IC Substrate Market

IC Substrate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707907 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

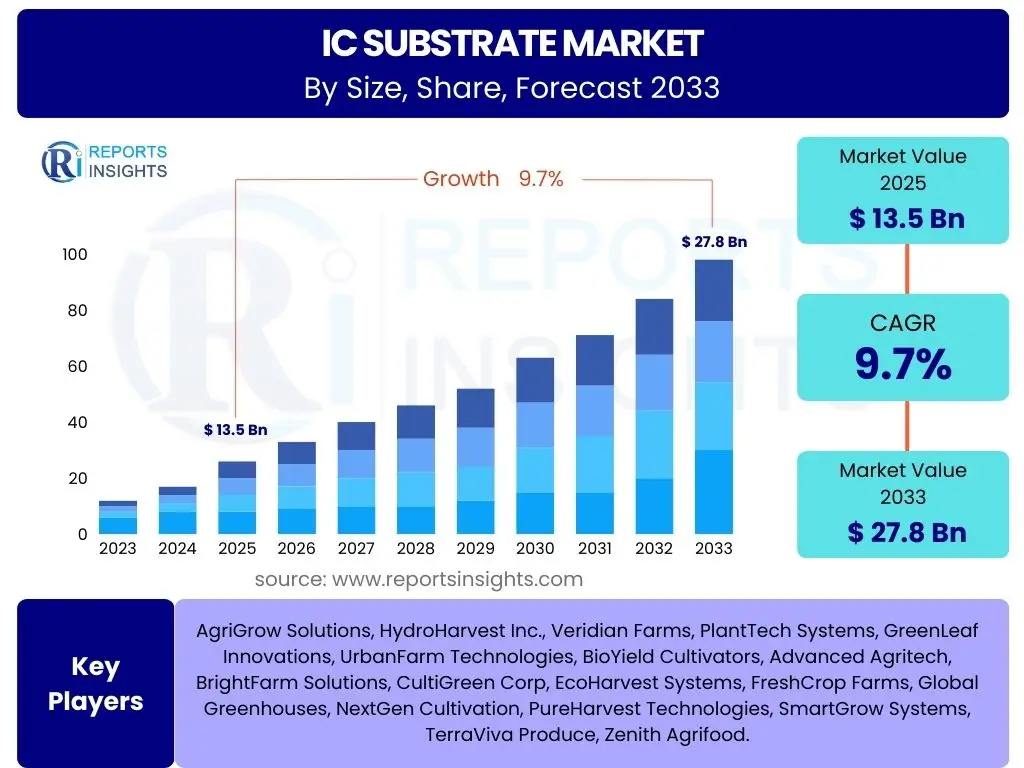

IC Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The IC Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 13.5 billion in 2025 and is projected to reach USD 27.8 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the escalating demand for advanced electronic devices, including smartphones, high-performance computing (HPC) systems, and automotive electronics, all of which rely heavily on sophisticated integrated circuit packaging technologies. The continuous miniaturization of electronic components and the increasing complexity of semiconductor devices necessitate the evolution of IC substrates to support higher pin counts, improved electrical performance, and enhanced thermal dissipation capabilities.

The market expansion is further propelled by rapid technological advancements in advanced packaging solutions such as flip-chip ball grid array (FC-BGA) and flip-chip chip scale package (FC-CSP), which require high-density interconnect substrates. These advancements are crucial for supporting the ever-increasing data processing demands across various industries, from telecommunications and consumer electronics to industrial automation. Moreover, the global push towards digitalization and the widespread adoption of 5G technology, artificial intelligence (AI), and the Internet of Things (IoT) are creating robust demand for high-performance, reliable IC substrates capable of handling complex functionalities and faster data transfer rates. This upward trajectory indicates a strong and sustained growth phase for the IC substrate industry throughout the forecast period.

Key IC Substrate Market Trends & Insights

User inquiries frequently highlight the evolving technological landscape and its implications for IC substrate development. Common questions revolve around how miniaturization, advanced packaging, and material innovations are shaping the industry. There is significant interest in understanding the shift towards higher-density interconnects, improved thermal management solutions, and the integration of new functionalities directly onto substrates. Users also seek insights into the sustainability aspects and the role of specialized substrates in emerging applications like quantum computing and advanced medical devices.

The market is witnessing a profound shift towards ultra-high-density interconnects and multi-layer substrates, driven by the need to integrate more functionalities into smaller form factors. This trend is inextricably linked to the proliferation of advanced packaging technologies, such as system-in-package (SiP) and chiplets, which demand superior electrical performance and thermal dissipation characteristics from the substrate. Furthermore, there has been a notable emphasis on developing more environmentally friendly and sustainable manufacturing processes and materials, reflecting broader industry commitments to ecological responsibility. The quest for enhanced power efficiency and signal integrity in high-frequency applications is also a critical underlying trend, pushing innovation in material science and design methodologies.

- Miniaturization and High-Density Interconnects: The continuous drive for smaller, more powerful devices necessitates finer line widths and spaces, increasing circuit density on substrates.

- Advanced Packaging Technologies: Widespread adoption of FC-BGA, FC-CSP, and SiP is accelerating, demanding substrates with enhanced electrical, thermal, and mechanical properties.

- Material Innovation: Development of low-dielectric constant (low-k) materials for improved signal integrity and advanced heat dissipation materials for thermal management.

- Sustainability and Green Manufacturing: Increasing focus on eco-friendly materials, reduced energy consumption, and sustainable manufacturing processes.

- Integration of Specialized Functions: Substrates are evolving beyond mere interconnection to include embedded components and integrate specialized functionalities directly.

AI Impact Analysis on IC Substrate

Common user questions regarding AI's impact on the IC substrate market often focus on how AI-driven applications are influencing demand for specific substrate types, the increased performance requirements, and the role of AI in optimizing substrate design and manufacturing. There is keen interest in understanding the material and structural innovations necessary to support AI processors, particularly those designed for high-performance computing and edge AI. Users are also exploring how AI itself can be leveraged within the substrate manufacturing process for quality control and efficiency improvements.

Artificial intelligence is a transformative force, profoundly impacting the IC substrate market by driving the demand for exceptionally high-performance and complex substrates. AI processors, especially those used in data centers, autonomous vehicles, and advanced robotics, require substrates capable of handling massive data throughput, high power delivery, and efficient thermal dissipation. This necessitates the development of multi-layer, high-density substrates with superior electrical properties and robust thermal management solutions, pushing the boundaries of current manufacturing capabilities. AI also influences substrate design through advanced simulation tools, enabling faster iteration and optimization for complex layouts and signal integrity.

Furthermore, AI is not only a demand driver but also a tool for innovation within the IC substrate industry. Machine learning algorithms are increasingly being employed in the design phase to optimize substrate layouts, predict performance characteristics, and identify potential manufacturing defects before production. In the manufacturing process, AI-powered systems are enhancing quality control, improving yield rates, and optimizing operational efficiency through predictive maintenance and process parameter adjustments. This dual impact of AI—as both a primary consumer of advanced substrates and a catalyst for their development and production—underscores its critical role in shaping the future of this market.

- Increased Demand for High-Performance Substrates: AI processors require advanced FC-BGA and FC-CSP substrates with high layer counts, fine pitch, and superior electrical characteristics.

- Enhanced Thermal Management Requirements: AI chips generate significant heat, necessitating substrates designed with efficient heat dissipation pathways and advanced materials.

- AI in Design and Simulation: AI/ML algorithms are optimizing substrate layouts, predicting signal integrity, and accelerating design cycles for complex packages.

- Manufacturing Process Optimization: AI-driven analytics and robotics improve yield rates, quality control, and predictive maintenance in substrate fabrication.

- Edge AI Proliferation: Growth in edge AI devices drives demand for smaller, more power-efficient substrates suitable for integration in compact form factors.

Key Takeaways IC Substrate Market Size & Forecast

User inquiries frequently focus on the overarching implications of the IC substrate market forecast, seeking concise summaries of what the projected growth means for stakeholders. Questions often explore the primary drivers of this growth, the most impactful technological shifts, and the regions expected to lead market expansion. There's also an interest in understanding the strategic imperatives for companies looking to capitalize on this growth, including investment areas and potential market vulnerabilities.

The IC Substrate Market is poised for substantial and sustained growth throughout the forecast period, driven by an insatiable global demand for advanced electronics. This growth is not merely incremental but represents a fundamental shift towards more complex and performance-intensive packaging solutions, making the substrate a critical component in the semiconductor ecosystem. Key to this expansion are the relentless advancements in communication technologies, such as 5G, and the pervasive integration of AI and IoT across all sectors, which collectively necessitate substrates with higher density, improved thermal efficiency, and superior electrical performance. The market's resilience is also underpinned by ongoing innovation in materials science and manufacturing processes, ensuring that substrates can keep pace with rapidly evolving chip designs.

Strategic success in this dynamic market will hinge on companies' abilities to invest in next-generation manufacturing capabilities, foster innovation in advanced materials, and adapt to rapidly changing design requirements. Collaboration across the semiconductor value chain—from material suppliers to OSATs (Outsourced Semiconductor Assembly and Test) and fabless companies—will be crucial for addressing complex technical challenges and accelerating time-to-market for novel solutions. Furthermore, navigating global supply chain complexities and geopolitical influences will remain paramount for maintaining stability and ensuring continuous innovation. The forecast underscores a vibrant market rich with opportunities for those prepared to meet its demanding technological and operational prerequisites.

- Significant Growth Potential: The market is projected for robust double-digit growth, indicating strong investment opportunities and expanding demand.

- Technological Advancements are Core: Innovation in advanced packaging and high-density interconnects will continue to be the primary growth catalysts.

- AI and 5G as Major Demand Drivers: The proliferation of AI and 5G technologies will substantially increase the need for high-performance substrates.

- Focus on Performance and Efficiency: Substrates must offer superior electrical characteristics, enhanced thermal management, and power efficiency for next-gen devices.

- Strategic Investment in R&D and Manufacturing: Companies need to continuously invest in advanced materials, process technologies, and capacity expansion to stay competitive.

IC Substrate Market Drivers Analysis

The expansion of the IC Substrate Market is fundamentally propelled by the exponential growth in demand for high-performance electronic devices across a multitude of applications. The proliferation of 5G technology, the Internet of Things (IoT), and artificial intelligence (AI) are creating an unprecedented need for integrated circuits that are more powerful, smaller, and more energy-efficient. This directly translates into a requirement for advanced IC substrates capable of supporting high-density interconnects, superior electrical performance, and efficient thermal management. As devices become more sophisticated, the role of the substrate transitions from a mere interconnector to a critical component enabling complex system-level integration.

Furthermore, the automotive industry's rapid adoption of advanced driver-assistance systems (ADAS), in-car infotainment, and electric vehicle (EV) technologies is significantly contributing to market growth. These applications demand extremely reliable and robust IC substrates that can withstand harsh operating conditions and provide consistent performance for safety-critical functions. Similarly, the continuous innovation in consumer electronics, particularly in smartphones, wearables, and gaming consoles, drives the need for ever-smaller, thinner, and more powerful packages, directly impacting substrate design and manufacturing. The increasing complexity of semiconductor designs and the transition to advanced packaging techniques like flip-chip and chiplets are thus key accelerators for the IC substrate market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of 5G and IoT Devices | +2.1% | Global, especially Asia Pacific, North America | 2025-2033 |

| Increased Demand for High-Performance Computing (HPC) and AI | +1.9% | North America, Asia Pacific (China, South Korea) | 2025-2033 |

| Advancements in Automotive Electronics (ADAS, EVs) | +1.5% | Europe, North America, Asia Pacific (Japan, Germany) | 2025-2033 |

| Continuous Miniaturization and Advanced Packaging Techniques | +1.7% | Global | 2025-2033 |

| Rising Demand for Consumer Electronics (Smartphones, Wearables) | +1.2% | Asia Pacific, North America, Europe | 2025-2033 |

IC Substrate Market Restraints Analysis

Despite the robust growth trajectory, the IC substrate market faces several significant restraints that could potentially temper its expansion. One of the primary concerns revolves around the high capital expenditure required for advanced manufacturing facilities and the intensive research and development necessary to keep pace with evolving semiconductor technologies. The cost associated with developing new materials, fine-pitch processing, and sophisticated inspection systems can be prohibitive for some market players, limiting market entry and consolidation.

Another major restraint is the inherent complexity and precision required in the manufacturing process of advanced IC substrates. Achieving extremely fine line widths and spaces, maintaining perfect layer registration, and ensuring defect-free production at high volumes pose substantial technical challenges. Any slight deviation can lead to reduced yields, increased waste, and elevated production costs. Furthermore, the global semiconductor supply chain is often susceptible to geopolitical tensions, trade disputes, and natural disasters, leading to raw material price volatility and potential disruptions in the supply of critical components, which can negatively impact production schedules and profitability across the IC substrate market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and R&D Costs | -0.8% | Global | 2025-2033 |

| Technical Complexity and Manufacturing Yield Challenges | -0.7% | Global | 2025-2033 |

| Supply Chain Volatility and Raw Material Price Fluctuations | -0.6% | Global | 2025-2033 |

| Stringent Quality and Reliability Standards | -0.5% | Global, especially Automotive & Medical sectors | 2025-2033 |

| Intense Competition and Pricing Pressures | -0.4% | Asia Pacific | 2025-2033 |

IC Substrate Market Opportunities Analysis

The IC Substrate Market is brimming with opportunities driven by several transformative technological shifts and burgeoning application areas. One significant avenue lies in the continuous evolution of advanced packaging technologies, such as 3D integration, chiplets, and fan-out wafer-level packaging (FOWLP). These innovations require ever more sophisticated substrates that can facilitate heterogeneous integration and enable higher levels of functionality in smaller footprints, thereby opening new design and material possibilities for substrate manufacturers. The pursuit of greater integration and performance presents a compelling opportunity for companies that can innovate in substrate design and manufacturing processes.

Furthermore, the emergence of new computing paradigms like quantum computing and neuromorphic computing, while still in nascent stages, represents long-term growth opportunities for highly specialized IC substrates. These future technologies will demand substrates with unique electrical, thermal, and mechanical properties, pushing the boundaries of current material science and fabrication techniques. Beyond these high-tech frontiers, the expansion into untapped or under-penetrated emerging markets, particularly in regions undergoing rapid digitalization and industrialization, offers substantial potential for market growth. Developing sustainable and eco-friendly substrate solutions, including bio-based or recycled materials, also presents a strategic opportunity to capture market share and align with global environmental objectives, differentiating products in a competitive landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Packaging Technologies (e.g., Chiplets, 3D ICs) | +1.8% | Global | 2025-2033 |

| Growth in Emerging Markets and Industrial IoT Adoption | +1.5% | Asia Pacific (Southeast Asia), Latin America, MEA | 2025-2033 |

| Innovation in Sustainable and Advanced Substrate Materials | +1.2% | Global | 2025-2033 |

| Expansion of Automotive ADAS and Autonomous Driving Systems | +1.1% | Europe, North America, Japan | 2025-2033 |

| New Applications in Quantum Computing and Medical Devices | +0.9% | North America, Europe | 2028-2033 (Longer term) |

IC Substrate Market Challenges Impact Analysis

The IC Substrate Market, while experiencing significant growth, is not without its share of formidable challenges that demand strategic foresight and technological prowess. One of the most persistent challenges is the relentless drive towards miniaturization and higher integration. As ICs become smaller and more powerful, the demands on substrates for finer line widths, tighter pitches, and increased layer counts push current manufacturing capabilities to their limits. Achieving these extremely precise specifications while maintaining high yields and acceptable costs is a continuous struggle for manufacturers, often requiring substantial investments in advanced lithography and etching technologies.

Another critical challenge lies in managing the escalating heat generated by high-performance chips, especially in AI and HPC applications. Effective thermal management at the substrate level is crucial to prevent performance degradation and ensure device reliability, necessitating the development of novel heat-dissipating materials and innovative substrate architectures. Furthermore, the global semiconductor industry faces a chronic shortage of skilled labor, particularly engineers and technicians with expertise in advanced packaging and substrate manufacturing. This talent gap can hinder R&D efforts, impede production scaling, and slow down the adoption of new technologies, posing a long-term threat to market growth and innovation. Navigating these complex technical and workforce challenges will be paramount for sustained success in the IC substrate market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Barriers to Further Miniaturization and Integration | -0.9% | Global | 2025-2033 |

| Thermal Management in High-Performance ICs | -0.8% | Global | 2025-2033 |

| Skilled Labor Shortage and Talent Gap | -0.7% | North America, Europe, Asia Pacific | 2025-2033 |

| Intellectual Property (IP) Protection and Counterfeiting | -0.5% | Global, particularly Asia Pacific | 2025-2033 |

| High Capital Outlay for Capacity Expansion | -0.6% | Global | 2025-2033 |

IC Substrate Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global IC Substrate market, covering historical data from 2019-2023 and offering a detailed forecast from 2025 to 2033. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. The report also includes extensive segmentation analysis by type, material, and application, alongside a thorough regional assessment, to offer precise insights into market size, growth trajectories, and competitive positioning across various geographies. Strategic profiles of leading market participants are also included to provide a complete understanding of the competitive environment and key stakeholder strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 27.8 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ibiden Co. Ltd., Unimicron Technology Corp., Samsung Electro-Mechanics (SEMCO), LG Innotek Co., Kinsus Interconnect Technology Corp., AT&S Austria Technologie & Systemtechnik AG, Shinko Electric Industries Co. Ltd., ASE Technology Holding Co. Ltd., TTM Technologies Inc., Daeduck Co. Ltd., Shennan Circuits Co. Ltd., Tripod Technology Corp., Nanya PCB Corp., Kyocera Corp., Eastern Company Ltd. (ECC), ZDT Electronics (Zhen Ding Technology), Suzhou Doosan Electronic Co., Fujitsu Interconnect Technologies, J.S.T. Mfg. Co., Ltd., Shenzhen Founder Microelectronics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The IC Substrate Market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across various categories. This segmentation is crucial for identifying specific growth pockets, understanding technological preferences, and assessing competitive landscapes within each sub-market. By analyzing the market across different types, materials, and applications, stakeholders can pinpoint areas of high potential and tailor their strategies accordingly.

The segmentation by type distinguishes between various packaging technologies, each catering to specific performance and cost requirements, such as Flip-Chip Ball Grid Array (FC-BGA) and Flip-Chip Chip Scale Package (FC-CSP), which are particularly dominant in high-performance applications. Material segmentation highlights the shift towards advanced organic and inorganic options that offer superior electrical, thermal, and mechanical properties. Furthermore, the application-based segmentation reveals how demand from sectors like consumer electronics, automotive, and telecommunications influences the market, reflecting the varying needs for robust, compact, and high-frequency substrates across these industries. This multi-dimensional segmentation provides a robust framework for market assessment and strategic planning.

- By Type: FC-BGA (Flip-Chip Ball Grid Array), FC-CSP (Flip-Chip Chip Scale Package), WB-CSP (Wire Bond Chip Scale Package), WB-BGA (Wire Bond Ball Grid Array), Others

- By Material: Organic Substrates (BT Resin, ABF, Glass Epoxy), Inorganic Substrates (Ceramic, Glass), Flexible Substrates

- By Application: Consumer Electronics, Automotive, Telecommunication, Industrial, Medical, Others

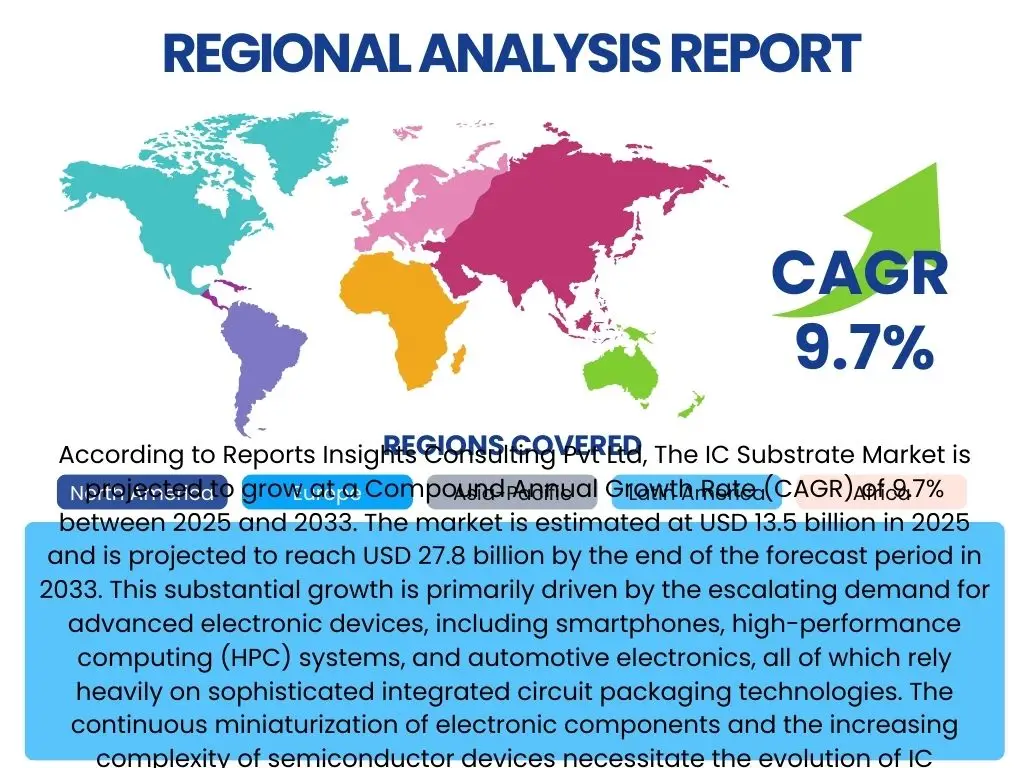

Regional Highlights

- Asia Pacific (APAC): APAC is expected to dominate the IC Substrate Market, driven by the presence of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, Japan, and China. High production capacities, continuous investments in advanced packaging technologies, and robust demand from consumer electronics, 5G infrastructure, and automotive sectors are key growth factors in this region. The region also benefits from a vast and growing market for electronic devices and a strong government focus on developing the domestic semiconductor industry.

- North America: North America represents a significant market for IC substrates, characterized by substantial investments in research and development, particularly in high-performance computing, AI, and data centers. The region is a hub for leading-edge technology innovation and boasts a strong ecosystem of fabless semiconductor companies and advanced packaging service providers. Demand is also robust from the automotive and defense sectors, which require highly reliable and specialized substrates.

- Europe: The European market for IC substrates is primarily driven by its strong automotive industry, industrial automation, and specialized medical device manufacturing. Countries like Germany, France, and the UK are investing in smart manufacturing initiatives and advanced automotive electronics, necessitating high-quality, durable, and reliable substrates. European innovation in material science also contributes to the market's technological advancements.

- Latin America & Middle East and Africa (MEA): These regions are emerging markets for IC substrates, with growth primarily influenced by increasing digitalization, expanding mobile penetration, and rising adoption of consumer electronics. While smaller in market share compared to established regions, rapid industrialization, infrastructure development, and growing investment in local manufacturing are creating new opportunities for IC substrate suppliers. The demand here is often for more cost-effective and standardized solutions, alongside increasing interest in higher-performance applications as technology adoption accelerates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the IC Substrate Market.- Ibiden Co. Ltd.

- Unimicron Technology Corp.

- Samsung Electro-Mechanics (SEMCO)

- LG Innotek Co.

- Kinsus Interconnect Technology Corp.

- AT&S Austria Technologie & Systemtechnik AG

- Shinko Electric Industries Co. Ltd.

- ASE Technology Holding Co. Ltd.

- TTM Technologies Inc.

- Daeduck Co. Ltd.

- Shennan Circuits Co. Ltd.

- Tripod Technology Corp.

- Nanya PCB Corp.

- Kyocera Corp.

- Eastern Company Ltd. (ECC)

- ZDT Electronics (Zhen Ding Technology)

- Suzhou Doosan Electronic Co.

- Fujitsu Interconnect Technologies

- J.S.T. Mfg. Co., Ltd.

- Shenzhen Founder Microelectronics.

Frequently Asked Questions

What is an IC Substrate?

An IC substrate is a foundational component in semiconductor packaging, serving as an electrical and mechanical interface between the integrated circuit (IC) chip and the printed circuit board (PCB). It facilitates electrical connections, distributes power, dissipates heat, and provides structural support for the fragile IC chip, enabling its integration into larger electronic systems.

What are the primary types of IC substrates?

The primary types of IC substrates include Flip-Chip Ball Grid Array (FC-BGA), Flip-Chip Chip Scale Package (FC-CSP), Wire Bond Chip Scale Package (WB-CSP), and Wire Bond Ball Grid Array (WB-BGA). These types differ in their connection methods, density, and suitability for various applications, with flip-chip technologies gaining prominence for high-performance devices.

Which materials are commonly used for IC substrates?

Common materials for IC substrates include organic laminates like BT (Bismaleimide Triazine) resin, ABF (Ajinomoto Build-up Film), and glass epoxy (FR-4). Inorganic materials such as ceramic (e.g., Alumina) and glass are also used for specialized applications requiring high thermal stability or unique electrical properties. Flexible substrates are emerging for bendable electronics.

How do advanced packaging technologies impact the IC substrate market?

Advanced packaging technologies, such as system-in-package (SiP), chiplets, and 3D integration, significantly impact the IC substrate market by demanding substrates with higher density interconnects, superior electrical performance, and enhanced thermal dissipation capabilities. These technologies drive innovation in substrate design and materials to accommodate complex multi-chip integration.

What are the key drivers for the growth of the IC Substrate Market?

The key drivers for market growth include the increasing adoption of 5G technology, the proliferation of AI and High-Performance Computing (HPC), continuous advancements in automotive electronics (ADAS, EVs), ongoing miniaturization efforts in consumer electronics, and the general demand for more powerful and compact electronic devices across all sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted