, adding to the complexity and cost of deployment.

Furthermore, issues related to interoperability and standardization pose a challenge. The lack of universal communication protocols and data formats among different sensor manufacturers and industrial systems can hinder seamless integration and data exchange. This often leads to fragmented solutions and increased integration costs. Additionally, a shortage of skilled professionals capable of deploying, maintaining, and analyzing data from advanced industrial sensor systems remains a significant bottleneck. The specialized expertise required for complex IIoT architectures and data analytics is not readily available in all regions, impacting the pace of adoption. These factors collectively necessitate strategic planning and investment in training and infrastructure development to mitigate their negative impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Integration Costs | -1.2% | Developing Economies, SMEs globally | 2025-2028 (Short-term) |

| Cybersecurity Concerns and Data Privacy Risks | -1.0% | Global, particularly in critical infrastructure sectors | 2025-2033 (Long-term) |

| Interoperability and Standardization Issues | -0.8% | Global, impacting multi-vendor industrial environments | 2025-2030 (Mid-term) |

| Shortage of Skilled Workforce and Technical Expertise | -0.7% | Global, more pronounced in less developed regions | 2025-2033 (Long-term) |

| Volatility of Raw Material Prices | -0.5% | Global, impacting sensor manufacturing costs | 2025-2027 (Short-term) |

Industrial Sensor Market Opportunities Analysis

The industrial sensor market is rich with opportunities, driven by expanding applications beyond traditional manufacturing sectors and continuous technological innovation. One significant opportunity lies in the burgeoning smart cities and smart infrastructure initiatives globally. The development of intelligent urban environments requires a vast array of sensors for traffic management, environmental monitoring, utility management, and public safety, opening new avenues for industrial sensor deployment. Another promising area is the expansion of industrial sensor applications into non-traditional verticals such as healthcare (for process automation in pharmaceuticals and medical device manufacturing), agriculture (for precision farming and yield optimization), and renewable energy (for monitoring solar panels and wind turbines). These emerging applications create demand for specialized and ruggedized sensor solutions.

Furthermore, advancements in miniaturization, low-power consumption, and the development of self-powered sensors offer substantial growth opportunities. These innovations enable the deployment of sensors in previously inaccessible or challenging environments, broadening the market scope. The increasing demand for sensor-as-a-service (SaaS) models also presents a lucrative opportunity, particularly for SMEs, by reducing upfront costs and offering flexible deployment options. This model allows businesses to leverage advanced sensor capabilities without significant capital expenditure. Lastly, the integration of 5G technology is set to revolutionize industrial connectivity, enabling ultra-reliable low-latency communication (URLLC) essential for real-time sensor data transmission and control. This will unlock new possibilities for autonomous industrial operations and highly responsive systems, solidifying the market's growth trajectory.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Industry Verticals (e.g., Healthcare, Agriculture, Smart Cities) | +1.8% | Global, particularly emerging economies and niche applications | 2025-2033 (Long-term) |

| Development of Miniaturized and Low-Power/Self-Powered Sensors | +1.5% | Global, R&D hubs in North America, Europe, East Asia | 2025-2033 (Long-term) |

| Adoption of Sensor-as-a-Service (SaaS) Models | +1.2% | Global, especially beneficial for SMEs | 2025-2030 (Mid-term) |

| Integration with 5G Technology for Enhanced Connectivity | +1.0% | Countries rolling out 5G industrial networks (China, USA, South Korea) | 2027-2033 (Long-term) |

| Increasing Demand for Environmental Monitoring and Sustainability Solutions | +0.9% | Europe, North America, and regions with strict environmental regulations | 2025-2033 (Long-term) |

Industrial Sensor Market Challenges Impact Analysis

The industrial sensor market encounters several significant challenges that necessitate strategic approaches for continued growth. A primary challenge involves the immense volume and complexity of data generated by modern industrial sensors. Effectively managing, processing, and analyzing this 'big data' to extract actionable insights requires sophisticated infrastructure, advanced analytics capabilities, and skilled personnel. Without robust data management strategies, the full potential of advanced sensors remains untapped, leading to inefficiencies and missed opportunities. Another critical hurdle is ensuring the interoperability of diverse sensor types and communication protocols within heterogeneous industrial environments. Different manufacturers often use proprietary systems, which complicates integration and creates silos, hindering the creation of a truly interconnected smart factory.

Furthermore, maintaining high accuracy and reliability of sensors in harsh industrial environments, characterized by extreme temperatures, vibrations, dust, and corrosive chemicals, poses a continuous engineering challenge. The lifespan and performance of sensors can be significantly impacted, leading to increased maintenance costs and potential operational disruptions. The rapid pace of technological innovation also presents a challenge of obsolescence, as newer, more capable sensors frequently emerge, requiring industries to constantly evaluate upgrades and replacements to remain competitive. Lastly, the power consumption of advanced, highly functional sensors can be a limiting factor, particularly for wireless deployments where battery life is critical. Addressing these multifaceted challenges is essential for sustained market expansion and the widespread adoption of next-generation industrial sensor technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Management and Analytics Complexities | -1.1% | Global, particularly in highly automated industries | 2025-2033 (Long-term) |

| Ensuring Interoperability Across Diverse Systems | -0.9% | Global, affecting integration projects across all regions | 2025-2030 (Mid-term) |

| Maintaining Accuracy and Reliability in Harsh Environments | -0.8% | Manufacturing, Oil & Gas, Mining, Energy sectors globally | 2025-2033 (Long-term) |

| Rapid Technological Obsolescence | -0.7% | Global, especially in technology-intensive industries | 2025-2030 (Mid-term) |

| High Power Consumption of Advanced Sensors | -0.6% | Global, impacts wireless and remote deployments | 2025-2028 (Short-term) |

Industrial Sensor Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Industrial Sensor Market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry landscape. The report segments the market extensively by type, technology, end-use industry, function, and connectivity, offering a granular view of market performance across various dimensions. It also includes a detailed regional analysis and profiles of key market players, making it an invaluable resource for stakeholders seeking to understand market trends, competitive positioning, and strategic growth avenues. The scope is designed to provide a holistic view for informed decision-making within the evolving industrial automation ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 22.5 Billion |

| Market Forecast in 2033 | USD 47.7 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Honeywell International Inc., ABB Ltd., Schneider Electric, Rockwell Automation Inc., Emerson Electric Co., TE Connectivity, Bosch Sensortec GmbH, Omron Corporation, Keyence Corporation, STMicroelectronics N.V., Sick AG, Balluff GmbH, IFM Electronic GmbH, Texas Instruments, NXP Semiconductors, AMS AG, Renesas Electronics, Eaton Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial sensor market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This comprehensive segmentation allows for a detailed analysis of market dynamics across various dimensions, including sensor types, underlying technologies, target end-use industries, specific functions performed, and connectivity methods. Each segment offers unique insights into demand patterns, technological preferences, and application-specific requirements. Understanding these segments is crucial for stakeholders to identify lucrative niche markets, tailor product development, and formulate effective market entry strategies, ultimately contributing to a more precise market forecast and strategic positioning within the complex industrial automation landscape.

By dissecting the market based on these granular attributes, the report highlights the areas of highest growth potential and identifies emerging trends within specific applications or technological advancements. For instance, the demand for vision sensors in robotic automation within the manufacturing sector or the increasing adoption of MEMS technology due to miniaturization benefits can be accurately tracked. This detailed breakdown ensures that the analysis captures the full spectrum of the industrial sensor market, from foundational components to advanced integrated systems, and provides a clear roadmap for future investment and innovation. The insights derived from this segmentation are vital for companies aiming to optimize their product portfolios and expand their market presence effectively.

- By Type: This segment includes a wide array of sensors based on their physical measurement capabilities.

- Position Sensors: Linear, Rotary, Proximity, Displacement

- Pressure Sensors: Absolute, Gauge, Differential, Vacuum

- Temperature Sensors: Thermocouple, RTD (Resistance Temperature Detector), Thermistor, Infrared

- Level Sensors: Point Level, Continuous Level

- Flow Sensors: Mass Flow, Volumetric Flow

- Proximity Sensors

- Optical Sensors

- Vision Sensors

- Others (e.g., Force, Humidity, Gas sensors)

- By Technology: This segment categorizes sensors based on the underlying technological principles and manufacturing processes.

- MEMS (Micro-Electro-Mechanical Systems)

- CMOS (Complementary Metal-Oxide-Semiconductor)

- Nanosensors

- Fiber Optic

- Others (e.g., Piezoelectric, Hall Effect)

- By End-Use Industry: This segment analyzes the adoption of industrial sensors across various industrial sectors.

- Manufacturing: Automotive, Electronics, Food & Beverage, Pharmaceutical, Chemicals

- Oil & Gas

- Mining

- Energy & Power

- Healthcare

- Building Automation

- Agriculture

- Water & Wastewater Management

- Aerospace & Defense

- Others (e.g., Logistics, Retail)

- By Function: This segment groups sensors based on their primary operational role within industrial processes.

- Detection

- Measurement

- Control

- Monitoring

- By Connectivity: This segment differentiates sensors based on their method of data transmission.

- Wired

- Wireless

Regional Highlights

- North America: This region is a significant market for industrial sensors, driven by early adoption of advanced manufacturing technologies, robust investments in industrial automation, and the presence of numerous key market players and R&D centers. The strong focus on smart factories, predictive maintenance, and the expansion of the aerospace and defense sectors contribute to its leading position. The United States and Canada are key contributors, with ongoing initiatives to upgrade industrial infrastructure and integrate IIoT solutions.

- Europe: Europe represents a mature and technologically advanced market for industrial sensors, characterized by strong emphasis on Industry 4.0 initiatives, particularly in countries like Germany. High adoption rates in the automotive, machinery, and pharmaceutical industries, coupled with stringent environmental regulations driving demand for efficient process monitoring, bolster market growth. Western European countries are at the forefront of implementing smart manufacturing solutions and sustainable industrial practices.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by rapid industrialization, increasing manufacturing activities, and significant government investments in smart city projects and industrial automation. Countries like China, Japan, South Korea, and India are key drivers, with China leading in terms of production and consumption. The expanding electronics, automotive, and food & beverage sectors are fueling the demand for various types of industrial sensors across this region.

- Latin America: This region demonstrates steady growth, primarily influenced by increasing investments in manufacturing, oil & gas, and mining sectors. Countries such as Brazil and Mexico are experiencing growth due to foreign direct investment in manufacturing and the modernization of existing industrial facilities. The adoption of automation solutions is gradually increasing, albeit at a slower pace compared to developed regions, indicating significant future potential.

- Middle East and Africa (MEA): The MEA region is emerging as a growth market, driven by diversification efforts away from oil-dependent economies, particularly in the Gulf Cooperation Council (GCC) countries. Investments in infrastructure development, smart city initiatives (e.g., NEOM in Saudi Arabia), and the expansion of the manufacturing sector are creating new opportunities for industrial sensor deployment. The oil & gas sector remains a significant consumer of robust and reliable sensors for monitoring and control applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Sensor Market.- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- Schneider Electric

- Rockwell Automation Inc.

- Emerson Electric Co.

- TE Connectivity

- Bosch Sensortec GmbH

- Omron Corporation

- Keyence Corporation

- STMicroelectronics N.V.

- Sick AG

- Balluff GmbH

- IFM Electronic GmbH

- Texas Instruments

- NXP Semiconductors

- AMS AG

- Renesas Electronics

- Eaton Corporation

Frequently Asked Questions

What is an industrial sensor?

An industrial sensor is a device designed to detect, measure, and transmit physical quantities, chemical properties, or the presence of objects within industrial environments. These devices convert real-world phenomena into electrical signals that can be interpreted and used by control systems, enabling automation, monitoring, and process optimization in factories, plants, and other industrial settings.

What are the primary applications of industrial sensors?

Industrial sensors are widely used across various applications including manufacturing automation, predictive maintenance, quality control, process monitoring, robotics, smart factory operations, and environmental sensing. They are critical for ensuring operational efficiency, safety, and productivity in sectors like automotive, electronics, food and beverage, oil and gas, and pharmaceutical industries.

What are the latest technological advancements in industrial sensors?

Recent advancements in industrial sensors include significant progress in miniaturization, enhanced wireless connectivity (e.g., 5G, LoRaWAN), integration with AI and machine learning for intelligent data processing at the edge, development of self-powered and energy-harvesting sensors, and the emergence of multi-sensor fusion systems for comprehensive data collection.

How does Industry 4.0 impact the industrial sensor market?

Industry 4.0 significantly boosts the industrial sensor market by driving the demand for smart, connected, and data-generating sensors. These sensors are foundational for enabling real-time data collection, analytics, and control within smart factories, supporting concepts like predictive maintenance, autonomous operations, and seamless human-machine interaction, thereby accelerating digital transformation.

What is the future outlook for the industrial sensor market?

The future outlook for the industrial sensor market is highly positive, driven by the ongoing global push for industrial automation, the proliferation of IIoT devices, and increasing investments in smart manufacturing infrastructure. The market is expected to witness continued innovation in sensor capabilities, expanding applications into new industry verticals, and a growing emphasis on AI-driven analytics for enhanced operational intelligence and efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted