In Building Wireless Market

In Building Wireless Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700876 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

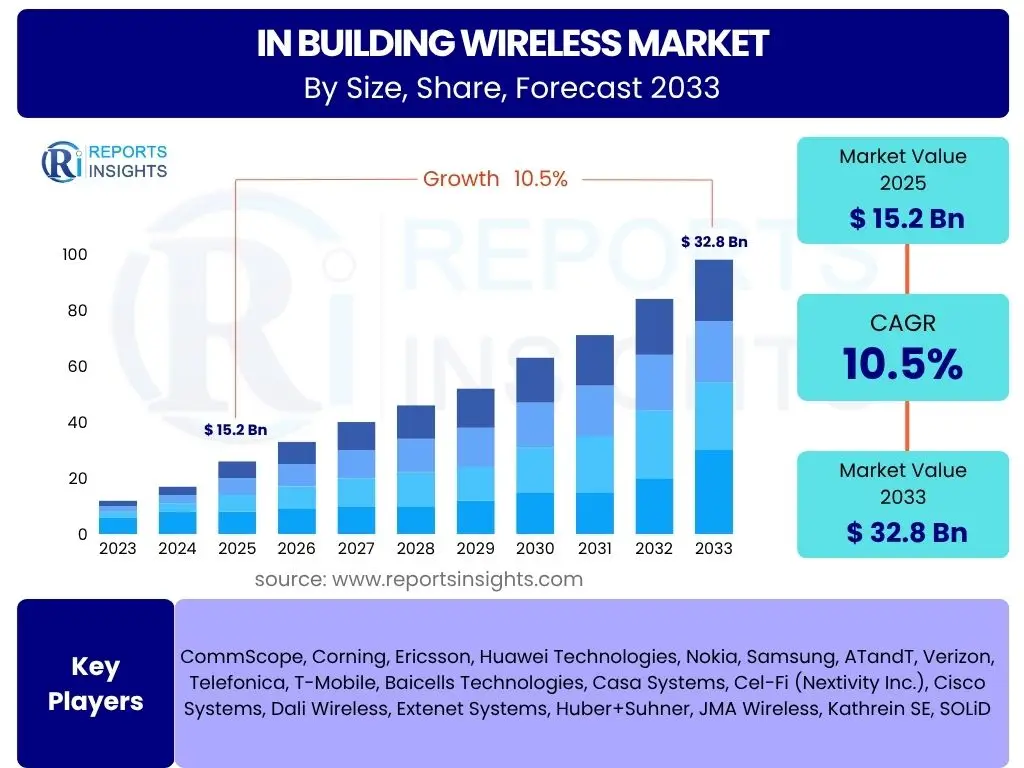

In Building Wireless Market Size

According to Reports Insights Consulting Pvt Ltd, The In Building Wireless Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 32.8 Billion by the end of the forecast period in 2033.

This robust growth trajectory is primarily driven by the escalating demand for seamless and high-speed connectivity within enclosed structures. As digital transformation accelerates across various sectors, the necessity for reliable indoor wireless coverage has become paramount, spanning from corporate offices and healthcare facilities to educational institutions and public venues. The proliferation of smart devices, Internet of Things (IoT) applications, and bandwidth-intensive services necessitates a resilient and pervasive in-building wireless infrastructure, ensuring consistent access to critical data and communication channels.

The market expansion is further supported by the global rollout of 5G networks, which promises unprecedented speeds, ultra-low latency, and massive connectivity. While outdoor 5G deployments are progressing, the inherent challenges of signal penetration through building materials underscore the critical role of dedicated in-building wireless solutions. These solutions are essential for extending the benefits of 5G indoors, thereby unlocking new use cases for enterprises and consumers alike, and contributing significantly to the overall market valuation.

Key In Building Wireless Market Trends & Insights

Users frequently inquire about the evolving landscape of the In Building Wireless market, seeking to understand the significant technological advancements and strategic shifts that are shaping its future. Common questions revolve around the adoption of next-generation technologies, the shift in deployment models, and the increasing integration of in-building solutions with broader smart infrastructure initiatives. The market is currently experiencing dynamic transformations driven by the confluence of advanced connectivity requirements, digital transformation imperatives, and the relentless pursuit of enhanced user experiences within enclosed environments.

One prominent trend is the widespread adoption of 5G technologies indoors, extending the capabilities of this high-speed, low-latency network beyond outdoor areas. This is complemented by the growing interest in private 5G networks, which offer enterprises dedicated, secure, and customizable wireless infrastructure for mission-critical applications. Furthermore, the convergence of Wi-Fi and cellular technologies is becoming increasingly prevalent, moving towards a unified and seamless indoor connectivity experience. This convergence often involves solutions that intelligently manage traffic across different wireless protocols to optimize performance and resource utilization.

Another key insight is the increasing demand for neutral host models and as-a-service offerings. Building owners and venue operators are exploring these models to reduce capital expenditure and simplify network management, opting for third-party providers to deploy and manage in-building wireless infrastructure. This shift democratizes access to advanced connectivity and facilitates faster deployment in diverse settings. The integration of in-building wireless systems with IoT platforms and smart building management systems also represents a significant trend, enabling advanced functionalities such as occupancy sensing, predictive maintenance, and energy optimization, thereby enhancing operational efficiency and sustainability within modern structures.

- Proliferation of 5G indoor deployments across various sectors.

- Growing adoption of private 5G networks for enterprise-specific applications.

- Convergence of Wi-Fi and cellular technologies for unified indoor connectivity.

- Increased preference for neutral host and 'as-a-Service' deployment models.

- Enhanced integration of in-building wireless with IoT and smart building systems for operational efficiency.

- Emphasis on sustainability and energy efficiency in network infrastructure design.

AI Impact Analysis on In Building Wireless

User queries regarding the impact of Artificial Intelligence (AI) on the In Building Wireless market often center on how AI can enhance network performance, automate operations, improve security, and create new service opportunities. Users are keen to understand if AI can address the complexities of managing diverse wireless technologies and ever-increasing traffic demands within confined spaces. The primary themes emerging from these inquiries include the potential for AI to optimize network resources, facilitate predictive maintenance, and personalize user experiences, transforming the way in-building wireless networks are designed, deployed, and managed.

AI's influence on in-building wireless is profound, primarily through its capacity to enable intelligent network management and optimization. AI algorithms can analyze vast amounts of network data in real-time, predicting traffic patterns, identifying potential bottlenecks, and dynamically allocating resources to ensure optimal performance and coverage. This proactive approach minimizes downtime and enhances the overall quality of service for users. Furthermore, AI-driven analytics can significantly improve network planning and design, helping identify ideal locations for access points and optimizing antenna configurations for maximum efficiency and reduced interference within complex indoor environments.

Beyond optimization, AI contributes to enhanced security and personalized user experiences within in-building wireless networks. AI-powered security solutions can detect anomalous behaviors and potential threats more effectively, providing real-time alerts and mitigating risks. For users, AI can enable context-aware services, such as personalized wayfinding, targeted promotions in retail environments, or optimized room temperature control in smart offices, all leveraging the robust connectivity provided by the in-building wireless infrastructure. The integration of AI also streamlines operational processes, leading to cost efficiencies and more agile network management strategies.

- Enhanced network optimization through real-time traffic analysis and resource allocation.

- Predictive maintenance and fault detection for improved network reliability and uptime.

- Automated network management and orchestration, reducing operational complexity.

- Improved security posture through AI-powered threat detection and anomaly identification.

- Personalized user experiences and context-aware services leveraging location intelligence.

- Optimized energy consumption and sustainability through intelligent resource management.

Key Takeaways In Building Wireless Market Size & Forecast

Users frequently ask for the most critical insights derived from the In Building Wireless market size and forecast, aiming to grasp the overarching implications for investment, strategic planning, and technological development. Common questions often focus on the longevity of growth, the primary factors sustaining it, and the essential considerations for stakeholders looking to capitalize on market opportunities. The consensus suggests a resilient and expanding market driven by fundamental connectivity needs and evolving technological landscapes, emphasizing the strategic importance of robust in-building infrastructure.

A central takeaway is the sustained, high-growth trajectory of the In Building Wireless market, underpinned by an incessant global demand for high-speed, reliable connectivity across diverse indoor environments. This growth is not merely incremental but represents a foundational shift towards pervasive digital enablement within all types of structures, from commercial complexes to residential units. The market's resilience is further bolstered by the essential nature of connectivity for modern operations, digital transformation initiatives, and the proliferation of IoT devices, ensuring continued investment and innovation.

Another crucial insight is the increasing complexity and technological sophistication required for effective in-building solutions. The seamless integration of 5G, Wi-Fi 6/7, and private network capabilities is becoming critical for addressing contemporary connectivity demands. Stakeholders must prioritize scalable, flexible, and future-proof architectures that can adapt to evolving standards and user expectations. Furthermore, strategic partnerships and collaboration among technology providers, building owners, and service providers will be instrumental in overcoming deployment challenges and accelerating market penetration, solidifying the market's robust long-term outlook.

- Sustained high growth anticipated due to indispensable demand for indoor connectivity.

- 5G and private network deployments are pivotal drivers for future market expansion.

- Technological convergence and integration are essential for comprehensive solutions.

- Strategic partnerships and flexible business models (e.g., neutral host) are key enablers.

- Continuous innovation in network optimization and management will define competitive advantage.

In Building Wireless Market Drivers Analysis

The In Building Wireless market is primarily propelled by a confluence of factors emphasizing the increasing reliance on seamless and high-performance connectivity within various enclosed environments. The escalating demand for ubiquitous and reliable network access, driven by the proliferation of smart devices and bandwidth-intensive applications, forms the fundamental catalyst. This is further amplified by the imperative for enterprises to undergo digital transformation, leveraging advanced wireless solutions to enhance operational efficiency, improve customer experiences, and foster innovation. The global rollout of 5G technology also serves as a significant driver, as its full potential can only be realized with robust indoor coverage, necessitating dedicated in-building wireless infrastructure to penetrate building materials effectively and deliver promised speeds and low latency.

Moreover, the growth of the Internet of Things (IoT) ecosystem and the emergence of smart building initiatives are creating substantial demand for interconnected devices and data exchange, requiring a robust and adaptable in-building wireless foundation. These applications, ranging from smart energy management and security systems to asset tracking and environmental monitoring, rely heavily on pervasive and secure indoor connectivity. Government initiatives and regulatory frameworks supporting smart city development and digital infrastructure upgrades also contribute significantly to market expansion by incentivizing the deployment of advanced in-building wireless solutions in public and private sectors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Demand for Seamless Connectivity | +1.8% | Global | Long-term |

| Proliferation of Smart Devices and IoT | +1.5% | Global | Mid-term to Long-term |

| Global 5G Network Rollout and Adoption | +2.0% | North America, Asia Pacific, Europe | Mid-term |

| Enterprise Digital Transformation Initiatives | +1.2% | Global | Mid-term |

In Building Wireless Market Restraints Analysis

Despite the strong growth prospects, the In Building Wireless market faces several significant restraints that could impede its expansion. One primary concern is the substantial capital expenditure and operational costs associated with deploying and maintaining complex in-building wireless systems. These costs can be prohibitive for smaller organizations or building owners, especially when considering the need for specialized equipment, skilled labor for installation, and ongoing management. Furthermore, the diverse range of building materials and architectural designs can complicate deployment, requiring customized solutions that further increase costs and implementation timelines.

Another considerable restraint is the intricate regulatory environment and challenges related to spectrum availability and management. Navigating various national and regional regulations, licensing requirements, and spectrum allocation policies can be complex and time-consuming, delaying project approvals and deployments. Interoperability issues among different wireless technologies and vendor solutions also pose a challenge, leading to potential integration complexities and performance inconsistencies. Additionally, the increasing focus on cybersecurity concerns in interconnected environments means that securing in-building wireless networks against sophisticated threats adds another layer of complexity and cost, requiring continuous investment in robust security measures and protocols.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Deployment and Maintenance Costs | -0.7% | Global | Ongoing |

| Complex Regulatory Environment and Spectrum Challenges | -0.5% | Global (varies by region) | Ongoing |

| Interoperability and Integration Issues | -0.4% | Global | Short-term to Mid-term |

| Cybersecurity Concerns and Data Privacy Risks | -0.3% | Global | Ongoing |

In Building Wireless Market Opportunities Analysis

The In Building Wireless market is rich with opportunities stemming from evolving technological landscapes and burgeoning connectivity demands. A significant opportunity lies in the burgeoning market for private 5G networks, offering enterprises dedicated, secure, and customizable wireless infrastructure for mission-critical applications within their premises. This allows for enhanced control, improved security, and optimized performance for industrial IoT, automation, and real-time communication needs, particularly in sectors such as manufacturing, logistics, and healthcare. The demand for such tailored solutions is poised to accelerate as more industries recognize the benefits of private cellular deployments over traditional Wi-Fi in specific operational contexts.

Furthermore, the increasing integration of in-building wireless systems with smart building platforms and the broader Internet of Things (IoT) ecosystem presents a vast avenue for growth. This convergence enables advanced functionalities like intelligent energy management, space optimization, predictive maintenance, and enhanced security, transforming buildings into truly intelligent environments. The emergence of neutral host models and 'as-a-service' offerings also provides a compelling opportunity, allowing property owners and venue operators to deploy advanced wireless solutions without significant upfront capital investment, thereby democratizing access to high-performance indoor connectivity and accelerating market penetration across various building types. These models foster collaboration between service providers and infrastructure owners, creating win-win scenarios for deployment and management.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Private 5G Networks | +1.5% | Global, particularly developed economies | Mid-term to Long-term |

| Integration with Smart Building and IoT Ecosystems | +1.2% | Global | Mid-term |

| Rise of Neutral Host and Wireless-as-a-Service Models | +1.0% | North America, Europe, Asia Pacific | Mid-term |

| Expansion into Underserved Verticals (e.g., Healthcare, Education) | +0.8% | Emerging Markets, Specific Developed Regions | Long-term |

In Building Wireless Market Challenges Impact Analysis

The In Building Wireless market, while robust, confronts several challenges that demand strategic responses from stakeholders. A primary challenge involves ensuring ubiquitous and high-quality coverage across a myriad of complex and architecturally diverse indoor environments. Signal propagation issues due to varied building materials, structural designs, and constantly changing indoor layouts necessitate sophisticated planning and custom deployments, which can be both time-consuming and expensive. Achieving consistent performance for all users, regardless of their location within a large building or dense urban structure, remains a significant technical hurdle.

Another critical challenge is the persistent shortage of skilled professionals capable of designing, deploying, and maintaining advanced in-building wireless systems. The convergence of different technologies, such as cellular (DAS, small cells) and Wi-Fi, along with the integration of IoT and smart building systems, requires a diverse skill set that is currently in high demand. Moreover, the rapidly evolving technological landscape, characterized by new standards like Wi-Fi 7 and advancements in 5G, means that existing infrastructure can quickly become outdated. This necessitates continuous upgrades and investment, posing a financial burden and a strategic challenge for ensuring long-term relevance and competitiveness in the market. Managing the increasing volume of data traffic and ensuring efficient spectrum utilization within confined spaces also presents ongoing operational complexities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Ubiquitous and High-Quality Coverage | -0.6% | Global | Ongoing |

| Skilled Workforce Shortage and Training Needs | -0.5% | Global | Ongoing |

| Rapid Technological Obsolescence and Upgrade Cycles | -0.4% | Global | Ongoing |

| Managing Complex Interoperability and Ecosystem Integration | -0.3% | Global | Ongoing |

In Building Wireless Market - Updated Report Scope

This report provides a comprehensive analysis of the global In Building Wireless Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape from 2019 to 2033. It examines the market size, growth drivers, restraints, opportunities, and challenges, incorporating the latest technological advancements, including the impact of 5G and Artificial Intelligence. The scope encompasses various components, technologies, applications, and end-uses, presenting a holistic view of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 32.8 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CommScope, Corning, Ericsson, Huawei Technologies, Nokia, Samsung, ATandT, Verizon, Telefonica, T-Mobile, Baicells Technologies, Casa Systems, Cel-Fi (Nextivity Inc.), Cisco Systems, Dali Wireless, Extenet Systems, Huber+Suhner, JMA Wireless, Kathrein SE, SOLiD |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The In Building Wireless Market is comprehensively segmented to provide a detailed understanding of its diverse facets, enabling precise market analysis and strategic planning. This segmentation considers various aspects, including the components that comprise these systems, the underlying technologies utilized, the specific applications they serve across different industries, the end-user demographics, and the spectrum bands they operate within. This multi-dimensional approach helps to delineate the market's structure, identify key growth areas, and assess the performance of different segments, reflecting the technological evolution and varied connectivity demands across global markets.

Understanding these segments is crucial for stakeholders to tailor their product offerings, service strategies, and market entry approaches effectively. For instance, the Hardware component segment is expected to continue its dominance due to the essential nature of physical infrastructure, while the Services segment is projected for rapid growth driven by the increasing complexity of deployments and the trend towards managed services. Similarly, the commercial and public venues applications are significant contributors to market revenue, fueled by the demand for high-density user connectivity, whereas industrial applications are emerging rapidly with the rise of private networks for IoT and automation.

- By Component:

- Hardware: Distributed Antenna Systems (DAS), Small Cells, Repeaters, Antennas, Cables & Connectors, Fiber Optic Solutions

- Software: Network Management Systems (NMS), Orchestration Software, Network Analytics & Optimization Tools, Security Software

- Services: Consulting & Design, System Integration & Installation, Maintenance & Support, Managed Services

- By Technology:

- Distributed Antenna Systems (DAS): Passive DAS, Active DAS, Hybrid DAS

- Small Cells: Femtocells, Picocells, Microcells

- Wi-Fi: Wi-Fi 6/6E, Wi-Fi 7, Earlier Wi-Fi Standards

- Private LTE/5G

- By Application:

- Commercial: Corporate Offices, Retail Spaces, Hospitality (Hotels, Restaurants), Shopping Malls

- Residential: Multi-Dwelling Units (MDUs), Smart Homes

- Industrial: Manufacturing Plants, Warehouses, Logistics Centers, Oil & Gas

- Public Venues: Stadiums, Arenas, Airports, Train Stations, Convention Centers, Exhibition Halls

- Healthcare: Hospitals, Clinics, Medical Facilities

- Education: Universities, Schools, Libraries

- Government: Government Buildings, Public Safety Agencies

- By End-Use:

- Enterprise

- Residential

- Government & Public Safety

- Healthcare & Education

- By Spectrum Band:

- Sub-6 GHz

- mmWave

Regional Highlights

The global In Building Wireless Market exhibits distinct growth patterns and maturity levels across different geographical regions, influenced by varying technological adoption rates, regulatory landscapes, and investment capacities. Understanding these regional dynamics is crucial for market participants to formulate targeted strategies and capitalize on localized opportunities. Each region presents a unique set of drivers and challenges, contributing to the overall global market trajectory.

- North America: This region holds a significant share of the In Building Wireless market, driven by early adoption of advanced wireless technologies, extensive deployment of 5G networks, and a strong focus on digital transformation across enterprises. The presence of major technology providers and a high demand for seamless connectivity in commercial, public, and residential buildings contributes to its leading position. Investments in smart cities and critical infrastructure upgrades also bolster market growth in countries like the United States and Canada.

- Europe: Europe is a substantial market for In Building Wireless solutions, characterized by stringent regulatory frameworks, increasing demand for reliable indoor connectivity in smart cities, and ongoing 5G rollouts. Countries like Germany, the UK, and France are actively investing in enhancing indoor coverage, particularly in commercial properties, healthcare facilities, and public transportation hubs. The region also shows a growing interest in private cellular networks for industrial applications, supporting continued market expansion.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market for In Building Wireless, fueled by rapid urbanization, significant investments in digital infrastructure, and the widespread adoption of 5G across emerging economies like China, India, Japan, and South Korea. The immense population density in urban areas, coupled with a booming manufacturing sector and expanding commercial real estate, creates a massive demand for robust indoor wireless solutions. Government initiatives supporting smart factories and smart cities are also key drivers.

- Latin America: This region is experiencing steady growth in the In Building Wireless market, driven by increasing smartphone penetration, expanding broadband infrastructure, and a growing need for improved indoor connectivity in commercial and residential developments. While still in nascent stages compared to developed markets, countries like Brazil and Mexico are witnessing increased investments in wireless infrastructure to address connectivity gaps and support digital inclusion.

- Middle East and Africa (MEA): The MEA region is demonstrating strong potential, primarily influenced by ambitious national visions for digital transformation, smart city projects, and significant investments in telecommunications infrastructure, particularly in the GCC countries. The construction of new commercial complexes, mega-events, and tourist attractions demands high-performance in-building wireless solutions. However, diverse economic conditions and geopolitical factors can influence the pace of adoption across different countries in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the In Building Wireless Market.- CommScope

- Corning

- Ericsson

- Huawei Technologies

- Nokia

- Samsung

- ATandT

- Verizon

- Telefonica

- T-Mobile

- Baicells Technologies

- Casa Systems

- Cel-Fi (Nextivity Inc.)

- Cisco Systems

- Dali Wireless

- Extenet Systems

- Huber+Suhner

- JMA Wireless

- Kathrein SE

- SOLiD

Frequently Asked Questions

What is the current market size and projected growth of the In Building Wireless market?

The In Building Wireless Market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 32.8 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 10.5% during the forecast period. This growth is driven by the escalating demand for seamless indoor connectivity and the global rollout of 5G networks.

What are the primary technologies driving growth in in-building wireless solutions?

Key technologies driving growth include Distributed Antenna Systems (DAS), Small Cells, and advanced Wi-Fi standards (Wi-Fi 6/6E/7). The emergence and increasing adoption of private LTE/5G networks are also significantly contributing to market expansion, offering dedicated and secure connectivity solutions for enterprises.

How does 5G impact in-building wireless connectivity?

5G significantly impacts in-building wireless by extending high-speed, low-latency, and massive connectivity benefits indoors. Due to 5G's higher frequencies and signal penetration challenges through building materials, dedicated in-building 5G solutions (like 5G-ready DAS and small cells) are crucial for delivering the full potential of 5G services within buildings, enabling new applications and enhancing user experiences.

What are the key challenges faced by the In Building Wireless market?

Major challenges include the high costs associated with deployment and maintenance of complex systems, navigating intricate regulatory environments and spectrum allocation issues, ensuring interoperability among diverse technologies, and addressing growing cybersecurity threats. Additionally, the shortage of skilled professionals and the rapid pace of technological obsolescence pose ongoing challenges.

Which regions are expected to show the most significant growth in this market?

The Asia Pacific (APAC) region is projected to exhibit the fastest growth, driven by rapid urbanization, extensive 5G deployments, and significant investments in digital infrastructure across countries like China, India, Japan, and South Korea. North America and Europe also maintain strong market positions due to advanced technological adoption and ongoing infrastructure upgrades.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted