Industrial Computed Tomography Market

Industrial Computed Tomography Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709479 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

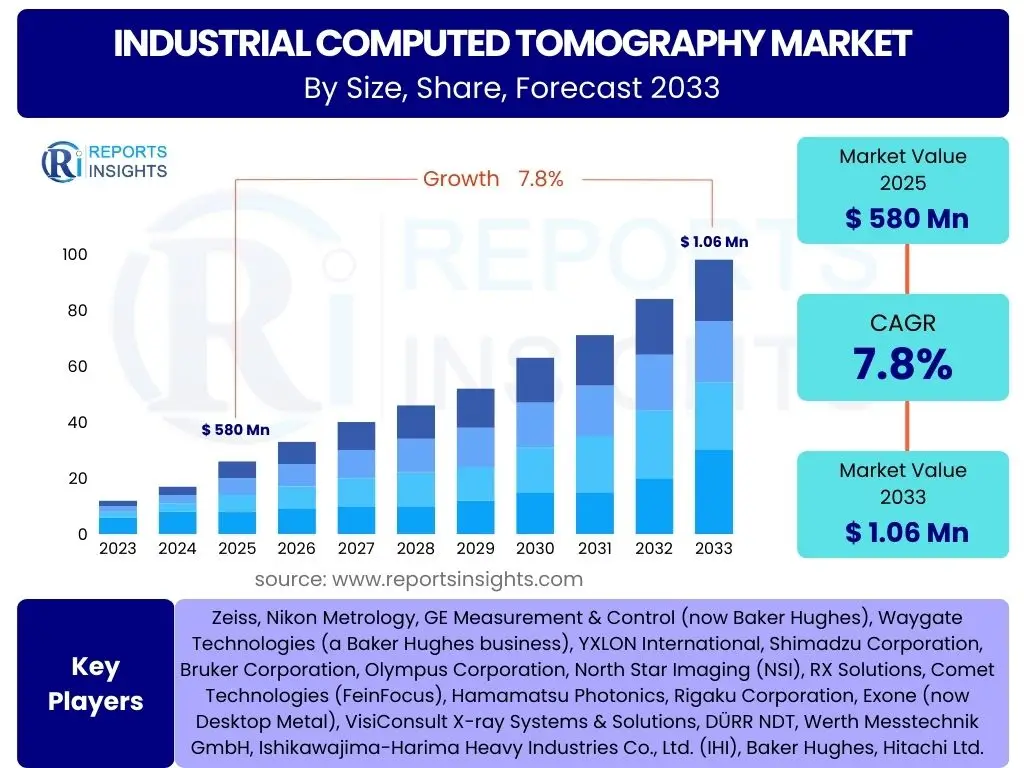

Industrial Computed Tomography Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Computed Tomography Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 580 Million in 2025 and is projected to reach USD 1.06 Billion by the end of the forecast period in 2033.

Key Industrial Computed Tomography Market Trends & Insights

The Industrial Computed Tomography (CT) market is undergoing significant transformation driven by advancements in imaging technology, increasing demand for non-destructive testing (NDT), and the pervasive adoption of automation across manufacturing sectors. Users frequently inquire about the integration of advanced algorithms, the expansion into new application areas, and the quest for faster, more accurate inspection processes. There is a clear market emphasis on solutions that can provide intricate internal defect detection, precise dimensional metrology, and comprehensive material analysis without compromising part integrity.

Furthermore, the market exhibits a strong trend towards higher resolution systems, enabling the examination of increasingly complex and miniature components, particularly in electronics and medical device manufacturing. The push for real-time analysis capabilities and the ability to handle a wider range of material densities are also prominent. Industry stakeholders are keenly interested in how these technological enhancements contribute to improved product quality, reduced waste, and accelerated product development cycles, ultimately bolstering competitive advantage.

- Enhanced resolution and speed in imaging systems.

- Growing adoption of inline and automated CT inspection for production lines.

- Integration of advanced software for data analysis, simulation, and reverse engineering.

- Expansion of applications beyond traditional quality control to material science and additive manufacturing.

- Development of compact and portable CT systems for diverse industrial environments.

AI Impact Analysis on Industrial Computed Tomography

Artificial Intelligence (AI) is poised to significantly revolutionize the Industrial Computed Tomography sector by enhancing virtually every stage of the CT workflow, from data acquisition to analysis and decision-making. Common user questions revolve around how AI can accelerate scan times, improve image quality, automate defect detection, and provide more insightful interpretations of complex volumetric data. The expectation is that AI algorithms will enable faster, more accurate identification of anomalies, reduce human error, and streamline the entire inspection process, moving towards predictive maintenance and smart manufacturing paradigms.

The core of AI's impact lies in its ability to process vast amounts of data generated by CT scanners, identifying patterns and correlations that human operators might miss. This leads to more precise defect classification, optimized metrology, and enhanced material characterization. Users are also keen on AI's potential to facilitate adaptive scanning protocols, where the system intelligently adjusts parameters based on the object being scanned, and its role in developing digital twins for comprehensive product lifecycle management. Concerns often relate to data privacy, algorithm bias, and the need for robust validation protocols for AI-driven insights.

- Automated defect detection and classification, significantly reducing inspection time.

- Improved image reconstruction and noise reduction, leading to higher quality and more interpretable data.

- Enhanced metrology capabilities through AI-powered feature recognition and measurement automation.

- Predictive maintenance for CT systems and components, optimizing operational efficiency.

- Facilitation of digital twin creation and advanced material characterization through deep learning.

Key Takeaways Industrial Computed Tomography Market Size & Forecast

The Industrial Computed Tomography market is experiencing robust growth, driven by an increasing global emphasis on product quality, safety, and operational efficiency across diverse manufacturing sectors. Key takeaways from the market size and forecast analysis reveal a consistent upward trajectory, primarily fueled by the accelerating adoption of Industry 4.0 principles, which demand sophisticated, non-destructive inspection capabilities for complex components and advanced materials. Stakeholders frequently inquire about the underlying drivers of this growth, the most promising application areas, and the geographical regions poised for significant expansion.

The forecast period indicates a sustained demand for CT solutions that can provide high-resolution, volumetric data for critical applications such as aerospace, automotive, and medical device manufacturing. The market is not merely growing in volume but also evolving in complexity, with a clear shift towards integrated systems that combine CT with other inspection technologies, alongside the development of faster, more automated, and AI-enabled solutions. Understanding these dynamics is crucial for strategic planning, investment decisions, and navigating the competitive landscape of industrial quality assurance.

- Consistent high growth projected, indicating strong industry confidence and expanding application base.

- Technological advancements, particularly in AI and automation, are central to market expansion.

- The shift towards additive manufacturing and complex component design necessitates advanced inspection tools like industrial CT.

- Aerospace and automotive sectors remain key revenue contributors, with emerging opportunities in electronics and medical devices.

- Investment in R&D for enhanced resolution, speed, and analytical software will be critical for market leadership.

Industrial Computed Tomography Market Drivers Analysis

The Industrial Computed Tomography market is significantly propelled by the increasing demand for non-destructive testing and inspection across various industries. As manufacturing processes become more complex, especially with the rise of additive manufacturing and the use of advanced materials, the need for precise internal quality inspection without compromising the integrity of the component becomes paramount. This fundamental requirement drives the adoption of CT systems, which offer unparalleled volumetric data and detailed defect analysis.

Furthermore, stringent quality control standards and regulatory requirements, particularly in safety-critical sectors such as aerospace, automotive, and medical devices, act as powerful market drivers. Manufacturers are compelled to implement advanced inspection technologies to ensure compliance, mitigate risks, and uphold product reliability. The continuous technological advancements in CT systems, including higher resolution detectors, faster scan times, and sophisticated software for data analysis and visualization, further enhance their appeal and broaden their applicability, thereby sustaining market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for non-destructive testing (NDT) | +2.1% | Global, particularly Asia Pacific & Europe | Medium to Long-term |

| Growth in additive manufacturing & complex geometries | +1.8% | North America, Europe | Medium-term |

| Stringent quality control standards & regulations | +1.5% | Global, all regulated industries | Ongoing |

| Technological advancements in CT systems | +1.3% | Global | Short to Medium-term |

| Industry 4.0 & automation integration | +1.1% | Europe, North America, parts of Asia | Medium-term |

Industrial Computed Tomography Market Restraints Analysis

Despite the robust growth, the Industrial Computed Tomography market faces several significant restraints that could impede its full potential. A primary limiting factor is the high initial investment cost associated with acquiring advanced CT systems. These systems often involve substantial capital expenditure, including the cost of the scanner, specialized software, and necessary infrastructure adjustments, making them less accessible for small and medium-sized enterprises (SMEs) with limited budgets. This financial barrier can slow down adoption rates, particularly in emerging economies or for companies still evaluating the return on investment.

Another crucial restraint is the complexity involved in operating and maintaining industrial CT equipment. These systems require highly skilled personnel for setup, calibration, scanning, and especially for interpreting the complex volumetric data generated. The shortage of adequately trained technicians and engineers, coupled with the ongoing costs of software licenses, maintenance, and regular calibration, adds to the operational burden. Furthermore, the scan speed for very large or dense objects can still be a limitation, making real-time inline inspection challenging for certain high-volume production environments, which necessitates careful integration planning.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment for CT systems | -1.7% | Global, especially SMEs | Short to Medium-term |

| Requirement for highly skilled operators & data analysts | -1.2% | Global | Medium-term |

| Limited scan speed for very large/dense objects | -0.9% | Specific heavy industries | Short to Medium-term |

| Complexity of data interpretation & software integration | -0.8% | Global | Short-term |

Industrial Computed Tomography Market Opportunities Analysis

The Industrial Computed Tomography market is rich with opportunities, particularly driven by the accelerating pace of technological innovation and the expansion into new application domains. One of the most significant opportunities lies in the integration of CT systems with advanced analytics, artificial intelligence, and machine learning. This integration promises to unlock deeper insights from inspection data, automate anomaly detection, predict material failures, and optimize manufacturing processes, thereby creating significant value for end-users and expanding the scope of CT beyond traditional quality control.

Furthermore, the rapid growth of additive manufacturing (3D printing) presents a substantial opportunity. Components produced via additive manufacturing often feature complex internal geometries and require thorough internal defect inspection and metrology, which CT systems are uniquely positioned to provide. The push towards miniaturization in industries like electronics and medical devices also creates a niche for micro and nano-CT systems, enabling inspection of intricate small-scale components. Emerging markets, especially in Asia Pacific, offer significant untapped potential due to their expanding manufacturing bases and increasing adoption of advanced industrial technologies, fueled by governmental support for industrial modernization.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of AI and machine learning for data analysis | +2.0% | Global | Medium to Long-term |

| Expanding applications in additive manufacturing & 3D printing | +1.9% | North America, Europe, Asia Pacific | Medium-term |

| Miniaturization trends in electronics and medical devices | +1.6% | Global | Long-term |

| Penetration into emerging markets (e.g., Asia Pacific) | +1.4% | Asia Pacific, Latin America | Medium to Long-term |

| Development of hybrid inspection solutions | +1.2% | Global | Medium-term |

Industrial Computed Tomography Market Challenges Impact Analysis

The Industrial Computed Tomography market, while promising, faces several operational and technological challenges that demand strategic attention from market participants. One significant challenge is the inherent difficulty in scanning objects made from highly dense materials or components with very complex internal structures, which can lead to image artifacts, reduced penetration, or excessively long scan times. This limitation can restrict the applicability of CT in certain heavy industries or for specific advanced materials, requiring continuous innovation in X-ray sources and detector technologies.

Another prevalent challenge is the substantial volume of data generated by high-resolution CT scans. Processing, storing, and efficiently analyzing terabytes of volumetric data necessitate robust computing infrastructure and sophisticated software algorithms, which can be costly and technically demanding for many end-users. Ensuring data interoperability and seamless integration of CT systems with existing manufacturing execution systems (MES) or quality management systems (QMS) also presents a considerable hurdle. Furthermore, the competitive landscape is intensifying, pushing manufacturers to innovate rapidly while navigating intellectual property rights and maintaining competitive pricing strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Difficulty in scanning highly dense or complex materials | -1.5% | Global, heavy industries | Ongoing |

| Managing and analyzing large volumetric data sets | -1.0% | Global | Short to Medium-term |

| Integration with existing manufacturing ecosystems | -0.8% | Global | Medium-term |

| High maintenance and operational costs post-acquisition | -0.7% | Global | Long-term |

Industrial Computed Tomography Market - Updated Report Scope

This comprehensive market insights report provides an in-depth analysis of the Industrial Computed Tomography market, covering its current landscape, growth projections, key trends, and the impact of emerging technologies. It offers a detailed examination of market size, segmentation by component, application, end-use industry, dimension, and type, alongside regional dynamics and the profiles of leading market players, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 580 Million |

| Market Forecast in 2033 | USD 1.06 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Zeiss, Nikon Metrology, GE Measurement & Control (now Baker Hughes), Waygate Technologies (a Baker Hughes business), YXLON International, Shimadzu Corporation, Bruker Corporation, Olympus Corporation, North Star Imaging (NSI), RX Solutions, Comet Technologies (FeinFocus), Hamamatsu Photonics, Rigaku Corporation, Exone (now Desktop Metal), VisiConsult X-ray Systems & Solutions, DÜRR NDT, Werth Messtechnik GmbH, Ishikawajima-Harima Heavy Industries Co., Ltd. (IHI), Baker Hughes, Hitachi Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Computed Tomography market is meticulously segmented to provide a granular view of its diverse facets, enabling a detailed understanding of market dynamics across various components, applications, end-use industries, dimensions, and system types. This comprehensive segmentation highlights the specific growth drivers and challenges pertinent to each category, offering insights into where investment and innovation are concentrated. The categorization helps in identifying emerging niches and understanding the evolving demands of different industrial sectors.

- By Component: This segment includes the essential hardware, software, and services that constitute an industrial CT system. Hardware components such as X-ray tubes, detectors, and manipulators are fundamental for data acquisition. Software, encompassing image reconstruction, analysis, and metrology tools, is crucial for data processing and interpretation. Services like installation, maintenance, calibration, and training ensure optimal system performance and longevity.

- By Application: Industrial CT finds extensive applications across a spectrum of industrial needs. Key applications include precise quality control and inspection for internal defects, detailed material research for new alloy development, accelerated product development through rapid prototyping inspection, high-accuracy metrology for dimensional verification, non-destructive failure analysis, and reverse engineering for design replication or improvement.

- By End-use Industry: The technology is critical across numerous sectors. The automotive industry utilizes CT for inspecting engine components and castings. Aerospace & Defense relies on it for turbine blades and structural integrity. Electronics & Semiconductors use it for solder joint and PCB inspection. Medical Devices leverage it for implant and device quality. Energy, general manufacturing, and research & academia also benefit significantly from CT capabilities.

- By Dimension: Segmentation by dimension reflects the evolving capabilities of CT systems. 2D CT provides cross-sectional slices. 3D CT offers full volumetric data, crucial for complex internal structures. Emerging 4D CT systems enable time-resolved analysis, observing dynamic processes or material changes over time, particularly valuable in material science and process optimization.

- By Type: This segmentation distinguishes systems based on their resolution and typical object size. Micro-CT systems offer high-resolution imaging for small and intricate components. Nano-CT pushes these limits further for even finer details. Industrial X-ray CT encompasses a broader range, suitable for larger industrial parts and general inspection tasks.

Regional Highlights

- North America: This region is a significant market due to the presence of key aerospace, automotive, and medical device manufacturers, coupled with substantial R&D investments. The early adoption of advanced manufacturing technologies and stringent quality control standards drive demand for high-end industrial CT systems.

- Europe: Europe represents a mature market with a strong focus on advanced manufacturing, particularly in Germany and France. The region benefits from robust R&D infrastructure, high automation rates in industries, and a strong emphasis on precision engineering, leading to continuous demand for sophisticated CT solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by rapid industrialization, increasing foreign direct investment in manufacturing, and the expansion of electronics, automotive, and general manufacturing sectors, especially in China, Japan, and India. Governments are also promoting Industry 4.0 initiatives, boosting adoption.

- Latin America: This region shows steady growth, particularly in automotive manufacturing in Mexico and Brazil, and mining operations. Increased investment in infrastructure and manufacturing modernization initiatives are gradually driving the adoption of industrial CT.

- Middle East & Africa (MEA): The MEA market is emerging, driven by diversification efforts in oil & gas, defense, and nascent manufacturing sectors. Investment in infrastructure projects and the growing need for quality assurance in critical industrial applications contribute to its growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Computed Tomography Market.- Zeiss

- Nikon Metrology

- GE Measurement & Control (now Baker Hughes)

- Waygate Technologies (a Baker Hughes business)

- YXLON International

- Shimadzu Corporation

- Bruker Corporation

- Olympus Corporation

- North Star Imaging (NSI)

- RX Solutions

- Comet Technologies (FeinFocus)

- Hamamatsu Photonics

- Rigaku Corporation

- Exone (now Desktop Metal)

- VisiConsult X-ray Systems & Solutions

- DÜRR NDT

- Werth Messtechnik GmbH

- Ishikawajima-Harima Heavy Industries Co., Ltd. (IHI)

- Baker Hughes

- Hitachi Ltd.

Frequently Asked Questions

What is Industrial Computed Tomography (CT)?

Industrial Computed Tomography (CT) is a non-destructive testing (NDT) method that uses X-rays to generate 2D cross-sectional images or 3D volumetric representations of an object's internal structure without causing any damage. It allows for detailed inspection, dimensional measurement, and material analysis of complex components, revealing internal defects, porosities, and assembly issues that are invisible to the naked eye or other surface inspection methods.

What are the primary applications of Industrial CT?

The primary applications of Industrial CT include quality control and inspection for internal defects in castings, welds, and additive manufactured parts; precise dimensional metrology for complex geometries; material analysis to identify composition variations or foreign inclusions; failure analysis to pinpoint root causes of product breakdowns; and reverse engineering to create digital models of physical objects. It is widely used in aerospace, automotive, medical devices, and electronics industries.

How does AI impact Industrial CT systems?

AI significantly impacts Industrial CT systems by enhancing various aspects of the workflow. It is used for automated defect detection and classification, reducing human intervention and speeding up inspection. AI algorithms improve image reconstruction quality by reducing noise and artifacts, and optimize scanning parameters for better results. Furthermore, AI facilitates advanced data analysis, enabling predictive maintenance, digital twin creation, and more accurate material characterization by identifying complex patterns in volumetric data.

What are the key drivers for the growth of the Industrial CT market?

Key drivers for the Industrial CT market growth include the increasing global demand for non-destructive testing, the proliferation of additive manufacturing requiring internal inspection, stringent quality control standards across safety-critical industries, continuous technological advancements in CT hardware and software (especially AI integration), and the broader trend towards automation and Industry 4.0 in manufacturing processes. These factors collectively push industries to adopt more precise and reliable inspection solutions.

What are the main challenges faced by the Industrial CT market?

The main challenges in the Industrial CT market include the high initial capital investment required for purchasing advanced CT systems, the need for highly skilled operators and data analysts for complex operation and interpretation, limitations in scanning very large or dense objects which can impact scan speed and penetration, and the technical complexity of managing and integrating vast amounts of volumetric data with existing enterprise systems. Addressing these challenges is crucial for broader market adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted