IC Tray Market

IC Tray Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703381 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

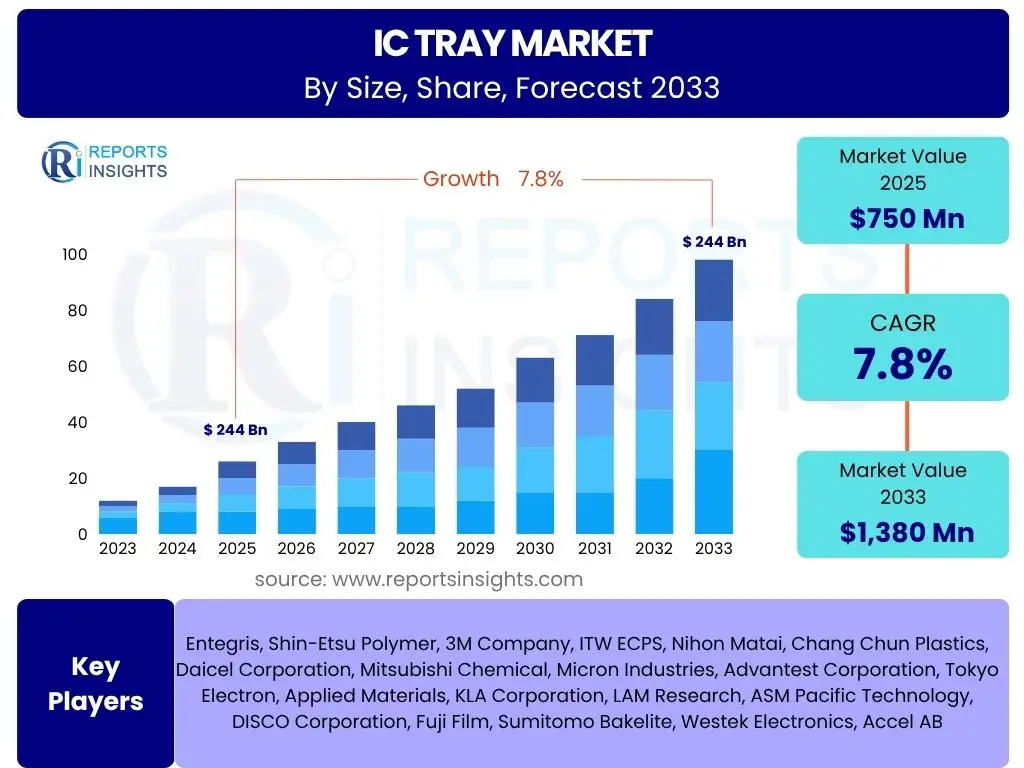

IC Tray Market Size

According to Reports Insights Consulting Pvt Ltd, The IC Tray Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 750 Million in 2025 and is projected to reach USD 1,380 Million by the end of the forecast period in 2033.

Key IC Tray Market Trends & Insights

The IC Tray market is currently shaped by several transformative trends driven by the rapid evolution of the semiconductor industry. Users frequently inquire about the impact of advanced packaging technologies, the increasing demand for high-performance computing components, and the imperative for sustainable manufacturing practices on the IC Tray landscape. A significant shift towards more robust, precision-engineered trays capable of handling sensitive, smaller, and higher-density integrated circuits is observed, reflecting a broader industry push for miniaturization and enhanced performance. Furthermore, the global emphasis on supply chain resilience and localized manufacturing is influencing regional market dynamics and investment patterns for IC Tray production.

Emerging trends indicate a strong focus on material innovation, with a move towards recyclable and bio-based polymers to align with environmental regulations and corporate sustainability goals. The integration of smart manufacturing principles, including automation and data analytics in tray production, is also gaining traction, promising improved efficiency and quality control. The proliferation of IoT devices and the ongoing build-out of 5G infrastructure are further fueling the demand for specialized IC Trays, particularly those designed for high-frequency and low-power applications. These trends collectively underscore a market adapting to both technological advancements and growing environmental consciousness.

- Miniaturization and increasing density of integrated circuits driving demand for precision trays.

- Growth of advanced packaging technologies like Wafer Level Packaging (WLP) and 3D stacking.

- Rising adoption of sustainable and recyclable materials for IC Tray manufacturing.

- Integration of automation and smart manufacturing processes in tray production.

- Increasing demand from emerging applications such as 5G, AI, and automotive electronics.

- Focus on enhanced thermal management properties in tray design for high-performance chips.

- Emphasis on supply chain diversification and regionalized manufacturing capabilities.

AI Impact Analysis on IC Tray

The proliferation and advancement of Artificial Intelligence (AI) are profoundly influencing the IC Tray market, primarily through their direct impact on semiconductor manufacturing and logistics. Users frequently explore how AI can optimize IC Tray design, predict material requirements, and enhance quality control during production. The increased demand for AI-specific chips, such as GPUs and specialized AI accelerators, directly translates into a greater need for advanced IC Trays capable of handling these high-value, high-performance components with utmost precision and protection. AI is also being explored for predictive maintenance of manufacturing equipment used in tray production, reducing downtime and improving operational efficiency.

Beyond the direct demand for AI-related hardware, AI technologies are also revolutionizing the operational aspects of the IC Tray industry itself. AI-driven algorithms can optimize tray sorting, inspection, and inventory management, leading to significant cost reductions and improved throughput. Furthermore, the insights generated by AI from production data can inform future tray designs, ensuring they meet the evolving requirements of next-generation semiconductors, which are often developed with AI capabilities in mind. This symbiotic relationship positions AI as both a demand driver and an efficiency enabler within the IC Tray market.

- Increased demand for IC Trays to accommodate AI-specific chips (GPUs, NPUs, accelerators).

- AI-driven optimization of IC Tray design for thermal management and protection.

- Application of AI for predictive maintenance in IC Tray manufacturing processes.

- Enhanced quality inspection and defect detection using AI-powered vision systems.

- AI-enabled inventory management and logistics optimization for IC Trays.

- Improved supply chain forecasting and resilience through AI analytics.

- Development of smart trays with embedded sensors for real-time monitoring, facilitated by AI.

Key Takeaways IC Tray Market Size & Forecast

An analysis of the IC Tray market size and forecast reveals several critical insights regarding its trajectory and underlying growth drivers. Common user questions often center on identifying the primary factors contributing to market expansion, understanding the projected growth rate, and discerning the most promising segments or regions for future investment. A key takeaway is the robust and consistent growth anticipated throughout the forecast period, largely propelled by the sustained expansion of the global semiconductor industry and the pervasive integration of electronics across various sectors.

The market's resilience is further highlighted by its ability to adapt to technological shifts, such as the increasing complexity of integrated circuits and the demand for advanced packaging solutions. While the overall market trajectory is positive, specific segments, particularly those serving high-growth applications like AI, 5G, and automotive electronics, are expected to exhibit accelerated expansion. Stakeholders should focus on material innovation, operational efficiency, and strategic regional expansion to capitalize on these opportunities and mitigate potential challenges arising from supply chain volatility or increasing competition.

- The IC Tray market is poised for steady growth, driven by the expanding semiconductor industry.

- Miniaturization and increasing chip complexity are key demand generators for advanced trays.

- Technological advancements in packaging, such as 3D ICs, directly influence tray design and demand.

- The automotive, consumer electronics, and telecom sectors represent significant end-use growth areas.

- Geographic shifts in semiconductor manufacturing are creating new regional market opportunities.

- Material innovation towards sustainable and high-performance polymers is crucial for future growth.

- Supply chain resilience and localized production are becoming increasingly important competitive factors.

IC Tray Market Drivers Analysis

The IC Tray market is significantly propelled by the relentless expansion and innovation within the global semiconductor industry. The escalating demand for integrated circuits across diverse applications, from consumer electronics to advanced automotive systems and data centers, directly translates into a heightened need for IC Trays for handling, transporting, and protecting these sensitive components. Furthermore, the ongoing miniaturization of electronic devices and the increasing complexity of chip designs necessitate high-precision, robust trays capable of safeguarding smaller, more fragile, and higher-density ICs.

Technological advancements in packaging, such as flip-chip, Wafer Level Packaging (WLP), and 3D stacking, also serve as critical drivers, requiring specialized tray designs that can accommodate these intricate structures and ensure their integrity throughout the supply chain. The rapid deployment of 5G technology, the widespread adoption of Artificial Intelligence (AI) and Machine Learning (ML), and the proliferation of the Internet of Things (IoT) devices are creating new avenues for growth, as each of these technologies relies heavily on sophisticated semiconductor components that require reliable IC Tray solutions for their production and distribution. Environmental considerations are also subtly driving innovation, as manufacturers seek trays made from more sustainable materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Semiconductor Industry | +2.5% | Global, particularly Asia Pacific (APAC) | Long-term (2025-2033) |

| Miniaturization & Complex Chip Designs | +1.8% | Global, all advanced electronics manufacturing hubs | Mid to Long-term (2025-2033) |

| Advancements in Packaging Technologies (e.g., 3D ICs, WLP) | +1.5% | North America, APAC (Taiwan, South Korea, Japan) | Mid-term (2026-2030) |

| Rising Demand for Consumer Electronics & Automotive Electronics | +1.2% | Asia Pacific (China, India), Europe, North America | Long-term (2025-2033) |

| Expansion of 5G, AI, and IoT Technologies | +0.8% | Global, particularly developed economies | Mid to Long-term (2025-2033) |

IC Tray Market Restraints Analysis

Despite its robust growth trajectory, the IC Tray market faces several significant restraints that could temper its expansion. One primary concern is the relatively high manufacturing cost associated with producing high-precision IC Trays, especially those designed for advanced packaging applications. These costs are often driven by specialized material requirements, intricate molding processes, and stringent quality control measures, which can limit broader adoption in cost-sensitive segments. Furthermore, the market's dependence on specific polymer materials, such as various types of engineering plastics, exposes it to raw material price volatility and supply chain disruptions.

Another restraint stems from the rapid technological obsolescence inherent in the semiconductor industry. As chip designs evolve at an accelerated pace, IC Trays designed for previous generations may quickly become obsolete, leading to potential inventory write-offs and increased R&D costs for continuous product development. Moreover, intense competition within the IC Tray manufacturing sector, characterized by a fragmented market and the presence of numerous regional and global players, can exert downward pressure on pricing, affecting profit margins for manufacturers. Environmental regulations concerning plastic waste and manufacturing emissions also present a growing challenge, pushing companies towards more expensive, sustainable alternatives or complex recycling processes, thus impacting operational costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs & Material Volatility | -1.5% | Global, especially emerging economies | Long-term (2025-2033) |

| Rapid Technological Obsolescence in Semiconductor Industry | -1.0% | Global, impacting R&D intensive regions | Mid to Long-term (2025-2033) |

| Intense Market Competition & Pricing Pressure | -0.7% | Asia Pacific (APAC), North America | Short to Mid-term (2025-2029) |

| Environmental Regulations & Sustainability Pressures | -0.5% | Europe, North America, parts of APAC | Mid to Long-term (2026-2033) |

| Supply Chain Disruptions & Geopolitical Risks | -0.3% | Global, with varying regional severity | Short-term (2025-2027) |

IC Tray Market Opportunities Analysis

The IC Tray market is presented with several promising opportunities that can significantly contribute to its future growth and diversification. One major opportunity lies in the burgeoning demand for sustainable packaging solutions within the semiconductor industry. As environmental consciousness grows and regulations tighten, the development and adoption of bio-based, recycled, and recyclable IC Tray materials offer a substantial competitive advantage and open new market segments. Companies investing in green manufacturing processes and materials can cater to a growing niche of environmentally responsible clients and gain market share.

Furthermore, the continuous innovation in semiconductor packaging, particularly the shift towards ultra-thin, highly integrated, and complex packages, creates a constant need for specialized, custom-designed IC Trays. This trend offers an opportunity for manufacturers to develop high-value, niche products that command better pricing and require advanced engineering expertise. The expansion of semiconductor fabrication plants (fabs) and outsourced semiconductor assembly and test (OSAT) facilities in new geographic regions, driven by supply chain diversification initiatives, also presents an opportunity for IC Tray suppliers to establish localized production or distribution networks, reducing logistics costs and improving responsiveness to regional demands. The growth of emerging markets, particularly in Southeast Asia and parts of Latin America, is also fostering new demand for consumer electronics and, consequently, IC Trays.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Sustainable Materials | +1.7% | Europe, North America, Asia Pacific (Japan, South Korea) | Mid to Long-term (2026-2033) |

| Increasing Demand for Custom & Advanced Packaging Trays | +1.4% | Global, driven by high-tech industries | Long-term (2025-2033) |

| Expansion of Semiconductor Manufacturing in Emerging Regions | +1.0% | Southeast Asia, India, Mexico, Eastern Europe | Mid to Long-term (2026-2033) |

| Integration with Smart Factory & Industry 4.0 Solutions | +0.8% | Global, particularly advanced manufacturing hubs | Mid-term (2027-2031) |

| Growth in Niche Markets (e.g., Medical Devices, High-Reliability Defense) | +0.5% | North America, Europe, parts of APAC | Long-term (2025-2033) |

IC Tray Market Challenges Impact Analysis

The IC Tray market navigates a landscape riddled with distinct challenges that necessitate strategic responses from industry players. A significant challenge is the intense and often cutthroat competition among numerous manufacturers, leading to price erosion and compressed profit margins, particularly for standardized tray products. This competitive pressure often forces companies to invest heavily in R&D to differentiate their offerings, which can be a financial strain for smaller enterprises. Furthermore, the rapid pace of technological advancements within the semiconductor industry means that IC Tray designs must constantly evolve to accommodate new chip dimensions, sensitivities, and packaging methods, posing a continuous challenge for product development and validation.

Another critical challenge revolves around ensuring stringent quality control and reliability, given the high value and delicate nature of the integrated circuits they transport. Any defect in an IC Tray can lead to significant damage to chips, resulting in substantial financial losses for clients and reputational damage for tray manufacturers. Supply chain volatility, encompassing raw material shortages, fluctuating prices, and logistical bottlenecks, represents an ongoing operational challenge. Geopolitical tensions and trade disputes can exacerbate these issues, impacting the global flow of materials and finished products. Moreover, managing the environmental impact of plastic waste from discarded trays and adhering to evolving sustainability regulations worldwide adds complexity and cost to manufacturing processes, demanding innovative solutions for recycling or alternative materials.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Price Erosion | -1.2% | Global, particularly in Asia Pacific (APAC) | Long-term (2025-2033) |

| Rapid Technological Shifts & Product Obsolescence | -0.9% | Global, impacting R&D cycles | Mid to Long-term (2025-2033) |

| Ensuring High Quality & Reliability for Delicate ICs | -0.6% | Global, critical for high-value applications | Ongoing (2025-2033) |

| Supply Chain Volatility & Geopolitical Risks | -0.4% | Global, varying by region and material dependency | Short to Mid-term (2025-2028) |

| Environmental Compliance & Waste Management | -0.3% | Europe, North America, parts of Asia | Mid to Long-term (2026-2033) |

IC Tray Market - Updated Report Scope

This comprehensive market research report on the IC Tray market provides an in-depth analysis of industry trends, market dynamics, and competitive landscape. It covers historical data, current market conditions, and future projections to offer a holistic view of the market's evolution from 2019 to 2033. The report segments the market by various criteria, including material type, application, and end-use industry, providing granular insights into key growth areas and emerging opportunities. It also includes detailed regional breakdowns and profiles of leading companies, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 750 Million |

| Market Forecast in 2033 | USD 1,380 Million |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Entegris, Shin-Etsu Polymer, 3M Company, ITW ECPS, Nihon Matai, Chang Chun Plastics, Daicel Corporation, Mitsubishi Chemical, Micron Industries, Advantest Corporation, Tokyo Electron, Applied Materials, KLA Corporation, LAM Research, ASM Pacific Technology, DISCO Corporation, Fuji Film, Sumitomo Bakelite, Westek Electronics, Accel AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The IC Tray market is extensively segmented to provide a detailed understanding of its diverse components and drivers. These segmentations allow for a granular analysis of market dynamics, enabling stakeholders to identify specific growth areas, understand demand patterns, and tailor their strategies effectively. The primary segmentations include material type, which differentiates between conductive and non-conductive polymers critical for electrostatic discharge (ESD) protection, and the classification by tray type, such as JEDEC standard trays or highly specialized custom solutions for unique chip designs.

Further segmentation by application highlights the varied uses of IC Trays across the semiconductor manufacturing process, from testing and burn-in to final assembly, handling, and shipping. This is crucial for understanding demand at different stages of the value chain. Lastly, segmentation by end-use industry categorizes demand based on where the integrated circuits are ultimately deployed, such as consumer electronics, automotive, telecommunications, or industrial applications. Each segment possesses distinct requirements and growth trajectories, collectively shaping the overall market landscape.

- By Material:

- Conductive Polymers: Essential for electrostatic discharge (ESD) protection, commonly used for sensitive ICs.

- Non-Conductive Polymers: Used where ESD protection is not the primary concern, offering cost-effectiveness.

- Others: Includes emerging materials like bio-based polymers and advanced composites.

- By Type:

- JEDEC Trays: Standardized trays conforming to JEDEC specifications for broad compatibility.

- Custom Trays: Tailored trays designed for specific, often unique, IC packages or handling requirements.

- Speciality Trays: Designed for extreme conditions such as high temperatures or specific chemical resistances.

- By Application:

- Test: Trays designed for automated testing of ICs.

- Burn-in: Trays used to hold ICs during burn-in processes for reliability testing under stress.

- Assembly & Handling: Trays facilitating the automated assembly and internal transfer of ICs.

- Shipping: Robust trays for secure transportation of finished ICs.

- Storage: Trays for long-term or short-term warehousing of ICs.

- By End-Use Industry:

- Consumer Electronics: Smartphones, laptops, wearables, home appliances.

- Automotive: Infotainment, ADAS, power management, electric vehicle components.

- Telecommunications: 5G infrastructure, network equipment, optical modules.

- Industrial: Automation, robotics, power electronics, control systems.

- Medical: Diagnostic equipment, implantable devices, monitoring systems.

- Data Centers: Servers, storage, networking components for cloud computing.

- Others: Defense, aerospace, scientific instruments.

Regional Highlights

- North America: The North American market for IC Trays is characterized by a strong presence of leading semiconductor companies, significant investment in R&D, and early adoption of advanced technologies like AI and quantum computing. Demand is primarily driven by the robust telecommunications, data center, and automotive sectors, with a growing emphasis on domestic semiconductor manufacturing and supply chain resilience. The region's focus on high-performance computing and specialized chip design creates a consistent need for high-precision, custom IC Trays.

- Europe: Europe represents a mature market for IC Trays, with demand stemming from its well-established automotive electronics, industrial automation, and telecommunications industries. The region is at the forefront of implementing stringent environmental regulations, which are increasingly driving the adoption of sustainable and recyclable IC Tray materials. Innovation in advanced packaging and the growth of localized manufacturing initiatives, supported by EU policies, contribute to a stable and evolving market.

- Asia Pacific (APAC): APAC dominates the global IC Tray market, owing to its position as the world's leading hub for semiconductor manufacturing, assembly, and packaging. Countries like China, Taiwan, South Korea, and Japan host a vast number of foundries, OSAT companies, and electronics manufacturers. The sheer volume of chip production, coupled with rapid growth in consumer electronics, 5G deployment, and automotive applications, ensures sustained high demand for IC Trays. Emerging economies within APAC, such as India and Southeast Asian nations, are also witnessing increased investment in electronics manufacturing, further fueling market expansion.

- Latin America: The Latin American IC Tray market is in a nascent but growing phase, primarily influenced by expanding consumer electronics assembly operations and a developing automotive industry. While smaller in scale compared to other regions, increasing foreign direct investment in manufacturing and a growing middle class are contributing to rising demand for electronic devices, which in turn drives the need for IC Trays. The market here is largely dependent on imports, but local manufacturing capabilities are slowly emerging.

- Middle East and Africa (MEA): The MEA region is currently a smaller contributor to the global IC Tray market, with demand primarily associated with the import and assembly of electronic goods. However, strategic investments in technological infrastructure, telecommunications, and a nascent electronics manufacturing sector, particularly in countries like UAE and Saudi Arabia, suggest potential for future growth. The region's increasing adoption of smart technologies and consumer electronics is expected to gradually stimulate demand for IC Trays.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the IC Tray Market.- Entegris

- Shin-Etsu Polymer

- 3M Company

- ITW ECPS

- Nihon Matai

- Chang Chun Plastics

- Daicel Corporation

- Mitsubishi Chemical

- Micron Industries

- Advantest Corporation

- Tokyo Electron

- Applied Materials

- KLA Corporation

- LAM Research

- ASM Pacific Technology

- DISCO Corporation

- Fuji Film

- Sumitomo Bakelite

- Westek Electronics

- Accel AB

Frequently Asked Questions

What is an IC Tray and its primary function?

An IC Tray, or Integrated Circuit Tray, is a specialized container designed to hold, protect, and transport integrated circuits (chips) during various stages of manufacturing, testing, handling, and shipping. Its primary function is to prevent physical damage, ensure proper alignment for automated processes, and offer electrostatic discharge (ESD) protection for sensitive electronic components.

What materials are commonly used for manufacturing IC Trays?

IC Trays are typically manufactured from various engineering plastics, including conductive polymers like polyphenylene sulfide (PPS) and polycarbonate (PC) for ESD protection, as well as non-conductive polymers. The choice of material depends on factors such as temperature requirements, mechanical strength, chemical resistance, and the need for static dissipation.

How does the growth of advanced semiconductor packaging influence the IC Tray market?

The increasing adoption of advanced semiconductor packaging technologies, such as flip-chip, Wafer Level Packaging (WLP), and 3D stacking, significantly influences the IC Tray market by demanding more precise, custom-designed, and highly specialized trays. These advanced packages are often smaller, more delicate, and have unique form factors, requiring trays that offer superior protection and compatibility with complex automated handling systems.

Which industries are the primary end-users for IC Trays?

The primary end-user industries for IC Trays are broadly distributed across the electronics sector. Key segments include consumer electronics (smartphones, laptops), automotive electronics (ADAS, infotainment), telecommunications (5G infrastructure), industrial automation, medical devices, and data centers. Each industry requires specific types of IC Trays tailored to their unique handling and protection needs.

What are the key sustainability trends impacting IC Tray manufacturing?

Key sustainability trends impacting IC Tray manufacturing include the growing demand for trays made from recycled or bio-based materials, efforts to reduce overall plastic waste, and the implementation of more energy-efficient production processes. Manufacturers are increasingly focusing on developing reusable, recyclable, or biodegradable tray solutions to align with global environmental regulations and corporate sustainability goals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted