Industrial Rectifier Market

Industrial Rectifier Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708189 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Industrial Rectifier Market Size

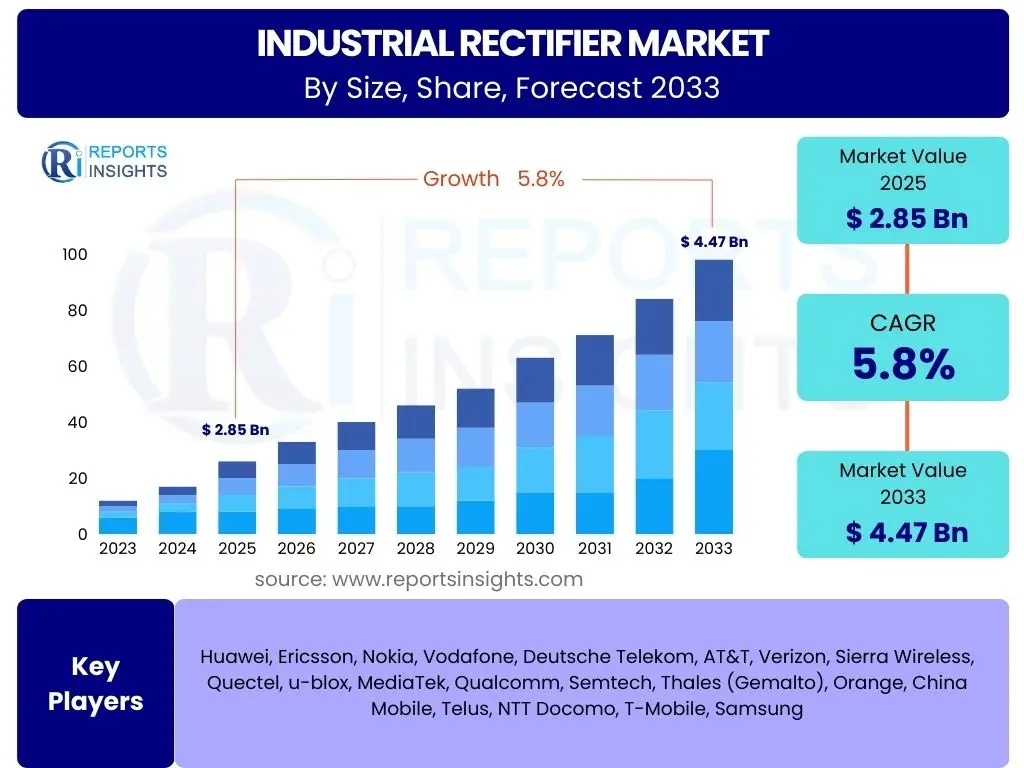

According to Reports Insights Consulting Pvt Ltd, The Industrial Rectifier Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 4.47 billion by the end of the forecast period in 2033.

Key Industrial Rectifier Market Trends & Insights

The industrial rectifier market is experiencing dynamic shifts driven by advancements in power electronics and evolving industrial demands. Key trends indicate a strong focus on enhancing energy efficiency, integrating renewable energy sources, and adapting to the requirements of digitalized industrial processes. The growing need for stable and reliable DC power in various heavy industries, coupled with the global push towards sustainable energy solutions, is shaping the market landscape. These trends reflect a broader industrial movement towards optimization, automation, and environmental responsibility.

Further insights highlight the increasing adoption of high-power density rectifiers that offer improved performance in smaller footprints. There is a notable surge in demand for modular and customizable rectifier solutions, allowing industries to scale their power systems according to specific operational needs. Additionally, the market is witnessing an emphasis on robust designs capable of operating in harsh industrial environments, ensuring durability and prolonged operational life. The integration of smart monitoring and control features is also gaining traction, enabling predictive maintenance and enhancing system reliability.

- Focus on enhanced energy efficiency and power factor correction.

- Rising integration with renewable energy systems (solar, wind).

- Increasing demand for high-power density and compact rectifier solutions.

- Shift towards modular and customizable designs for varied industrial applications.

- Growing adoption of smart features for monitoring, control, and predictive maintenance.

- Development of robust rectifiers for harsh operating conditions.

- Utilisation of advanced semiconductor materials like SiC and GaN for improved performance.

AI Impact Analysis on Industrial Rectifier

The integration of Artificial Intelligence (AI) into the industrial rectifier domain is poised to revolutionize operational efficiency and system reliability. Common user questions often revolve around how AI can optimize power management, predict failures, and enhance the overall performance of rectifier units. The analysis indicates that AI's primary influence will be through advanced diagnostics, predictive maintenance, and real-time operational adjustments, moving industrial rectifiers beyond traditional reactive maintenance models to proactive, data-driven management. This paradigm shift is expected to significantly reduce downtime, lower operational costs, and extend the lifespan of critical power infrastructure.

Users express strong expectations for AI to facilitate intelligent load balancing, optimize energy consumption through dynamic adjustments based on demand patterns, and improve fault detection mechanisms. Concerns often include the complexity of integrating AI systems with existing legacy infrastructure and the need for robust cybersecurity measures to protect connected devices. Despite these challenges, the potential for AI to transform industrial rectifiers into smarter, more resilient, and self-optimizing components within a broader industrial ecosystem is widely recognized as a significant growth vector for the market, enabling more efficient and sustainable power conversion solutions.

- Enabling predictive maintenance through anomaly detection and operational data analysis.

- Optimizing power conversion efficiency by dynamic load management and voltage regulation.

- Facilitating intelligent fault diagnosis and rapid system recovery.

- Enhancing energy management through AI-driven demand forecasting and resource allocation.

- Supporting integration into smart grid architectures for seamless power flow.

- Automating operational parameters and remote monitoring capabilities.

- Improving system reliability and extending equipment lifespan.

Key Takeaways Industrial Rectifier Market Size & Forecast

The Industrial Rectifier Market is poised for substantial growth, driven by an accelerating pace of industrialization, the global expansion of renewable energy capacity, and increasing investments in robust power infrastructure across diverse sectors. A significant takeaway from the market forecast is the consistent demand for high-performance and energy-efficient power conversion solutions, particularly within manufacturing, telecommunications, and heavy industries. The market's resilience is further bolstered by the continuous need for stable direct current (DC) power for critical applications, ensuring uninterrupted operations and supporting technological advancements.

Another crucial insight is the anticipated regional variations in market expansion, with developing economies in Asia Pacific and Latin America expected to lead growth due to rapid infrastructure development and industrial expansion. Conversely, mature markets in North America and Europe will focus on modernization, efficiency upgrades, and the integration of smart technologies. The forecast underscores the importance of technological innovation in meeting stringent energy regulations and addressing the rising complexity of power systems. Stakeholders will need to prioritize R&D in advanced materials and smart functionalities to capitalize on emerging opportunities and maintain competitive advantages.

- Robust market growth projected through 2033, driven by industrial expansion and technological advancements.

- Increasing demand for energy-efficient and reliable DC power solutions across industries.

- Significant growth opportunities in renewable energy integration and smart grid development.

- Asia Pacific is expected to remain a dominant region due to rapid industrialization and infrastructure projects.

- Focus on predictive maintenance and AI integration for enhanced system reliability and efficiency.

- Continuous innovation in power electronics and semiconductor technology is critical for market competitiveness.

Industrial Rectifier Market Drivers Analysis

The industrial rectifier market is significantly propelled by several key drivers that reflect global industrial and technological shifts. A primary driver is the accelerating trend of industrial automation and digitalization, often associated with Industry 4.0 initiatives. As industries adopt more automated processes, robotic systems, and advanced machinery, the demand for stable, reliable, and precise DC power supply intensifies, making industrial rectifiers an indispensable component. These rectifiers ensure the continuous and efficient operation of critical equipment, minimizing downtime and optimizing production outputs across various sectors.

Furthermore, the rapid expansion of renewable energy infrastructure, particularly solar and wind power, serves as a substantial catalyst for market growth. Rectifiers are essential for converting the alternating current (AC) generated by these sources into direct current (DC) for energy storage or into suitable AC forms for grid integration. This green energy transition, coupled with increasing investments in telecommunications, data centers, and electric vehicle (EV) charging infrastructure, further solidifies the demand for high-performance industrial rectifiers. The ongoing modernization and expansion of existing industrial facilities worldwide also contribute to the consistent uptake of advanced rectifier solutions, as industries strive for greater energy efficiency and operational resilience.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrial Automation and Digitalization (Industry 4.0) | +1.5% | Global, particularly North America, Europe, APAC (China, Japan, South Korea) | Short to Medium Term (2025-2029) |

| Rapid Expansion of Renewable Energy Infrastructure | +1.2% | Global, particularly Europe, APAC (China, India), North America | Medium to Long Term (2026-2033) |

| Increasing Investment in Data Centers and Telecommunications | +0.9% | North America, APAC, Europe | Short to Medium Term (2025-2030) |

| Modernization and Expansion of Existing Industrial Facilities | +0.8% | Global, particularly Emerging Economies (APAC, Latin America) | Medium Term (2025-2031) |

| Growing Demand for Electric Vehicle (EV) Charging Infrastructure | +0.7% | Europe, North America, APAC (China) | Medium to Long Term (2027-2033) |

Industrial Rectifier Market Restraints Analysis

Despite robust growth prospects, the industrial rectifier market faces several significant restraints that could potentially impede its expansion. One prominent restraint is the high initial capital expenditure associated with deploying advanced industrial rectifier systems. Many small and medium-sized enterprises (SMEs) and even larger corporations may find the upfront costs of purchasing, installing, and integrating these sophisticated power conversion units challenging, especially when considering the additional expenses for ancillary equipment and infrastructure upgrades. This can lead to a slower adoption rate, particularly in budget-sensitive regions or industries.

Another critical restraint involves the technical complexities and challenges associated with integrating new rectifier systems into existing legacy industrial infrastructure. Older facilities often operate with antiquated power distribution networks and control systems, making the seamless integration of modern, digitally-controlled rectifiers a complex and resource-intensive task. Furthermore, the market is susceptible to the volatility of raw material prices, such as copper, aluminum, and silicon, which are crucial components in rectifier manufacturing. Fluctuations in these prices can directly impact production costs, leading to increased final product prices and potentially dampening demand. Additionally, intense competition from alternative power conversion technologies and the availability of lower-cost, albeit less efficient, solutions in some market segments further contribute to market restraints.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure for Advanced Systems | -0.8% | Global, particularly Emerging Economies | Short to Medium Term (2025-2029) |

| Complex Integration with Legacy Industrial Infrastructure | -0.6% | Global, particularly Mature Markets (Europe, North America) | Medium Term (2026-2031) |

| Fluctuating Raw Material Prices and Supply Chain Volatility | -0.5% | Global | Short Term (2025-2027) |

| Availability of Alternative Power Conversion Technologies | -0.4% | Global | Medium Term (2027-2033) |

| Stringent Regulatory and Certification Requirements | -0.3% | Europe, North America | Ongoing |

Industrial Rectifier Market Opportunities Analysis

The industrial rectifier market is rich with opportunities stemming from global shifts towards sustainable energy, advanced manufacturing, and digitalization. A significant opportunity lies in the burgeoning development of smart grid infrastructure worldwide. As grids become more intelligent and resilient, the demand for sophisticated power conversion devices that can efficiently manage bidirectional power flow and integrate diverse energy sources, including renewables, will grow exponentially. Industrial rectifiers are pivotal in ensuring grid stability, enabling effective energy storage, and supporting the flexible operation of modern electrical networks, thereby presenting a substantial growth avenue.

Furthermore, the rapid global expansion of electric vehicle (EV) charging infrastructure offers another compelling opportunity. High-power rectifiers are fundamental components in fast charging stations, converting grid AC power into the DC power required for EV batteries. As governments and private entities invest heavily in deploying extensive EV charging networks, the demand for robust and efficient industrial rectifiers will surge. Beyond this, opportunities abound in untapped or underserved markets, particularly in developing economies experiencing rapid industrialization and urbanization. These regions often have nascent industrial sectors and burgeoning infrastructure projects that necessitate reliable power solutions, opening doors for market entry and expansion. The continuous innovation in wide-bandgap semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) also presents an opportunity to develop more compact, efficient, and higher-performing rectifiers, catering to evolving industrial requirements and pushing technological boundaries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Smart Grid Infrastructure | +1.3% | Global, particularly Europe, North America, China | Medium to Long Term (2026-2033) |

| Emergence of Electric Vehicle (EV) Charging Infrastructure | +1.1% | Europe, North America, APAC (China) | Medium to Long Term (2027-2033) |

| Untapped Markets in Developing Economies (e.g., Africa, Southeast Asia) | +0.9% | APAC, Latin America, MEA | Medium Term (2025-2031) |

| Advancements in Wide-Bandgap Semiconductor Technologies (SiC, GaN) | +0.8% | Global, particularly R&D Hubs | Long Term (2028-2033) |

| Customization and Modular Design for Diverse Industrial Applications | +0.6% | Global | Short to Medium Term (2025-2030) |

Industrial Rectifier Market Challenges Impact Analysis

The industrial rectifier market is not without its significant challenges, which require strategic responses from manufacturers and stakeholders to ensure sustained growth. A primary challenge is the intense market competition, leading to considerable price pressure. With numerous established and emerging players vying for market share, companies are often forced to reduce profit margins to remain competitive, especially in segments where product differentiation is minimal. This competitive landscape necessitates continuous innovation and cost-effective production methods to maintain viability and profitability, pushing companies to invest heavily in research and development.

Meeting stringent and evolving regulatory standards for energy efficiency, electromagnetic compatibility (EMC), and environmental compliance presents another substantial hurdle. Different regions and countries impose varying regulations, requiring manufacturers to develop versatile product lines that can meet diverse compliance requirements, which adds to design complexity and certification costs. Furthermore, the technical complexity involved in designing high-power, compact, and highly reliable rectifier systems, particularly for specialized applications, poses a significant engineering challenge. Ensuring optimal performance, thermal management, and robust operation in harsh industrial environments demands advanced technical expertise and meticulous design processes. Finally, the industrial rectifier market also faces challenges related to the shortage of skilled labor for the installation, maintenance, and servicing of complex power electronic systems, potentially affecting market adoption and operational efficiency in certain regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressure | -0.7% | Global | Ongoing |

| Meeting Stringent Regulatory Standards (Efficiency, EMC) | -0.5% | Europe, North America, China | Ongoing |

| Technical Complexity in Designing High-Power, Compact, and Reliable Systems | -0.4% | Global | Ongoing |

| Shortage of Skilled Labor for Installation and Maintenance | -0.3% | Global, particularly Developing Economies | Medium Term (2025-2031) |

| Vulnerability to Cybersecurity Threats in Connected Systems | -0.2% | Global | Long Term (2028-2033) |

Industrial Rectifier Market - Updated Report Scope

This report provides a comprehensive analysis of the global Industrial Rectifier Market, segmenting it across various dimensions including type, phase, power rating, and end-use industry, alongside an in-depth regional assessment. It covers market size, growth drivers, restraints, opportunities, challenges, and competitive landscape. The scope extends to analyzing the impact of emerging technologies like AI and advanced semiconductor materials on market dynamics, offering a forward-looking perspective on the industry's trajectory. The insights are designed to assist stakeholders in making informed strategic decisions and identifying key growth areas within the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 4.47 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., Schneider Electric SE, Eaton Corporation, General Electric Company, Fuji Electric Co., Ltd., Delta Electronics, Inc., TDK-Lambda Corporation, Murata Manufacturing Co., Ltd., Vertiv Holdings Co, Hitachi, Ltd., Mitsubishi Electric Corporation, Advanced Energy Industries, Inc., Cosel Co., Ltd., MEAN WELL Enterprises Co., Ltd., Lite-On Technology Corporation, CUI Inc., Sanken Electric Co., Ltd., Infineon Technologies AG, Vicor Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial rectifier market is extensively segmented to reflect the diversity of products and applications, providing a granular view of market dynamics. These segmentations are critical for understanding specific growth drivers, competitive landscapes, and technological preferences within different industrial contexts. The primary segmentation categories include product type, phase, power rating, and end-use industry, each offering unique insights into market demands and opportunities.

Analyzing these segments allows for a targeted approach to market strategy, identifying which rectifier types or power ratings are gaining traction in particular industries or regions. For instance, the demand for controlled rectifiers with higher power ratings is robust in heavy industries like metal and mining, while uncontrolled rectifiers might find broader application in less demanding settings. Understanding the nuances of these segmentations is key to navigating the complex industrial rectifier landscape, enabling businesses to tailor their offerings to precise market needs and capitalize on emerging trends.

- By Type:

- Controlled Rectifiers

- Uncontrolled Rectifiers

- By Phase:

- Single-Phase Rectifiers

- Three-Phase Rectifiers

- By Power Rating:

- Low Power Rectifiers (Up to 10kW)

- Medium Power Rectifiers (10kW-100kW)

- High Power Rectifiers (Above 100kW)

- By End-Use Industry:

- Metal & Mining

- Oil & Gas

- Chemical

- Power Generation & Utilities

- Telecommunications

- Automotive

- Data Centers

- Marine

- Defense

- Others

Regional Highlights

- North America: This region demonstrates a strong demand for industrial rectifiers driven by the modernization of existing industrial infrastructure, significant investments in data centers, and the growing adoption of renewable energy sources. The presence of advanced manufacturing facilities and a high rate of technological integration, including AI and IoT in industrial processes, further bolsters market growth. Emphasis on energy efficiency and robust power solutions for critical applications defines this market.

- Europe: Europe is characterized by stringent environmental regulations and a strong focus on industrial automation and decarbonization efforts. The region's push towards smart grids and the substantial growth in offshore wind and solar energy projects necessitate high-efficiency industrial rectifiers. Western European countries, in particular, lead in adopting advanced power electronics for diverse industrial applications, including automotive and heavy manufacturing.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to rapid industrialization, extensive infrastructure development, and substantial investments in manufacturing capabilities across countries like China, India, Japan, and South Korea. The region's expanding telecommunications sector, burgeoning data center market, and large-scale renewable energy projects are primary drivers. The increasing demand for electric vehicles also contributes significantly to the growth of high-power rectifier solutions.

- Latin America: This region is experiencing steady growth in the industrial rectifier market, primarily fueled by infrastructure development projects, growth in the mining and oil and gas sectors, and increasing industrialization. While currently smaller in market share compared to APAC or Europe, the ongoing economic development and foreign investments are creating new opportunities for power electronics, including industrial rectifiers, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): The MEA region is characterized by significant investments in the oil and gas industry, infrastructure development, and emerging renewable energy projects. Countries like Saudi Arabia and the UAE are diversifying their economies, leading to the growth of various industrial sectors requiring reliable power solutions. The market here is still nascent but shows considerable potential for expansion, particularly with increasing government initiatives towards industrial modernization and energy diversification.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Rectifier Market.- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- Eaton Corporation

- General Electric Company

- Fuji Electric Co., Ltd.

- Delta Electronics, Inc.

- TDK-Lambda Corporation

- Murata Manufacturing Co., Ltd.

- Vertiv Holdings Co

- Hitachi, Ltd.

- Mitsubishi Electric Corporation

- Advanced Energy Industries, Inc.

- Cosel Co., Ltd.

- MEAN WELL Enterprises Co., Ltd.

- Lite-On Technology Corporation

- CUI Inc.

- Sanken Electric Co., Ltd.

- Infineon Technologies AG

- Vicor Corporation

Frequently Asked Questions

What is an industrial rectifier and its primary function?

An industrial rectifier is an electrical device that converts alternating current (AC) into direct current (DC), primarily used in industrial applications requiring a stable and reliable DC power supply. Its main function is to provide controlled DC power for various processes such as electrolysis, motor drives, charging batteries, and operating sensitive electronic equipment in manufacturing, telecommunications, and heavy industries.

Which end-use industries drive the demand for industrial rectifiers?

The demand for industrial rectifiers is predominantly driven by industries such as metal and mining, oil and gas, chemical processing, power generation and utilities, telecommunications, automotive manufacturing, and data centers. These sectors rely heavily on stable DC power for their operational processes, automation systems, and critical infrastructure, ensuring efficiency and continuity.

How does AI impact the future of the industrial rectifier market?

AI significantly impacts the industrial rectifier market by enabling advanced capabilities such as predictive maintenance, real-time operational optimization, and intelligent fault detection. AI integration enhances system reliability, reduces downtime, and improves energy efficiency through data-driven adjustments, transforming rectifiers into smarter, more autonomous components within industrial ecosystems.

What are the key factors driving the growth of the Industrial Rectifier Market?

The key factors driving market growth include increasing industrial automation and digitalization, the rapid expansion of renewable energy infrastructure, rising investments in data centers and telecommunications, and the ongoing modernization of industrial facilities. These trends collectively necessitate reliable and efficient DC power solutions provided by industrial rectifiers.

Which geographical region is expected to lead the Industrial Rectifier Market growth?

The Asia Pacific (APAC) region is expected to lead the Industrial Rectifier Market growth. This is primarily due to rapid industrialization, extensive infrastructure development projects, a booming manufacturing sector, and significant investments in renewable energy and telecommunications across countries like China, India, and other Southeast Asian nations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted