Industrial Cybersecurity Market

Industrial Cybersecurity Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700049 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

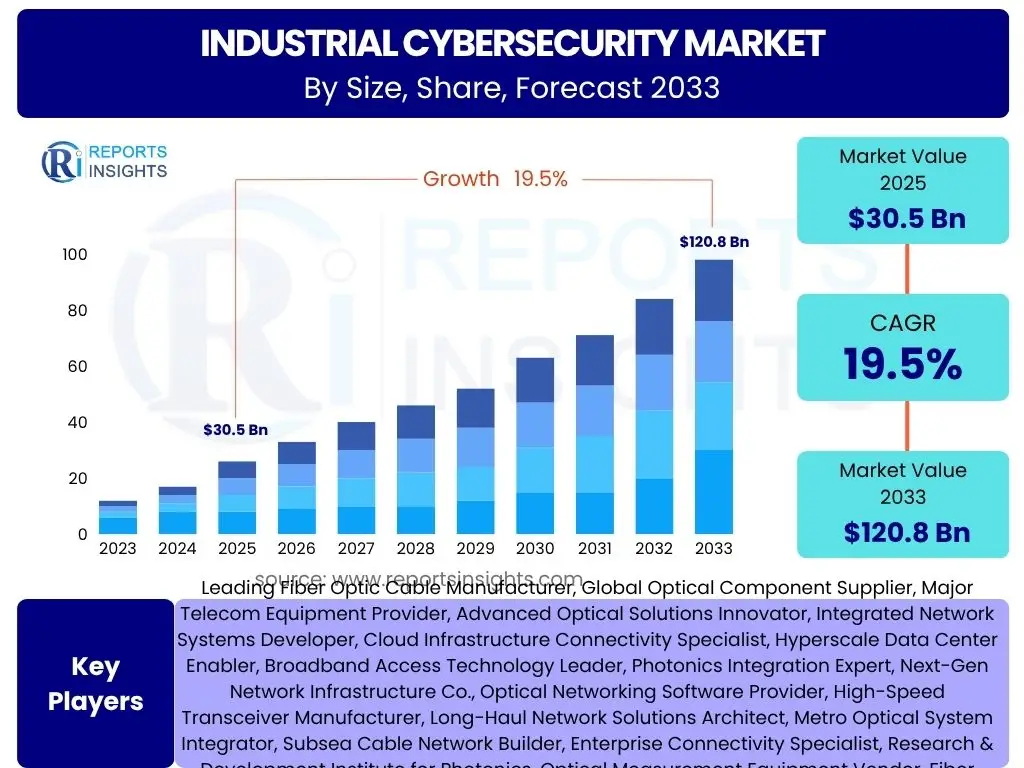

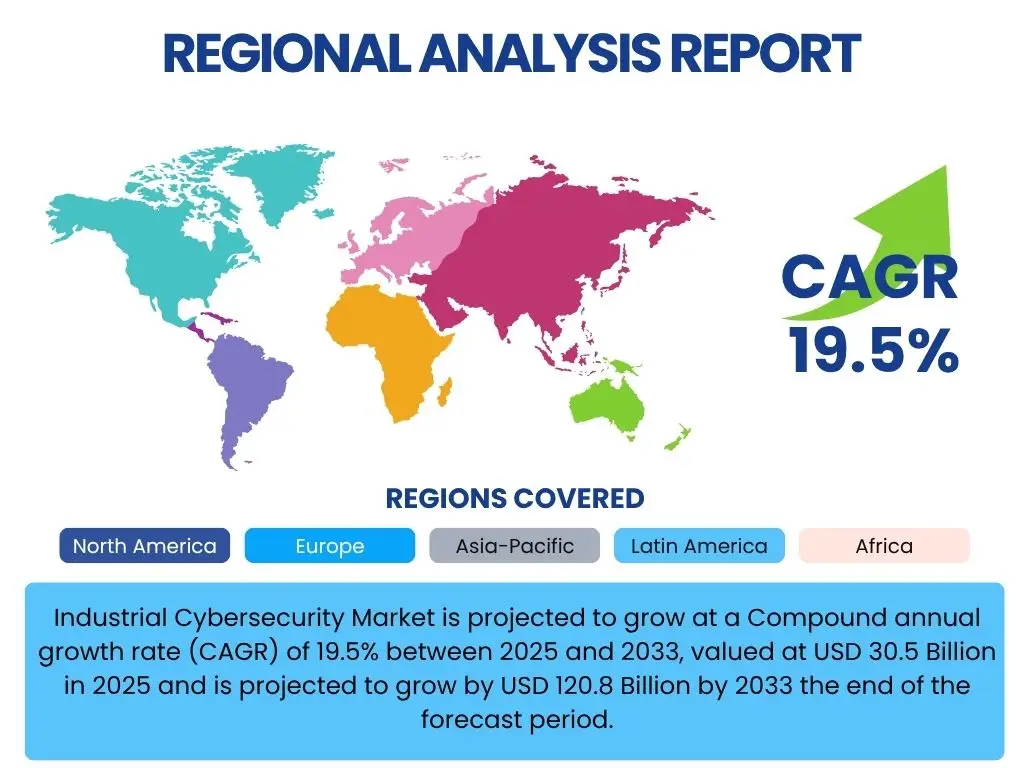

Industrial Cybersecurity Market is projected to grow at a Compound annual growth rate (CAGR) of 19.5% between 2025 and 2033, valued at USD 30.5 Billion in 2025 and is projected to grow by USD 120.8 Billion by 2033 the end of the forecast period.

Key Industrial Cybersecurity Market Trends & Insights

The industrial cybersecurity landscape is rapidly evolving, driven by the increasing digital transformation of operational technologies (OT) and industrial control systems (ICS). Organizations are realizing the critical importance of protecting these interconnected environments from sophisticated cyber threats, which can lead to significant operational disruptions, safety hazards, and financial losses. The convergence of IT and OT networks further complicates the security posture, necessitating integrated and robust cybersecurity solutions tailored to industrial environments. This proactive shift is fueled by a heightened awareness of supply chain vulnerabilities and the potential for nation-state-sponsored attacks targeting critical infrastructure. The emphasis is now on comprehensive defense mechanisms that not only detect but also actively prevent intrusions, ensuring the resilience and continuity of industrial operations.

- Increasing IT/OT convergence driving integrated security solutions.

- Rising sophistication of cyber threats targeting critical infrastructure.

- Growing adoption of IoT and Industry 4.0 technologies in industrial settings.

- Stricter regulatory compliance and industry standards for industrial control systems.

- Shift from reactive incident response to proactive threat intelligence and prevention.

- Demand for specialized industrial cybersecurity workforce and expertise.

AI Impact Analysis on Industrial Cybersecurity

Artificial intelligence (AI) is poised to fundamentally transform the industrial cybersecurity market by enhancing both defensive and offensive capabilities. AI-powered solutions offer unprecedented speed and accuracy in detecting anomalies, predicting potential threats, and automating responses within complex industrial environments. This includes leveraging machine learning algorithms to analyze vast datasets from OT networks, identifying patterns indicative of sophisticated cyberattacks that might elude traditional signature-based detection methods. From real-time threat intelligence to adaptive security postures, AI integration provides a scalable and efficient means to combat the escalating volume and complexity of cyber threats targeting industrial control systems. However, the dual-use nature of AI also means that adversaries can employ similar techniques to craft more evasive and potent attacks, demanding continuous innovation in defensive AI applications.

- AI-driven anomaly detection improving threat identification accuracy.

- Machine learning algorithms enhancing predictive threat intelligence.

- Automated incident response capabilities for faster mitigation.

- Enhanced vulnerability management through AI-powered risk assessment.

- Potential for AI to generate more sophisticated and adaptive cyberattacks.

- Need for explainable AI to ensure transparency and trust in autonomous security decisions.

Key Takeaways Industrial Cybersecurity Market Size & Forecast

- The Industrial Cybersecurity Market is set for robust expansion, driven by accelerating digital transformation in industrial sectors.

- Forecasts indicate a significant increase in market valuation, reflecting heightened investment in protecting operational technologies and critical infrastructure.

- Key growth drivers include escalating cyber threats, stringent regulatory mandates, and the widespread adoption of Industry 4.0 technologies.

- Geographic regions with high industrialization and advanced digital economies are expected to contribute substantially to market revenue.

- The market will witness continuous innovation in AI-powered security solutions and integrated IT/OT platforms.

Industrial Cybersecurity Market Drivers Analysis

The industrial cybersecurity market is experiencing significant tailwinds, primarily driven by the escalating sophistication of cyber threats targeting operational technology (OT) and industrial control systems (ICS). As industries embrace digital transformation and integrate IT and OT networks, the attack surface expands dramatically, making robust cybersecurity solutions imperative. Organizations are increasingly recognizing that disruptions to industrial operations due to cyberattacks can lead to severe financial losses, production halts, safety incidents, and reputational damage. This heightened awareness is translating into greater budget allocation for proactive security measures. Furthermore, a growing body of stringent regulatory compliance mandates, such as those related to critical infrastructure protection, compel industrial entities to adopt comprehensive cybersecurity frameworks, thereby propelling market growth. The ongoing expansion of the Industrial Internet of Things (IIoT) and Industry 4.0 initiatives also introduces new vulnerabilities, necessitating specialized cybersecurity solutions to protect interconnected devices and intelligent systems. This confluence of factors underscores a foundational shift in how industries perceive and prioritize their cybersecurity investments, moving beyond mere compliance to strategic risk management.

Technological advancements in areas like artificial intelligence, machine learning, and blockchain are also contributing to the development of more effective and adaptive industrial cybersecurity solutions. These innovations enable real-time threat detection, predictive analytics, and automated responses, making industrial environments more resilient against evolving threats. The increasing reliance on remote operations and cloud-based industrial applications further necessitates robust security protocols, driving demand for secure connectivity and data protection. Moreover, the global geopolitical landscape often sees critical infrastructure as targets for nation-state actors, which further intensifies the need for advanced industrial cybersecurity defenses. The market is thus poised for sustained growth as industries worldwide strive to secure their vital operational assets and maintain business continuity in an increasingly connected and threatened digital age.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Sophistication of Cyber Threats | +4.5% | Global, especially North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Rising IT/OT Convergence and Digital Transformation | +4.0% | Global, particularly developed economies | Medium to Long-term (2025-2033) |

| Stringent Regulatory Compliance and Standards | +3.5% | North America (NIST, NERC-CIP), Europe (NIS2, GDPR), Asia Pacific (national regulations) | Medium to Long-term (2025-2033) |

| Expansion of IIoT and Industry 4.0 Technologies | +3.0% | Global, especially manufacturing hubs | Long-term (2026-2033) |

| Growing Awareness of Supply Chain Vulnerabilities | +2.5% | Global, impacting various industrial sectors | Medium-term (2025-2030) |

Industrial Cybersecurity Market Restraints Analysis

Despite the strong growth drivers, the industrial cybersecurity market faces several notable restraints that could temper its expansion. One significant challenge is the high initial investment cost associated with deploying comprehensive industrial cybersecurity solutions. This often includes not only software and hardware but also extensive planning, integration with existing legacy systems, and workforce training, making it a substantial financial undertaking for many organizations, particularly small and medium-sized enterprises (SMEs). The complexity of integrating new security technologies with deeply embedded, often proprietary operational technology (OT) systems poses another formidable hurdle. Many industrial environments rely on outdated legacy systems that were not designed with modern cybersecurity in mind, making them difficult to patch, update, or integrate with advanced security tools without risking operational disruption.

Furthermore, a critical shortage of skilled cybersecurity professionals specializing in OT and ICS environments presents a significant bottleneck. The unique skill set required to understand both IT security principles and the nuances of industrial control systems is rare, leading to a talent gap that hinders effective implementation and management of industrial cybersecurity programs. Resistance to change within traditionally risk-averse industrial sectors also acts as a restraint, as some organizations may be hesitant to adopt new technologies or alter established operational practices due to perceived risks to uptime and production continuity. The lack of standardized security frameworks and inconsistent regulatory enforcement across different regions and industries can also create uncertainty and fragmentation, complicating the market landscape and slowing adoption rates. Overcoming these restraints will require a combination of innovative, cost-effective solutions, targeted skill development programs, and a greater emphasis on proactive risk management education within industrial leadership.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Implementation Costs | -2.0% | Global, especially SMEs in developing regions | Medium-term (2025-2030) |

| Complexity of Integrating with Legacy OT Systems | -1.5% | Global, particularly older industrial facilities | Long-term (2025-2033) |

| Shortage of Skilled OT Cybersecurity Professionals | -1.0% | Global, acute in all major industrial regions | Long-term (2025-2033) |

| Lack of Standardized Security Frameworks | -0.8% | Global, affecting cross-industry adoption | Medium-term (2025-2030) |

Industrial Cybersecurity Market Opportunities Analysis

The industrial cybersecurity market presents a plethora of lucrative opportunities for growth and innovation. The rapid expansion of smart factories, driven by Industry 4.0 initiatives, creates a vast greenfield for advanced security solutions. As manufacturing and other industrial sectors increasingly adopt automation, robotics, and the Industrial Internet of Things (IIoT), the need for embedded and integrated security from the ground up becomes paramount. This shift allows for the deployment of cutting-edge security architectures designed specifically for highly connected environments, offering opportunities for vendors to provide comprehensive platforms rather than fragmented point solutions. Furthermore, the growing trend of digital transformation extends to operational resilience and business continuity planning, positioning cybersecurity as an integral component of overall enterprise risk management strategies. This expanded scope of cybersecurity from a purely technical function to a strategic business imperative opens doors for advisory services, managed security services, and tailored solutions that address specific industry risks.

The convergence of IT and OT security operations represents a significant opportunity for vendors to offer unified security platforms that bridge the historical divide between these two domains. Solutions that provide visibility, control, and threat detection across both IT and OT networks are in high demand, enabling organizations to achieve a holistic security posture. The increasing focus on supply chain security, driven by recent high-profile incidents, also creates a demand for solutions that secure the entire industrial value chain, from component suppliers to end-product delivery. Moreover, the emergence of advanced technologies like AI, machine learning, and blockchain within cybersecurity offers avenues for developing highly predictive, automated, and resilient security systems. These technologies can enhance anomaly detection, improve threat intelligence, and secure data integrity in ways previously unimaginable. The untapped potential in emerging economies, coupled with their rapid industrialization, also offers significant market expansion opportunities for innovative and scalable industrial cybersecurity solutions tailored to local infrastructure and regulatory contexts.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Smart Factories and IIoT | +3.0% | Global, particularly Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Demand for Unified IT/OT Security Solutions | +2.5% | Global, strong in mature markets | Medium to Long-term (2025-2033) |

| Expansion of Managed Industrial Cybersecurity Services | +2.0% | Global, especially for SMEs lacking in-house expertise | Medium-term (2025-2030) |

| Integration of AI and Blockchain for Enhanced Security | +1.5% | Global, driven by technological innovation | Long-term (2027-2033) |

Industrial Cybersecurity Market Challenges Impact Analysis

The industrial cybersecurity market, while burgeoning, is not without its significant challenges that impact its trajectory. A primary challenge is the inherent complexity and heterogeneity of industrial control systems (ICS) and operational technology (OT) environments. Unlike standardized IT networks, OT systems often comprise a mix of proprietary protocols, legacy hardware, and custom software, making it difficult to implement uniform security measures. This architectural diversity necessitates highly specialized solutions and expertise, which are often scarce. Another critical challenge is ensuring operational uptime and safety. Any cybersecurity intervention in an industrial setting carries the risk of disrupting critical processes, potentially leading to production losses, equipment damage, or even physical harm. This "safety-first" mentality often prioritizes continuous operation over immediate security patching or system upgrades, creating vulnerabilities that are difficult to address without planned downtime.

Furthermore, the convergence of IT and OT networks, while a driver, also presents a substantial challenge. It blurs the traditional air gap between these environments, exposing OT systems to a wider range of IT-borne threats and requiring a unified security strategy that few organizations have fully achieved. The lack of visibility into OT networks, often due to obscure protocols and embedded systems, is another pervasive issue, making it difficult for security teams to monitor assets, detect anomalies, and respond effectively to threats. Moreover, the evolving threat landscape, characterized by increasingly sophisticated and targeted attacks from nation-state actors and organized cybercrime groups, constantly challenges the efficacy of existing defenses. This necessitates continuous investment in advanced threat intelligence, threat hunting, and adaptive security measures. Finally, budget constraints and a general lack of awareness at the senior management level regarding the unique risks of industrial cyberattacks can impede necessary investment and strategic planning, thereby slowing market adoption and mature security posture development within organizations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity and Heterogeneity of OT/ICS Environments | -1.8% | Global, pervasive across all industrial sectors | Long-term (2025-2033) |

| Ensuring Operational Uptime and Safety | -1.5% | Global, especially critical infrastructure sectors | Long-term (2025-2033) |

| Lack of Visibility into OT Networks | -1.2% | Global, common challenge for all organizations | Medium-term (2025-2030) |

| Evolving and Sophisticated Threat Landscape | -1.0% | Global, continuously adapting threats | Long-term (Ongoing) |

Industrial Cybersecurity Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the Industrial Cybersecurity Market, providing a detailed analysis of its historical performance, current landscape, and future growth trajectories. It offers critical insights into market size estimations, growth drivers, restraints, opportunities, and the impact of emerging technologies like AI. The report meticulously segments the market to provide granular data across various components, deployment models, security types, services, and end-use industries, enabling stakeholders to identify high-growth areas and strategic imperatives. Furthermore, it offers a robust regional analysis, spotlighting key country-level developments and regulatory influences. The competitive landscape section profiles leading market players, assessing their strategies, product portfolios, and market positioning. This report serves as an invaluable resource for industry participants, investors, and decision-makers seeking actionable intelligence to navigate and capitalize on the evolving industrial cybersecurity domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 30.5 Billion |

| Market Forecast in 2033 | USD 120.8 Billion |

| Growth Rate | 19.5% from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Claroty, Dragos, Forescout Technologies, Fortinet, Honeywell, IBM, Indegy, Kaspersky, Lockheed Martin, Microsoft, Nozomi Networks, Palo Alto Networks, Rockwell Automation, Schneider Electric, Siemens, Sophos, Tenable, Trend Micro, Waterfall Security Solutions, ABB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Cybersecurity Market is comprehensively segmented to provide a granular understanding of its diverse facets, enabling precise market analysis and strategic decision-making. These segments encompass various components of cybersecurity solutions, deployment models, specific security types, the wide array of end-use industries, and organizational scales. This detailed segmentation helps in identifying niche markets, understanding specific industry requirements, and assessing the competitive landscape within each sub-segment. Such a detailed breakdown ensures that businesses can tailor their offerings to specific market needs and optimize their go-to-market strategies, ranging from the foundational hardware and software solutions to the critical services that support industrial operations.

Understanding the market through these lenses highlights the varied adoption rates and priorities across different industrial sectors and enterprise sizes. For instance, large enterprises in critical infrastructure sectors often prioritize comprehensive, on-premise solutions with extensive managed services, whereas SMEs might opt for more cloud-based, scalable, and cost-effective solutions. The distinct challenges and regulatory environments within each end-use industry also shape the demand for particular security types, from network and endpoint protection to specialized device and application security for operational technologies. This multi-dimensional segmentation provides stakeholders with actionable intelligence to navigate the complexities of the industrial cybersecurity market and unlock its full potential.

- Component: This segment is crucial as it defines the building blocks of an industrial cybersecurity solution.

- Hardware: Encompasses physical devices that secure industrial networks and control systems, such as specialized firewalls tailored for OT environments, ruggedized routers and switches, and sensors that monitor physical and digital parameters for anomalies.

- Software: Includes a wide array of applications and platforms designed to protect industrial assets. This ranges from Security Information and Event Management (SIEM) for centralized logging and analysis, Intrusion Detection/Prevention Systems (IDPS) for real-time threat detection, Data Loss Prevention (DLP) for sensitive operational data, Endpoint Security for industrial workstations and devices, Identity and Access Management (IAM) for controlled access, Vulnerability Management for identifying weaknesses, and Security Analytics for deriving actionable insights from security data.

- Services: Critical for successful implementation and ongoing management, covering expert consulting for strategic planning, Managed Security Services (MSS) for outsourced security operations, implementation and integration services for seamless deployment, maintenance and support for operational continuity, and specialized training and education services for workforce development in OT security.

- Deployment: This categorizes how industrial cybersecurity solutions are physically or logically implemented.

- On-Premise: Solutions hosted and managed within an organization's own infrastructure, offering maximum control and often preferred for highly sensitive or air-gapped industrial networks.

- Cloud-Based: Solutions delivered as a service over the internet, providing scalability, flexibility, and reduced infrastructure overhead, increasingly adopted for IIoT applicationsand remote monitoring.

- Hybrid: A combination of on-premise and cloud-based components, offering a balance of control and flexibility, common in converged IT/OT environments.

- Security Type: Focuses on the specific aspects of the industrial environment being protected.

- Network Security: Protecting the communication pathways and protocols within OT networks, including firewalls, VPNs, and network segmentation.

- Endpoint Security: Securing individual devices, controllers, and human-machine interfaces (HMIs) connected to the industrial network.

- Application Security: Protecting the software applications running on industrial systems from vulnerabilities and attacks.

- Database Security: Ensuring the integrity and confidentiality of critical data stored in industrial databases.

- Cloud Security: Securing industrial data and applications hosted in cloud environments, particularly relevant for IIoT platforms.

- Device Security: Specifically securing the array of IIoT devices, sensors, and actuators that constitute the edge of industrial networks.

- System Security: Comprehensive protection for the entire industrial control system, including PLCs, DCS, and SCADA systems.

- End-Use Industry: Identifies the various sectors adopting industrial cybersecurity solutions, each with unique operational contexts and threat models.

- Energy & Utilities: Including critical sectors like Oil & Gas, Power Generation (electricity grids), and Water & Wastewater management, which are prime targets for cyberattacks due to their critical societal function.

- Manufacturing: Subdivided into Discrete Manufacturing (e.g., automotive, electronics) and Process Manufacturing (e.g., chemicals, food & beverage), both increasingly reliant on automation and digital systems.

- Transportation: Encompassing vital infrastructure such as Rail networks, Ports, and Airports, where cyber resilience is paramount for public safety and economic flow.

- Chemicals & Pharmaceuticals: Industries with complex processes, high safety requirements, and valuable intellectual property, demanding robust security.

- Mining: Increasingly automated operations requiring cybersecurity for remote control systems and heavy machinery.

- Food & Beverage: Protecting production lines, supply chains, and quality control systems from cyber interference.

- Healthcare (Industrial OT): Securing operational technology in healthcare settings, such as building management systems, medical device manufacturing, and facility infrastructure.

- Others: Includes a broader range of applications like smart building automation systems, and various components of smart cities infrastructure.

- Organization Size: Differentiates the market based on the scale of enterprises and their specific cybersecurity needs and resource availability.

- Small and Medium-sized Enterprises (SMEs): Often face budget constraints and lack in-house expertise, driving demand for managed services and accessible cloud-based solutions.

- Large Enterprises: Typically have complex, dispersed operations, requiring highly integrated, comprehensive, and customizable industrial cybersecurity solutions.

Regional Highlights

The industrial cybersecurity market exhibits distinct characteristics and growth patterns across various geographical regions, influenced by factors such as industrial maturity, regulatory frameworks, and the prevalence of cyber threats.- North America: This region consistently leads the industrial cybersecurity market, primarily driven by the presence of a vast critical infrastructure base, high levels of industrial automation, and stringent regulatory mandates such as NERC-CIP (North American Electric Reliability Corporation – Critical Infrastructure Protection) and various national security directives. The United States and Canada are at the forefront, with significant investments from the energy, manufacturing, and defense sectors. High awareness of cyber risks, coupled with robust cybersecurity spending and a proactive approach to adopting advanced security solutions, further consolidates its leading position.

- Europe: Europe is a key market, propelled by strong regulatory initiatives like the NIS2 Directive (Network and Information Systems Directive) and GDPR, which emphasize the protection of critical infrastructure and operational data. Countries such as Germany, the UK, France, and the Nordics are major contributors, with advanced manufacturing (Industry 4.0), energy, and automotive industries driving demand. The region shows a strong emphasis on research and development in OT security and fostering collaborative ecosystems between public and private sectors to enhance resilience.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, fueled by rapid industrialization, massive investments in smart factories, and the escalating adoption of IoT and AI in countries like China, India, Japan, and South Korea. While awareness and regulatory frameworks are still evolving in some parts, the sheer scale of industrial expansion and the increasing number of cyber incidents are compelling organizations to ramp up their industrial cybersecurity spending. Government initiatives supporting digital transformation and critical infrastructure protection are significant growth catalysts.

- Latin America: This region is experiencing steady growth, driven by the modernization of its oil & gas, mining, and manufacturing sectors. Countries like Brazil, Mexico, and Argentina are increasing their investments in industrial control systems, which in turn necessitates improved cybersecurity measures. The market here is primarily influenced by the need to secure critical infrastructure and address rising cybercrime targeting industrial assets, though budget constraints and a developing regulatory landscape can pose challenges.

- Middle East & Africa (MEA): The MEA region, particularly the Gulf Cooperation Council (GCC) countries, is witnessing significant growth due to large-scale investments in oil & gas, utilities, and smart city projects. National cybersecurity strategies and increasing awareness of the criticality of industrial assets are pushing the adoption of advanced solutions. South Africa and Saudi Arabia are notable markets, with a focus on protecting vital energy infrastructure and diversifying their industrial bases, leading to substantial cybersecurity investments.

Top Key Players:

The market research report covers the analysis of key stake holders of the Industrial Cybersecurity Market. Some of the leading players profiled in the report include -- Claroty

- Dragos

- Forescout Technologies

- Fortinet

- Honeywell

- IBM

- Kaspersky

- Lockheed Martin

- Microsoft

- Nozomi Networks

- Palo Alto Networks

- Rockwell Automation

- Schneider Electric

- Siemens

- Sophos

- Tenable

- Trend Micro

- Waterfall Security Solutions

- ABB

- Cisco Systems

Frequently Asked Questions:

What is industrial cybersecurity and why is it important?

Industrial cybersecurity refers to the protection of industrial control systems (ICS), operational technology (OT), and critical infrastructure from cyber threats. It encompasses safeguarding the integrity, confidentiality, and availability of data and systems that manage physical processes in sectors like manufacturing, energy, and transportation. Its importance stems from the severe consequences of cyberattacks on these systems, which can lead to operational downtime, equipment damage, environmental harm, safety incidents, and significant financial losses, directly impacting business continuity and public safety.

How does IT/OT convergence impact industrial cybersecurity?

IT/OT convergence involves integrating information technology (IT) networks with operational technology (OT) systems to improve efficiency and data flow in industrial environments. While offering significant operational benefits, this convergence simultaneously expands the attack surface for cyber threats. It exposes historically isolated OT systems to common IT-borne vulnerabilities and advanced persistent threats, necessitating a unified and holistic cybersecurity strategy that bridges the gap between IT and OT security practices to ensure comprehensive protection across the entire enterprise.

What are the primary challenges in securing industrial control systems?

Securing industrial control systems (ICS) presents unique challenges due to several factors. These include the widespread use of legacy systems not designed with modern security in mind, proprietary protocols that complicate integration of security tools, the paramount need to ensure continuous operational uptime (prioritizing safety over patching), a critical shortage of professionals skilled in both IT security and OT environments, and the physical location of some systems in harsh or remote environments. These factors collectively make robust ICS cybersecurity implementation and management a complex task.

Which industries are most vulnerable to industrial cyberattacks?

Industries heavily reliant on operational technology and critical infrastructure are most vulnerable to industrial cyberattacks. These primarily include the energy and utilities sector (power grids, oil & gas, water treatment), manufacturing (especially smart factories with high automation), transportation (rail, ports, aviation), chemicals, and defense. Attacks on these sectors can have cascading effects on national security, public services, and economic stability, making them attractive targets for nation-state actors, cybercriminals, and hacktivists.

What role does Artificial Intelligence (AI) play in industrial cybersecurity?

Artificial Intelligence (AI), particularly machine learning, plays a transformative role in industrial cybersecurity by significantly enhancing threat detection and response capabilities. AI algorithms can analyze vast amounts of data from OT networks to identify subtle anomalies and patterns indicative of advanced cyber threats that might be missed by traditional methods. This enables predictive threat intelligence, automated incident response, and more efficient vulnerability management, allowing industrial organizations to proactively defend against sophisticated and evolving cyberattacks with greater speed and accuracy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted