In Vehicle Infotainment Cyber Security Market

In Vehicle Infotainment Cyber Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709062 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

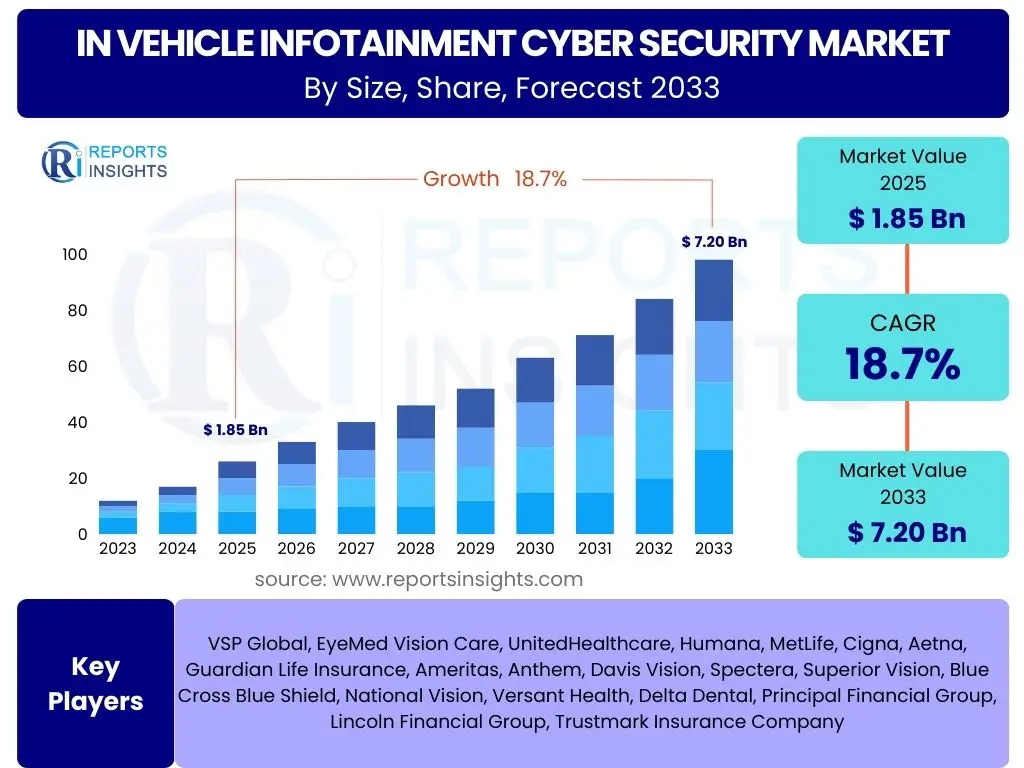

In Vehicle Infotainment Cyber Security Market Size

According to Reports Insights Consulting Pvt Ltd, The In Vehicle Infotainment Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 7.20 Billion by the end of the forecast period in 2033.

Key In Vehicle Infotainment Cyber Security Market Trends & Insights

The In Vehicle Infotainment (IVI) Cyber Security market is currently characterized by several pivotal trends, driven by the increasing complexity and connectivity of modern vehicles. Users are primarily concerned with understanding how evolving technologies like 5G, cloud integration, and advanced sensor systems are impacting vehicle security architectures. There is significant interest in the proactive measures being adopted by original equipment manufacturers (OEMs) and Tier 1 suppliers to mitigate new and sophisticated cyber threats, moving beyond reactive patching to predictive and preventive security solutions.

Furthermore, the market is witnessing a strong emphasis on end-to-end security, encompassing not just the IVI system itself but also its integration with the broader vehicle network, external cloud services, and mobile applications. Users frequently inquire about the efficacy of over-the-air (OTA) updates for security patches and new feature deployments, alongside the challenges associated with managing software supply chain vulnerabilities. The growing regulatory landscape across different regions is also a key area of interest, as consumers and industry players seek clarity on compliance requirements and their influence on product development and market dynamics.

- Proliferation of Connected Car Services: Increased reliance on cloud-based services and vehicle-to-everything (V2X) communication.

- Advanced Threat Detection Systems: Integration of AI and machine learning for real-time anomaly detection and intrusion prevention.

- Over-the-Air (OTA) Updates for Security: Essential for rapid deployment of patches and software enhancements.

- Regulatory Compliance and Standardization: Growing demand for common security standards and certifications across regions.

- Supply Chain Security: Focus on securing the entire software and hardware development lifecycle from external threats.

- Data Privacy Concerns: Enhanced measures to protect personal and vehicle operational data gathered by IVI systems.

- Integration of Automotive Ethernet: High-bandwidth communication protocols increasing attack surface and demanding robust security.

AI Impact Analysis on In Vehicle Infotainment Cyber Security

User queries regarding the impact of Artificial Intelligence (AI) on In Vehicle Infotainment (IVI) Cyber Security often revolve around its dual nature: AI as a powerful tool for defense and as a potential enabler for advanced cyberattacks. There is a strong interest in how AI can enhance threat detection capabilities, moving from signature-based systems to behavior-based and predictive analytics that can identify novel attack vectors in real-time. Users want to understand the efficacy of AI in processing vast amounts of telematics data to identify anomalies and potential security breaches before they escalate, thereby bolstering the overall resilience of IVI systems.

Conversely, concerns are frequently raised about the vulnerabilities inherent in AI systems themselves. Questions often arise about the security of AI models against adversarial attacks, data poisoning, and model manipulation, which could lead to misinterpretations or bypasses of security protocols. Furthermore, the role of AI in autonomous driving systems is closely linked to IVI security, as any compromise in one could affect the safety-critical functions of the other. The market anticipates significant investments in developing AI-powered security solutions that can not only detect sophisticated threats but also protect the integrity and trustworthiness of the AI components embedded within vehicles.

- Enhanced Threat Detection: AI algorithms rapidly analyze data patterns to identify and predict cyber threats.

- Predictive Security Analytics: Machine learning models anticipate potential vulnerabilities and proactive defense strategies.

- Autonomous Driving Security Integration: AI's role in securing ADAS and other critical vehicle functions through IVI.

- AI-Powered Attack Vectors: Risk of AI being used by malicious actors for sophisticated and automated cyberattacks.

- Adaptive Security Measures: AI enabling systems to learn and adapt defenses against evolving threat landscapes.

- Data Anomaly Detection: AI for identifying unusual behavior in vehicle networks and IVI systems.

- Cybersecurity for AI Models: Need to secure the AI models themselves from tampering and adversarial attacks.

Key Takeaways In Vehicle Infotainment Cyber Security Market Size & Forecast

The In Vehicle Infotainment Cyber Security market is poised for substantial expansion, a key takeaway that resonates with industry stakeholders and consumers alike. The rapid integration of advanced connectivity features, coupled with the increasing sophistication of cyber threats targeting automotive systems, underscores the critical need for robust security solutions. Users frequently inquire about the underlying factors driving this significant growth, often pointing to the proliferation of connected car services, the development of autonomous driving technologies, and the ever-present demand for a secure and seamless user experience within vehicles.

Another crucial insight is the shift from a reactive to a proactive cybersecurity posture within the automotive industry. The market forecast indicates a sustained focus on preventative measures, including embedded security, secure boot processes, and continuous monitoring, rather than merely addressing vulnerabilities post-exploit. This proactive approach is essential for maintaining consumer trust and adhering to stringent regulatory requirements globally. The market's growth trajectory highlights not only the increasing awareness of cyber risks but also the substantial investment being directed towards securing the complex digital ecosystem of modern automobiles.

- Significant Market Expansion: Driven by increased vehicle connectivity and digitization.

- Rising Investment in Automotive Cybersecurity: OEMs and suppliers are prioritizing security infrastructure.

- Proactive Security Mandate: Shift towards embedded, preventative security measures.

- Convergence of Technologies: IVI security increasingly intertwined with ADAS and autonomous driving systems.

- Regulatory Influence: Government mandates and industry standards are shaping market development.

- Consumer Demand for Security: Growing awareness among consumers regarding vehicle data privacy and safety.

In Vehicle Infotainment Cyber Security Market Drivers Analysis

The In Vehicle Infotainment Cyber Security market is significantly propelled by the accelerated adoption of connected vehicle technologies and the subsequent expansion of the digital attack surface within automobiles. As modern vehicles become more sophisticated, integrating extensive infotainment systems, telematics, and advanced driver-assistance features, the imperative for robust cybersecurity solutions intensifies. This transformation creates a fertile ground for cyber threats, compelling manufacturers and consumers to invest heavily in protective measures, thereby fueling market growth.

Furthermore, the evolving regulatory landscape, particularly in regions such as Europe and North America, plays a critical role in mandating and standardizing cybersecurity practices in the automotive sector. Compliance with regulations like UNECE WP.29 demands a systemic approach to vehicle cybersecurity throughout the entire product lifecycle, pushing OEMs to integrate security from the design phase onwards. This regulatory pressure, combined with a heightened consumer awareness regarding data privacy and vehicle safety, forms a powerful driver for the In Vehicle Infotainment Cyber Security market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Connectivity and Digitization of Vehicles | +5.2% | Global, particularly North America, Europe, Asia Pacific | Short-term to Long-term |

| Rising Sophistication of Cyber Threats and Attacks | +4.8% | Global | Short-term to Long-term |

| Stricter Regulatory Compliance and Standards (e.g., UNECE WP.29) | +4.0% | Europe, North America, Japan, South Korea | Mid-term |

| Integration of Advanced Driver-Assistance Systems (ADAS) and Autonomous Driving Features | +3.5% | North America, Europe, China | Mid-term to Long-term |

| Growing Consumer Awareness Regarding Data Privacy and Vehicle Security | +1.2% | Global | Short-term to Mid-term |

In Vehicle Infotainment Cyber Security Market Restraints Analysis

Despite the robust growth drivers, the In Vehicle Infotainment Cyber Security market faces significant restraints that can impede its expansion. One primary challenge is the substantial cost associated with implementing comprehensive cybersecurity measures, particularly for smaller automotive manufacturers or those with legacy vehicle architectures. Integrating sophisticated security hardware and software from the ground up, and maintaining continuous security updates throughout a vehicle's lengthy lifecycle, requires considerable financial investment and technical expertise, which can be a barrier to widespread adoption.

Another critical restraint stems from the lack of universal standardization across the global automotive industry. While some regional regulations are emerging, a globally harmonized set of cybersecurity standards for IVI systems is still evolving. This fragmented regulatory landscape complicates the development of unified security solutions, potentially leading to increased development costs and slower market penetration as manufacturers struggle to meet diverse compliance requirements across different jurisdictions. The complexity of integrating security into highly distributed and diverse vehicle electronic architectures also presents a significant technical hurdle.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implementing and Maintaining Robust Cybersecurity Solutions | -2.5% | Global, particularly emerging markets | Short-term to Mid-term |

| Lack of Universal Standardization and Harmonized Regulations | -1.8% | Global | Mid-term |

| Complexity of Vehicle Electronic Architectures and Legacy System Integration | -1.5% | Global | Short-term to Mid-term |

| Shortage of Skilled Cybersecurity Professionals in the Automotive Sector | -1.0% | North America, Europe, Asia Pacific | Long-term |

In Vehicle Infotainment Cyber Security Market Opportunities Analysis

The In Vehicle Infotainment Cyber Security market presents numerous opportunities for growth and innovation, particularly with the increasing convergence of automotive and IT sectors. The continuous expansion of connected services, such as subscription-based features, remote diagnostics, and entertainment platforms, opens new avenues for security providers to offer advanced, tailored solutions. This includes cloud-based security services, threat intelligence platforms, and robust authentication mechanisms that protect sensitive user data and vehicle functionality, creating recurring revenue streams and deepening market penetration.

Furthermore, the advent of autonomous driving technologies and the growing ecosystem of smart city infrastructure represent significant long-term opportunities. As vehicles become more autonomous and communicate extensively with their environment, the scope of cybersecurity extends beyond the vehicle itself to external networks and infrastructure. This necessitates the development of sophisticated, real-time threat detection and response systems that can ensure the safety and integrity of these highly interconnected systems, fostering innovation in areas like V2X security and over-the-air firmware updates with cryptographic validation. Partnerships between automotive OEMs and specialized cybersecurity firms are also emerging as a key strategy to capitalize on these evolving opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Connected Car Services and Subscription Models | +4.0% | Global | Short-term to Mid-term |

| Development of Autonomous Driving and V2X Communication Technologies | +3.5% | North America, Europe, China | Mid-term to Long-term |

| Post-sales Security Updates and Lifecycle Management Solutions | +2.8% | Global | Short-term to Long-term |

| Strategic Partnerships and Collaborations between OEMs and Cybersecurity Vendors | +2.0% | Global | Short-term to Mid-term |

| Emergence of New Cybersecurity Technologies (e.g., Quantum Cryptography, Blockchain for Security) | +1.5% | North America, Europe, Asia Pacific | Long-term |

In Vehicle Infotainment Cyber Security Market Challenges Impact Analysis

The In Vehicle Infotainment Cyber Security market faces persistent challenges rooted in the dynamically evolving nature of cyber threats and the inherent complexity of automotive systems. The constantly changing threat landscape requires continuous adaptation and updates to security solutions, often outpacing the traditional development cycles of the automotive industry. This ongoing battle against new attack vectors, zero-day exploits, and advanced persistent threats demands significant research and development investments and agile security deployment strategies, which can be difficult to implement across diverse vehicle models and platforms.

Another significant challenge is managing the vast and intricate software supply chain that contributes to modern IVI systems. Components sourced from various vendors, each with their own security postures, introduce potential vulnerabilities at multiple points. Ensuring the integrity and security of every piece of software and hardware throughout the supply chain is a monumental task. Furthermore, balancing robust security measures with user experience and system performance remains a delicate act; overly intrusive security protocols can deter users or hinder the functionality of infotainment systems, posing a persistent dilemma for developers and manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving and Sophisticated Cyber Threat Landscape | -2.8% | Global | Short-term to Long-term |

| Managing Software Supply Chain Risks and Third-Party Vulnerabilities | -2.2% | Global | Mid-term |

| Balancing Security Measures with User Experience and System Performance | -1.7% | Global | Short-term |

| Complexity of Real-time Threat Response and Incident Management | -1.3% | Global | Short-term to Mid-term |

| Integration with Legacy Systems and Varying Vehicle Lifespans | -1.0% | Global | Mid-term to Long-term |

In Vehicle Infotainment Cyber Security Market - Updated Report Scope

This report provides a comprehensive analysis of the In Vehicle Infotainment Cyber Security market, offering critical insights into market size, growth drivers, restraints, opportunities, and challenges. It delves into the technological advancements and strategic initiatives shaping the industry, providing a forward-looking perspective on market dynamics. The scope encompasses detailed segmentation analysis, regional highlights, and profiles of key industry players, ensuring a holistic view of the market landscape from 2019 through 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 7.20 Billion |

| Growth Rate | 18.7% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Argus Cyber Security, Harman International (a Samsung Company), Elektrobit (a Continental AG Company), NXP Semiconductors, Infineon Technologies AG, Symantec Corporation (a Broadcom Company), Trillium Secure Inc., Uptake Technologies Inc., Green Hills Software, Vector Informatik GmbH, SafeRide Technologies, Karamba Security, Irdeto (a MultiChoice Group Company), GuardKnox Cyber Technologies, Qualcomm Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The In Vehicle Infotainment Cyber Security market is meticulously segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed examination of market dynamics across various security types, reflecting the multi-layered approach required for robust vehicle protection. Furthermore, the categorization by application highlights the critical areas within IVI systems that demand specialized cybersecurity solutions, from essential telematics to advanced driver-assistance features, each presenting unique vulnerability profiles and security imperatives.

Moreover, segmenting the market by vehicle type, including passenger cars, commercial vehicles, and electric vehicles, enables an understanding of how distinct automotive categories influence security requirements and adoption rates. The component-based segmentation provides insights into the technological building blocks of IVI cybersecurity, such as dedicated hardware security modules, sophisticated software solutions, and comprehensive network defense systems. This granular analysis facilitates targeted strategy development and identifies specific growth pockets within the broader market.

- By Security Type:

- Hardware Security

- Software Security

- Network Security

- By Application:

- Telematics

- Navigation

- Entertainment

- Advanced Driver-Assistance Systems (ADAS)

- By Vehicle Type:

- Passenger Car

- Commercial Vehicle

- Electric Vehicle

- By Component:

- Security Processing Unit (SPU)

- Security Gateways

- Intrusion Detection and Prevention Systems (IDPS)

- Threat Intelligence Platforms

- Secure Boot and Firmware Over-the-Air (FOTA)

- Endpoint Security Solutions

Regional Highlights

- North America: Expected to hold a significant market share due to early adoption of advanced connected car technologies, a strong presence of major automotive OEMs and technology providers, and increasing regulatory pressure for vehicle cybersecurity. High consumer awareness regarding data privacy and security also drives demand.

- Europe: Demonstrates robust growth, largely propelled by stringent regulations such as UNECE WP.29, which mandates cybersecurity management systems for vehicles. The region's focus on electric vehicle adoption and smart mobility initiatives further boosts the need for advanced IVI cybersecurity.

- Asia Pacific (APAC): Emerging as the fastest-growing market, driven by rapidly increasing vehicle production and sales, significant investments in connected car infrastructure, and the growing prominence of electric vehicles, particularly in countries like China, Japan, and South Korea. Government initiatives promoting smart transportation also play a crucial role.

- Latin America: Witnessing gradual growth with increasing penetration of connected vehicles and the establishment of local manufacturing facilities by global automotive players. Market expansion is supported by improving economic conditions and a rising middle-class demographic.

- Middle East and Africa (MEA): Shows nascent but promising growth, driven by government initiatives to diversify economies through smart city projects and advancements in automotive technology. Increased adoption of premium vehicles with advanced infotainment systems contributes to market demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the In Vehicle Infotainment Cyber Security Market.- Argus Cyber Security

- Harman International (a Samsung Company)

- Elektrobit (a Continental AG Company)

- NXP Semiconductors

- Infineon Technologies AG

- Symantec Corporation (a Broadcom Company)

- Trillium Secure Inc.

- Uptake Technologies Inc.

- Green Hills Software

- Vector Informatik GmbH

- SafeRide Technologies

- Karamba Security

- Irdeto (a MultiChoice Group Company)

- GuardKnox Cyber Technologies

- Qualcomm Technologies Inc.

- Bosch GmbH

- Continental AG

- DENSO Corporation

- Hyundai Mobis

- Panasonic Corporation

Frequently Asked Questions

Analyze common user questions about the In Vehicle Infotainment Cyber Security market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is In Vehicle Infotainment (IVI) Cyber Security?

IVI Cyber Security refers to the measures and technologies implemented to protect a vehicle's infotainment system, and its connected components, from unauthorized access, manipulation, or damage by cyber threats. This includes securing data, preventing system compromise, and ensuring the safe operation of connected features like navigation, entertainment, and telematics.

Why is In Vehicle Infotainment Cyber Security important?

It is crucial because IVI systems are increasingly connected and integrated with critical vehicle functions, making them potential entry points for cyberattacks. A breach could lead to data theft, privacy violations, or even enable malicious actors to gain control over vehicle systems, posing serious safety risks to occupants and others on the road.

What are the main types of cyber threats targeting IVI systems?

Common threats include malware injection, denial-of-service (DoS) attacks, remote exploitation of software vulnerabilities, unauthorized access through unsecured Wi-Fi or Bluetooth connections, data tampering, and phishing attempts. These attacks can target the IVI unit itself, connected mobile devices, or cloud-based services.

How are car manufacturers addressing IVI cyber security?

Manufacturers are adopting a multi-layered approach, incorporating secure boot processes, hardware security modules (HSMs), intrusion detection/prevention systems (IDPS), secure over-the-air (OTA) update mechanisms, and secure communication protocols. They are also establishing security operations centers (SOCs) for continuous monitoring and incident response, and adhering to international cybersecurity regulations like UNECE WP.29.

What does the future hold for In Vehicle Infotainment Cyber Security?

The future involves increased integration of AI and machine learning for predictive threat detection, the adoption of advanced cryptographic solutions, and a stronger emphasis on end-to-end security across the entire vehicle lifecycle and supply chain. As autonomous driving and V2X communication expand, cybersecurity will become even more critical and complex, requiring dynamic, adaptive, and proactive defense strategies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted