Industrial Plastic Waste Recycling Market

Industrial Plastic Waste Recycling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703020 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

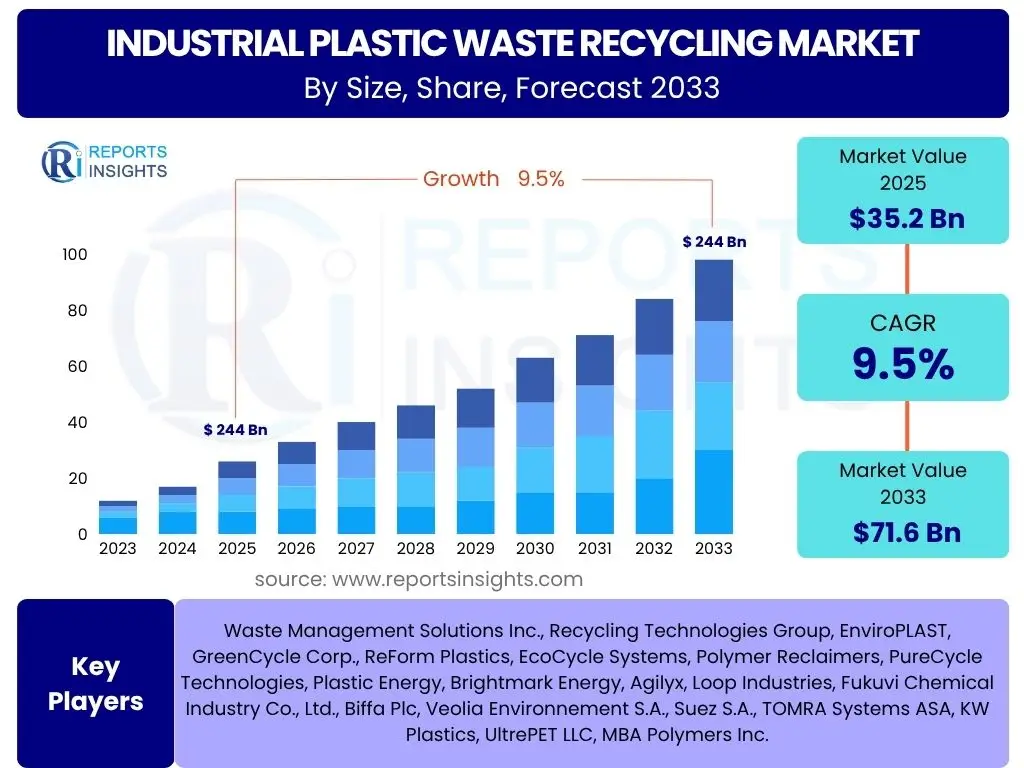

Industrial Plastic Waste Recycling Market Size

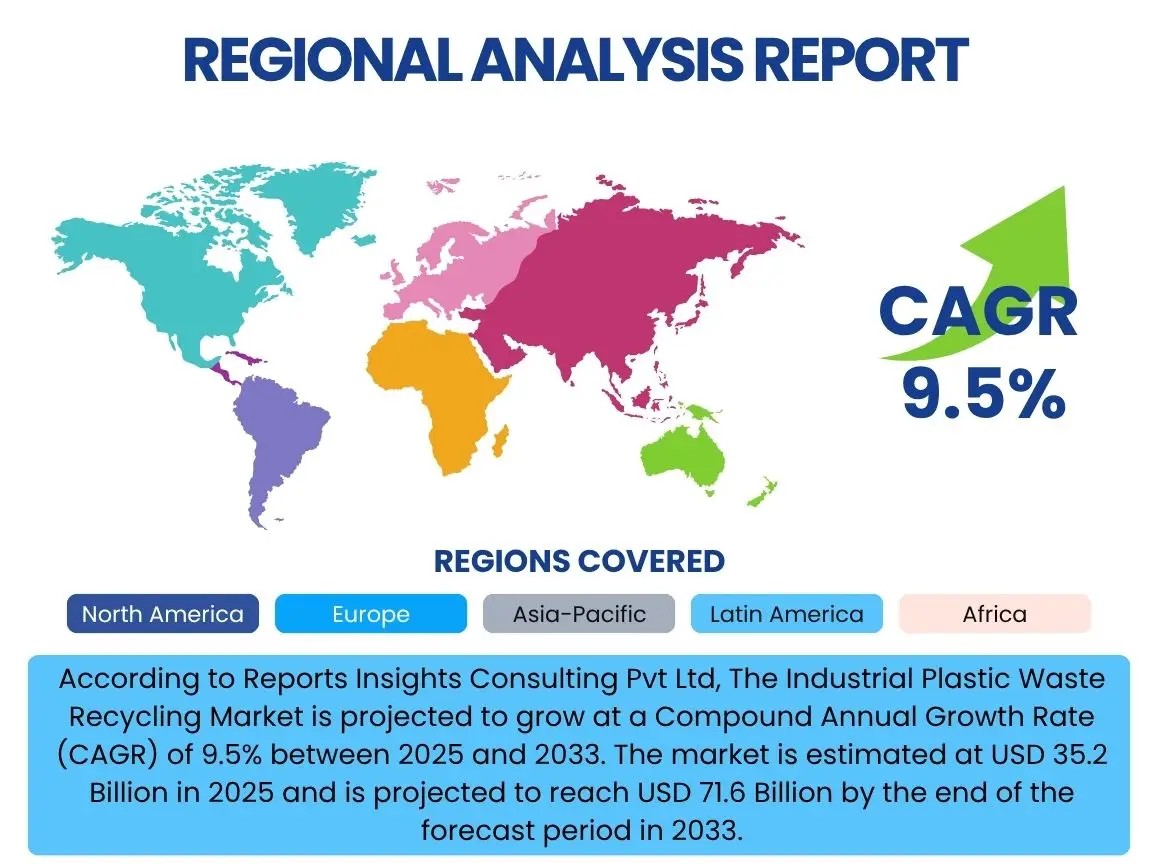

According to Reports Insights Consulting Pvt Ltd, The Industrial Plastic Waste Recycling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 35.2 Billion in 2025 and is projected to reach USD 71.6 Billion by the end of the forecast period in 2033.

Key Industrial Plastic Waste Recycling Market Trends & Insights

The Industrial Plastic Waste Recycling market is experiencing dynamic shifts driven by a global push towards circular economy principles and heightened environmental consciousness. Stakeholders are keen to understand the prevailing trends influencing market growth, including the increasing adoption of advanced recycling technologies and the impact of stringent regulatory frameworks. Key trends also encompass the growing demand for recycled content from various industries and the collaborative efforts between public and private sectors to enhance collection and sorting infrastructure. The evolution of materials science and processing techniques is further enabling the recycling of previously difficult-to-recycle plastics, opening new avenues for market expansion and value creation across the supply chain.

Furthermore, the market is witnessing significant investments in research and development aimed at improving the efficiency and economic viability of recycling processes. This includes innovations in sorting technologies, such as optical and robotic sorting, and the development of more energy-efficient recycling methods. The trend towards extended producer responsibility (EPR) schemes is also gaining momentum globally, placing greater onus on manufacturers for the end-of-life management of their plastic products. These collective trends highlight a market moving towards greater sustainability, technological sophistication, and integrated value chains.

- Accelerated adoption of circular economy models across industries.

- Increasing implementation of Extended Producer Responsibility (EPR) schemes.

- Significant advancements in chemical recycling technologies (e.g., pyrolysis, depolymerization).

- Rising corporate commitments to utilize recycled content in product manufacturing.

- Enhanced focus on automated sorting and separation technologies for mixed plastic waste.

- Growth in demand for high-quality recycled plastics by end-use industries.

AI Impact Analysis on Industrial Plastic Waste Recycling

Artificial Intelligence (AI) is poised to revolutionize the industrial plastic waste recycling sector by enhancing efficiency, accuracy, and operational intelligence. Common inquiries revolve around how AI can optimize sorting processes, improve material identification, and contribute to overall waste management effectiveness. AI-powered systems, particularly those utilizing computer vision and machine learning, are becoming instrumental in recognizing and separating different types of plastics with unprecedented precision, thereby reducing contamination rates and increasing the purity of recycled materials. This technological integration addresses critical challenges faced by traditional recycling methods, leading to higher quality outputs and more economically viable recycling operations.

Beyond sorting, AI’s influence extends to predictive maintenance for recycling machinery, optimizing logistics for waste collection and transport, and providing valuable data analytics for better resource management. By analyzing vast datasets, AI can identify patterns in waste streams, forecast material availability, and even suggest optimal processing parameters to maximize yield and minimize energy consumption. This holistic application of AI promises to transform the recycling industry into a more data-driven, efficient, and sustainable ecosystem, offering solutions to complex challenges like material traceability and end-to-end supply chain optimization. The deployment of AI is therefore seen as a key enabler for scaling recycling operations and achieving higher rates of plastic waste diversion from landfills.

- Enhanced sorting accuracy and speed through AI-powered computer vision.

- Optimized operational efficiency and throughput in recycling facilities.

- Predictive maintenance for machinery, reducing downtime and operational costs.

- Improved quality control and material purity through advanced identification.

- Data analytics for waste stream characterization and supply chain optimization.

- Robotic process automation for hazardous or repetitive tasks.

Key Takeaways Industrial Plastic Waste Recycling Market Size & Forecast

The Industrial Plastic Waste Recycling market is poised for substantial expansion, with key takeaways highlighting its strong growth trajectory and increasing strategic importance. The market’s projected CAGR indicates a robust demand for recycled plastic materials and a growing investment in recycling infrastructure globally. This sustained growth is a direct reflection of evolving regulatory landscapes, heightened corporate sustainability commitments, and advancements in recycling technologies that make processing more efficient and economically attractive. Stakeholders should recognize the critical role of innovation in driving this market forward, particularly in areas like chemical recycling and advanced sorting techniques, which are enabling higher value recovery from diverse plastic waste streams.

Furthermore, the market forecast underscores a shift towards a more circular economy, where plastic is viewed as a valuable resource rather than waste. This paradigm shift creates significant investment opportunities across the value chain, from waste collection and sorting to processing and end-product manufacturing using recycled content. The increasing pressure from consumers and investors for sustainable practices is also a powerful underlying factor, compelling industries to adopt more environmentally responsible approaches. Therefore, the long-term outlook for industrial plastic waste recycling remains highly positive, driven by both environmental necessity and compelling economic incentives.

- The market is set for robust growth, driven by environmental mandates and economic incentives.

- Technological innovation, particularly in chemical recycling, is a primary growth catalyst.

- Increased demand for Post-Consumer Recycled (PCR) content is bolstering market value.

- Regulatory frameworks, such as EPR schemes, are critical in shaping market dynamics.

- Significant investment opportunities exist across the recycling value chain.

- Global shifts towards a circular economy are fundamentally reshaping the industry.

Industrial Plastic Waste Recycling Market Drivers Analysis

The growth of the Industrial Plastic Waste Recycling market is primarily propelled by a confluence of stringent environmental regulations, growing corporate sustainability initiatives, and technological advancements that enhance recycling efficiency. Governments worldwide are implementing stricter policies on waste management, including bans on single-use plastics and mandates for recycled content in new products, thereby creating a compelling demand for recycled plastic. Simultaneously, major corporations are setting ambitious sustainability goals, driven by consumer pressure and investor expectations, leading to an increased adoption of recycled materials in their manufacturing processes. These factors collectively stimulate investment in recycling infrastructure and drive innovation in processing technologies, making recycling an increasingly attractive and necessary component of industrial operations.

Furthermore, the rising global consumption of plastics across various industrial sectors inevitably leads to a larger volume of plastic waste, intensifying the need for effective recycling solutions. Breakthroughs in recycling technologies, such as advanced mechanical recycling methods and the burgeoning field of chemical recycling, are transforming the economic viability of processing diverse plastic types, including those previously considered non-recyclable. These technological leaps are overcoming traditional barriers like contamination and mixed plastic streams, unlocking new opportunities for resource recovery and contributing significantly to the market's expansion. The combined effect of regulatory push, corporate responsibility, and technological innovation creates a powerful impetus for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | +2.5% | Europe, North America, APAC | 2025-2033 |

| Rising Corporate Sustainability Goals | +2.0% | Global | 2025-2033 |

| Technological Advancements in Recycling | +1.8% | Global | 2025-2033 |

| Increasing Demand for Recycled Content | +1.5% | Global | 2025-2033 |

| Growth in Plastic Production & Consumption | +1.0% | Asia Pacific, Latin America | 2025-2033 |

Industrial Plastic Waste Recycling Market Restraints Analysis

Despite the strong growth drivers, the Industrial Plastic Waste Recycling market faces several significant restraints that could impede its full potential. One major challenge is the high cost associated with collecting, sorting, and processing diverse industrial plastic waste streams. The varied composition and contamination levels of industrial plastic waste often necessitate complex and costly sorting technologies, impacting the economic viability of recycling operations, especially for smaller-scale recyclers. Additionally, the fluctuating prices of virgin plastic materials can undermine the competitiveness of recycled plastics; when virgin plastic prices are low, the incentive for industries to use more expensive recycled alternatives diminishes, creating market instability.

Furthermore, limitations in recycling infrastructure, particularly in developing regions, pose a substantial hurdle. Inadequate collection systems, a lack of advanced sorting facilities, and limited processing capacities can restrict the volume of plastic waste that can be effectively recycled. Technical challenges, such as the degradation of plastic quality after multiple recycling cycles and the difficulty in recycling certain complex or mixed plastic types, also present significant constraints. Overcoming these restraints requires substantial investment in infrastructure, policy support, and continued technological innovation to ensure the long-term sustainability and growth of the industrial plastic recycling sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Collection and Sorting Costs | -1.2% | Global | 2025-2030 |

| Fluctuating Virgin Plastic Prices | -1.0% | Global | 2025-2028 |

| Limited Recycling Infrastructure | -0.8% | Developing Regions | 2025-2033 |

| Quality Degradation of Recycled Plastics | -0.5% | Global | 2025-2033 |

Industrial Plastic Waste Recycling Market Opportunities Analysis

The Industrial Plastic Waste Recycling market is ripe with opportunities driven by innovation, evolving regulatory landscapes, and increasing demand for sustainable materials. One significant opportunity lies in the rapid development and commercialization of chemical recycling technologies, such as pyrolysis and depolymerization. These advanced methods can process mixed and contaminated plastics that are difficult to recycle mechanically, producing high-quality feedstocks for new plastic production, effectively closing the loop. This opens up new revenue streams and expands the types of plastic waste that can be diverted from landfills, addressing a critical gap in current recycling capabilities and increasing the overall recovery rate of plastic resources.

Furthermore, the growing emphasis on Extended Producer Responsibility (EPR) schemes globally presents a substantial opportunity for recycling service providers and technology developers. As producers become more accountable for the end-of-life management of their products, there will be increased investment in collection, sorting, and recycling infrastructure, fostering partnerships and creating new business models. Additionally, the burgeoning demand for recycled content across diverse end-use industries, including automotive, packaging, and construction, offers significant market expansion potential. Companies capable of supplying high-quality, consistent recycled materials will gain a competitive advantage, leveraging the market's shift towards sustainability and circularity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Chemical Recycling Technologies | +1.8% | Global | 2028-2033 |

| Increasing Investment in EPR Schemes | +1.5% | Europe, North America, Asia Pacific | 2025-2033 |

| Growth in End-Use Applications for Recycled Content | +1.2% | Global | 2025-2033 |

| Development of Advanced Sorting Solutions | +1.0% | Global | 2025-2030 |

Industrial Plastic Waste Recycling Market Challenges Impact Analysis

The Industrial Plastic Waste Recycling market, while promising, faces several inherent challenges that require innovative solutions and strategic interventions. One significant challenge is the inherent complexity and heterogeneity of industrial plastic waste streams. Industrial processes generate a wide variety of plastic types, often mixed with other materials or contaminants, making efficient sorting and processing difficult. This complexity necessitates advanced and costly sorting technologies, and even then, achieving high purity levels can be a challenge, impacting the quality and marketability of the recycled output. Furthermore, the decentralized nature of industrial waste generation across diverse industries and locations poses logistical hurdles for efficient collection and aggregation, leading to higher transportation costs.

Another major challenge revolves around the regulatory and economic landscape. Despite increasing environmental awareness, a lack of globally standardized recycling policies and enforcement can hinder investment and widespread adoption of best practices. The high capital expenditure required for setting up and operating modern recycling facilities, especially those incorporating advanced chemical recycling technologies, can be a barrier for new entrants and small-to-medium enterprises. Additionally, energy-intensive recycling processes contribute to operational costs and may have their own environmental footprint if not managed with renewable energy sources. Addressing these challenges is crucial for unlocking the full potential of the industrial plastic waste recycling market and ensuring its sustainable growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Industrial Waste Streams | -1.0% | Global | 2025-2030 |

| High Capital Investment Requirements | -0.8% | Global | 2025-2033 |

| Lack of Standardized Collection Systems | -0.7% | Developing Regions | 2025-2033 |

| Energy Intensity of Recycling Processes | -0.5% | Global | 2025-2033 |

Industrial Plastic Waste Recycling Market - Updated Report Scope

This report provides a comprehensive analysis of the Industrial Plastic Waste Recycling market, offering in-depth insights into its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges. It segments the market by plastic type, recycling process, source, and end-use industry, providing a granular view of market dynamics. The study also includes a detailed regional analysis and profiles of leading market players, offering a holistic understanding of the competitive landscape and strategic developments within the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.2 Billion |

| Market Forecast in 2033 | USD 71.6 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Waste Management Solutions Inc., Recycling Technologies Group, EnviroPLAST, GreenCycle Corp., ReForm Plastics, EcoCycle Systems, Polymer Reclaimers, PureCycle Technologies, Plastic Energy, Brightmark Energy, Agilyx, Loop Industries, Fukuvi Chemical Industry Co., Ltd., Biffa Plc, Veolia Environnement S.A., Suez S.A., TOMRA Systems ASA, KW Plastics, UltrePET LLC, MBA Polymers Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Plastic Waste Recycling market is comprehensively segmented to provide a detailed understanding of its diverse components and drivers. This segmentation allows for a nuanced analysis of market dynamics, revealing specific growth areas and challenges within each category. The primary segmentation dimensions include the type of plastic being recycled, the technological process employed for recycling, the industrial source of the plastic waste, and the various end-use industries that utilize recycled plastic materials. Each segment plays a crucial role in shaping the overall market landscape, reflecting distinct supply and demand characteristics.

Analyzing these segments provides valuable insights into market trends, technological preferences, and regional disparities in recycling capabilities and needs. For instance, the prevalence of certain plastic types from specific industrial sources can dictate the dominant recycling processes in a region, while the demand from particular end-use industries can influence the quality and type of recycled material produced. This multi-faceted segmentation helps stakeholders identify key opportunities for investment, innovation, and strategic partnerships, enabling them to tailor solutions that address specific market requirements and contribute to a more efficient and sustainable circular economy for plastics.

- By Plastic Type: Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), Polystyrene (PS), Others.

- By Recycling Process: Mechanical Recycling, Chemical Recycling (Pyrolysis, Gasification, Solvolysis, Depolymerization).

- By Source: Packaging Waste, Automotive, Construction, Electrical & Electronics, Consumer Goods, Others.

- By End-Use Industry: Packaging, Automotive, Building & Construction, Textiles, Electronics, Consumer Goods, Others.

Regional Highlights

- North America: This region demonstrates a strong commitment to industrial plastic waste recycling, driven by increasing environmental regulations, corporate sustainability goals, and technological advancements. The presence of established waste management infrastructure and growing investments in advanced recycling technologies, particularly chemical recycling, are key factors influencing market growth. Demand for recycled content from the packaging and automotive industries is also a significant driver.

- Europe: Europe is a frontrunner in industrial plastic waste recycling, largely due to its ambitious circular economy package, stringent waste management directives, and high rates of plastic collection. Countries within the EU are actively promoting Extended Producer Responsibility (EPR) schemes and setting ambitious targets for recycled content. Innovation in sorting technologies and chemical recycling processes, along with strong public and private sector collaboration, underpin the market's expansion.

- Asia Pacific (APAC): The APAC region is experiencing rapid growth in industrial plastic waste recycling, fueled by escalating plastic consumption, growing environmental concerns, and evolving regulatory frameworks in countries like China, India, and Japan. While challenges related to infrastructure and collection remain, increasing foreign investments, technological transfers, and the establishment of new recycling facilities are creating significant opportunities for market development. The expanding manufacturing sector and rising awareness about sustainability are also contributing factors.

- Latin America: This region is characterized by nascent but growing industrial plastic waste recycling efforts. Increasing environmental awareness, coupled with the implementation of new waste management policies in countries like Brazil and Mexico, is driving market growth. Challenges include informal recycling sectors and limited infrastructure, but opportunities arise from growing industrialization and the need for sustainable waste solutions.

- Middle East and Africa (MEA): The MEA region's industrial plastic waste recycling market is in its early stages but holds substantial potential. Growth is driven by urbanization, industrial development, and a gradual shift towards more sustainable waste management practices. While infrastructure development is a key challenge, rising investments in large-scale industrial projects and a growing focus on diversifying economies away from fossil fuels are creating demand for recycling solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Plastic Waste Recycling Market.- Waste Management Solutions Inc.

- Recycling Technologies Group

- EnviroPLAST

- GreenCycle Corp.

- ReForm Plastics

- EcoCycle Systems

- Polymer Reclaimers

- PureCycle Technologies

- Plastic Energy

- Brightmark Energy

- Agilyx

- Loop Industries

- Fukuvi Chemical Industry Co., Ltd.

- Biffa Plc

- Veolia Environnement S.A.

- Suez S.A.

- TOMRA Systems ASA

- KW Plastics

- UltrePET LLC

- MBA Polymers Inc.

Frequently Asked Questions

What are the primary drivers of growth in the Industrial Plastic Waste Recycling market?

The market is primarily driven by stringent environmental regulations, growing corporate sustainability goals, and significant technological advancements in recycling processes, which collectively increase the demand for recycled plastic content across various industries.

How do chemical recycling technologies impact the Industrial Plastic Waste Recycling market?

Chemical recycling technologies, such as pyrolysis and depolymerization, are a major opportunity as they enable the recycling of mixed and contaminated plastic waste, producing high-quality feedstocks and expanding the range of plastics that can be economically recycled.

What are the main challenges facing the industrial plastic waste recycling sector?

Key challenges include the high costs associated with collecting and sorting diverse industrial plastic waste, the fluctuating prices of virgin plastics, and the significant capital investment required for advanced recycling infrastructure.

Which regions are leading in industrial plastic waste recycling?

Europe and North America are currently leading, driven by advanced infrastructure, robust regulatory frameworks, and strong corporate commitments to sustainability. Asia Pacific is also experiencing rapid growth due to increasing industrialization and evolving environmental policies.

What role does Artificial Intelligence (AI) play in improving plastic recycling?

AI significantly enhances sorting accuracy and speed through computer vision, optimizes operational efficiency, enables predictive maintenance for machinery, and provides valuable data analytics for better waste stream management and material quality control.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted