Industrial Panel PC Market

Industrial Panel PC Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700693 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

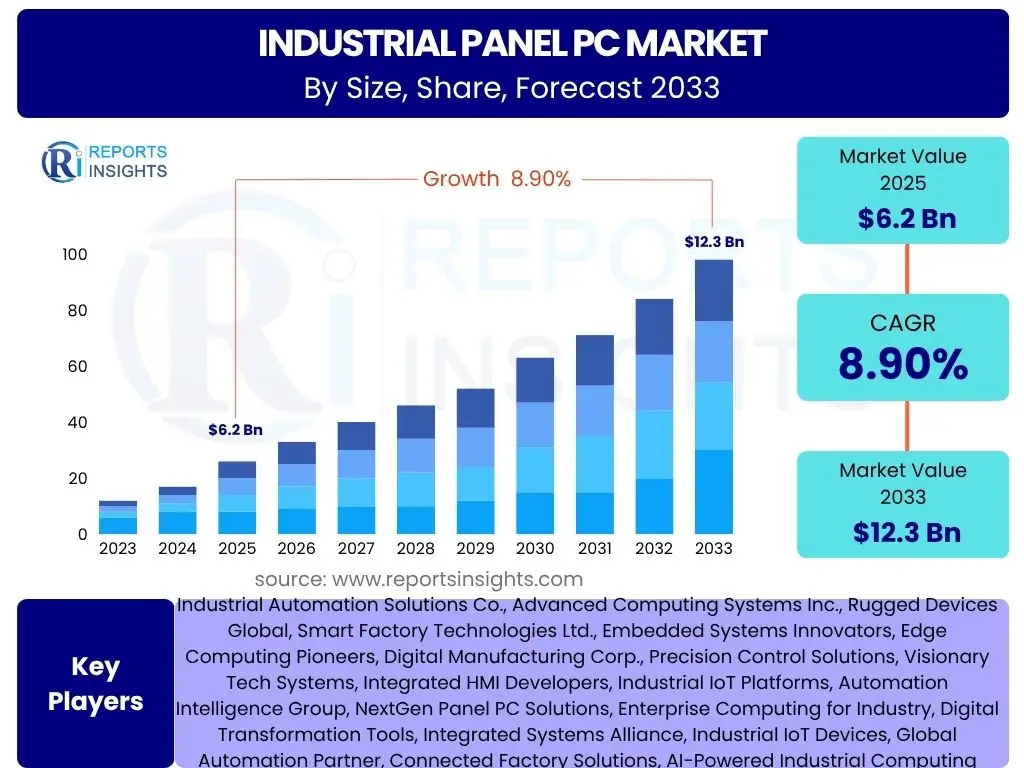

Industrial Panel PC Market Size

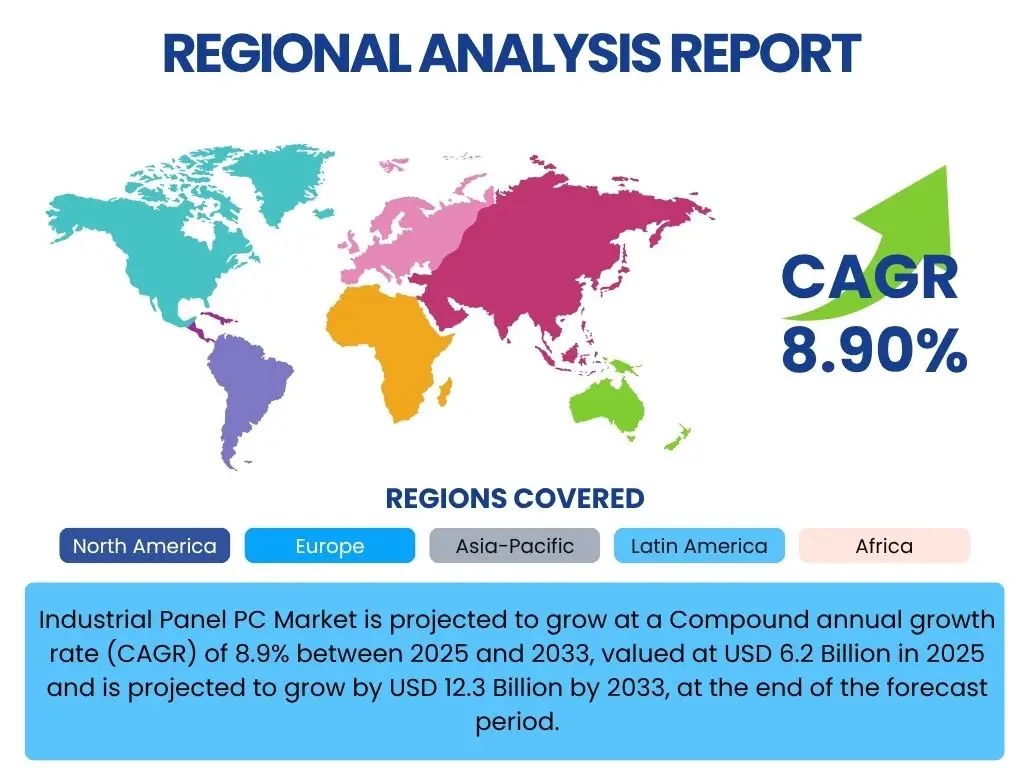

Industrial Panel PC Market is projected to grow at a Compound annual growth rate (CAGR) of 8.9% between 2025 and 2033, valued at USD 6.2 Billion in 2025 and is projected to grow by USD 12.3 Billion by 2033, at the end of the forecast period.

Key Industrial Panel PC Market Trends & Insights

The Industrial Panel PC market is currently experiencing dynamic shifts driven by several pivotal trends, reflecting the broader evolution of industrial automation and digital transformation initiatives globally. These trends are not only shaping current market demand but also dictating future innovations and strategic imperatives for market participants. The convergence of advanced hardware capabilities with sophisticated software integration is creating more robust, versatile, and intelligent industrial computing solutions.

- Increasing integration of Industrial Internet of Things (IIoT) and Industry 4.0 technologies.

- Growing demand for ruggedized and fanless designs for harsh industrial environments.

- Adoption of multi-touch and gesture control interfaces for enhanced user experience.

- Shift towards modular and customizable panel PC solutions.

- Expansion of edge computing capabilities for real-time data processing.

- Rising demand for high-resolution displays and advanced graphics processing.

- Emphasis on cybersecurity features in industrial computing systems.

- Development of energy-efficient and low-power consumption models.

AI Impact Analysis on Industrial Panel PC

The integration of Artificial Intelligence (AI) is fundamentally transforming the landscape of Industrial Panel PCs, transitioning them from mere data display and control units into intelligent, decision-making nodes within industrial ecosystems. AI capabilities, particularly at the edge, enable these devices to perform complex analytics, pattern recognition, and predictive tasks directly on the factory floor, significantly enhancing operational efficiency and fostering proactive maintenance strategies. This paradigm shift underscores a move towards more autonomous and responsive industrial operations.

- Enabling real-time AI inference and machine learning at the edge for immediate operational insights.

- Facilitating predictive maintenance through AI-driven anomaly detection and pattern recognition.

- Enhancing human-machine interface (HMI) with AI-powered natural language processing and voice commands.

- Optimizing quality control and inspection processes via AI-driven machine vision algorithms.

- Automating complex tasks and decision-making for improved efficiency and reduced human error.

- Supporting adaptive manufacturing processes through AI-powered robotic control and process optimization.

Key Takeaways Industrial Panel PC Market Size & Forecast

- The Industrial Panel PC market is poised for significant expansion, driven by accelerating digital transformation in manufacturing and industrial sectors.

- Rapid adoption of Industry 4.0 principles and IIoT technologies is a primary catalyst for market growth.

- Demand for rugged, high-performance computing solutions capable of operating in diverse and harsh environments remains a crucial market characteristic.

- Technological advancements, including multi-touch interfaces, enhanced connectivity, and edge AI integration, are broadening application scope and user experience.

- Asia Pacific is expected to emerge as a dominant region, propelled by robust industrialization and smart factory initiatives.

- The market's future trajectory is strongly influenced by ongoing innovations in processing power, display technology, and cybersecurity features.

Industrial Panel PC Market Drivers Analysis

The Industrial Panel PC market is propelled by a confluence of macroeconomic trends and technological advancements, each contributing significantly to its upward trajectory. The increasing digitalization of industrial operations, coupled with the imperative for enhanced efficiency and real-time data access, underpins much of this growth. Furthermore, the global drive towards smarter, more connected manufacturing environments necessitates robust and reliable computing solutions at every level of operation, from shop floor control to executive dashboards. These drivers collectively foster an environment conducive to sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Adoption of Industry 4.0 and IIoT Technologies: The global shift towards smart factories, automation, and interconnected industrial ecosystems fundamentally relies on advanced computing solutions. Industrial Panel PCs serve as critical Human-Machine Interfaces (HMIs) and data processing hubs, facilitating real-time monitoring, control, and data acquisition necessary for Industry 4.0 implementations. This pervasive digitalization across manufacturing, energy, and logistics sectors drives sustained demand. | +2.5% | Global, particularly high growth in Asia Pacific (China, India, Japan), Europe (Germany), and North America (USA) | Long-term (2025-2033) |

| Increasing Demand for Industrial Automation and Control Systems: Industries worldwide are investing heavily in automation to enhance productivity, reduce operational costs, and improve safety. Industrial Panel PCs are integral components of these automation systems, used in process control, robotic applications, and quality assurance. Their ruggedness and ability to withstand harsh environments make them ideal for factory floors and other demanding industrial settings. | +2.0% | North America, Europe, Asia Pacific, with significant expansion in emerging economies. | Mid to Long-term (2025-2033) |

| Growing Need for Data Visualization and Real-time Monitoring: In modern industrial settings, decision-making is increasingly data-driven. Industrial Panel PCs provide intuitive interfaces for visualizing complex operational data, performance metrics, and equipment status in real time. This capability is crucial for optimizing production processes, identifying bottlenecks, and ensuring operational continuity across various sectors. | +1.8% | Globally, especially in highly regulated industries like Pharmaceuticals, Food & Beverage, and Energy. | Mid-term (2025-2030) |

| Development of Edge Computing Capabilities: The proliferation of IIoT devices generates massive amounts of data at the network edge. Industrial Panel PCs are increasingly equipped with robust processing power to perform edge computing, allowing data to be processed closer to its source. This reduces latency, conserves bandwidth, and enables faster decision-making, which is vital for critical industrial applications. | +1.6% | Global, with particular emphasis in manufacturing, logistics, and smart city infrastructure. | Mid to Long-term (2025-2033) |

| Increased Focus on Workforce Efficiency and Safety: Intuitive and responsive Industrial Panel PCs enhance operator efficiency by providing seamless interaction with machinery and systems. Features like multi-touch screens and customizable interfaces reduce training time and minimize human error. Furthermore, by integrating safety protocols and alarm systems, these devices contribute to a safer working environment. | +1.0% | Across all industrial sectors, with strong emphasis in developed economies and regions with stringent safety regulations. | Short to Mid-term (2025-2028) |

Industrial Panel PC Market Restraints Analysis

Despite the robust growth drivers, the Industrial Panel PC market faces certain impediments that could moderate its expansion. These restraints often stem from the inherent complexities of industrial environments, the specialized nature of these devices, and the broader economic landscape. Addressing these challenges through innovation and strategic planning is crucial for market participants to sustain growth momentum and maintain competitive advantage in the evolving industrial automation sector. Understanding these limitations is as critical as recognizing the growth opportunities for accurate market forecasting.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs: Industrial Panel PCs, especially high-performance or highly customized models, typically involve a significant upfront investment compared to commercial-grade PCs. This can be a barrier for small and medium-sized enterprises (SMEs) with limited capital budgets, despite the long-term benefits of enhanced durability and reliability. | -1.2% | Globally, particularly impacting SMEs in developing and developed regions. | Mid-term (2025-2029) |

| Technological Obsolescence and Rapid Innovation Cycle: The rapid pace of technological advancements, particularly in processing power, connectivity standards, and AI integration, can lead to quick obsolescence of existing Industrial Panel PCs. While this drives upgrades, it also imposes continuous investment burdens on end-users who must regularly update their systems to maintain competitive edge and leverage the latest functionalities. | -0.9% | Developed economies and technology-intensive industries. | Long-term (2025-2033) |

| Cybersecurity Concerns and Vulnerabilities: As Industrial Panel PCs become more interconnected within IIoT networks, they become potential targets for cyberattacks. The risk of data breaches, operational disruptions, and intellectual property theft is a significant concern for industrial enterprises. Ensuring robust cybersecurity measures, though critical, adds complexity and cost, potentially slowing adoption for risk-averse organizations. | -0.7% | Global, especially in critical infrastructure and highly automated industries. | Long-term (2025-2033) |

| Integration Complexities with Legacy Systems: Many industrial facilities still operate with legacy machinery and control systems that may not be easily compatible with newer Industrial Panel PC technologies. The challenges associated with integrating modern devices into outdated infrastructures, including software compatibility and hardware interface issues, can deter or delay upgrades for some enterprises. | -0.5% | Mature industrial economies with established infrastructure, such as parts of Europe and North America. | Mid-term (2025-2030) |

Industrial Panel PC Market Opportunities Analysis

The Industrial Panel PC market is characterized by numerous burgeoning opportunities that promise to accelerate its growth trajectory. These opportunities stem from evolving technological landscapes, expanding application areas, and increasing strategic investments across various industrial sectors. The drive towards greater efficiency, connectivity, and intelligence in manufacturing and operational processes opens new avenues for innovation and market penetration. Capitalizing on these opportunities requires a deep understanding of emerging needs and a proactive approach to developing tailored solutions that address the specific demands of diverse end-use industries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Vertical Markets: Beyond traditional manufacturing, new sectors are increasingly adopting Industrial Panel PCs. These include healthcare (e.g., medical device control, patient monitoring), logistics and warehousing (e.g., inventory management, fleet tracking), smart city infrastructure (e.g., public transport kiosks, utility management), and agriculture (e.g., precision farming equipment control). Each new vertical offers substantial untapped potential for specialized solutions. | +2.0% | Global, with strong potential in emerging markets for infrastructure development. | Long-term (2025-2033) |

| Rising Demand for Customizable and Modular Solutions: Industries increasingly seek flexible computing solutions that can be tailored to specific operational requirements. The modular design of Industrial Panel PCs, allowing for easy upgrades of components like processors, memory, and I/O ports, presents a significant opportunity. This customization reduces total cost of ownership and extends product lifecycle, appealing to a broader range of industrial clients. | +1.5% | North America, Europe, and Asia Pacific where diverse manufacturing sectors thrive. | Mid-term (2025-2030) |

| Integration with Advanced Technologies (AI, ML, AR/VR): The convergence of Industrial Panel PCs with cutting-edge technologies like Artificial Intelligence (AI) for predictive analytics, Machine Learning (ML) for process optimization, and Augmented Reality/Virtual Reality (AR/VR) for maintenance and training, creates powerful new application possibilities. This integration enhances functionality and opens pathways for highly sophisticated industrial applications. | +1.3% | Developed economies with strong R&D capabilities and high technological adoption rates. | Long-term (2025-2033) |

| Focus on Energy Efficiency and Sustainability: As industries globally prioritize sustainability, there is a growing demand for energy-efficient Industrial Panel PCs. Devices that consume less power, generate less heat, and are made from recyclable materials offer a competitive advantage. This trend aligns with corporate social responsibility initiatives and can lead to operational cost savings for end-users, creating a strong market pull. | +0.8% | Europe and North America, driven by stringent environmental regulations and corporate sustainability goals. | Short to Mid-term (2025-2028) |

Industrial Panel PC Market Challenges Impact Analysis

While the Industrial Panel PC market is characterized by robust growth and significant opportunities, it is also navigating several inherent challenges that demand strategic attention from market participants. These challenges range from technological complexities and supply chain vulnerabilities to the evolving regulatory landscape and the need for specialized skill sets. Successfully addressing these impediments is crucial for ensuring sustained market expansion and maintaining competitive advantage. Innovators and solution providers must develop proactive strategies to mitigate these risks and turn potential roadblocks into pathways for growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Component Shortages: The global electronics industry has periodically faced challenges like semiconductor shortages and logistics disruptions, which directly impact the manufacturing and availability of Industrial Panel PCs. These disruptions can lead to increased production costs, extended lead times, and inability to meet market demand, thereby hindering growth and customer satisfaction. | -1.5% | Global, affecting all regions dependent on electronics manufacturing hubs. | Short to Mid-term (2025-2027) |

| Evolving Connectivity Standards and Interoperability Issues: The rapid evolution of industrial communication protocols (e.g., 5G, TSN, Wi-Fi 6) and the diverse range of legacy systems create interoperability challenges. Ensuring seamless communication between Industrial Panel PCs and a variety of industrial equipment, sensors, and cloud platforms requires significant effort in design and integration, which can increase complexity and development costs. | -1.0% | Global, particularly in industries undergoing significant digital transformation. | Mid-term (2025-2030) |

| Addressing Thermal Management in Fanless Designs: As Industrial Panel PCs become more powerful, especially with high-performance processors and integrated AI accelerators, managing heat dissipation in compact, fanless enclosures becomes increasingly challenging. Inadequate thermal management can lead to performance throttling or premature component failure, which is unacceptable in mission-critical industrial applications. | -0.8% | Global, especially in environments with extreme temperatures or where dust and noise are concerns. | Long-term (2025-2033) |

| Lack of Skilled Workforce for Implementation and Maintenance: The sophisticated nature of modern Industrial Panel PCs and their integration into complex industrial ecosystems requires a highly skilled workforce for installation, configuration, troubleshooting, and maintenance. A shortage of professionals with expertise in industrial IT, automation, and cybersecurity can hinder deployment and optimization of these advanced systems. | -0.7% | Globally, particularly in regions with less developed technical education infrastructure. | Long-term (2025-2033) |

Industrial Panel PC Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Industrial Panel PC market, offering critical insights into its current landscape and future growth trajectories. It meticulously details market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report is designed to equip business professionals and decision-makers with actionable intelligence, facilitating informed strategic planning and investment decisions within the dynamic industrial computing sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 12.3 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Industrial Automation Solutions Co., Advanced Computing Systems Inc., Rugged Devices Global, Smart Factory Technologies Ltd., Embedded Systems Innovators, Edge Computing Pioneers, Digital Manufacturing Corp., Precision Control Solutions, Visionary Tech Systems, Integrated HMI Developers, Industrial IoT Platforms, Automation Intelligence Group, NextGen Panel PC Solutions, Enterprise Computing for Industry, Digital Transformation Tools, Integrated Systems Alliance, Industrial IoT Devices, Global Automation Partner, Connected Factory Solutions, AI-Powered Industrial Computing |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Panel PC market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. This detailed segmentation enables stakeholders to identify specific growth avenues, assess competitive landscapes within niches, and tailor strategies to address distinct market requirements. By dissecting the market across various parameters, this report offers unparalleled insights into product preferences, application trends, and end-user demands, facilitating targeted market penetration and product development initiatives.

- By Type: This segment categorizes Industrial Panel PCs based on their design and functionality, addressing varied environmental and operational needs.

- Fanless Panel PCs: Designed for harsh environments where dust, debris, and noise are concerns, offering silent operation and increased reliability due to fewer moving parts.

- Capacitive Touch Panel PCs: Featuring highly responsive, multi-touch interfaces similar to consumer devices, ideal for intuitive interaction in clean environments.

- Resistive Touch Panel PCs: Known for their durability and ability to be operated with gloves or a stylus, suitable for rugged industrial settings.

- Multi-touch Panel PCs: Enabling gestures and multi-finger inputs, enhancing user experience and efficiency in complex applications.

- High-Performance Panel PCs: Equipped with powerful processors and ample memory for demanding applications like machine vision, AI inference, and complex data processing.

- Slim Panel PCs: Compact and space-saving designs suitable for installations where physical space is at a premium, without compromising on functionality.

- By Screen Size: This segmentation reflects the diverse visual and interactive requirements across industrial applications, from compact control panels to large-scale data visualization displays.

- Less than 10 Inches: Typically used for compact control boxes, embedded systems, or specialized machinery where space is limited.

- 10 to 15 Inches: A versatile and popular size for general HMI applications, offering a balance between compactness and readability.

- 15 to 21 Inches: Commonly employed in larger control rooms, detailed process monitoring, or interactive kiosks requiring extensive data visualization.

- More than 21 Inches: Utilized for large-scale data dashboards, collaborative displays, or applications requiring comprehensive visual overviews.

- By Operating System: This segment analyzes the market based on the software platforms that power Industrial Panel PCs, influencing compatibility, security, and developer ecosystems.

- Windows-based: Dominant in industrial settings due to broad software compatibility and familiarity, offering robust performance and extensive driver support.

- Linux-based: Preferred for its open-source flexibility, security, and real-time capabilities, often chosen for embedded systems and specialized applications.

- Android-based: Gaining traction for its user-friendly interface, cost-effectiveness, and connectivity options, particularly in logistics and commercial HMI applications.

- Proprietary OS: Custom operating systems developed for specific industrial applications, offering optimized performance and enhanced security for niche requirements.

- By Application: This segmentation highlights the primary uses of Industrial Panel PCs across various operational functions within industrial environments.

- Human-Machine Interface (HMI): The primary application, enabling operators to monitor and control industrial processes, machinery, and systems.

- Process Control & Automation: Integral for managing and automating complex manufacturing processes, ensuring precision and efficiency.

- Data Acquisition & Monitoring: Collecting and displaying real-time data from sensors and machinery for performance analysis and decision-making.

- Machine Vision & Inspection: Powering vision systems for automated quality control, defect detection, and precise component placement.

- Logistics & Warehousing: Used in inventory management, material handling, automated guided vehicles (AGVs), and supply chain optimization.

- Digital Signage & Kiosks: Deployments in industrial facilities for informational displays, interactive training, and employee self-service.

- By End-Use Industry: This segment identifies the major industrial sectors driving the adoption of Industrial Panel PCs, reflecting their diverse needs and operational complexities.

- Manufacturing:

- Discrete Manufacturing: Automotive, electronics, machinery, aerospace, where individual products are assembled.

- Process Manufacturing: Chemicals, pharmaceuticals, food & beverage, oil & gas, where materials are processed in continuous or batch operations.

- Automotive: For vehicle assembly lines, robotic control, quality inspection, and testing systems.

- Oil & Gas: Used in exploration, drilling, refining, and pipeline monitoring in hazardous environments.

- Energy & Utilities: For power generation, distribution, renewable energy management, and smart grid applications.

- Pharmaceuticals & Healthcare: In cleanroom environments for process control, laboratory automation, and medical device integration.

- Food & Beverage: For process control, packaging, quality assurance, and temperature monitoring in hygiene-sensitive areas.

- Chemicals: For monitoring and controlling complex chemical reactions and processes.

- Mining: In heavy machinery control, remote operations, and environmental monitoring in harsh conditions.

- Marine & Offshore: For navigation systems, engine room monitoring, and cargo management on vessels and offshore platforms.

- Transportation: In railway control systems, traffic management, and onboard computing for commercial vehicles.

- Manufacturing:

Regional Highlights

The global Industrial Panel PC market exhibits distinct regional growth patterns, influenced by factors such as industrialization levels, technological adoption rates, government initiatives, and the presence of key manufacturing hubs. Understanding these regional dynamics is crucial for market players to formulate effective expansion strategies and allocate resources efficiently. Each region presents a unique set of drivers and challenges that shape its contribution to the overall market.- Asia Pacific (APAC): This region is poised to be the fastest-growing and largest market for Industrial Panel PCs, driven by aggressive industrialization, expansion of manufacturing bases, and significant investments in smart factory initiatives, particularly in countries like China, India, Japan, and South Korea. The increasing adoption of automation across diverse industries, coupled with government support for digital transformation programs and favorable policies, fuels the demand for robust and cost-effective industrial computing solutions. The growth of the automotive, electronics, and food & beverage sectors further contributes to APAC's market dominance, making it a critical hub for both demand and supply of Industrial Panel PCs.

- North America: The market in North America is characterized by high technological maturity, a strong emphasis on advanced manufacturing, and early adoption of Industry 4.0 and IIoT technologies. The United States, in particular, leads in integrating sophisticated automation systems and AI into industrial processes. Demand is driven by the need for enhanced operational efficiency, data security, and compliance with stringent industrial standards. The presence of major manufacturing and aerospace industries, coupled with a focus on reshoring manufacturing and upgrading existing infrastructure, ensures consistent demand for high-performance and reliable industrial panel PCs.

- Europe: Europe represents a mature yet continually innovating market for Industrial Panel PCs, with countries like Germany, France, and the UK at the forefront of industrial automation and smart factory deployment. The region's emphasis on precision engineering, sustainable manufacturing practices, and adherence to strict regulatory frameworks drives the adoption of highly reliable, energy-efficient, and secure panel PCs. The automotive, machinery, and chemical industries are significant end-users. The continuous push for digitalization and the adoption of advanced robotics contribute substantially to the market's stability and steady growth in Europe.

- Latin America: The Industrial Panel PC market in Latin America is in a nascent but growing phase, primarily driven by increasing foreign direct investment in manufacturing and the modernization of industrial infrastructure. Countries such as Brazil and Mexico are experiencing growth due to expanding automotive production, food & beverage processing, and mining sectors. The region's focus on improving industrial efficiency and competitiveness is leading to a gradual but steady adoption of automation technologies, including Industrial Panel PCs, though market penetration remains lower compared to more developed regions.

- Middle East and Africa (MEA): This region is experiencing significant investment in industrial diversification, infrastructure development, and smart city projects, especially in the GCC countries. The oil & gas sector remains a major consumer of Industrial Panel PCs for operational control and monitoring in harsh environments. As these economies seek to reduce reliance on hydrocarbons and develop non-oil sectors like manufacturing, logistics, and tourism, the demand for industrial automation and associated computing solutions is projected to rise steadily, albeit from a smaller base.

Top Key Players:

The market research report covers the analysis of key stake holders of the Industrial Panel PC Market. Some of the leading players profiled in the report include -- Industrial Automation Solutions Co.

- Advanced Computing Systems Inc.

- Rugged Devices Global

- Smart Factory Technologies Ltd.

- Embedded Systems Innovators

- Edge Computing Pioneers

- Digital Manufacturing Corp.

- Precision Control Solutions

- Visionary Tech Systems

- Integrated HMI Developers

- Industrial IoT Platforms

- Automation Intelligence Group

- NextGen Panel PC Solutions

- Enterprise Computing for Industry

- Digital Transformation Tools

- Integrated Systems Alliance

- Industrial IoT Devices

- Global Automation Partner

- Connected Factory Solutions

- AI-Powered Industrial Computing

Frequently Asked Questions:

What is an Industrial Panel PC?

An Industrial Panel PC is an all-in-one computing solution specifically designed for industrial environments. It integrates a computer, display, and touchscreen into a single, ruggedized unit. These devices are built to withstand harsh conditions, including extreme temperatures, dust, moisture, vibrations, and electromagnetic interference, making them ideal for factory floors, control rooms, and other demanding industrial applications. They serve as essential Human-Machine Interfaces (HMIs) for monitoring, controlling, and visualizing industrial processes.What are the primary applications of Industrial Panel PCs?

Industrial Panel PCs are widely used across various applications in manufacturing and industrial sectors. Their primary uses include Human-Machine Interface (HMI) for real-time process control, data acquisition and monitoring, machine vision systems for quality inspection, and automation control in smart factories. They are also integral to logistics and warehousing for inventory management and tracking, and in specialized applications within the automotive, oil & gas, pharmaceutical, and energy industries.How does Industry 4.0 impact the Industrial Panel PC market?

Industry 4.0 significantly impacts the Industrial Panel PC market by driving the demand for advanced, interconnected, and intelligent computing solutions. As industries move towards smart factories, automation, and the Industrial Internet of Things (IIoT), Industrial Panel PCs serve as critical components for enabling real-time data exchange, edge computing, and seamless integration between operational technology (OT) and information technology (IT) systems. This paradigm shift necessitates more powerful, rugged, and network-enabled panel PCs capable of supporting complex automation and data analytics tasks.What are the key technological trends shaping the Industrial Panel PC market?

Key technological trends shaping the Industrial Panel PC market include the increasing adoption of multi-touch and gesture control interfaces for enhanced user experience, the expansion of edge computing capabilities for local data processing and reduced latency, and the integration of Artificial Intelligence (AI) for predictive analytics and smarter automation. Furthermore, there's a growing emphasis on enhanced cybersecurity features, modular designs for greater customization, and the development of fanless and highly ruggedized solutions for extreme operating conditions.Which regions are showing the most significant growth in the Industrial Panel PC market?

The Asia Pacific (APAC) region is currently demonstrating the most significant growth in the Industrial Panel PC market. This growth is primarily fueled by rapid industrialization, massive investments in manufacturing automation, and the widespread adoption of smart factory initiatives in countries like China, India, Japan, and South Korea. North America and Europe also maintain strong market positions due to advanced manufacturing industries and ongoing digital transformation efforts, but APAC's industrial expansion positions it for accelerated market expansion.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted