Immunochemistry Analyzer Market

Immunochemistry Analyzer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700175 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

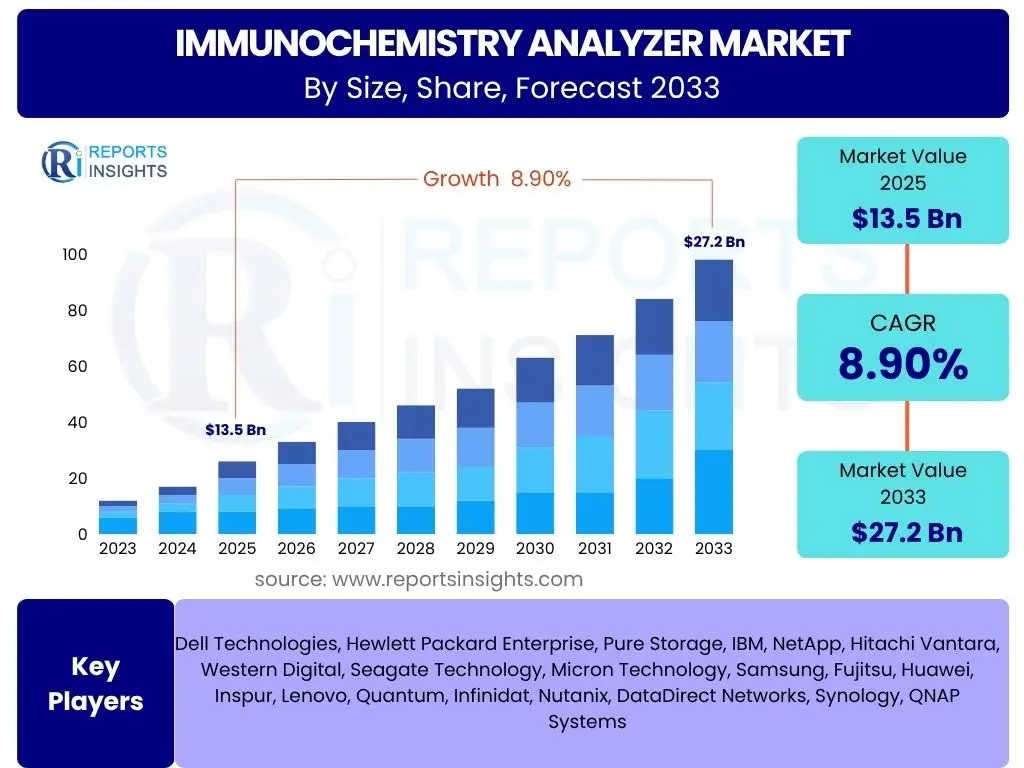

Immunochemistry Analyzer Market is projected to grow at a Compound annual growth rate (CAGR) of 8.9% between 2025 and 2033, current valued at USD 13.5 billion in 2025 and is projected to grow by USD 27.2 billion by 2033 the end of the forecast period.

Key Immunochemistry Analyzer Market Trends & Insights

The immunochemistry analyzer market is currently witnessing a transformative phase characterized by a convergence of technological advancements, evolving diagnostic needs, and a heightened focus on automation and efficiency. A pivotal trend involves the increasing integration of artificial intelligence and machine learning, which are enhancing the precision, speed, and analytical capabilities of these systems, moving beyond traditional immunoassay techniques towards more sophisticated diagnostic solutions. This shift is driven by the growing prevalence of chronic and infectious diseases globally, necessitating rapid and accurate diagnostic tools for effective disease management and patient outcomes. Furthermore, the market is seeing a surge in demand for point-of-care (POC) testing, driven by the need for immediate results and decentralized diagnostic services, especially in remote or underserved areas, contributing to a more accessible healthcare landscape.

- Automation and high-throughput systems adoption.

- Integration of Artificial Intelligence and Machine Learning for enhanced diagnostics.

- Expansion of point-of-care (POC) immunochemistry testing.

- Rising demand for multiplex assays and personalized medicine.

- Shift towards chemiluminescence immunoassay (CLIA) and electrochemiluminescence immunoassay (ECLIA) technologies.

- Focus on compact, user-friendly, and cost-effective analyzer designs.

- Increased application in oncology, infectious diseases, and endocrinology.

AI Impact Analysis on Immunochemistry Analyzer

Artificial intelligence (AI) is poised to significantly revolutionize the immunochemistry analyzer market, transcending mere data processing to enable more intelligent and autonomous diagnostic workflows. AI algorithms can optimize instrument calibration, predict potential malfunctions, and enhance quality control, thereby improving operational efficiency and reducing downtime in laboratories. Beyond operational improvements, AI’s analytical capabilities are crucial for interpreting complex immunological data, identifying subtle biomarkers, and correlating test results with clinical outcomes, leading to more accurate and timely diagnoses. This integration is particularly impactful in high-volume testing environments, where AI can manage vast datasets, identify patterns invisible to human analysis, and support the development of novel diagnostic assays, ultimately accelerating disease detection and prognosis.

- Enhanced precision and accuracy in test results.

- Automated data analysis and interpretation for complex immunoassays.

- Predictive maintenance and optimized instrument performance.

- Accelerated biomarker discovery and assay development.

- Improved quality control and calibration processes.

- Reduced human error and increased throughput in laboratories.

- Personalized diagnostic insights through advanced data correlation.

Key Takeaways Immunochemistry Analyzer Market Size & Forecast

- The global immunochemistry analyzer market is projected to reach USD 27.2 billion by 2033.

- Anticipated growth rate stands at a robust CAGR of 8.9% from 2025 to 2033.

- Market expansion is driven by increasing prevalence of chronic and infectious diseases.

- Technological advancements, particularly in automation and AI, are key growth facilitators.

- Rising demand for early and accurate disease diagnosis fuels market size.

- North America and Europe currently dominate the market, with Asia Pacific exhibiting the fastest growth.

- Point-of-care testing is expected to significantly contribute to market expansion.

Immunochemistry Analyzer Market Drivers Analysis

The growth of the immunochemistry analyzer market is propelled by a confluence of critical factors, each contributing significantly to the expanding demand for advanced diagnostic solutions. A primary driver is the escalating global burden of chronic diseases such as cardiovascular disorders, diabetes, and various cancers, alongside the persistent threat of infectious diseases. These conditions necessitate frequent and accurate diagnostic testing, where immunochemistry analyzers play a crucial role in detecting specific biomarkers and pathogens, thereby enabling early diagnosis and effective disease management. Furthermore, the continuous advancements in immunoassay technologies, including the development of more sensitive, specific, and rapid test methodologies, are enhancing the utility and adoption of these analyzers across diverse healthcare settings, solidifying their indispensable role in modern diagnostics.

Another compelling driver is the demographic shift towards an aging global population, which inherently leads to a higher incidence of age-related illnesses requiring extensive diagnostic screenings. Geriatric populations are more susceptible to chronic conditions and complex health issues, driving the need for sophisticated analytical tools like immunochemistry analyzers to monitor disease progression, assess treatment efficacy, and support personalized healthcare approaches. Additionally, increasing healthcare expenditure in emerging economies and the expanding access to diagnostic services are creating new avenues for market penetration. Governments and private healthcare providers are investing heavily in upgrading diagnostic infrastructure, which includes the procurement of advanced immunochemistry analyzers, reflecting a global commitment to improving public health outcomes and diagnostic capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing prevalence of chronic and infectious diseases | +1.8% | Global, especially Asia Pacific and Africa | Long-term (5+ years) |

| Technological advancements in immunoassay techniques | +1.5% | North America, Europe | Mid-term (3-5 years) |

| Growing geriatric population worldwide | +1.2% | Europe, North America, Japan | Long-term (5+ years) |

| Rising demand for early and accurate disease diagnosis | +1.0% | Global | Short-term (1-3 years) |

| Increasing adoption of automation in clinical laboratories | +0.8% | North America, Europe, developed Asia Pacific | Mid-term (3-5 years) |

| Expanding healthcare infrastructure and expenditure in emerging economies | +0.7% | China, India, Brazil, Southeast Asia | Long-term (5+ years) |

| Shift towards personalized medicine and companion diagnostics | +0.6% | North America, Europe | Long-term (5+ years) |

Immunochemistry Analyzer Market Restraints Analysis

Despite robust growth prospects, the immunochemistry analyzer market faces several significant restraints that could impede its expansion. A primary limiting factor is the high initial cost associated with acquiring advanced immunochemistry analyzers, coupled with substantial ongoing maintenance and operational expenses. This financial barrier can be particularly prohibitive for small and medium-sized diagnostic laboratories, clinics, and healthcare facilities in developing regions, which may struggle to allocate the necessary capital investment. Furthermore, the specialized nature of these instruments often requires proprietary reagents and consumables, leading to vendor lock-in and inflated recurring costs, thereby increasing the overall cost of ownership and potentially deterring widespread adoption, especially in resource-constrained environments.

Another critical restraint is the stringent and complex regulatory landscape governing diagnostic devices, particularly in major markets. The lengthy and arduous approval processes, encompassing rigorous clinical trials and compliance with diverse national and international standards, can significantly delay market entry for new products and innovations. This regulatory burden not only increases development costs but also extends the time to market, posing challenges for manufacturers to rapidly introduce cutting-edge technologies. Moreover, the shortage of skilled professionals trained in operating and maintaining sophisticated immunochemistry analyzers, coupled with difficulties in accurate interpretation of complex test results, presents an operational bottleneck. This scarcity of expertise, particularly in remote or less developed areas, can limit the efficient utilization of these advanced instruments and impact the quality of diagnostic services, thereby acting as a significant impediment to market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost of advanced immunochemistry analyzers | -1.5% | Global, especially emerging economies | Long-term (5+ years) |

| Stringent regulatory approval processes | -1.0% | North America, Europe, regulated APAC | Mid-term (3-5 years) |

| Lack of skilled professionals and training infrastructure | -0.8% | Emerging markets, rural areas | Long-term (5+ years) |

| Reimbursement challenges and budget constraints | -0.7% | Europe, certain parts of Asia | Mid-term (3-5 years) |

| Potential for false positives/negatives in certain assays | -0.5% | Global | Short-term (1-3 years) |

| Intense competition leading to pricing pressures | -0.4% | Global, particularly competitive regions | Short-term (1-3 years) |

| Integration complexities with existing laboratory information systems | -0.3% | Global, especially large hospital networks | Mid-term (3-5 years) |

Immunochemistry Analyzer Market Opportunities Analysis

The immunochemistry analyzer market is ripe with substantial opportunities that promise to accelerate its growth trajectory in the coming years. One of the most significant opportunities lies in the increasing demand for point-of-care (POC) testing solutions. POC immunochemistry analyzers offer rapid results at the patient’s bedside or in community settings, reducing turnaround times and improving patient management, especially for critical conditions. This decentralization of testing services is particularly beneficial in rural or remote areas where access to centralized laboratories is limited, opening up vast untapped markets and enabling more proactive health monitoring and immediate clinical decision-making, thereby broadening the market's reach beyond traditional hospital settings.

Another burgeoning opportunity stems from the growing focus on personalized medicine and companion diagnostics. As healthcare shifts towards tailored treatments based on individual patient profiles, immunochemistry analyzers are becoming instrumental in identifying specific biomarkers that predict drug response or disease progression. This integration allows for more precise therapeutic interventions and reduces adverse drug reactions, enhancing treatment efficacy and patient safety. Furthermore, the expansion into emerging economies presents a colossal opportunity, driven by improving healthcare infrastructure, rising disposable incomes, and increasing awareness about early disease diagnosis. These regions, with their large populations and burgeoning healthcare markets, are investing heavily in advanced diagnostic technologies, creating a fertile ground for manufacturers to expand their footprint and introduce innovative immunochemistry solutions tailored to local needs and economic conditions, fostering significant long-term growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for point-of-care (POC) testing | +1.7% | Global, especially rural and remote areas | Long-term (5+ years) |

| Emergence of novel biomarkers and assays | +1.4% | North America, Europe, leading research hubs | Mid-term (3-5 years) |

| Expansion into untapped emerging markets | +1.2% | China, India, Brazil, Southeast Asia, Africa | Long-term (5+ years) |

| Integration with digital health platforms and AI | +1.0% | North America, Europe | Mid-term (3-5 years) |

| Increasing focus on personalized medicine and companion diagnostics | +0.9% | Global, especially developed healthcare systems | Long-term (5+ years) |

| Development of compact and automated systems for smaller labs | +0.7% | Global, particularly price-sensitive regions | Short-term (1-3 years) |

| Growing application in drug monitoring and therapeutic areas | +0.6% | Global, pharmaceutical industry | Mid-term (3-5 years) |

Immunochemistry Analyzer Market Challenges Impact Analysis

The immunochemistry analyzer market, while promising, grapples with several notable challenges that could potentially hinder its projected growth. One significant challenge is intense market competition, characterized by the presence of numerous established players and the constant entry of new innovators. This competitive landscape often leads to price wars and reduced profit margins, forcing manufacturers to continuously invest in research and development to differentiate their offerings, which can strain resources, particularly for smaller and newer market entrants. The need for constant innovation to stay ahead, coupled with pressure to offer cost-effective solutions, creates a delicate balancing act for market participants, impacting overall market profitability and sustainability.

Another critical challenge is the inherent complexity in standardizing test results across different analyzer platforms and manufacturers. Variations in assay methodologies, calibration procedures, and reagent formulations can lead to inconsistencies in results, which poses a significant hurdle for clinical interpretation and inter-laboratory comparisons. This lack of universal standardization can undermine diagnostic confidence and complicates the implementation of consistent treatment protocols, particularly for conditions requiring precise and comparable measurements over time or across different healthcare providers. Additionally, the rapid pace of technological obsolescence demands continuous investment in upgrading existing systems and developing new ones, which is a considerable financial burden for both manufacturers and end-users. Laboratories face the dilemma of investing in expensive new equipment while their current instruments may still be functional but are quickly becoming outdated, leading to difficult procurement decisions and affecting budget allocations, thereby presenting a persistent challenge to market progression.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense market competition and pricing pressure | -1.2% | Global | Short-term (1-3 years) |

| Complexity in standardizing test results across platforms | -0.9% | Global | Mid-term (3-5 years) |

| Rapid technological obsolescence requiring constant upgrades | -0.8% | Global, especially developed markets | Long-term (5+ years) |

| Supply chain disruptions for reagents and components | -0.6% | Global, particularly post-pandemic | Short-term (1-3 years) |

| Data security and privacy concerns with connected systems | -0.5% | Global | Mid-term (3-5 years) |

| Ethical considerations in AI-driven diagnostics | -0.4% | North America, Europe | Long-term (5+ years) |

| Resistance to adopting new technologies in established labs | -0.3% | Global, particularly older infrastructure | Mid-term (3-5 years) |

Immunochemistry Analyzer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the immunochemistry analyzer market, offering critical insights into its current dynamics and future projections. The scope encompasses detailed segmentation, competitive landscape assessment, and regional analyses, designed to equip stakeholders with actionable intelligence for strategic decision-making. The report leverages a robust research methodology, combining primary and secondary research to deliver accurate and reliable market estimations, trends, and growth opportunities. It aims to serve as an indispensable resource for businesses, investors, and healthcare professionals seeking a thorough understanding of the immunochemistry analyzer sector, enabling them to navigate market complexities and capitalize on emerging avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 billion |

| Market Forecast in 2033 | USD 27.2 billion |

| Growth Rate | 8.9% from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Company A, Company B, Company C, Company D, Company E, Company F, Company G, Company H, Company I, Company J, Company K, Company L, Company M, Company N, Company O, Company P, Company Q, Company R |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The immunochemistry analyzer market is meticulously segmented to provide a granular view of its various components and their respective growth trajectories, offering stakeholders a detailed understanding of key revenue streams and emerging opportunities. This comprehensive breakdown allows for targeted strategic planning and resource allocation across different product categories, application areas, and end-user segments, reflecting the multifaceted nature of the diagnostic industry.- Product Type:

This segment categorizes the market based on the different components that comprise immunochemistry analyzer systems. Instruments represent the core analytical devices, ranging from fully automated high-throughput systems crucial for large laboratories to semi-automated units suitable for smaller setups, each designed for specific volumes and operational needs. Reagents and consumables are indispensable for every test performed, encompassing a wide array of antibodies, antigens, calibrators, and controls that ensure assay accuracy and reliability. Software and services include the analytical platforms that process data, manage workflows, and provide essential support for instrument operation and maintenance, optimizing laboratory efficiency and diagnostic output.

- Instruments

- Automated Analyzers: These highly sophisticated systems offer complete automation from sample loading to result generation, ideal for high-volume testing in large hospitals and commercial diagnostic laboratories, minimizing manual intervention and reducing human error.

- Semi-automated Analyzers: Characterized by manual sample loading but automated analysis, these analyzers are suited for medium-throughput laboratories and specialized tests, balancing cost-efficiency with analytical capabilities.

- Reagents & Consumables

- Antibodies: Critical components that specifically bind to target analytes, forming the basis of immunological reactions in various assays.

- Antigens: Used in certain assays to detect specific antibodies in patient samples, crucial for infectious disease diagnosis and autoimmune conditions.

- Calibrators: Essential for establishing the analytical curve of an assay, ensuring accurate quantitative measurement of analytes.

- Controls: Used for monitoring the performance and accuracy of the immunochemistry analyzer and its reagents, vital for quality assurance.

- Others: Includes buffers, wash solutions, reaction vessels, and other disposable materials necessary for the operation of the analyzers and assays.

- Software & Services: Encompasses the analytical software, data management systems, laboratory information system (LIS) integration, and post-sales support services, including installation, training, and routine maintenance, enhancing the overall functionality and longevity of the systems.

- Instruments

- Application:

The application segment delineates the primary therapeutic and diagnostic areas where immunochemistry analyzers are extensively utilized. Infectious diseases represent a significant application, with analyzers being instrumental in detecting viral, bacterial, and parasitic infections, facilitating rapid diagnosis and guiding appropriate treatment. Oncology applications focus on identifying cancer biomarkers for early detection, prognosis, and monitoring treatment response, contributing to personalized cancer care. Endocrinology involves the measurement of hormones and metabolic markers for diagnosing and managing conditions like diabetes, thyroid disorders, and reproductive health issues. Cardiology applications include assessing cardiac markers for acute myocardial infarction and heart failure, while drug monitoring ensures therapeutic levels of prescribed medications in patients, preventing toxicity or sub-therapeutic effects.

- Infectious Diseases: Diagnostics for conditions such as HIV, hepatitis, dengue, and various bacterial infections, crucial for public health surveillance and clinical management.

- Endocrinology: Testing for thyroid hormones, reproductive hormones, insulin, and other endocrine markers essential for metabolic and hormonal health assessment.

- Oncology: Detection and monitoring of tumor markers like PSA, CA-125, CEA, and AFP, vital for cancer screening, diagnosis, and post-treatment surveillance.

- Cardiology: Measurement of cardiac enzymes and biomarkers such as Troponin, BNP, and CK-MB for diagnosing heart attacks and assessing cardiac function.

- Drug Monitoring: Therapeutic drug monitoring (TDM) to ensure optimal drug concentrations in patient bloodstreams, particularly for narrow therapeutic index drugs.

- Autoimmune Diseases: Identification of autoantibodies for the diagnosis and management of conditions like rheumatoid arthritis, lupus, and celiac disease.

- Others: Includes applications in toxicology, allergy testing, and various niche diagnostic areas not covered by the primary categories.

- End User:

This segment categorizes the market based on the primary entities that utilize immunochemistry analyzers, reflecting the diverse settings where diagnostic testing occurs. Hospitals are major end-users, leveraging these analyzers for routine and specialized diagnostic tests across various departments, supporting inpatient and outpatient care. Diagnostic laboratories, including independent and reference labs, utilize these high-throughput systems for processing a vast volume of samples, serving as central hubs for comprehensive testing services. Research institutes and academic centers employ these analyzers for scientific investigations, biomarker discovery, and clinical trials, contributing to advancements in diagnostic medicine. Pharmaceutical and biotechnology companies use them in drug discovery, development, and clinical trials, assessing drug efficacy and safety profiles.

- Hospitals: Utilize analyzers for a broad range of diagnostic tests, from emergency care to specialized departments, supporting quick patient diagnosis and treatment decisions.

- Diagnostic Laboratories: Including independent and centralized reference laboratories, these are high-volume users, performing a vast array of tests for clinicians and other healthcare facilities.

- Research Institutes: Employ immunochemistry analyzers for basic and translational research, biomarker identification, and validation of new diagnostic assays.

- Pharmaceutical & Biotechnology Companies: Use analyzers in drug development, clinical trials, and quality control for assessing drug efficacy, safety, and pharmacokinetics.

- Others: Encompasses blood banks, academic institutions, public health organizations, and point-of-care settings like physician offices and urgent care centers.

Regional Highlights

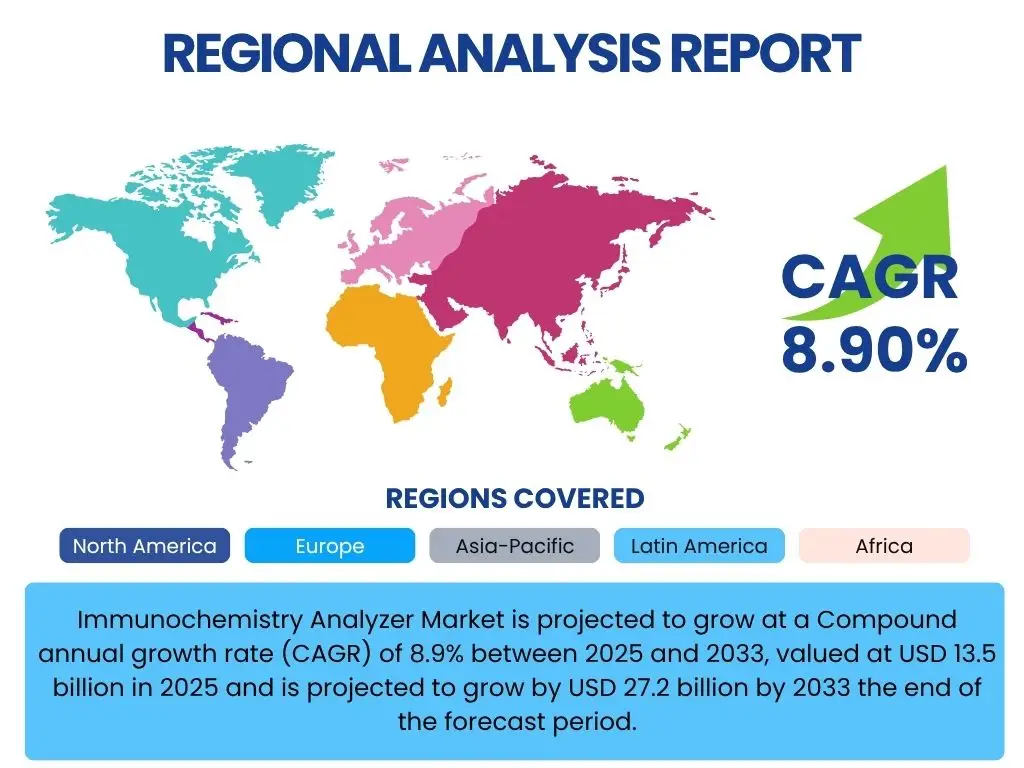

North America currently stands as the leading region in the immunochemistry analyzer market, driven by robust healthcare infrastructure, high adoption rates of advanced diagnostic technologies, and significant investments in research and development. The presence of key market players, a high prevalence of chronic diseases, and favorable reimbursement policies further contribute to its dominance. The United States, in particular, leads the regional market due to its advanced diagnostic capabilities and extensive network of clinical laboratories. Europe follows closely, propelled by increasing awareness regarding early disease diagnosis, growing geriatric populations, and supportive government initiatives for healthcare modernization. Countries like Germany, the UK, and France are major contributors, characterized by well-established healthcare systems and a focus on integrating innovative diagnostic solutions. The region also benefits from a strong emphasis on research and development in in-vitro diagnostics. Asia Pacific is projected to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period, making it a critical growth engine for the market. This rapid expansion is attributed to improving healthcare expenditure, rising disposable incomes, and the increasing burden of chronic and infectious diseases in countries like China, India, and Japan. The expanding patient pool, growing medical tourism, and government initiatives aimed at upgrading diagnostic facilities are creating lucrative opportunities for market players in this region. Latin America is experiencing steady growth, driven by increasing access to healthcare services and a rising demand for advanced diagnostics in countries such as Brazil and Mexico. The Middle East and Africa (MEA) region is also witnessing gradual growth, fueled by improving healthcare infrastructure, increasing health awareness, and strategic investments in medical technologies, particularly in countries like Saudi Arabia and the UAE. However, these regions still face challenges related to healthcare affordability and infrastructure development compared to developed markets.

Top Key Players:

The market research report covers the analysis of key stake holders of the Immunochemistry Analyzer Market. Some of the leading players profiled in the report include -- Company A

- Company B

- Company C

- Company D

- Company E

- Company F

- Company G

- Company H

- Company I

- Company J

- Company K

- Company L

- Company M

- Company N

- Company O

- Company P

- Company Q

- Company R

Frequently Asked Questions:

What is an immunochemistry analyzer?

Immunochemistry analyzers are sophisticated laboratory instruments designed to detect and quantify specific substances, known as analytes, in biological samples (such as blood or urine) by utilizing antibody-antigen reactions. These instruments are fundamental for various diagnostic applications, including the identification of hormones, proteins, therapeutic drugs, and disease markers, providing crucial insights for disease diagnosis, monitoring, and treatment management.How does an immunochemistry analyzer work?

An immunochemistry analyzer operates by employing immunoassay techniques where antibodies or antigens are used to detect target analytes. The process typically involves mixing a patient sample with specific reagents that contain antibodies or antigens labeled with a detectable marker (e.g., enzymes, fluorescent dyes, or chemiluminescent substances). When the target analyte is present, it binds to the labeled reagent, forming an immune complex. The analyzer then measures the signal produced by this label, which is proportional to the concentration of the analyte in the sample. This allows for precise quantitative or qualitative analysis of various biomarkers.What are the primary applications of immunochemistry analyzers?

Immunochemistry analyzers are extensively used across a wide range of clinical applications due to their high specificity and sensitivity. Key applications include the diagnosis and monitoring of infectious diseases (e.g., HIV, hepatitis), endocrine disorders (e.g., thyroid conditions, diabetes), oncology (e.g., tumor markers for cancer detection), cardiac markers (e.g., troponin for heart attacks), and therapeutic drug monitoring. They also play a crucial role in fertility testing, autoimmune disease diagnosis, and allergy testing, providing comprehensive diagnostic capabilities.What are the different types of immunochemistry analyzers available in the market?

The immunochemistry analyzer market offers various types tailored to different laboratory needs and throughput requirements. These typically include automated analyzers, which handle high volumes of samples with minimal manual intervention, semi-automated analyzers, which require some manual steps but automate the testing process, and point-of-care (POC) analyzers, designed for rapid testing outside the central laboratory setting. Technologies commonly employed include chemiluminescence immunoassay (CLIA), enzyme-linked immunosorbent assay (ELISA), radioimmunoassay (RIA), and electrochemiluminescence immunoassay (ECLIA), each offering distinct advantages in terms of sensitivity, speed, and cost.What are the key trends shaping the immunochemistry analyzer market?

The immunochemistry analyzer market is being shaped by several transformative trends. A significant trend is the increasing adoption of automation and high-throughput systems to enhance efficiency and reduce turnaround times in large laboratories. The integration of artificial intelligence (AI) and machine learning is improving diagnostic accuracy, data interpretation, and predictive maintenance. Furthermore, there is a growing demand for compact, user-friendly point-of-care (POC) testing solutions, allowing for decentralized diagnostics. Other notable trends include the development of multiplex assays for simultaneous detection of multiple analytes and a shift towards more sensitive and rapid immunoassay technologies like chemiluminescence.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted