Industrial Control for Process Automation Market

Industrial Control for Process Automation Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702811 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Industrial Control for Process Automation Market Size

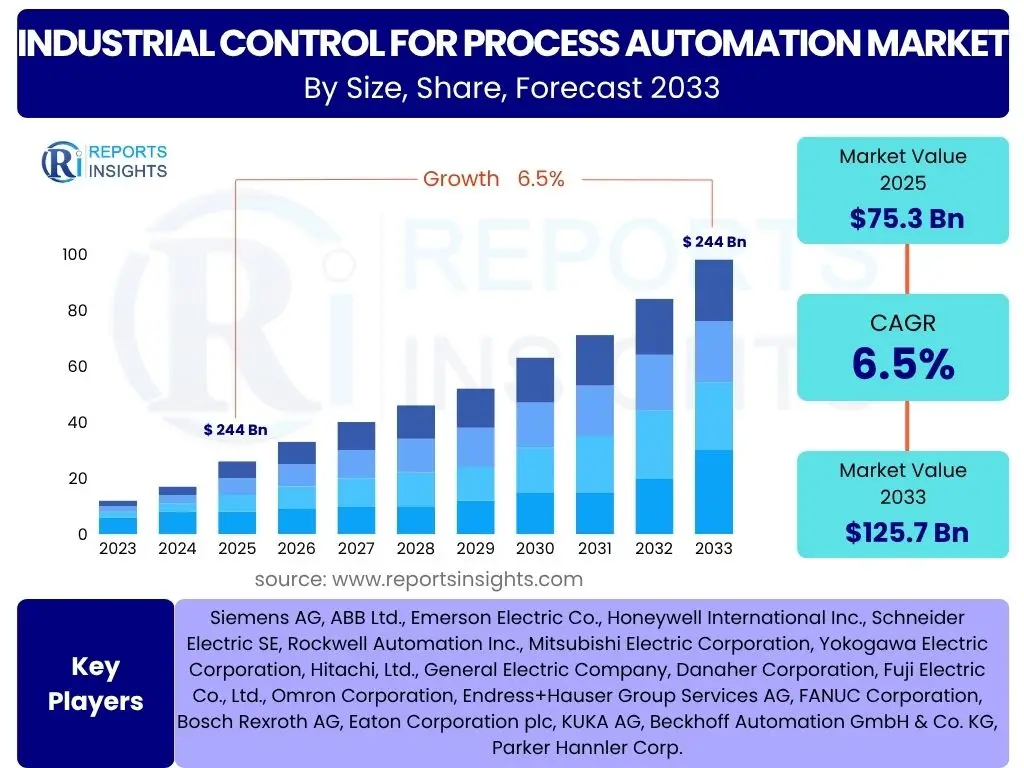

According to Reports Insights Consulting Pvt Ltd, The Industrial Control for Process Automation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 75.3 Billion in 2025 and is projected to reach USD 125.7 Billion by the end of the forecast period in 2033.

Key Industrial Control for Process Automation Market Trends & Insights

The Industrial Control for Process Automation market is undergoing significant transformation, largely driven by the imperative for enhanced operational efficiency, sustainability, and technological integration across various industrial sectors. Users frequently inquire about the impact of digital transformation on traditional control systems, the proliferation of connected devices, and the evolving role of data analytics in real-time process management. A key theme emerging from these inquiries is the shift towards more intelligent, autonomous, and interconnected industrial environments, emphasizing remote capabilities and proactive maintenance strategies. This reflects a broad industry movement towards Industry 4.0 principles, where advanced technologies enable more adaptive and resilient operations.

Another area of consistent interest revolves around the adoption of cloud-based solutions and the increasing emphasis on cybersecurity measures. As industrial control systems become more intertwined with IT networks and the broader internet, concerns about data integrity and system vulnerabilities are paramount. The demand for solutions that offer both robust control and secure connectivity is shaping market development. Furthermore, inquiries highlight the growing importance of energy efficiency and resource optimization, pushing industries to invest in control systems that not only automate but also minimize environmental impact and reduce operational costs. This multifaceted evolution underscores a dynamic market driven by both technological innovation and strategic business objectives.

- Industrial IoT (IIoT) integration for enhanced connectivity and data collection across operational technologies.

- Increased adoption of predictive maintenance solutions to minimize downtime and optimize asset performance.

- Development and deployment of digital twins for real-time simulation, monitoring, and optimization of processes.

- Expansion of cloud-based and edge computing solutions for flexible, scalable, and secure data processing.

- Heightened focus on industrial cybersecurity to protect critical infrastructure from evolving cyber threats.

- Growing emphasis on energy efficiency and sustainability through optimized process control.

- Shift towards modular, scalable, and flexible automation systems to adapt to changing production needs.

- Remote operation and monitoring capabilities gaining traction due to geographical distribution and workforce flexibility requirements.

AI Impact Analysis on Industrial Control for Process Automation

Common user questions regarding AI's impact on Industrial Control for Process Automation reveal a strong interest in how artificial intelligence can move beyond traditional automation to enable smarter, more autonomous operations. Users are keen to understand AI's practical applications, such as optimizing complex processes, enhancing predictive capabilities, and enabling real-time decision-making in dynamic industrial environments. There is a clear expectation that AI will lead to significant improvements in efficiency, quality control, and resource utilization, pushing the boundaries of what automated systems can achieve. However, concerns frequently arise about the integration challenges of AI with existing legacy infrastructure, the need for specialized skills to manage AI-driven systems, and the crucial aspects of data privacy and cybersecurity in an AI-enhanced landscape.

The potential for AI to introduce new levels of operational intelligence is a major area of exploration. Users envision AI empowering control systems to learn from operational data, predict equipment failures before they occur, and adapt process parameters automatically for optimal performance. This extends to questions about AI's role in improving safety protocols, reducing human error, and even facilitating autonomous decision-making in critical industrial scenarios. While the benefits are widely anticipated, the discussions also highlight the importance of robust data governance frameworks and ethical considerations in deploying AI solutions that directly influence physical processes. The collective view is that AI will be a transformative force, but its successful implementation hinges on addressing technological, human, and security challenges holistically.

- Enhanced process optimization through AI algorithms that analyze vast datasets to identify optimal operating parameters, leading to improved throughput and reduced waste.

- Advanced predictive maintenance capabilities, leveraging AI to forecast equipment failures with greater accuracy, minimizing unplanned downtime and extending asset lifespan.

- Development of autonomous control systems that can make real-time decisions and adjust operations without direct human intervention, improving responsiveness and efficiency.

- Improved quality control and anomaly detection by analyzing sensor data and identifying deviations from normal patterns, ensuring consistent product quality.

- Real-time decision making support for operators, providing actionable insights derived from complex data analysis, enabling quicker and more informed responses to operational changes.

- Increased cybersecurity threat detection and response by identifying unusual network traffic patterns or system behaviors indicative of cyberattacks.

- Optimization of energy consumption through AI-driven load balancing and resource allocation, contributing to sustainability efforts and cost reduction.

- Facilitation of human-machine collaboration, allowing AI to handle repetitive tasks while humans focus on strategic oversight and problem-solving.

Key Takeaways Industrial Control for Process Automation Market Size & Forecast

Common user inquiries about the Industrial Control for Process Automation market size and forecast consistently point towards a desire to understand the overall growth trajectory, the primary factors driving this expansion, and the areas presenting the most significant investment opportunities. Users are seeking clarity on whether the market will continue its upward trend, particularly in light of global economic shifts and technological advancements. The forecast indicates robust and sustained growth, signaling a healthy investment climate for companies operating within or looking to enter this sector. This growth is predominantly fueled by the widespread adoption of digital transformation initiatives across industries, emphasizing automation, data-driven decision-making, and the pursuit of operational excellence.

Furthermore, there is keen interest in identifying which specific technologies or segments within industrial control are poised for accelerated growth, alongside understanding the regional dynamics that influence market expansion. The analysis suggests that while established markets like North America and Europe will continue to be strongholds due to ongoing modernization efforts, emerging economies, particularly in Asia Pacific, will witness rapid acceleration driven by new infrastructure development and industrialization. The increasing integration of advanced technologies such as Artificial Intelligence, Machine Learning, and Industrial Internet of Things is a pivotal element shaping this future landscape, promising enhanced efficiencies and capabilities for process automation across diverse verticals. These insights collectively highlight a market that is not only growing in size but also evolving in complexity and technological sophistication.

- The Industrial Control for Process Automation market is projected for significant and sustained growth, indicating a robust sector for investment and innovation.

- Technological advancements, particularly in Industrial IoT, AI, and cloud computing, are primary catalysts for market expansion, driving new capabilities and efficiencies.

- Operational efficiency and productivity improvements remain core objectives for end-users, fueling demand for advanced automation solutions.

- Strategic investment opportunities are emerging in areas such as predictive maintenance, digital twins, and cybersecurity solutions for industrial environments.

- Regional disparities in growth are expected, with Asia Pacific showing strong potential due to rapid industrialization, while North America and Europe maintain leading positions through modernization efforts.

- The shift towards smart manufacturing and Industry 4.0 principles is a foundational trend influencing market development and technology adoption.

Industrial Control for Process Automation Market Drivers Analysis

The Industrial Control for Process Automation market is experiencing significant growth propelled by several key drivers. The global push towards Industry 4.0 and digital transformation is paramount, compelling industries to adopt intelligent automation systems that integrate physical and digital processes. This paradigm shift enables real-time data exchange, enhanced connectivity, and autonomous operations, leading to unprecedented levels of efficiency and productivity. Businesses across various sectors are recognizing the competitive advantage offered by modernized control systems, driving investment in these technologies to streamline operations, reduce human error, and optimize resource utilization. This fundamental shift in industrial philosophy serves as a powerful foundational driver.

Furthermore, the escalating demand for operational efficiency and increased productivity directly fuels the market's expansion. Industries are under continuous pressure to lower operating costs, improve product quality, and accelerate time-to-market. Advanced industrial control systems offer solutions to these challenges by automating complex tasks, minimizing waste, and optimizing resource allocation. Alongside this, stringent regulatory compliance and evolving safety standards, particularly in sectors such as chemicals, pharmaceuticals, and oil & gas, necessitate the adoption of reliable and precise control automation to ensure adherence to environmental, health, and safety mandates. The growing imperative for energy efficiency and sustainable practices also plays a crucial role, as modern control systems contribute to reducing energy consumption and carbon footprints, aligning with global environmental goals.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industry 4.0 and Digital Transformation Initiatives | +2.5% | Global (Strong in Developed Nations) | Short to Medium Term |

| Increasing Demand for Operational Efficiency and Productivity | +2.0% | Global | Medium Term |

| Growing Emphasis on Regulatory Compliance and Safety Standards | +1.5% | North America, Europe, Asia Pacific | Medium Term |

| Rise of Smart Factories and Advanced Automation Adoption | +2.0% | Asia Pacific, Europe | Short to Medium Term |

Industrial Control for Process Automation Market Restraints Analysis

Despite the robust growth drivers, the Industrial Control for Process Automation market faces certain restraints that could temper its expansion. One significant hurdle is the high initial investment required for implementing advanced industrial control systems. These systems often involve substantial capital outlay for hardware, software, integration services, and personnel training, which can be prohibitive for small and medium-sized enterprises (SMEs) or industries with limited capital budgets. The perceived return on investment (ROI) may not always be immediately apparent, leading to delayed adoption or a preference for incremental upgrades rather than full-scale system overhauls. This financial barrier can slow down market penetration, especially in cost-sensitive regions or sectors.

Another major restraint is the escalating threat of cybersecurity risks and vulnerabilities. As industrial control systems become more interconnected and integrated with IT networks, they become prime targets for cyberattacks, ranging from data breaches to operational disruptions. The potential for malicious actors to compromise critical infrastructure or production processes poses a severe risk, leading to significant financial losses, reputational damage, and even safety hazards. The lack of a skilled workforce and expertise in managing, operating, and maintaining these complex, highly technical systems also acts as a significant impediment. The scarcity of professionals proficient in industrial automation, cybersecurity, and data analytics creates a talent gap that can hinder the effective deployment and optimization of advanced control solutions. Additionally, the complexities associated with integrating new, sophisticated automation systems with existing legacy infrastructure present significant technical and operational challenges, often leading to protracted implementation periods and unforeseen costs, further restraining market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs and Implementation Complexity | -1.8% | Global | Medium Term |

| Increasing Cybersecurity Risks and Vulnerabilities | -1.5% | Global | Medium to Long Term |

| Lack of Skilled Workforce and Expertise in Advanced Automation | -1.2% | Global | Medium Term |

| Integration Challenges with Legacy Industrial Systems | -1.0% | Global | Medium Term |

Industrial Control for Process Automation Market Opportunities Analysis

The Industrial Control for Process Automation market presents numerous growth opportunities driven by technological advancements and evolving industry needs. The rapid emergence of Artificial Intelligence (AI) and Machine Learning (ML), coupled with advanced analytics, stands out as a significant opportunity. These technologies enable control systems to move beyond simple automation to predictive, adaptive, and autonomous operations, offering unprecedented levels of efficiency, optimization, and problem-solving capabilities. Industries are increasingly looking to leverage AI/ML for tasks such as anomaly detection, predictive maintenance, process optimization, and complex decision-making, opening new revenue streams for solution providers and fostering innovation within the market.

Furthermore, the growing demand for cloud-based and edge computing solutions provides another substantial opportunity. Cloud platforms offer scalability, flexibility, and cost-effectiveness for data storage, processing, and application deployment in industrial environments, facilitating remote monitoring and distributed control. Edge computing, on the other hand, enables real-time data processing closer to the source, reducing latency and enhancing responsiveness for critical applications. This hybrid approach caters to the diverse needs of modern industrial operations, from large-scale enterprises to remote facilities. Additionally, the expansion into developing economies, particularly in Asia Pacific and Latin America, represents a vast untapped market. Rapid industrialization, infrastructure development, and increasing foreign investments in these regions are driving the need for sophisticated automation solutions. Customization and the development of modular automation solutions also offer a fertile ground for growth, as industries seek tailored systems that can adapt to specific production requirements and scale as operations evolve, providing specialized solutions that address niche market demands and integrate seamlessly into existing frameworks.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI/ML and Advanced Analytics in Control Systems | +2.2% | Global | Medium to Long Term |

| Increasing Demand for Cloud-based and Edge Computing Solutions | +1.8% | Global | Short to Medium Term |

| Expansion into Developing Economies and Emerging Markets | +2.0% | Asia Pacific, Latin America, MEA | Long Term |

| Growing Need for Customized and Modular Automation Solutions | +1.5% | Global | Short to Medium Term |

Industrial Control for Process Automation Market Challenges Impact Analysis

The Industrial Control for Process Automation market faces several significant challenges that can impede its growth and widespread adoption. A primary concern is the issue of interoperability and standardization. The industrial landscape is characterized by a vast array of proprietary systems, protocols, and devices from different vendors, making seamless integration and data exchange highly complex. This lack of universal standards leads to fragmented ecosystems, increased integration costs, and difficulties in creating cohesive, plant-wide automation solutions. Overcoming these technical barriers requires significant investment in middleware and custom programming, which adds to the overall project complexity and can deter potential adopters.

Another critical challenge revolves around data management and security concerns. The proliferation of connected devices and the vast amounts of operational data generated by industrial control systems raise significant questions about how this data is collected, stored, processed, and protected. Ensuring data integrity, confidentiality, and availability, especially in an era of increasing cyber threats, is paramount. Industries are grappling with the complexities of securing their operational technology (OT) networks from sophisticated cyberattacks, which can have devastating consequences. The rapid pace of technological obsolescence also poses a challenge; as new technologies emerge, existing systems can quickly become outdated, necessitating continuous upgrades and significant capital expenditure to remain competitive. This cycle of innovation requires industries to consistently invest in modernization, potentially straining budgets. Furthermore, global economic volatility and geopolitical risks can significantly impact investment decisions and supply chains within the industrial automation sector, creating uncertainty and hindering market stability, making long-term planning difficult for businesses and suppliers alike.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability and Standardization Issues Across Systems | -1.3% | Global | Medium Term |

| Complex Data Management and Evolving Security Concerns | -1.7% | Global | Medium to Long Term |

| Rapid Technological Obsolescence and Need for Constant Upgrades | -1.0% | Global | Medium Term |

| Economic Volatility and Geopolitical Risks Impacting Investment | -0.8% | Global | Short Term |

Industrial Control for Process Automation Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Industrial Control for Process Automation market, covering historical trends, current market dynamics, and future growth projections from 2025 to 2033. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis across various components, industry verticals, and solutions. The report also highlights regional market insights and profiles key players, delivering actionable intelligence for stakeholders seeking to understand and capitalize on the evolving landscape of industrial process automation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 75.3 Billion |

| Market Forecast in 2033 | USD 125.7 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., Emerson Electric Co., Honeywell International Inc., Schneider Electric SE, Rockwell Automation Inc., Mitsubishi Electric Corporation, Yokogawa Electric Corporation, Hitachi, Ltd., General Electric Company, Danaher Corporation, Fuji Electric Co., Ltd., Omron Corporation, Endress+Hauser Group Services AG, FANUC Corporation, Bosch Rexroth AG, Eaton Corporation plc, KUKA AG, Beckhoff Automation GmbH & Co. KG, Parker Hannler Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Control for Process Automation market is comprehensively segmented to provide a granular view of its diverse landscape and to identify specific growth areas and market dynamics. This segmentation allows for a detailed understanding of how different components, industry verticals, and solution types contribute to the overall market size and growth trajectory. Analyzing the market through these various lenses helps stakeholders identify niche opportunities, understand end-user preferences, and tailor strategies to specific market segments, thereby maximizing market penetration and profitability. Each segment is characterized by unique technological requirements, adoption rates, and market drivers, making a detailed analysis crucial for strategic planning.

The component-based segmentation provides insight into the demand for critical hardware and software elements that form the backbone of industrial control systems, such as Distributed Control Systems (DCS), Programmable Logic Controllers (PLC), and Supervisory Control and Data Acquisition (SCADA) systems. The industry vertical segmentation reveals which sectors are the primary consumers of these technologies, ranging from traditional heavy industries like Oil & Gas and Power Generation to rapidly evolving sectors such as Food & Beverage and Pharmaceuticals. Furthermore, segmenting by solution and service type clarifies the market for consulting, integration, implementation, and ongoing maintenance and support services, reflecting the lifecycle needs of industrial automation projects. This multi-dimensional segmentation is vital for a thorough market assessment, highlighting both established demand and emerging trends across the industrial spectrum.

- By Component:

- Distributed Control Systems (DCS)

- Programmable Logic Controllers (PLC)

- Supervisory Control and Data Acquisition (SCADA)

- Human Machine Interface (HMI)

- Manufacturing Execution Systems (MES)

- Industrial Safety Systems

- Field Devices (Sensors, Actuators, Valves)

- Others (Analyzers, Transmitters)

- By Industry Vertical:

- Oil and Gas

- Power Generation

- Chemicals and Petrochemicals

- Food and Beverage

- Water and Wastewater Treatment

- Pharmaceuticals and Biotechnology

- Metals and Mining

- Pulp and Paper

- Automotive

- Discrete Manufacturing

- Others

- By Solution/Service:

- Consulting

- Integration & Implementation

- Maintenance & Support

Regional Highlights

- North America: Characterized by early adoption of advanced industrial automation technologies, significant investments in research and development, and a strong presence of key market players. The region's focus on modernization of aging infrastructure and smart manufacturing initiatives drives consistent demand.

- Europe: A leader in Industry 4.0 adoption, with robust manufacturing sectors and stringent regulatory environments promoting automation and safety. Western European countries, particularly Germany, lead in integrating advanced control systems and smart factory concepts.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid industrialization, increasing manufacturing activities, and significant government initiatives promoting automation in countries like China, India, Japan, and South Korea. Investments in new industrial plants and infrastructure development are key drivers.

- Latin America: Exhibits growing potential driven by expanding process industries, including oil and gas, mining, and food and beverage. Economic development and foreign investments are gradually boosting the adoption of industrial control solutions, albeit at a slower pace compared to developed regions.

- Middle East and Africa (MEA): Growth in this region is primarily propelled by large-scale investments in the oil and gas sector, petrochemicals, and infrastructure development projects. The push for economic diversification and industrialization also contributes to the increasing demand for advanced process automation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Control for Process Automation Market.- Siemens AG

- ABB Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Schneider Electric SE

- Rockwell Automation Inc.

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- Hitachi, Ltd.

- General Electric Company

- Danaher Corporation

- Fuji Electric Co., Ltd.

- Omron Corporation

- Endress+Hauser Group Services AG

- FANUC Corporation

- Bosch Rexroth AG

- Eaton Corporation plc

- KUKA AG

- Beckhoff Automation GmbH & Co. KG

- Parker Hannler Corp.

Frequently Asked Questions

What is Industrial Control for Process Automation?

Industrial Control for Process Automation refers to the systems and technologies employed to monitor, manage, and control continuous or batch processes within industrial facilities. These systems regulate variables like temperature, pressure, flow, and level to ensure efficient, safe, and consistent production in industries such as oil & gas, chemicals, and power generation.

What are the primary components of Industrial Control Systems?

Key components typically include Distributed Control Systems (DCS) for complex processes, Programmable Logic Controllers (PLC) for discrete control, Supervisory Control and Data Acquisition (SCADA) for wide-area monitoring, Human Machine Interface (HMI) for operator interaction, Manufacturing Execution Systems (MES), and various field devices such as sensors, actuators, and control valves.

Which industries are the major end-users of these systems?

Major end-users of Industrial Control for Process Automation systems span a wide range of sectors, including oil and gas, power generation, chemicals and petrochemicals, food and beverage, water and wastewater treatment, pharmaceuticals and biotechnology, metals and mining, and pulp and paper, all seeking enhanced operational efficiency and safety.

How does AI influence Industrial Control for Process Automation?

AI significantly enhances industrial control by enabling advanced capabilities such as predictive maintenance, real-time process optimization, autonomous control systems, and improved quality control. It leverages data analytics to identify patterns, forecast potential issues, and make informed decisions, leading to greater efficiency, reduced downtime, and enhanced operational intelligence.

What are the key drivers for market growth in this sector?

Key drivers for market growth include the increasing adoption of Industry 4.0 and digital transformation initiatives, rising demand for operational efficiency and productivity across industries, stringent regulatory compliance and safety standards, and the global trend towards smart factories and advanced automation solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted