Industrial Electronic Market

Industrial Electronic Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706670 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Industrial Electronic Market Size

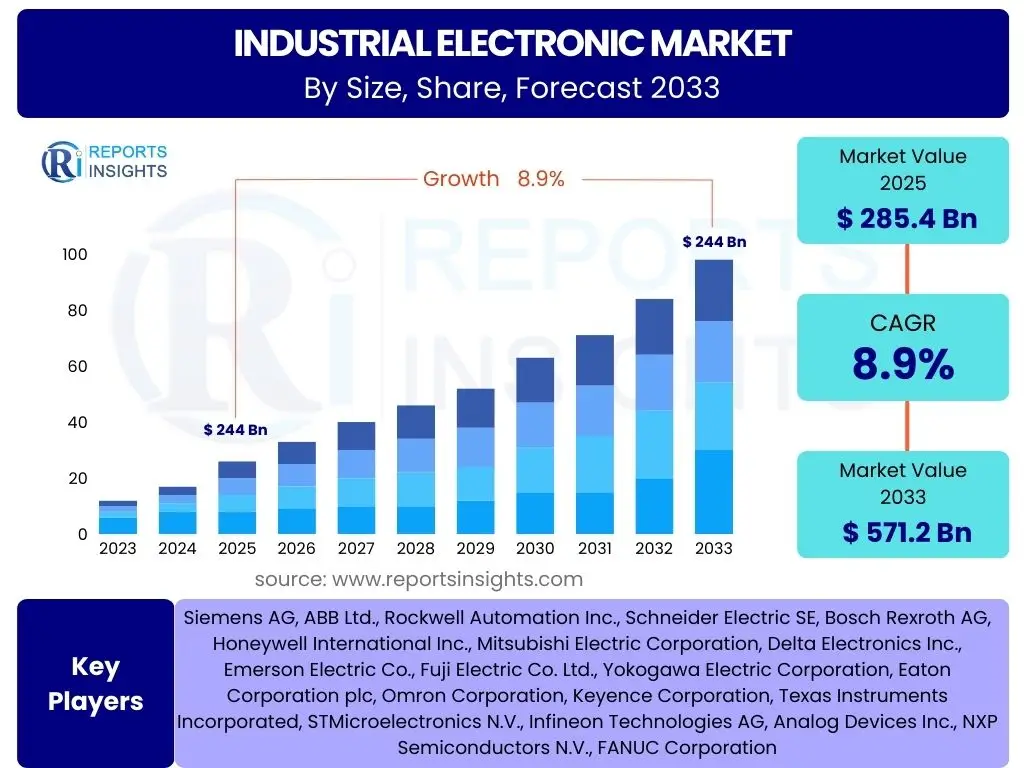

According to Reports Insights Consulting Pvt Ltd, The Industrial Electronic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 285.4 billion in 2025 and is projected to reach USD 571.2 billion by the end of the forecast period in 2033.

Key Industrial Electronic Market Trends & Insights

The industrial electronic market is currently experiencing a transformative phase, driven by rapid technological advancements and increasing demand for automation across various sectors. Key trends indicate a significant shift towards smart manufacturing, where interconnected devices and data analytics play a crucial role in optimizing production processes. This evolution is fueled by the widespread adoption of the Internet of Things (IoT) and artificial intelligence (AI), leading to more intelligent, efficient, and predictive industrial operations. Companies are heavily investing in solutions that enhance operational visibility, reduce downtime, and improve overall productivity, reflecting a broader industry push towards Industry 4.0 paradigms.

Furthermore, sustainability and energy efficiency are emerging as paramount considerations within the industrial electronics landscape. There is a growing demand for electronic components and systems that consume less power, generate less waste, and integrate renewable energy sources. This trend is not only driven by regulatory pressures and environmental concerns but also by the potential for significant cost savings over the long term. Miniaturization and modularity are also gaining traction, enabling more flexible and adaptable industrial setups that can be easily reconfigured or upgraded, catering to the dynamic needs of modern manufacturing and processing industries.

- Proliferation of Industry 4.0 and Smart Manufacturing Initiatives

- Increasing Adoption of Industrial IoT (IIoT) for Enhanced Connectivity and Data Collection

- Growing Integration of Artificial Intelligence (AI) and Machine Learning (ML) for Predictive Analytics and Automation

- Emphasis on Energy Efficiency and Sustainable Electronic Solutions

- Advancements in Power Electronics and Semiconductor Technologies

- Miniaturization and Modularity of Industrial Electronic Components

- Rise of Edge Computing for Real-Time Data Processing in Industrial Environments

- Demand for Enhanced Cybersecurity Measures in Connected Industrial Systems

- Development of Human-Machine Interface (HMI) and Augmented Reality (AR) for Operational Support

- Expansion of Collaborative Robotics and Automated Guided Vehicles (AGVs)

AI Impact Analysis on Industrial Electronic

Artificial intelligence is profoundly reshaping the industrial electronic landscape, transitioning it from traditional, reactive systems to highly intelligent, proactive, and adaptive environments. User queries frequently revolve around how AI enhances operational efficiency, enables predictive capabilities, and drives automation. AI algorithms, when integrated with industrial electronic systems, facilitate advanced data analysis from sensors and connected devices. This enables capabilities such as real-time fault detection, anomaly identification, and predictive maintenance, significantly reducing unplanned downtime and optimizing asset utilization. The implementation of AI is also critical in optimizing complex manufacturing processes, improving quality control, and streamlining supply chain logistics, which directly impacts productivity and cost efficiency.

Moreover, the impact of AI extends to transforming human-machine interaction and enabling more sophisticated automation. AI-powered robots and automated systems, which rely heavily on advanced industrial electronics, are becoming more autonomous and capable of performing intricate tasks with greater precision. This shift addresses concerns about labor shortages and enhances workplace safety by taking over hazardous or repetitive tasks. The long-term expectation is that AI will continue to drive innovation in industrial electronics, fostering the development of self-optimizing factories and fully autonomous production lines, ultimately leading to a more resilient and responsive industrial ecosystem. However, concerns regarding data privacy, system integration complexities, and the need for a skilled workforce capable of managing these advanced AI systems also frequently arise.

- Enabling Predictive Maintenance and Anomaly Detection in Industrial Machinery

- Optimizing Manufacturing Processes and Production Efficiency through AI Algorithms

- Enhancing Quality Control and Defect Detection with Computer Vision and Machine Learning

- Facilitating Autonomous Operations in Robotics and Automated Guided Vehicles (AGVs)

- Improving Supply Chain Management and Logistics through AI-driven Forecasting

- Driving Real-time Data Analytics and Decision-Making at the Edge

- Personalizing Human-Machine Interface (HMI) for Enhanced Operator Experience

- Reducing Energy Consumption and Optimizing Resource Allocation

- Accelerating Research and Development of New Industrial Electronic Components

- Strengthening Cybersecurity Posture through AI-powered Threat Detection

Key Takeaways Industrial Electronic Market Size & Forecast

The industrial electronic market is poised for substantial growth, driven by an accelerating global push towards digitalization and automation across diverse industrial sectors. Key inquiries often focus on the market's significant expansion trajectory, the underlying factors contributing to this growth, and the projected future valuation. The forecast indicates robust expansion, with the market value expected to nearly double by 2033. This growth is primarily fueled by continuous advancements in smart manufacturing technologies, the widespread adoption of IoT devices, and the increasing integration of artificial intelligence into industrial processes. The inherent demand for improved operational efficiency, reduced production costs, and enhanced safety standards is a consistent driver for this market's upward trend.

Furthermore, the market's resilience is underpinned by its critical role in facilitating the Industry 4.0 revolution, which is seeing sustained investment from both developed and emerging economies. The market insights also highlight the pivotal role of specific component categories, such as sensors, controllers, and power electronics, which form the backbone of modern industrial automation systems. The competitive landscape is characterized by innovation and strategic collaborations, aiming to address the evolving demands for high-performance, energy-efficient, and secure industrial electronic solutions. The projected growth underscores the industrial electronic sector as a vital enabler of global industrial transformation, making it a critical area for investment and technological development.

- Significant market expansion projected to reach USD 571.2 billion by 2033.

- CAGR of 8.9% reflects strong growth potential driven by digital transformation.

- Core drivers include Industry 4.0 adoption, automation demand, and AI integration.

- Key component areas like sensors, controllers, and power supplies are central to growth.

- Market evolution emphasizes efficiency, safety, and sustainable solutions.

- Investments in smart manufacturing and IIoT are primary growth catalysts.

- Emerging markets are significant contributors to overall market expansion.

Industrial Electronic Market Drivers Analysis

The industrial electronic market is experiencing significant growth propelled by several robust drivers. A primary catalyst is the accelerating adoption of Industry 4.0 principles, which emphasize automation, data exchange, and manufacturing technologies. This paradigm shift necessitates advanced industrial electronic components and systems to enable smart factories, interconnected production lines, and real-time data analysis. Additionally, the increasing global demand for automation in manufacturing across various sectors, including automotive, electronics, and pharmaceuticals, directly fuels the need for sophisticated control systems, sensors, and robotics, all of which rely heavily on specialized industrial electronics. Governments and industries worldwide are investing heavily in these transformative technologies to enhance productivity, reduce operational costs, and maintain competitive advantages.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerating Adoption of Industry 4.0 and Smart Manufacturing | +2.1% | Global, particularly APAC (China, Japan), Europe (Germany), North America (US) | Short to Long Term (2025-2033) |

| Growing Demand for Industrial Automation and Robotics | +1.8% | Global, especially in high-labor-cost regions and emerging economies | Short to Long Term (2025-2033) |

| Expansion of Industrial IoT (IIoT) Ecosystem | +1.5% | North America, Europe, China | Medium to Long Term (2026-2033) |

| Focus on Energy Efficiency and Sustainable Manufacturing Practices | +1.2% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

Industrial Electronic Market Restraints Analysis

Despite robust growth, the industrial electronic market faces several notable restraints that could temper its expansion. One significant challenge is the high initial capital investment required for implementing advanced industrial electronic systems and automation technologies. Many small and medium-sized enterprises (SMEs) find it difficult to justify these substantial upfront costs, particularly when faced with uncertain return on investment periods. This financial barrier can impede widespread adoption, especially in price-sensitive emerging markets. Additionally, the complexity associated with integrating diverse industrial electronic components and software from various vendors often leads to interoperability issues and prolonged deployment times, creating further hurdles for businesses seeking to modernize their operations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Implementation Costs | -1.5% | Global, particularly affecting SMEs and emerging economies | Short to Medium Term (2025-2029) |

| Concerns Regarding Cybersecurity Threats and Data Privacy | -1.0% | Global, especially in highly networked industries | Short to Long Term (2025-2033) |

| Lack of Skilled Workforce for Advanced Industrial Technologies | -0.8% | Global, pronounced in developed and rapidly developing regions | Medium to Long Term (2026-2033) |

Industrial Electronic Market Opportunities Analysis

The industrial electronic market presents substantial growth opportunities driven by evolving technological landscapes and increasing industrial demands. A significant opportunity lies in the burgeoning adoption of AI and machine learning for predictive maintenance and operational optimization. These technologies, integrated with advanced sensors and control systems, enable industries to minimize downtime, improve asset utilization, and enhance overall efficiency, creating new revenue streams for solution providers. The expansion into niche applications, such as smart agriculture, advanced healthcare automation, and intelligent transportation systems, also represents fertile ground for market expansion beyond traditional manufacturing sectors.

Furthermore, the growing emphasis on sustainable manufacturing practices and energy conservation opens avenues for innovation in power electronics and energy management systems. Industries are increasingly seeking electronic solutions that not only enhance productivity but also reduce their environmental footprint and operational energy costs. This demand drives the development of more efficient converters, inverters, and power supply units. The strategic focus on modular and customizable industrial electronic solutions also allows for greater flexibility and scalability, catering to the diverse and evolving needs of various end-use industries, thus fostering long-term market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Applications (e.g., Smart Agriculture, Healthcare) | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term (2027-2033) |

| Development of Advanced Power Electronics for Energy Management | +1.4% | Global, particularly Europe and North America | Short to Long Term (2025-2033) |

| Integration with AI and Machine Learning for Predictive Analytics | +1.3% | North America, Europe, Asia Pacific | Short to Long Term (2025-2033) |

Industrial Electronic Market Challenges Impact Analysis

The industrial electronic market faces several significant challenges that could impede its growth trajectory. One major hurdle is the rapid pace of technological obsolescence, where components and systems quickly become outdated due to continuous innovation. This necessitates frequent upgrades and investments, posing a financial burden on businesses and increasing the risk of stranded assets. Additionally, ensuring interoperability between disparate systems and technologies from various manufacturers remains a complex challenge. The lack of universal standards for communication protocols and data formats can lead to integration difficulties, higher development costs, and reduced flexibility for end-users, hindering the seamless implementation of comprehensive industrial automation solutions.

Moreover, the escalating geopolitical tensions and supply chain disruptions, as witnessed in recent years, pose substantial risks to the industrial electronic market. The globalized nature of electronics manufacturing means that any disruptions in raw material supply, component production, or logistics can lead to increased costs, delays, and shortages, directly impacting the availability and pricing of industrial electronic products. Navigating complex regulatory landscapes and compliance requirements, particularly concerning environmental standards and data security, also adds layers of complexity for manufacturers and end-users alike. These factors collectively demand robust risk mitigation strategies and foster a need for greater supply chain resilience within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Continuous Upgrades | -1.2% | Global | Short to Long Term (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Instability | -1.0% | Global, particularly impacting Asia Pacific manufacturing hubs | Short to Medium Term (2025-2029) |

| Complexities in System Integration and Interoperability | -0.9% | Global, especially for highly customized industrial setups | Medium Term (2026-2030) |

Industrial Electronic Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Industrial Electronic Market, detailing its current size, historical performance, and future growth projections. It offers granular insights into market dynamics, including key drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation by component, end-use industry, and application, alongside a thorough regional analysis. The report identifies emerging trends, the impact of artificial intelligence, and profiles leading market players to provide a holistic understanding of the competitive landscape and strategic opportunities for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 285.4 billion |

| Market Forecast in 2033 | USD 571.2 billion |

| Growth Rate | 8.9% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., Rockwell Automation Inc., Schneider Electric SE, Bosch Rexroth AG, Honeywell International Inc., Mitsubishi Electric Corporation, Delta Electronics Inc., Emerson Electric Co., Fuji Electric Co. Ltd., Yokogawa Electric Corporation, Eaton Corporation plc, Omron Corporation, Keyence Corporation, Texas Instruments Incorporated, STMicroelectronics N.V., Infineon Technologies AG, Analog Devices Inc., NXP Semiconductors N.V., FANUC Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial electronic market is meticulously segmented to provide a granular understanding of its diverse landscape and growth opportunities. This segmentation considers various aspects, including the type of components utilized, the specific end-use industries served, and the broad applications where these electronics are deployed. By analyzing these distinct segments, stakeholders can identify high-growth areas, understand industry-specific demands, and tailor their strategies to target particular market niches more effectively. This detailed breakdown enables a comprehensive assessment of market dynamics across different product categories and vertical markets.

Each segment exhibits unique growth drivers and adoption patterns. For instance, the component segment highlights the demand for advanced sensors and controllers crucial for automation, while the end-use industry segment showcases the varying levels of technology adoption across sectors like automotive, manufacturing, and energy. The application segment, conversely, reveals the pervasive impact of industrial electronics in areas such as industrial automation, process control, and robotics. This multi-dimensional segmentation is vital for strategic planning, product development, and market entry decisions, offering a clear roadmap for navigating the complexities of the industrial electronic ecosystem.

- By Component:

- Sensors (Proximity, Temperature, Pressure, Level, Flow, Position, Vision, etc.)

- Actuators (Motors, Valves, Relays, etc.)

- Controllers (PLCs, DCS, Industrial PCs, CNC Controllers)

- Power Supplies & Converters (AC/DC, DC/DC, Inverters, Rectifiers)

- Memory Devices

- Processors & Microcontrollers

- Interface Modules

- Other Components

- By End-Use Industry:

- Manufacturing (Automotive, Electronics, Food & Beverage, Pharmaceutical & Medical Devices, Heavy Machinery, Textiles, etc.)

- Energy & Power

- Oil & Gas

- Mining

- Chemicals

- Water & Wastewater Management

- Aerospace & Defense

- Healthcare

- Agriculture

- Other Industries

- By Application:

- Industrial Automation

- Process Control

- Motion Control

- Robotics

- Test & Measurement

- Energy Management

- Safety & Security Systems

- Communication Systems

- Condition Monitoring

- Other Applications

Regional Highlights

- North America: This region is a leading adopter of advanced industrial electronics, driven by strong investments in smart factories, digital transformation, and a robust automotive and aerospace manufacturing base. The presence of major technology providers and a high focus on automation and efficiency further contribute to its market dominance.

- Europe: Characterized by strong manufacturing economies, particularly in Germany and Italy, Europe is at the forefront of Industry 4.0 adoption. Government initiatives supporting smart manufacturing and a strong emphasis on energy efficiency and sustainable production methods fuel the demand for sophisticated industrial electronic solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to rapid industrialization, increasing automation in countries like China, India, Japan, and South Korea, and significant government support for high-tech manufacturing. The booming electronics and automotive sectors, coupled with a large manufacturing base, drive substantial demand.

- Latin America: This region is experiencing steady growth, propelled by the modernization of its industrial infrastructure, particularly in sectors such as automotive, mining, and food & beverage. Increasing foreign investments and efforts to enhance manufacturing competitiveness are key growth factors.

- Middle East and Africa (MEA): Growth in MEA is largely influenced by industrial diversification initiatives in oil-rich economies and investments in infrastructure development. Automation in the oil & gas, energy, and construction sectors is driving the adoption of industrial electronic solutions, though at a slower pace compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Electronic Market.- Siemens AG

- ABB Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Bosch Rexroth AG

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Delta Electronics Inc.

- Emerson Electric Co.

- Fuji Electric Co. Ltd.

- Yokogawa Electric Corporation

- Eaton Corporation plc

- Omron Corporation

- Keyence Corporation

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Infineon Technologies AG

- Analog Devices Inc.

- NXP Semiconductors N.V.

- FANUC Corporation

Frequently Asked Questions

What is the projected growth rate of the Industrial Electronic Market?

The Industrial Electronic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033.

What are the primary drivers of the Industrial Electronic Market?

Key drivers include the accelerating adoption of Industry 4.0, increasing demand for industrial automation and robotics, expansion of the Industrial IoT (IIoT) ecosystem, and a growing focus on energy efficiency and sustainable manufacturing practices.

How is Artificial Intelligence impacting industrial electronics?

AI is significantly impacting industrial electronics by enabling predictive maintenance, optimizing manufacturing processes, enhancing quality control through computer vision, facilitating autonomous operations in robotics, and improving real-time data analytics.

Which regions are leading in the adoption of industrial electronics?

North America and Europe are leading adopters, driven by mature industrial sectors and strong Industry 4.0 initiatives. Asia Pacific, particularly China and India, is projected to be the fastest-growing region due to rapid industrialization and manufacturing expansion.

What are the main challenges facing the Industrial Electronic Market?

Major challenges include rapid technological obsolescence, high initial investment costs for advanced systems, complexities in system integration and interoperability, and vulnerabilities in global supply chains.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted